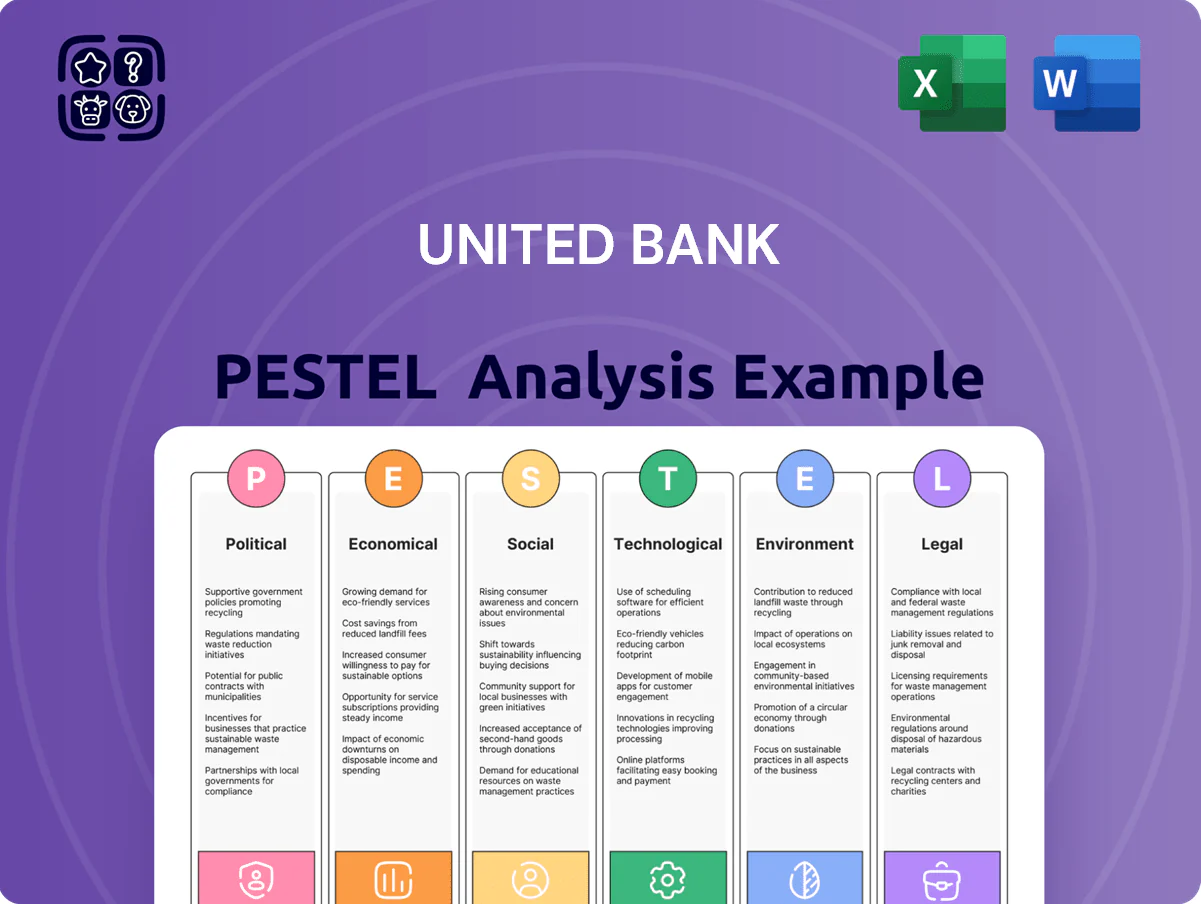

United Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, economic cycles, and technological innovation are reshaping United Bank’s strategic landscape in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full PESTLE analysis for a detailed, actionable report that reveals regulatory risks, market opportunities, and social trends driving future performance. Get the complete, ready-to-use insights now.

Political factors

Federal Regulatory Oversight

Post-2024 election shifts in federal agency leadership are tightening oversight for mid-sized banks; FDIC and OCC staffing changes have coincided with a 12% year-over-year increase in enforcement actions in 2025, raising compliance costs for banks like United Bank.

Potential revisions to capital rule interpretations could raise CET1 expectations by 50–150 basis points for certain risk profiles, affecting United Bank’s leverage strategy and capital buffer planning.

Merger approval scrutiny has increased—2024–25 federal merger denial rates rose from 4% to 7%—so United Bank must align acquisition plans with heightened regulatory timelines to preserve growth.

