United Bank for Africa Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

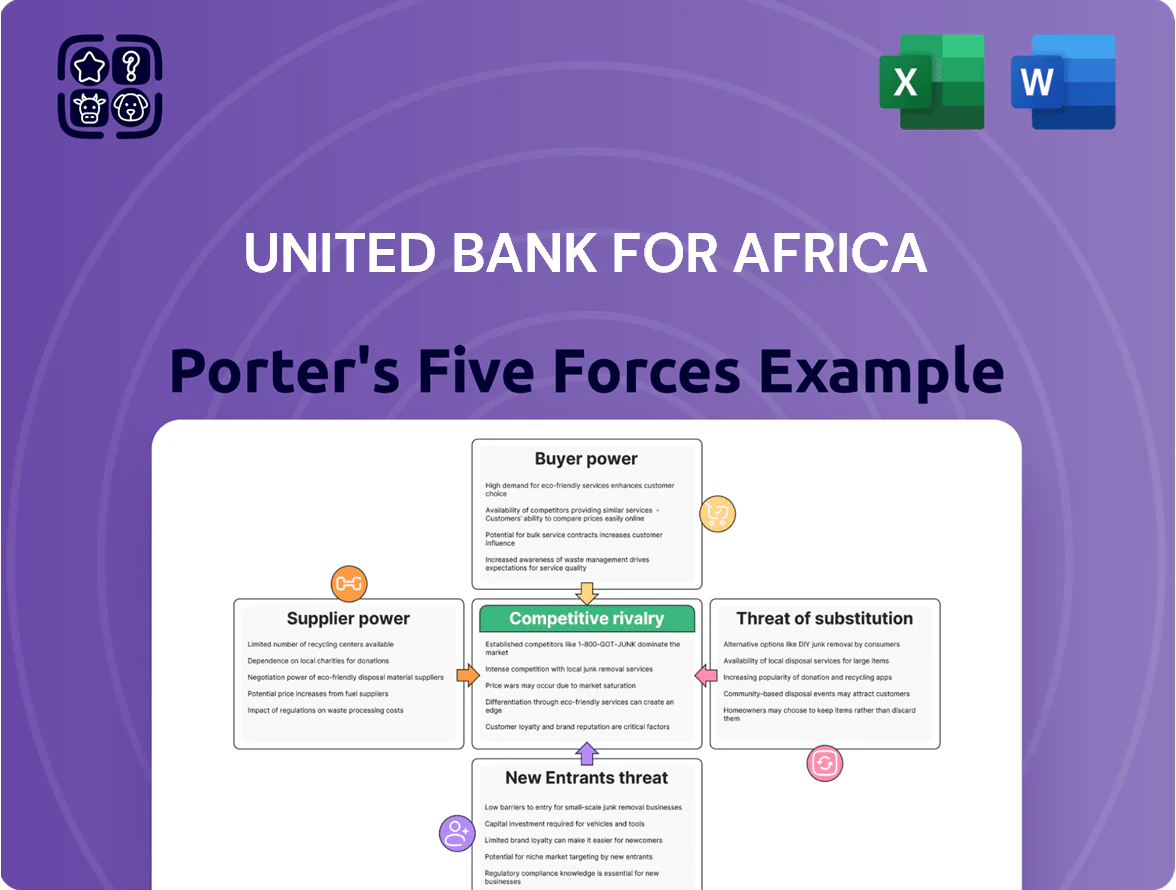

Suppliers Bargaining Power

Concentration of low-cost retail deposits

Retail depositors are UBA’s primary capital suppliers, but bargaining power stays low because individual savers are fragmented; by end-2025 UBA held roughly 62% of deposits in current and savings accounts across its 1,200+ branches and digital channels. This high share of low-cost retail deposits reduced UBA’s cost of funds to about 3.1% in 2025, versus 4.5% for institutional funding. The retail-heavy mix gives UBA a stable funding base less sensitive to rate swings, supporting net interest margins and lending capacity.

