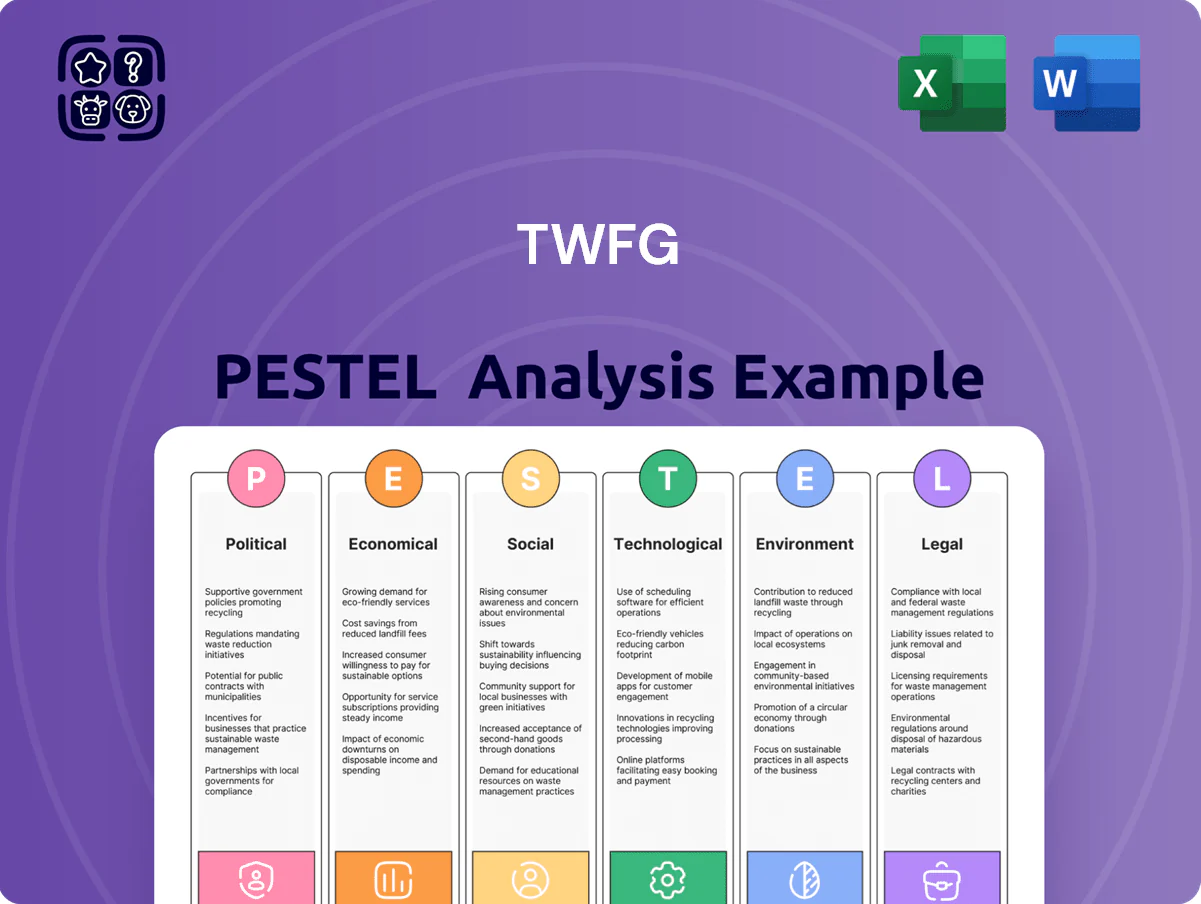

TWFG PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of TWFG—concise, research-backed insights that reveal how political, economic, social, technological, legal, and environmental forces will shape the company’s trajectory; buy the full report to get the complete, actionable breakdown in editable formats and use it to inform investments, strategy, or competitive planning.

Political factors

State insurance commission oversight

The regulatory landscape for TWFG is shaped by state insurance commissioners who control rate filings and licensing; Texas and Florida account for roughly 35% of TWFG’s premium volume, amplifying their impact.

