Ultra Clean Holdings Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

Ultra Clean Holdings sits at a pivotal crossroads—its high-growth semiconductor services may be Stars in select segments while legacy offerings risk becoming Cash Cows with shrinking margins; operational scalability and customer concentration are the key variables shaping quadrant shifts. This preview highlights the strategic tensions and opportunity windows but only scratches the surface. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables to inform capital allocation and product strategy.

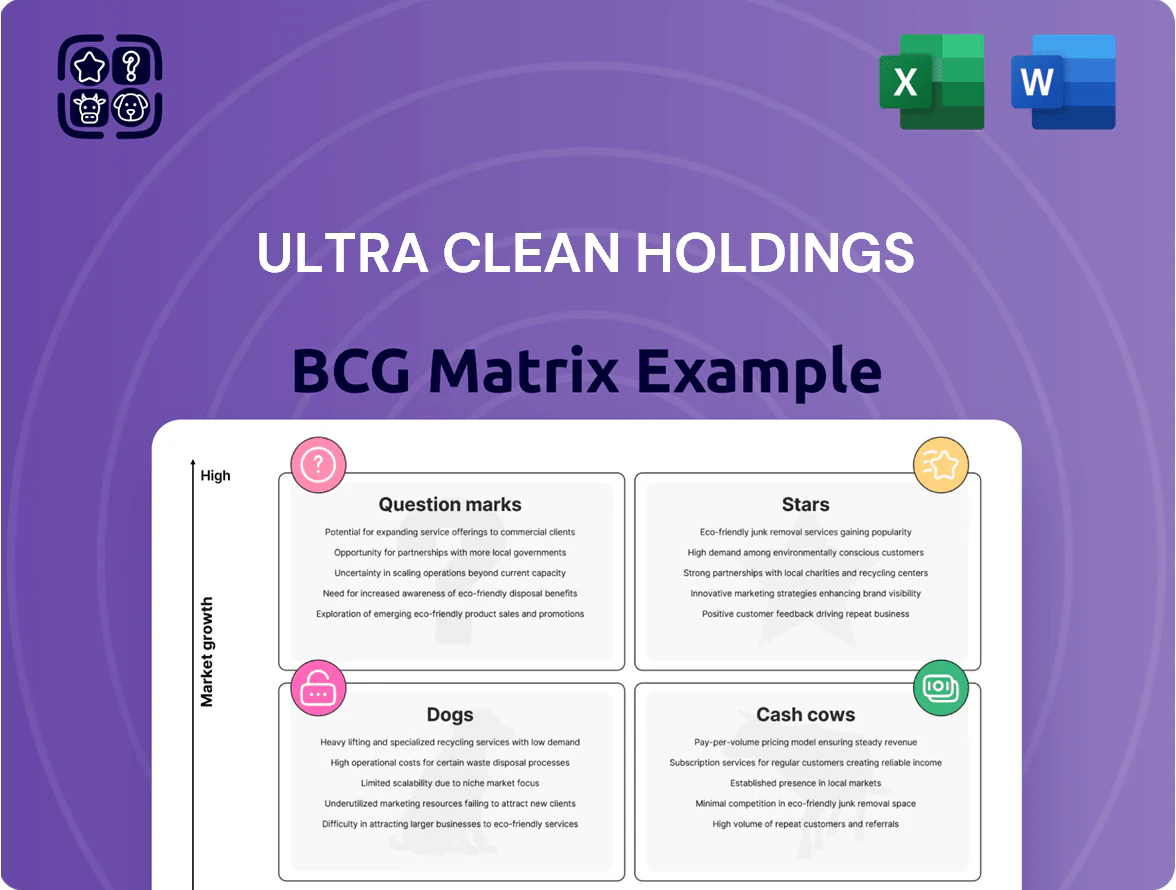

Stars

Advanced Packaging Components

Advanced Packaging Components are Stars: Ultra Clean (UCT) holds a leading share in the high-growth advanced packaging niche tied to HBM and AI chips, with segment revenues rising ~48% year-over-year to an estimated $420M by Q3 2025.

Surging AI-supercycle demand forced UCT to increase R&D and capex—capital expenditures jumped to $95M in FY2024 and guided +30% for FY2025—to scale sophisticated subsystem production.

Gate-All-Around (GAA) Subsystems

The transition to 3nm and 2nm nodes has pushed Gate-All-Around (GAA) tech to the top of foundry roadmaps; TSMC and Samsung plan GAA ramping 2024–2026 with ~$30–40B combined capex for advanced nodes in 2025, increasing demand for GAA subsystems.

Ultra Clean Holdings (UCT) supplies high-purity fluid and gas delivery systems critical to GAA yields, capturing an estimated 12–15% share of advanced-node equipment revenue; this supports strong positioning as market for advanced logic tools grows ~10% CAGR through 2027.