Dependency on global technology and core banking providers

The bargaining power of technology suppliers is high because UBA depends on specialized global vendors for core banking and digital platforms; estimated vendor-driven IT spend was about 12–15% of UBA’s 2024 operating expenses (UBA FY2024 report) which underscores dependency.

High switching costs and mission‑critical software give vendors leverage over pricing and SLAs; a single major outage can hit revenue and reputation—Pan‑African outage surveys show average bank downtime costs ~$250k–$1M per hour.

As UBA pushes digital transformation through 2025, managing vendor contracts, enforcing uptime guarantees, and negotiating capex vs opex are vital to control costs and cybersecurity risk.

Influence of skilled financial and tech talent

The limited pool of bankers, data analysts, and cybersecurity experts across UBA’s 20+ African markets increases supplier (talent) bargaining power, pushing salary premiums; for example, cybersecurity salaries rose ~18% in Nigeria 2023–2024. Competition from banks and fintechs has lifted hiring costs and turnover risk, prompting UBA to expand its UBA Academy and pay market-leading packages—personnel expense increased 12.5% in FY2024 to shore retention.

Regulatory requirements and central bank mandates

Central banks and regulators act as non-market suppliers of UBA’s operating rules and liquidity, with absolute power over reserve ratios, interest-rate corridors, and capital adequacy that squeeze margins and funding costs.

In 2025 UBA adjusted to tighter macro‑prudential rules across 20 African subsidiaries; a 100–200bps rise in reserve requirements in key markets cut group liquidity by an estimated $350m and raised funding costs ~40bps.

- Absolute regulatory power: reserve, corridor, capital rules

- 20 African subsidiaries subject to evolving 2025 policies

- Estimated $350m liquidity impact from reserve hikes

- Funding costs up ~40bps where requirements tightened

Access to international wholesale and debt markets

For foreign-currency needs and long-term projects, United Bank for Africa (UBA) taps international development finance institutions and global bond markets, giving these suppliers moderate bargaining power tied to UBA’s credit ratings and regional macro stability.

UBA’s successful $750m Eurobond in October 2025 and $500m multilateral credit lines in Q4 2025 show a balanced supplier relationship—suppliers supply large liquidity but need UBA’s African footprint.

Supply power rises if Nigerian macro risks or rating downgrades increase, and falls as UBA improves metrics like CET1 and external reserves.

- October 2025: $750m Eurobond issued

- Q4 2025: $500m multilateral lines

- Supplier power = moderate; tied to ratings, macro stability

Mixed supplier power: cheap retail funding vs costly tech, rising talent & regulator control

Suppliers’ bargaining power is mixed: retail depositors low-power (62% CASA, cost of funds ~3.1% in 2025), tech vendors high-power (IT ~12–15% opex; outage cost $250k–$1M/hr), talent power rising (cybersecurity pay +18% Nigeria 2023–24; personnel expense +12.5% FY2024), regulators absolute power (reserve hikes cost ~$350m liquidity, +40bps funding), and international lenders moderate (Oct 2025 $750m Eurobond; Q4 2025 $500m lines).

| Supplier | Key metric |

|---|---|

| Retail deposits | 62% CASA; CoF 3.1% (2025) |

| Tech vendors | IT 12–15% opex; outage $250k–$1M/hr |

| Regulators | $350m liquidity; +40bps funding |

| Intl lenders | $750m Eurobond; $500m lines (Oct–Q4 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for United Bank for Africa, uncovering competitive drivers, customer bargaining power, supplier influence, threat of entrants and substitutes, and highlighting emerging disruptions and strategic defenses to protect market share.

A concise Porter's Five Forces snapshot for United Bank for Africa—distills competitive pressures into a single page for rapid strategic decisions.