As of December 2025, political pressure to cap premium increases led Texas and Florida regulators to deny or substantially reduce about 18% of filed rate hikes, raising scrutiny on carrier profitability.

TWFG must adapt distribution and carrier selection locally to keep insurers willing to write in high-risk zones where catastrophe exposure drove a 22% rise in claims severity across 2023–2025.

Federal tax policy and corporate rates

The 2024 election aftermath sharpened focus on corporate tax and pass-through deductions; proposals could raise C-corp rates from 21% toward 25% or limit Section 199A benefits, directly affecting TWFG independent agents operating as S-corps/LLCs. Changes to pass-through incentives would alter after-tax margins and constrain capital for branch expansion—TWFG notes a potential 5–12% hit to net agent earnings under modeled scenarios. The company actively monitors legislation to guide agents on tax-efficient growth and capital allocation strategies.

National Flood Insurance Program stability

Political debates over reauthorization and funding of the National Flood Insurance Program (NFIP) create uncertainty for personal lines agents; NFIP faced multiple short-term extensions in 2023–2025, contributing to transactional delays. Federal legislative gridlock can delay real estate closings, impacting TWFG clients who rely on timely flood coverage for mortgage requirements. TWFG offsets this risk by offering a diversified portfolio of private flood alternatives—private flood policies grew ~18% industrywide in 2024—ensuring deal continuity despite NFIP instability.

Trade policies and commercial liability

Ongoing changes to trade agreements and tariffs have raised input costs for TWFG commercial clients in manufacturing and logistics, with US tariffs on select imports contributing to a 5–8% rise in landed costs in 2024.

Heightened political tensions that disrupted supply chains in 2023–2024 increased demand for marine and cargo insurance by about 12% among mid-market firms.

TWFG strategists monitor geopolitics to recalibrate commercial risk advice and coverage recommendations for mid-market owners, citing a 2024 uptick in claims severity of roughly 9%.

- Tariff-driven landed cost increase 5–8% (2024)

- Marine/cargo insurance demand +12% (2023–24)

- Claims severity rise ~9% (2024)

Governmental healthcare mandates

The political debate over the Affordable Care Act and supplemental benefits remained active through end-2025, with proposed federal rule changes potentially affecting employer mandate thresholds and reporting requirements that impact TWFG’s life and health segments.

Federal adjustments to employer-sponsored coverage could change addressable market size; 2024 CMS data showed 156 million covered under employer plans, so even small mandate shifts materially affect broker volumes and premium flow for TWFG.

TWFG must update product offerings and compliance systems rapidly while preserving agent economics; maintaining commission margins near industry medians (around 10–15% for supplemental products in 2024–25) will be critical to retention and distribution.

- Active policy shifts through 2025 alter employer mandate scope and reporting

- 156 million covered by employer plans (CMS 2024) amplifies impact of changes

- Maintain agent commissions ~10–15% to protect distribution

- Requires rapid product and compliance updates to stay competitive

Insurer margins squeezed: rate cuts, higher catastrophe costs, tax and NFIP uncertainty

State insurance regulators (TX, FL ≈35% premium) tightened rate approvals—~18% of filings reduced/denied by Dec 2025—pressuring margins; catastrophe-driven claims severity rose 22% (2023–25). Federal tax proposals could raise C-corp to ~25% and cut pass-through benefits, risking a 5–12% drop in agent net earnings. NFIP uncertainty (multiple short extensions through 2025) boosted private flood market ~18% (2024). Commercial tariffs lifted landed costs 5–8% (2024), raising marine/cargo demand ~12% (2023–24).

| Metric | Value |

|---|---|

| TX+FL premium share | ≈35% |

| Rate filings reduced/denied (to Dec 2025) | ≈18% |

| Claims severity (2023–25) | +22% |

| Private flood growth (2024) | +18% |

| Landed cost impact (2024) | +5–8% |

| Marine/cargo demand (2023–24) | +12% |

| Potential C-corp rate (proposal) | ≈25% |

| Agent earnings risk (modeled) | -5–12% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact TWFG, with data-backed trends and region-specific examples to reveal risks and opportunities for executives, investors, and strategists.

