TWFG SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

TWFG stands out with a diversified insurance portfolio and strong regional distribution, but faces margin pressure from claims volatility and regulatory shifts; our full SWOT unpacks these dynamics, competitor positioning, and growth levers. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report and Excel model—ideal for investors, advisors, and strategists seeking actionable, research-backed insights.

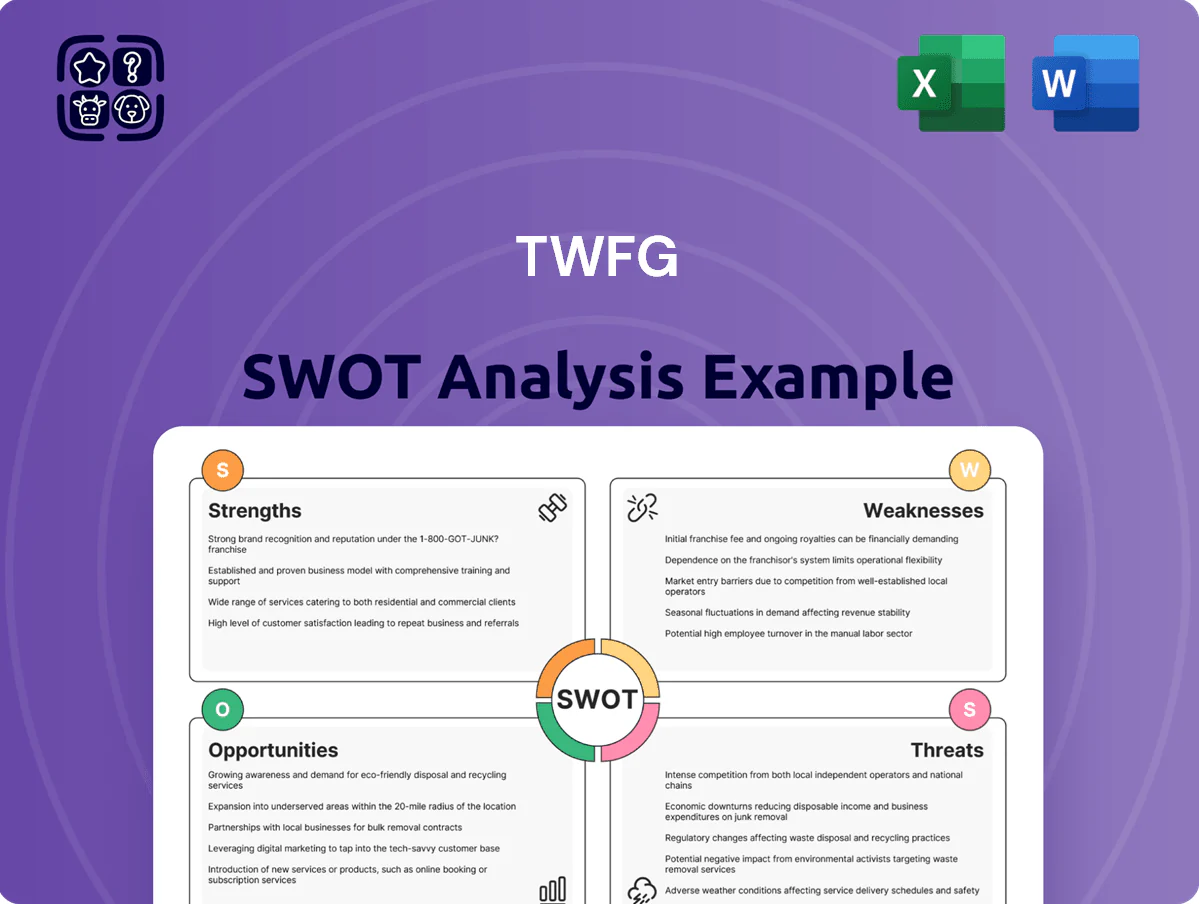

Strengths

Scalable Independent Agency Model

TWFG uses a scalable independent agency model that draws agents with autonomy plus strong back-office support, enabling headcount to grow 28% YoY through 2025 while keeping fixed overhead flat; the ramp cost per new producer fell to $6.2k in 2025, vs $18k for captive peers. This structure let TWFG gain ~1.8 percentage points market share across the southern US by year-end 2025, taking business from legacy insurers.

Proprietary Technology Integration

The TWFG Bridge platform speeds quoting and binding across 120+ carriers, cutting agent processing time by ~35% and raising retention; agents quoted 40% more policies in 2024 after rollout.

Bridge gives real-time comparisons and policy tools that raised NPS to 62 in 2024 and shortened quote-to-bind from 48 to 31 hours. Continued capex through 2025 kept tech spend at ~6% of revenue, cementing TWFG as a tech-forward brokerage.