Customers Bargaining Power

Low switching costs for retail and SME clients

Retail and SME customers face low switching costs as digital onboarding and mobile apps let them open accounts in minutes, and 78% of Nigerian bank customers used mobile banking in 2024, raising their bargaining power over fees and rates. As of 2025, real-time price comparison tools and interbank rate transparency mean consumers can shift deposits for a 20–50 bps difference. UBA responds by improving CX, personalizing offers, and expanding loyalty programs—its 2024 customer retention rose 3.2 percentage points after these initiatives.

Negotiating leverage of large corporate and institutional clients

Corporate and government clients—about 22% of UBA Group’s 2024 deposits (NGN equivalent)—wield strong bargaining power due to large transaction volumes and deposit balances.

They press for bespoke products, lower lending spreads and dedicated RM teams; UBA reports tailored-transaction income rising 14% y/y in 2024, reflecting these demands.

UBA’s pan‑African network across 20 countries and 2024 cross‑border remittances of $2.1bn help retain these clients versus local banks.

Increased price sensitivity in a high-inflation environment

Persistent inflation across several African markets in 2025—Nigeria CPI ~33.2% YoY (Jan 2025), Ghana ~44% YoY (2024 avg)—has raised customer sensitivity to fees and interest spreads, pushing retail clients to prioritize low-cost providers for payments and credit.

That bargaining power forces banks to cut visible transaction costs; surveys show 42% of consumers switch banks for cheaper fees in 2024–25.

UBA responded by shifting 58% of volume to its digital channels in 2024, lowering per-transaction costs and preserving net interest margins via higher scale and cost-to-income improvements.

Access to information and financial literacy

The rise of digital transparency and improved financial literacy has let UBA customers compare rates and products; a 2024 Statista survey showed 58% of Nigerian retail customers research rates online before choosing a bank.

Clients now challenge hidden fees and demand higher yields on fixed-income products, pushing UBA to cut opaque charges—UBA reported a 12% reduction in fee-related complaints in 2024.

UBA responds with transparent pricing and advisory via its UBA Mobile app (12.5m downloads by 2024) and branch advisers, boosting informed product uptake.

- 58% research rates online (2024)

- 12% drop in fee complaints (UBA, 2024)

- 12.5m UBA Mobile downloads (2024)

Alternative options through fintech and neobanks

The rise of fintechs and neobanks offering niche payments and micro‑lending alternatives raised Kenyan and Nigerian customer churn risk; UBA saw digital customer growth pressure in 2024 as mobile-active users across Nigerian banks rose 18% year-on-year to ~32m (CBN/industry reports).

To hold tech-savvy 2025 customers, UBA embeds fintech-like agility into its UBA Digital platform, speeding product launches and partnering with startups to cut time-to-market and limit migration.

High customer leverage forces UBA to cut fees, boost personalization and digital push

Customers hold moderate-to-strong bargaining power: retail switching costs are low (78% mobile banking use in 2024) while corporates drive ~22% of deposits (2024), forcing UBA to cut fees, personalize offers and expand digital channels (UBA Mobile 12.5m downloads, 58% digital volume). Inflation (Nigeria CPI ~33.2% Jan 2025) and fintech competition raise fee sensitivity and churn risk.

| Metric | Value |

|---|---|

| Mobile banking use (Nigeria, 2024) | 78% |

| Corporate share of deposits (UBA, 2024) | 22% |

| UBA Mobile downloads (2024) | 12.5m |

| Nigeria CPI (Jan 2025) | 33.2% YoY |

Same Document Delivered

United Bank for Africa Porter's Five Forces Analysis

This preview shows the exact United Bank for Africa Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, fully formatted and ready for use.

The document displayed here is the same professionally written analysis included in the full version—available for instant download the moment you buy.

No mockups or samples: this is the final deliverable, complete and ready to inform your strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Suppliers Bargaining Power

Concentration of low-cost retail deposits

Retail depositors are UBA’s primary capital suppliers, but bargaining power stays low because individual savers are fragmented; by end-2025 UBA held roughly 62% of deposits in current and savings accounts across its 1,200+ branches and digital channels. This high share of low-cost retail deposits reduced UBA’s cost of funds to about 3.1% in 2025, versus 4.5% for institutional funding. The retail-heavy mix gives UBA a stable funding base less sensitive to rate swings, supporting net interest margins and lending capacity.