Condenses TWFG’s full PESTLE into a crisp summary for quick reference in meetings or presentations, using clear language and visual segmentation so teams can rapidly assess external risks and align on strategy.

Economic factors

Interest rate environment and investment income

Federal Reserve hikes in 2025 raised the policy rate to about 5.25% by mid-year, boosting insurers’ investment yields on float and supporting narrower loss-adjusted pricing for TWFG-distributed products.

Higher yields improved portfolio returns—US life & P/C insurer net investment income rose ~12% YoY in 2024–25—enabling competitive premiums through carriers TWFG represents.

However, mortgage rates near 7% cooled housing starts and existing home sales down ~10% YoY in 2025, likely reducing new homeowners policies sourced by TWFG’s agency network.

Inflationary pressure on claim costs

Persistent inflation in building materials (lumber up ~20% in 2024 vs 2021) and automotive parts (+15% YoY in 2024) has increased average claim severity, pushing US P&C loss costs up ~12% in 2023–24; carriers raised premiums accordingly.

Hard market conditions in property lines

By end-2025 the property insurance market remains hard with industry combined ratios near 103% and capacity down roughly 15% year-over-year; tight underwriting and rate increases (average homeowners rate up ~12% in 2024–25) favor TWFG’s independent broker model that can access 50+ carriers to place difficult risks. Agents face higher placement effort and longer bind times, especially for clients in catastrophe zones where reinsurance costs surged >20% in 2024.

Consumer disposable income levels

The U.S. real disposable personal income rose 1.8% year-over-year in Q4 2025, influencing demand for umbrella policies and high-value floaters as higher income supports premium customers who prioritize comprehensive protection.

TWFG monitors regional GDP and household income trends—areas with median household incomes above the national $76,000 (2024) are targeted for growth in affluent segments.

A 10-point drop in consumer confidence (Conference Board) typically correlates with clients tightening coverage—raising deductibles or lowering limits to reduce premiums.

- Q4 2025 real disposable income +1.8% YoY

- National median household income $76,000 (2024)

- 10-point confidence drop → higher deductibles/lower limits

Consolidation in the brokerage industry

Consolidation in the brokerage industry accelerated through 2025, with private equity deals totaling an estimated $18.7 billion in agency acquisitions in 2024–25, intensifying competition for talent and portfolios against well-funded consolidators targeting independents.

As a large national player, TWFG faces higher acquisition and retention costs; competing requires offering autonomy plus national-scale benefits to attract agents reluctant to sell outright.

Key points:

- PE agency deal value ~ $18.7B (2024–25)

- Increased bidding drives up acquisition premiums and agent compensation

- TWFG must emphasize autonomy + scale to win independents

Higher rates lift insurer income; costs, housing slump and PE deals squeeze agencies

Elevated rates (Fed ~5.25% by mid-2025) boosted insurer investment income (+~12% YoY 2024–25) supporting tighter pricing; higher mortgage rates (~7%) cut housing activity ~10% YoY reducing new-home policies; material/parts inflation raised P&C loss costs ~12% (2023–24) and homeowners rates +~12% (2024–25); PE agency deals ~$18.7B (2024–25)increase acquisition costs for TWFG.

| Metric | Value |

|---|---|

| Fed rate mid-2025 | ~5.25% |

| Insurer NII change | +~12% YoY |

| Housing activity | -~10% YoY |

| P&C loss cost | +~12% |

| PE agency deals | $18.7B |

Preview Before You Purchase

TWFG PESTLE Analysis

The preview shown here is the exact TWFG PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders or teasers—this is the real, final file you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of TWFG—concise, research-backed insights that reveal how political, economic, social, technological, legal, and environmental forces will shape the company’s trajectory; buy the full report to get the complete, actionable breakdown in editable formats and use it to inform investments, strategy, or competitive planning.