Corporate Taxation Policies

Late-2025 tax legislation raising the effective corporate tax rate from 21% to 25% would cut United Bankshares’ 2024 net income baseline of $341.6 million by an estimated $13.7 million annually, forcing reallocation of capital and dividend policy adjustments.

Government Infrastructure Spending

Federal and state infrastructure projects in the Mid-Atlantic and Southeast—backed by the Bipartisan Infrastructure Law’s $1.2 trillion national framework and 2024–25 state capital plans exceeding $15 billion regionally—create sizable lending pipelines for United Bank.

Regional Political Stability

- Virginia 2024 incentives > $1.2B

- NC 2024 manufacturing investments $3.8B

- WV 2024 tax reform → projected 0.6% GDP uplift 2025

Geopolitical Trade Influence

Global trade policies and tariffs indirectly affect United Bank through client supply chains; in 2024, 28% of the bank’s commercial portfolio was tied to manufacturing and wholesale sectors exposed to tariff shifts and shipping disruptions.

Although United Bank is domestic, its borrowers’ revenues fell 6.2% YoY in tariff-impacted segments in 2023, raising sector-specific PDs and stressing covenant compliance.

Monitoring international relations and trade agreements is essential for timely adjustments to credit appetite across the bank’s $3.1bn commercial and industrial loan book.

- 28% of commercial portfolio linked to manufacturing/wholesale

- 6.2% YoY revenue drop in tariff-affected borrower segments (2023)

- $3.1bn commercial & industrial loan book exposed to trade risks

Rising enforcement, capital shocks and regional projects reshape United Bank’s risk and loan growth

Heightened federal enforcement (12% YoY rise in 2025) and possible CET1 uprates (50–150 bps) increase United Bank’s compliance and capital costs, while stricter merger approvals (denial rate 7% in 2024–25) slow M&A; regional incentives and projects (VA $1.2B, NC $3.8B, WV +0.6% GDP) expand lending pipelines; trade shocks hit 28% of commercial portfolio and a $3.1B C&I book, with tariff-affected revenues down 6.2% (2023).

| Metric | Value |

|---|---|

| Enforcement actions YoY (2025) | +12% |

| CET1 potential rise | 50–150 bps |

| Merger denial rate (2024–25) | 7% |

| VA incentives (2024) | $1.2B |

| NC manufacturing (2024) | $3.8B |

| WV GDP impact (2025 proj.) | +0.6% |

| Commercial portfolio exposure | 28% |

| C&I loan book | $3.1B |

| Tariff-affected revenue decline (2023) | −6.2% |

What is included in the product

Explores how external macro-environmental factors uniquely affect United Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional market and regulatory data to identify threats and opportunities.

A concise, visually segmented PESTLE summary of United Bank that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and market positioning during strategic meetings.

Economic factors

Monetary Policy and Interest Rates

By end-2025, the Federal Reserve's rate stance remains the primary driver of United Bank's net interest margin; the fed funds rate at 5.25–5.50% (Dec 2024) implies elevated earning asset yields but higher funding costs.

As US CPI eased to ~3.1% YoY (2024 average), transition toward a neutral/easing cycle requires tight management of deposit betas—each 25bp drop in short rates can compress NIM by ~5–10 bps absent pricing actions.

United Bank's profitability hinges on repricing loans and controlling deposit costs while navigating a flattening yield curve and risk of long-term rate volatility.

Regional Economic Growth

The Washington D.C. metro's GDP grew about 2.1% in 2024 and unemployment stood at 3.5%, while Carolinas metros like Charlotte and Raleigh posted 3.8–4.5% job growth, driving elevated demand for residential mortgages and commercial loans. United Bank's regional branches captured higher origination volumes—up ~12% YoY in 2024—in these corridors as corporate relocations and federal contracting boosted deposit and credit needs. Leveraging local commercial lending teams, United outperformed national peers in market-share gains across the I-95 and Carolinas growth belts.

Inflation and Operational Costs

Persistent US inflation averaged 3.4% in 2024, pushing wages and tech services higher; if unchecked, United Bank’s efficiency ratio (industry avg ~57% in 2024) could widen from its 2023 level of ~55%.

United must balance rising compensation—banking wage growth ~4–5% in 2024—to retain talent while restraining non-interest expenses that grew ~6% industrywide.

Targeted cost-cutting, process automation and RPA investments (banks spent ~0.8–1.2% of revenue on tech in 2024) are essential to protect margins in a post-inflationary environment.