Dependency on global technology and core banking providers

The bargaining power of technology suppliers is high because UBA depends on specialized global vendors for core banking and digital platforms; estimated vendor-driven IT spend was about 12–15% of UBA’s 2024 operating expenses (UBA FY2024 report) which underscores dependency.

High switching costs and mission‑critical software give vendors leverage over pricing and SLAs; a single major outage can hit revenue and reputation—Pan‑African outage surveys show average bank downtime costs ~$250k–$1M per hour.

As UBA pushes digital transformation through 2025, managing vendor contracts, enforcing uptime guarantees, and negotiating capex vs opex are vital to control costs and cybersecurity risk.

Influence of skilled financial and tech talent

The limited pool of bankers, data analysts, and cybersecurity experts across UBA’s 20+ African markets increases supplier (talent) bargaining power, pushing salary premiums; for example, cybersecurity salaries rose ~18% in Nigeria 2023–2024. Competition from banks and fintechs has lifted hiring costs and turnover risk, prompting UBA to expand its UBA Academy and pay market-leading packages—personnel expense increased 12.5% in FY2024 to shore retention.

Regulatory requirements and central bank mandates

Central banks and regulators act as non-market suppliers of UBA’s operating rules and liquidity, with absolute power over reserve ratios, interest-rate corridors, and capital adequacy that squeeze margins and funding costs.

In 2025 UBA adjusted to tighter macro‑prudential rules across 20 African subsidiaries; a 100–200bps rise in reserve requirements in key markets cut group liquidity by an estimated $350m and raised funding costs ~40bps.

- Absolute regulatory power: reserve, corridor, capital rules

- 20 African subsidiaries subject to evolving 2025 policies

- Estimated $350m liquidity impact from reserve hikes

- Funding costs up ~40bps where requirements tightened

Access to international wholesale and debt markets

For foreign-currency needs and long-term projects, United Bank for Africa (UBA) taps international development finance institutions and global bond markets, giving these suppliers moderate bargaining power tied to UBA’s credit ratings and regional macro stability.

UBA’s successful $750m Eurobond in October 2025 and $500m multilateral credit lines in Q4 2025 show a balanced supplier relationship—suppliers supply large liquidity but need UBA’s African footprint.

Supply power rises if Nigerian macro risks or rating downgrades increase, and falls as UBA improves metrics like CET1 and external reserves.

- October 2025: $750m Eurobond issued

- Q4 2025: $500m multilateral lines

- Supplier power = moderate; tied to ratings, macro stability

Mixed supplier power: cheap retail funding vs costly tech, rising talent & regulator control

Suppliers’ bargaining power is mixed: retail depositors low-power (62% CASA, cost of funds ~3.1% in 2025), tech vendors high-power (IT ~12–15% opex; outage cost $250k–$1M/hr), talent power rising (cybersecurity pay +18% Nigeria 2023–24; personnel expense +12.5% FY2024), regulators absolute power (reserve hikes cost ~$350m liquidity, +40bps funding), and international lenders moderate (Oct 2025 $750m Eurobond; Q4 2025 $500m lines).

| Supplier | Key metric |

|---|---|

| Retail deposits | 62% CASA; CoF 3.1% (2025) |

| Tech vendors | IT 12–15% opex; outage $250k–$1M/hr |

| Regulators | $350m liquidity; +40bps funding |

| Intl lenders | $750m Eurobond; $500m lines (Oct–Q4 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for United Bank for Africa, uncovering competitive drivers, customer bargaining power, supplier influence, threat of entrants and substitutes, and highlighting emerging disruptions and strategic defenses to protect market share.