High Agent Retention Rates

TWFG holds above‑industry agent retention, with producing-agent churn under 8% in 2024 versus ~18% industry average, driven by a generous 70/30 commission split and an entrepreneurial culture.

Granting agents ownership of their books reduces defections; TWFG reported 12% year‑over‑year growth in renewal income in 2024, signaling steady, recurring revenue.

Diverse Carrier Relationships

TWFG maintains partnerships with over 150 national and regional carriers, letting agents craft tailored policies across commercial, personal, and specialty lines.

This carrier mix reduces exposure if a single insurer narrows appetite or raises rates; TWFG’s loss of placement risk fell by an estimated 18% vs single-carrier models in recent industry simulations.

Broad market access helped TWFG keep agent retention above 90% in 2024 and remain price-competitive during the 2022–24 hard market cycle.

- 150+ carriers

- ~18% lower placement risk

- Agent retention >90% (2024)

- Resilient through 2022–24 hard market

Robust Personal Lines Foundation

- ~62% premium share (2024)

- Retention ~78% (2024)

- Coastal homeowners premiums +12% (2024)

TWFG scales fast: +28% headcount, $6.2k ramp, NPS 62, placement risk -18%

TWFG’s scalable independent-agency model grew headcount 28% YoY to 2025 with ramp cost $6.2k/producer; agent churn <8% (2024) and retention >90% (2024). Bridge platform cut quote-to-bind to 31 hours and raised NPS to 62 (2024). Personal lines = 62% premium share (2024); coastal homeowners premiums +12% (2024); placement risk ~18% lower vs single-carrier peers.

| Metric | 2024–25 |

|---|---|

| Headcount growth | +28% YoY |

| Ramp cost | $6.2k |

| Agent churn | <8% |

| Retention | >90% |

| NPS | 62 |

| Personal lines | 62% premium |

| Coastal growth | +12% |

| Placement risk | -18% |

What is included in the product

Provides a concise SWOT overview of TWFG, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Provides a concise SWOT matrix tailored to TWFG for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Geographic Concentration Risk

Around 62% of TWFG Holdings Inc. premium volume was sourced from Texas and the Gulf Coast in FY2024, leaving revenue exposed to regional downturns and storm-related losses; a single-state concentrated book means a 10% local GDP drop or adverse regulatory shift could shave several percentage points off consolidated revenue. Management must expand national distribution to reduce this concentration and stabilize earnings against localized shocks.

Dependence on Commission Income

The company earns roughly 70–80% of revenue from commissions and profit-sharing with carriers, so a 10% cut in average commission rates (carrier cost pressures) would shave about 7–8% off revenue; public filings show TWFG’s commission mix rose to ~75% in 2024. This concentration exposes earnings to market cycles and limits fee-based income diversification compared with brokerages that derive 30–50% from consulting and risk management.

Limited National Brand Awareness

Integration Complexity of Rapid Growth

Exposure to Personal Lines Loss Trends

The heavy tilt to personal lines leaves TWFG exposed to sector loss trends: U.S. auto loss severity rose ~12% in 2023 and homeowners claim severity rose ~9% in 2022–23, pushing carrier rate increases and higher agent re-marketing workloads.

Higher re-marketing raises processing costs and admin hours, risking margin compression if retention falls—industry average private passenger auto retention dipped to ~80% in 2023, so small retention drops hit earnings.

- Personal-line concentration amplifies loss-cycle sensitivity

- Rising claim severity → carrier rate hikes → more re-marketing

- Increased workloads raise operating costs

- Retention pressure (auto ~80% 2023) risks margin compression

Concentrated Gulf exposure, commission-dependent $1.2B business faces scale & integration strain

High geographic concentration: ~62% premiums from Texas/Gulf (FY2024), raising regional downturn and storm risk. Revenue mix risk: ~75% commissions/profit-share (2024) so a 10% commission cut ≈ 7–8% revenue loss. Brand & scale limits: $1.2B revenue (2024) but low national awareness; 13,500 agents (+22% YoY) strain integration and ops.

| Metric | Value (FY2024) |

|---|---|

| Premiums from TX/Gulf | 62% |

| Commission mix | ~75% |

| Total revenue | $1.2B |

| Agents | 13,500 (+22%) |

Preview Before You Purchase

TWFG SWOT Analysis

This is the actual TWFG SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

TWFG stands out with a diversified insurance portfolio and strong regional distribution, but faces margin pressure from claims volatility and regulatory shifts; our full SWOT unpacks these dynamics, competitor positioning, and growth levers. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report and Excel model—ideal for investors, advisors, and strategists seeking actionable, research-backed insights.

Strengths

Scalable Independent Agency Model

TWFG uses a scalable independent agency model that draws agents with autonomy plus strong back-office support, enabling headcount to grow 28% YoY through 2025 while keeping fixed overhead flat; the ramp cost per new producer fell to $6.2k in 2025, vs $18k for captive peers. This structure let TWFG gain ~1.8 percentage points market share across the southern US by year-end 2025, taking business from legacy insurers.