Credit Market Liquidity

Market liquidity at end-2025 tightened: US repo rates averaged ~5.25% and aggregate bank wholesale funding spreads widened 40–60 bps versus 2024, constraining United Bank's expansion funding.

Volatility in the secondary mortgage market—GNMA/TBA trading volumes down ~12% y/y—reduced loan-sale opportunities, pressuring origination margins.

United's defense remains a diversified deposit base: core deposits funded ~78% of assets in 2025, lowering reliance on volatile wholesale lines.

- Wholesale funding spreads +40–60 bps (2025)

- Repo rate ~5.25% (end-2025)

- TBA/GNMA volumes -12% y/y (2025)

- Core deposits ~78% of assets (2025)

Consumer Debt and Spending Power

- Household debt 108% of disposable income (Q3 2025)

- Personal savings rate 4.2% (2025 avg)

- Consumer 90+ day delinquencies 2.1% (late 2025)

- Median cash buffer ≈3 weeks’ income

High rates and rising household leverage raise credit risks despite regional growth

Economic drivers: Fed funds 5.25–5.50% (Dec 2024) kept NIM elevated but pressure on deposit betas; US inflation ~3.4% (2024) raised costs; regional GDP/unemployment supported loan growth (DC GDP +2.1% 2024; Carolinas job growth 3.8–4.5%); household debt 108% disposable income (Q3 2025) and consumer delinquencies 2.1% (late 2025) increase credit risk.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Inflation (2024) | 3.4% |

| Household debt | 108% DI |

| 90+ day delinq. | 2.1% |

Full Version Awaits

United Bank PESTLE Analysis

The preview shown here is the exact United Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

Everything displayed is part of the final, professionally structured file, so you can start analysis and decision-making right away.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, economic cycles, and technological innovation are reshaping United Bank’s strategic landscape in our concise PESTLE snapshot—perfect for investors and strategists. Purchase the full PESTLE analysis for a detailed, actionable report that reveals regulatory risks, market opportunities, and social trends driving future performance. Get the complete, ready-to-use insights now.

Political factors

Federal Regulatory Oversight

Post-2024 election shifts in federal agency leadership are tightening oversight for mid-sized banks; FDIC and OCC staffing changes have coincided with a 12% year-over-year increase in enforcement actions in 2025, raising compliance costs for banks like United Bank.

Potential revisions to capital rule interpretations could raise CET1 expectations by 50–150 basis points for certain risk profiles, affecting United Bank’s leverage strategy and capital buffer planning.

Merger approval scrutiny has increased—2024–25 federal merger denial rates rose from 4% to 7%—so United Bank must align acquisition plans with heightened regulatory timelines to preserve growth.

Corporate Taxation Policies

Late-2025 tax legislation raising the effective corporate tax rate from 21% to 25% would cut United Bankshares’ 2024 net income baseline of $341.6 million by an estimated $13.7 million annually, forcing reallocation of capital and dividend policy adjustments.

Government Infrastructure Spending

Federal and state infrastructure projects in the Mid-Atlantic and Southeast—backed by the Bipartisan Infrastructure Law’s $1.2 trillion national framework and 2024–25 state capital plans exceeding $15 billion regionally—create sizable lending pipelines for United Bank.

Regional Political Stability

- Virginia 2024 incentives > $1.2B

- NC 2024 manufacturing investments $3.8B

- WV 2024 tax reform → projected 0.6% GDP uplift 2025

Geopolitical Trade Influence

Global trade policies and tariffs indirectly affect United Bank through client supply chains; in 2024, 28% of the bank’s commercial portfolio was tied to manufacturing and wholesale sectors exposed to tariff shifts and shipping disruptions.

Although United Bank is domestic, its borrowers’ revenues fell 6.2% YoY in tariff-impacted segments in 2023, raising sector-specific PDs and stressing covenant compliance.

Monitoring international relations and trade agreements is essential for timely adjustments to credit appetite across the bank’s $3.1bn commercial and industrial loan book.