A concise Porter's Five Forces snapshot for United Bank for Africa—distills competitive pressures into a single page for rapid strategic decisions.

Customers Bargaining Power

Low switching costs for retail and SME clients

Retail and SME customers face low switching costs as digital onboarding and mobile apps let them open accounts in minutes, and 78% of Nigerian bank customers used mobile banking in 2024, raising their bargaining power over fees and rates. As of 2025, real-time price comparison tools and interbank rate transparency mean consumers can shift deposits for a 20–50 bps difference. UBA responds by improving CX, personalizing offers, and expanding loyalty programs—its 2024 customer retention rose 3.2 percentage points after these initiatives.

Negotiating leverage of large corporate and institutional clients

Corporate and government clients—about 22% of UBA Group’s 2024 deposits (NGN equivalent)—wield strong bargaining power due to large transaction volumes and deposit balances.

They press for bespoke products, lower lending spreads and dedicated RM teams; UBA reports tailored-transaction income rising 14% y/y in 2024, reflecting these demands.

UBA’s pan‑African network across 20 countries and 2024 cross‑border remittances of $2.1bn help retain these clients versus local banks.

Increased price sensitivity in a high-inflation environment

Persistent inflation across several African markets in 2025—Nigeria CPI ~33.2% YoY (Jan 2025), Ghana ~44% YoY (2024 avg)—has raised customer sensitivity to fees and interest spreads, pushing retail clients to prioritize low-cost providers for payments and credit.

That bargaining power forces banks to cut visible transaction costs; surveys show 42% of consumers switch banks for cheaper fees in 2024–25.

UBA responded by shifting 58% of volume to its digital channels in 2024, lowering per-transaction costs and preserving net interest margins via higher scale and cost-to-income improvements.

Access to information and financial literacy

The rise of digital transparency and improved financial literacy has let UBA customers compare rates and products; a 2024 Statista survey showed 58% of Nigerian retail customers research rates online before choosing a bank.

Clients now challenge hidden fees and demand higher yields on fixed-income products, pushing UBA to cut opaque charges—UBA reported a 12% reduction in fee-related complaints in 2024.

UBA responds with transparent pricing and advisory via its UBA Mobile app (12.5m downloads by 2024) and branch advisers, boosting informed product uptake.

- 58% research rates online (2024)

- 12% drop in fee complaints (UBA, 2024)

- 12.5m UBA Mobile downloads (2024)

Alternative options through fintech and neobanks

The rise of fintechs and neobanks offering niche payments and micro‑lending alternatives raised Kenyan and Nigerian customer churn risk; UBA saw digital customer growth pressure in 2024 as mobile-active users across Nigerian banks rose 18% year-on-year to ~32m (CBN/industry reports).

To hold tech-savvy 2025 customers, UBA embeds fintech-like agility into its UBA Digital platform, speeding product launches and partnering with startups to cut time-to-market and limit migration.

High customer leverage forces UBA to cut fees, boost personalization and digital push

Customers hold moderate-to-strong bargaining power: retail switching costs are low (78% mobile banking use in 2024) while corporates drive ~22% of deposits (2024), forcing UBA to cut fees, personalize offers and expand digital channels (UBA Mobile 12.5m downloads, 58% digital volume). Inflation (Nigeria CPI ~33.2% Jan 2025) and fintech competition raise fee sensitivity and churn risk.

| Metric | Value |

|---|---|

| Mobile banking use (Nigeria, 2024) | 78% |

| Corporate share of deposits (UBA, 2024) | 22% |

| UBA Mobile downloads (2024) | 12.5m |

| Nigeria CPI (Jan 2025) | 33.2% YoY |

Same Document Delivered

United Bank for Africa Porter's Five Forces Analysis

This preview shows the exact United Bank for Africa Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, fully formatted and ready for use.

The document displayed here is the same professionally written analysis included in the full version—available for instant download the moment you buy.

No mockups or samples: this is the final deliverable, complete and ready to inform your strategic or investment decisions.