Political factors

State insurance commission oversight

The regulatory landscape for TWFG is shaped by state insurance commissioners who control rate filings and licensing; Texas and Florida account for roughly 35% of TWFG’s premium volume, amplifying their impact.

As of December 2025, political pressure to cap premium increases led Texas and Florida regulators to deny or substantially reduce about 18% of filed rate hikes, raising scrutiny on carrier profitability.

TWFG must adapt distribution and carrier selection locally to keep insurers willing to write in high-risk zones where catastrophe exposure drove a 22% rise in claims severity across 2023–2025.

Federal tax policy and corporate rates

The 2024 election aftermath sharpened focus on corporate tax and pass-through deductions; proposals could raise C-corp rates from 21% toward 25% or limit Section 199A benefits, directly affecting TWFG independent agents operating as S-corps/LLCs. Changes to pass-through incentives would alter after-tax margins and constrain capital for branch expansion—TWFG notes a potential 5–12% hit to net agent earnings under modeled scenarios. The company actively monitors legislation to guide agents on tax-efficient growth and capital allocation strategies.

National Flood Insurance Program stability

Political debates over reauthorization and funding of the National Flood Insurance Program (NFIP) create uncertainty for personal lines agents; NFIP faced multiple short-term extensions in 2023–2025, contributing to transactional delays. Federal legislative gridlock can delay real estate closings, impacting TWFG clients who rely on timely flood coverage for mortgage requirements. TWFG offsets this risk by offering a diversified portfolio of private flood alternatives—private flood policies grew ~18% industrywide in 2024—ensuring deal continuity despite NFIP instability.

Trade policies and commercial liability

Ongoing changes to trade agreements and tariffs have raised input costs for TWFG commercial clients in manufacturing and logistics, with US tariffs on select imports contributing to a 5–8% rise in landed costs in 2024.

Heightened political tensions that disrupted supply chains in 2023–2024 increased demand for marine and cargo insurance by about 12% among mid-market firms.

TWFG strategists monitor geopolitics to recalibrate commercial risk advice and coverage recommendations for mid-market owners, citing a 2024 uptick in claims severity of roughly 9%.

- Tariff-driven landed cost increase 5–8% (2024)

- Marine/cargo insurance demand +12% (2023–24)

- Claims severity rise ~9% (2024)

Governmental healthcare mandates

The political debate over the Affordable Care Act and supplemental benefits remained active through end-2025, with proposed federal rule changes potentially affecting employer mandate thresholds and reporting requirements that impact TWFG’s life and health segments.

Federal adjustments to employer-sponsored coverage could change addressable market size; 2024 CMS data showed 156 million covered under employer plans, so even small mandate shifts materially affect broker volumes and premium flow for TWFG.

TWFG must update product offerings and compliance systems rapidly while preserving agent economics; maintaining commission margins near industry medians (around 10–15% for supplemental products in 2024–25) will be critical to retention and distribution.

- Active policy shifts through 2025 alter employer mandate scope and reporting

- 156 million covered by employer plans (CMS 2024) amplifies impact of changes

- Maintain agent commissions ~10–15% to protect distribution

- Requires rapid product and compliance updates to stay competitive

Insurer margins squeezed: rate cuts, higher catastrophe costs, tax and NFIP uncertainty

State insurance regulators (TX, FL ≈35% premium) tightened rate approvals—~18% of filings reduced/denied by Dec 2025—pressuring margins; catastrophe-driven claims severity rose 22% (2023–25). Federal tax proposals could raise C-corp to ~25% and cut pass-through benefits, risking a 5–12% drop in agent net earnings. NFIP uncertainty (multiple short extensions through 2025) boosted private flood market ~18% (2024). Commercial tariffs lifted landed costs 5–8% (2024), raising marine/cargo demand ~12% (2023–24).

| Metric | Value |

|---|---|

| TX+FL premium share | ≈35% |

| Rate filings reduced/denied (to Dec 2025) | ≈18% |

| Claims severity (2023–25) | +22% |

| Private flood growth (2024) | +18% |

| Landed cost impact (2024) | +5–8% |

| Marine/cargo demand (2023–24) | +12% |

| Potential C-corp rate (proposal) | ≈25% |

| Agent earnings risk (modeled) | -5–12% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact TWFG, with data-backed trends and region-specific examples to reveal risks and opportunities for executives, investors, and strategists.