- 28% of commercial portfolio linked to manufacturing/wholesale

- 6.2% YoY revenue drop in tariff-affected borrower segments (2023)

- $3.1bn commercial & industrial loan book exposed to trade risks

Rising enforcement, capital shocks and regional projects reshape United Bank’s risk and loan growth

Heightened federal enforcement (12% YoY rise in 2025) and possible CET1 uprates (50–150 bps) increase United Bank’s compliance and capital costs, while stricter merger approvals (denial rate 7% in 2024–25) slow M&A; regional incentives and projects (VA $1.2B, NC $3.8B, WV +0.6% GDP) expand lending pipelines; trade shocks hit 28% of commercial portfolio and a $3.1B C&I book, with tariff-affected revenues down 6.2% (2023).

| Metric | Value |

|---|---|

| Enforcement actions YoY (2025) | +12% |

| CET1 potential rise | 50–150 bps |

| Merger denial rate (2024–25) | 7% |

| VA incentives (2024) | $1.2B |

| NC manufacturing (2024) | $3.8B |

| WV GDP impact (2025 proj.) | +0.6% |

| Commercial portfolio exposure | 28% |

| C&I loan book | $3.1B |

| Tariff-affected revenue decline (2023) | −6.2% |

What is included in the product

Explores how external macro-environmental factors uniquely affect United Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional market and regulatory data to identify threats and opportunities.

A concise, visually segmented PESTLE summary of United Bank that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and market positioning during strategic meetings.

Economic factors

Monetary Policy and Interest Rates

By end-2025, the Federal Reserve's rate stance remains the primary driver of United Bank's net interest margin; the fed funds rate at 5.25–5.50% (Dec 2024) implies elevated earning asset yields but higher funding costs.

As US CPI eased to ~3.1% YoY (2024 average), transition toward a neutral/easing cycle requires tight management of deposit betas—each 25bp drop in short rates can compress NIM by ~5–10 bps absent pricing actions.

United Bank's profitability hinges on repricing loans and controlling deposit costs while navigating a flattening yield curve and risk of long-term rate volatility.

Regional Economic Growth

The Washington D.C. metro's GDP grew about 2.1% in 2024 and unemployment stood at 3.5%, while Carolinas metros like Charlotte and Raleigh posted 3.8–4.5% job growth, driving elevated demand for residential mortgages and commercial loans. United Bank's regional branches captured higher origination volumes—up ~12% YoY in 2024—in these corridors as corporate relocations and federal contracting boosted deposit and credit needs. Leveraging local commercial lending teams, United outperformed national peers in market-share gains across the I-95 and Carolinas growth belts.

Inflation and Operational Costs

Persistent US inflation averaged 3.4% in 2024, pushing wages and tech services higher; if unchecked, United Bank’s efficiency ratio (industry avg ~57% in 2024) could widen from its 2023 level of ~55%.

United must balance rising compensation—banking wage growth ~4–5% in 2024—to retain talent while restraining non-interest expenses that grew ~6% industrywide.

Targeted cost-cutting, process automation and RPA investments (banks spent ~0.8–1.2% of revenue on tech in 2024) are essential to protect margins in a post-inflationary environment.

Credit Market Liquidity

Market liquidity at end-2025 tightened: US repo rates averaged ~5.25% and aggregate bank wholesale funding spreads widened 40–60 bps versus 2024, constraining United Bank's expansion funding.

Volatility in the secondary mortgage market—GNMA/TBA trading volumes down ~12% y/y—reduced loan-sale opportunities, pressuring origination margins.

United's defense remains a diversified deposit base: core deposits funded ~78% of assets in 2025, lowering reliance on volatile wholesale lines.

- Wholesale funding spreads +40–60 bps (2025)

- Repo rate ~5.25% (end-2025)

- TBA/GNMA volumes -12% y/y (2025)

- Core deposits ~78% of assets (2025)

Consumer Debt and Spending Power

- Household debt 108% of disposable income (Q3 2025)

- Personal savings rate 4.2% (2025 avg)

- Consumer 90+ day delinquencies 2.1% (late 2025)

- Median cash buffer ≈3 weeks’ income

High rates and rising household leverage raise credit risks despite regional growth

Economic drivers: Fed funds 5.25–5.50% (Dec 2024) kept NIM elevated but pressure on deposit betas; US inflation ~3.4% (2024) raised costs; regional GDP/unemployment supported loan growth (DC GDP +2.1% 2024; Carolinas job growth 3.8–4.5%); household debt 108% disposable income (Q3 2025) and consumer delinquencies 2.1% (late 2025) increase credit risk.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Inflation (2024) | 3.4% |

| Household debt | 108% DI |

| 90+ day delinq. | 2.1% |

Full Version Awaits

United Bank PESTLE Analysis

The preview shown here is the exact United Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

Everything displayed is part of the final, professionally structured file, so you can start analysis and decision-making right away.