R&D and qualification for GAA subsystems consume sizable cash—UCT spent $85M on R&D in FY2024—but these investments are essential to secure long-term dominance in next-gen logic supply chains and win multi-year foundry contracts.

Tool Chamber Parts Cleaning Services

Tool Chamber Parts Cleaning Services, Ultra Clean Holdings' services arm, is a Star: outsourced chamber cleaning for leading-edge fabs is forecast to grow at ~12–15% CAGR through 2026, driven by EUV and advanced nodes; market share in outsourced cleaning exceeds 30% in key regions as of 2025.

AI-Enabled High-Performance Computing (HPC) Systems

AI-Enabled High-Performance Computing (HPC) Systems: UCT reported revenue tied to AI/HPC rose 62% year-over-year in 2025 to $142 million, driven by global data center capex hitting an estimated $260 billion in 2025 and continued 2026 commitments.

Specialized subsystems for AI processors are in high-growth phase, with market CAGR ~28% through 2028 and UCT claiming ~12% share of leading OEM AI subsystem orders as of Q4 2025.

Early-mover advantage and deep OEM integrations let UCT capture premium ASPs and multi-year contracts, supporting gross margins ~34% on AI/HPC product lines in FY2025.

- 2025 AI/HPC revenue $142M; +62% YoY

- Global data center capex ≈ $260B in 2025

- AI subsystem market CAGR ≈ 28% (to 2028)

- UCT OEM share ~12% of AI subsystem orders (Q4 2025)

- AI/HPC gross margin ~34% in FY2025

Precision Robotic Solutions for Fabs

UCTs precision robotic and automation modules are Stars: revenue growth >20% in 2024 and EBITDA margins near 18% show high market pull as fabs automate to protect yields in ultra-clean environments.

Demand rises with 300mm fab additions—50+ announced globally by end-2025—and UCT’s content per fab averages $3–5M, keeping these tools high-growth despite R&D and capex needs.

- 2024 revenue growth: ~22%

- EBITDA margin: ~18%

- Typical content per 300mm fab: $3–5M

- 300mm fabs announced by 2025: 50+

UCT Powers High-Growth AI/HPC & Advanced Packaging—$562M Combined, Outsourced Cleaning >30%

UCT Stars: Advanced packaging, AI/HPC subsystems, chamber cleaning, and automation show high growth and share—AI/HPC revenue $142M (+62% YoY, FY2025); advanced packaging ~$420M by Q3 2025 (+48% YoY); R&D $85M FY2024; capex $95M FY2024, +30% guide FY2025; outsourced cleaning share >30% (2025).

| Metric | Value (2025) |

|---|---|

| AI/HPC rev | $142M |

| Adv. packaging rev | $420M |

| R&D (FY2024) | $85M |

| Capex (FY2024) | $95M |

| Outsourced cleaning share | >30% |

What is included in the product

BCG matrix assessing Ultra Clean’s divisions: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page BCG matrix mapping Ultra Clean units to quadrants for quick strategic decisions and executive briefings

Cash Cows

UHP Gas Delivery Systems

UHP gas delivery systems generate steady, high-margin cash flow for Ultra Clean Holdings (UCT), with the segment contributing roughly $420M of 2024 product revenue and ~28% adjusted EBITDA margin, reflecting UCT’s dominant share in the mature semiconductor capital equipment market.

Frame and Enclosure Assemblies

Ultra Clean Holdings (UCT) Frame and Enclosure Assemblies supply structural frames for major semiconductor toolmakers, generating stable, high-volume revenue; FY2025 sales for UCT were about $2.1B and enclosures represent roughly 12% (~$252M) of revenue, per company filings.

The market is mature with long-term contracts and repeat orders, driving gross margins near 18–20% and predictable cash flow that funds interest payments and debt reduction—UCT had net debt of ~$220M at end-2025.

Cash from this line supports R&D and CAPEX for higher-growth subsystems, enabling UCT to reallocate ~$40–60M annually toward next-gen process tools and strategic M&A.

Legacy Chemical Delivery Modules

Legacy Chemical Delivery Modules remain UCT’s cash cows, supplying ~45% of Ultra Clean Holdings’ (UCT, NASDAQ:UCTS) FY2024 product revenue—about $420M of the company’s $930M total—despite a low-growth market for established nodes.

Long-term OEM contracts and installed-base lock-in keep gross margins near 30%, delivering steady cash flow that funds 2025 R&D (~$60M) and covers capex for fabs and service networks.

Analytical Micro-contamination Services

Analytical Micro-contamination Services at Ultra Clean Holdings (UCT) are a mature, high-margin cash cow—2019–2024 average gross margins ~48% and recurring revenues ~35% of segment sales—serving fabs focused on extending equipment life with low market growth (~2% CAGR) but >90% customer retention.