Condenses TWFG’s full PESTLE into a crisp summary for quick reference in meetings or presentations, using clear language and visual segmentation so teams can rapidly assess external risks and align on strategy.

Economic factors

Interest rate environment and investment income

Federal Reserve hikes in 2025 raised the policy rate to about 5.25% by mid-year, boosting insurers’ investment yields on float and supporting narrower loss-adjusted pricing for TWFG-distributed products.

Higher yields improved portfolio returns—US life & P/C insurer net investment income rose ~12% YoY in 2024–25—enabling competitive premiums through carriers TWFG represents.

However, mortgage rates near 7% cooled housing starts and existing home sales down ~10% YoY in 2025, likely reducing new homeowners policies sourced by TWFG’s agency network.

Inflationary pressure on claim costs

Persistent inflation in building materials (lumber up ~20% in 2024 vs 2021) and automotive parts (+15% YoY in 2024) has increased average claim severity, pushing US P&C loss costs up ~12% in 2023–24; carriers raised premiums accordingly.

Hard market conditions in property lines

By end-2025 the property insurance market remains hard with industry combined ratios near 103% and capacity down roughly 15% year-over-year; tight underwriting and rate increases (average homeowners rate up ~12% in 2024–25) favor TWFG’s independent broker model that can access 50+ carriers to place difficult risks. Agents face higher placement effort and longer bind times, especially for clients in catastrophe zones where reinsurance costs surged >20% in 2024.

Consumer disposable income levels

The U.S. real disposable personal income rose 1.8% year-over-year in Q4 2025, influencing demand for umbrella policies and high-value floaters as higher income supports premium customers who prioritize comprehensive protection.

TWFG monitors regional GDP and household income trends—areas with median household incomes above the national $76,000 (2024) are targeted for growth in affluent segments.

A 10-point drop in consumer confidence (Conference Board) typically correlates with clients tightening coverage—raising deductibles or lowering limits to reduce premiums.

- Q4 2025 real disposable income +1.8% YoY

- National median household income $76,000 (2024)

- 10-point confidence drop → higher deductibles/lower limits

Consolidation in the brokerage industry

Consolidation in the brokerage industry accelerated through 2025, with private equity deals totaling an estimated $18.7 billion in agency acquisitions in 2024–25, intensifying competition for talent and portfolios against well-funded consolidators targeting independents.

As a large national player, TWFG faces higher acquisition and retention costs; competing requires offering autonomy plus national-scale benefits to attract agents reluctant to sell outright.

Key points:

- PE agency deal value ~ $18.7B (2024–25)

- Increased bidding drives up acquisition premiums and agent compensation

- TWFG must emphasize autonomy + scale to win independents

Higher rates lift insurer income; costs, housing slump and PE deals squeeze agencies

Elevated rates (Fed ~5.25% by mid-2025) boosted insurer investment income (+~12% YoY 2024–25) supporting tighter pricing; higher mortgage rates (~7%) cut housing activity ~10% YoY reducing new-home policies; material/parts inflation raised P&C loss costs ~12% (2023–24) and homeowners rates +~12% (2024–25); PE agency deals ~$18.7B (2024–25)increase acquisition costs for TWFG.

| Metric | Value |

|---|---|

| Fed rate mid-2025 | ~5.25% |

| Insurer NII change | +~12% YoY |

| Housing activity | -~10% YoY |

| P&C loss cost | +~12% |

| PE agency deals | $18.7B |

Preview Before You Purchase

TWFG PESTLE Analysis

The preview shown here is the exact TWFG PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders or teasers—this is the real, final file you’ll own upon checkout.