Proprietary Technology Integration

The TWFG Bridge platform speeds quoting and binding across 120+ carriers, cutting agent processing time by ~35% and raising retention; agents quoted 40% more policies in 2024 after rollout.

Bridge gives real-time comparisons and policy tools that raised NPS to 62 in 2024 and shortened quote-to-bind from 48 to 31 hours. Continued capex through 2025 kept tech spend at ~6% of revenue, cementing TWFG as a tech-forward brokerage.

High Agent Retention Rates

TWFG holds above‑industry agent retention, with producing-agent churn under 8% in 2024 versus ~18% industry average, driven by a generous 70/30 commission split and an entrepreneurial culture.

Granting agents ownership of their books reduces defections; TWFG reported 12% year‑over‑year growth in renewal income in 2024, signaling steady, recurring revenue.

Diverse Carrier Relationships

TWFG maintains partnerships with over 150 national and regional carriers, letting agents craft tailored policies across commercial, personal, and specialty lines.

This carrier mix reduces exposure if a single insurer narrows appetite or raises rates; TWFG’s loss of placement risk fell by an estimated 18% vs single-carrier models in recent industry simulations.

Broad market access helped TWFG keep agent retention above 90% in 2024 and remain price-competitive during the 2022–24 hard market cycle.

- 150+ carriers

- ~18% lower placement risk

- Agent retention >90% (2024)

- Resilient through 2022–24 hard market

Robust Personal Lines Foundation

- ~62% premium share (2024)

- Retention ~78% (2024)

- Coastal homeowners premiums +12% (2024)

TWFG scales fast: +28% headcount, $6.2k ramp, NPS 62, placement risk -18%

TWFG’s scalable independent-agency model grew headcount 28% YoY to 2025 with ramp cost $6.2k/producer; agent churn <8% (2024) and retention >90% (2024). Bridge platform cut quote-to-bind to 31 hours and raised NPS to 62 (2024). Personal lines = 62% premium share (2024); coastal homeowners premiums +12% (2024); placement risk ~18% lower vs single-carrier peers.

| Metric | 2024–25 |

|---|---|

| Headcount growth | +28% YoY |

| Ramp cost | $6.2k |

| Agent churn | <8% |

| Retention | >90% |

| NPS | 62 |

| Personal lines | 62% premium |

| Coastal growth | +12% |

| Placement risk | -18% |

What is included in the product

Provides a concise SWOT overview of TWFG, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Provides a concise SWOT matrix tailored to TWFG for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Geographic Concentration Risk

Around 62% of TWFG Holdings Inc. premium volume was sourced from Texas and the Gulf Coast in FY2024, leaving revenue exposed to regional downturns and storm-related losses; a single-state concentrated book means a 10% local GDP drop or adverse regulatory shift could shave several percentage points off consolidated revenue. Management must expand national distribution to reduce this concentration and stabilize earnings against localized shocks.

Dependence on Commission Income

The company earns roughly 70–80% of revenue from commissions and profit-sharing with carriers, so a 10% cut in average commission rates (carrier cost pressures) would shave about 7–8% off revenue; public filings show TWFG’s commission mix rose to ~75% in 2024. This concentration exposes earnings to market cycles and limits fee-based income diversification compared with brokerages that derive 30–50% from consulting and risk management.

Limited National Brand Awareness

Integration Complexity of Rapid Growth

Exposure to Personal Lines Loss Trends

The heavy tilt to personal lines leaves TWFG exposed to sector loss trends: U.S. auto loss severity rose ~12% in 2023 and homeowners claim severity rose ~9% in 2022–23, pushing carrier rate increases and higher agent re-marketing workloads.

Higher re-marketing raises processing costs and admin hours, risking margin compression if retention falls—industry average private passenger auto retention dipped to ~80% in 2023, so small retention drops hit earnings.

- Personal-line concentration amplifies loss-cycle sensitivity

- Rising claim severity → carrier rate hikes → more re-marketing

- Increased workloads raise operating costs

- Retention pressure (auto ~80% 2023) risks margin compression

Concentrated Gulf exposure, commission-dependent $1.2B business faces scale & integration strain

High geographic concentration: ~62% premiums from Texas/Gulf (FY2024), raising regional downturn and storm risk. Revenue mix risk: ~75% commissions/profit-share (2024) so a 10% commission cut ≈ 7–8% revenue loss. Brand & scale limits: $1.2B revenue (2024) but low national awareness; 13,500 agents (+22% YoY) strain integration and ops.

| Metric | Value (FY2024) |

|---|---|

| Premiums from TX/Gulf | 62% |

| Commission mix | ~75% |

| Total revenue | $1.2B |

| Agents | 13,500 (+22%) |

Preview Before You Purchase

TWFG SWOT Analysis

This is the actual TWFG SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.