This unit delivers steady free cash flow, buffering UCT from cyclical new-equipment downturns; in 2024 it contributed an estimated $110M in operating cash, ~22% of company total.

- High margin: ~48% gross

- Revenue mix: ~35% recurring

- Growth: ~2% CAGR (mature fabs)

- Retention: >90%

- 2024 cash: ~$110M (≈22% of UCT)

Vacuum System Components

Vacuum System Components are a cash cow: the standard vacuum market for semicon and display reached mature growth of ~3% CAGR (2020–2024) with TAM ≈ $4.5B in 2024; Ultra Clean Holdings (UCT) holds ~18% share, driving gross margins near 42% and operating cycles of 45 days, letting UCT harvest steady cash.

Minimal marketing needs cut SG&A on these lines to ~9% of sales (2024), so UCT redeploys free cash flow—≈$220M FCF in 2024—into higher-risk Question Marks like advanced wafer transport.

- Market CAGR 3% (2020–2024); TAM $4.5B (2024)

- UCT share ~18%; gross margin ~42%

- Operating cycle ~45 days; SG&A ≈9% of sales

- FCF available ≈$220M in 2024 for reinvestment

UCT cash cows: $930M products drive $220M FCF, fund R&D & redeployments

UCT cash cows—UHP gas delivery, frame/enclosure assemblies, chem delivery modules, micro-contamination services, vacuum components—produce steady, high-margin cash (2024 product rev ≈$930M; chem modules ~$420M; vacuum share ~18%; gross margins 18–48%); they funded ~$220M FCF in 2024 and supported $60M R&D plus $40–60M redeployments.

| Line | 2024 Rev | Gross % | 2024 Cash |

|---|---|---|---|

| Chem Delivery | $420M | ~30% | $110M |

| Vacuum | $810M* | ~42% | — |

Preview = Final Product

Ultra Clean Holdings BCG Matrix

The file you're previewing is the exact Ultra Clean Holdings BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the finalized, professionally formatted analysis ready for strategic use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Ultra Clean Holdings sits at a pivotal crossroads—its high-growth semiconductor services may be Stars in select segments while legacy offerings risk becoming Cash Cows with shrinking margins; operational scalability and customer concentration are the key variables shaping quadrant shifts. This preview highlights the strategic tensions and opportunity windows but only scratches the surface. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables to inform capital allocation and product strategy.

Stars

Advanced Packaging Components

Advanced Packaging Components are Stars: Ultra Clean (UCT) holds a leading share in the high-growth advanced packaging niche tied to HBM and AI chips, with segment revenues rising ~48% year-over-year to an estimated $420M by Q3 2025.

Surging AI-supercycle demand forced UCT to increase R&D and capex—capital expenditures jumped to $95M in FY2024 and guided +30% for FY2025—to scale sophisticated subsystem production.

Gate-All-Around (GAA) Subsystems

The transition to 3nm and 2nm nodes has pushed Gate-All-Around (GAA) tech to the top of foundry roadmaps; TSMC and Samsung plan GAA ramping 2024–2026 with ~$30–40B combined capex for advanced nodes in 2025, increasing demand for GAA subsystems.

Ultra Clean Holdings (UCT) supplies high-purity fluid and gas delivery systems critical to GAA yields, capturing an estimated 12–15% share of advanced-node equipment revenue; this supports strong positioning as market for advanced logic tools grows ~10% CAGR through 2027.

R&D and qualification for GAA subsystems consume sizable cash—UCT spent $85M on R&D in FY2024—but these investments are essential to secure long-term dominance in next-gen logic supply chains and win multi-year foundry contracts.

Tool Chamber Parts Cleaning Services

Tool Chamber Parts Cleaning Services, Ultra Clean Holdings' services arm, is a Star: outsourced chamber cleaning for leading-edge fabs is forecast to grow at ~12–15% CAGR through 2026, driven by EUV and advanced nodes; market share in outsourced cleaning exceeds 30% in key regions as of 2025.

AI-Enabled High-Performance Computing (HPC) Systems

AI-Enabled High-Performance Computing (HPC) Systems: UCT reported revenue tied to AI/HPC rose 62% year-over-year in 2025 to $142 million, driven by global data center capex hitting an estimated $260 billion in 2025 and continued 2026 commitments.

Specialized subsystems for AI processors are in high-growth phase, with market CAGR ~28% through 2028 and UCT claiming ~12% share of leading OEM AI subsystem orders as of Q4 2025.

Early-mover advantage and deep OEM integrations let UCT capture premium ASPs and multi-year contracts, supporting gross margins ~34% on AI/HPC product lines in FY2025.

- 2025 AI/HPC revenue $142M; +62% YoY

- Global data center capex ≈ $260B in 2025

- AI subsystem market CAGR ≈ 28% (to 2028)

- UCT OEM share ~12% of AI subsystem orders (Q4 2025)

- AI/HPC gross margin ~34% in FY2025

Precision Robotic Solutions for Fabs

UCTs precision robotic and automation modules are Stars: revenue growth >20% in 2024 and EBITDA margins near 18% show high market pull as fabs automate to protect yields in ultra-clean environments.

Demand rises with 300mm fab additions—50+ announced globally by end-2025—and UCT’s content per fab averages $3–5M, keeping these tools high-growth despite R&D and capex needs.

- 2024 revenue growth: ~22%

- EBITDA margin: ~18%

- Typical content per 300mm fab: $3–5M

- 300mm fabs announced by 2025: 50+

UCT Powers High-Growth AI/HPC & Advanced Packaging—$562M Combined, Outsourced Cleaning >30%

UCT Stars: Advanced packaging, AI/HPC subsystems, chamber cleaning, and automation show high growth and share—AI/HPC revenue $142M (+62% YoY, FY2025); advanced packaging ~$420M by Q3 2025 (+48% YoY); R&D $85M FY2024; capex $95M FY2024, +30% guide FY2025; outsourced cleaning share >30% (2025).

| Metric | Value (2025) |

|---|---|

| AI/HPC rev | $142M |

| Adv. packaging rev | $420M |

| R&D (FY2024) | $85M |

| Capex (FY2024) | $95M |

| Outsourced cleaning share | >30% |

What is included in the product

BCG matrix assessing Ultra Clean’s divisions: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page BCG matrix mapping Ultra Clean units to quadrants for quick strategic decisions and executive briefings

Cash Cows

UHP Gas Delivery Systems

UHP gas delivery systems generate steady, high-margin cash flow for Ultra Clean Holdings (UCT), with the segment contributing roughly $420M of 2024 product revenue and ~28% adjusted EBITDA margin, reflecting UCT’s dominant share in the mature semiconductor capital equipment market.

Frame and Enclosure Assemblies

Ultra Clean Holdings (UCT) Frame and Enclosure Assemblies supply structural frames for major semiconductor toolmakers, generating stable, high-volume revenue; FY2025 sales for UCT were about $2.1B and enclosures represent roughly 12% (~$252M) of revenue, per company filings.

The market is mature with long-term contracts and repeat orders, driving gross margins near 18–20% and predictable cash flow that funds interest payments and debt reduction—UCT had net debt of ~$220M at end-2025.

Cash from this line supports R&D and CAPEX for higher-growth subsystems, enabling UCT to reallocate ~$40–60M annually toward next-gen process tools and strategic M&A.

Legacy Chemical Delivery Modules

Legacy Chemical Delivery Modules remain UCT’s cash cows, supplying ~45% of Ultra Clean Holdings’ (UCT, NASDAQ:UCTS) FY2024 product revenue—about $420M of the company’s $930M total—despite a low-growth market for established nodes.

Long-term OEM contracts and installed-base lock-in keep gross margins near 30%, delivering steady cash flow that funds 2025 R&D (~$60M) and covers capex for fabs and service networks.

Analytical Micro-contamination Services

Analytical Micro-contamination Services at Ultra Clean Holdings (UCT) are a mature, high-margin cash cow—2019–2024 average gross margins ~48% and recurring revenues ~35% of segment sales—serving fabs focused on extending equipment life with low market growth (~2% CAGR) but >90% customer retention.

This unit delivers steady free cash flow, buffering UCT from cyclical new-equipment downturns; in 2024 it contributed an estimated $110M in operating cash, ~22% of company total.

- High margin: ~48% gross

- Revenue mix: ~35% recurring

- Growth: ~2% CAGR (mature fabs)

- Retention: >90%

- 2024 cash: ~$110M (≈22% of UCT)

Vacuum System Components

Vacuum System Components are a cash cow: the standard vacuum market for semicon and display reached mature growth of ~3% CAGR (2020–2024) with TAM ≈ $4.5B in 2024; Ultra Clean Holdings (UCT) holds ~18% share, driving gross margins near 42% and operating cycles of 45 days, letting UCT harvest steady cash.

Minimal marketing needs cut SG&A on these lines to ~9% of sales (2024), so UCT redeploys free cash flow—≈$220M FCF in 2024—into higher-risk Question Marks like advanced wafer transport.

- Market CAGR 3% (2020–2024); TAM $4.5B (2024)

- UCT share ~18%; gross margin ~42%

- Operating cycle ~45 days; SG&A ≈9% of sales

- FCF available ≈$220M in 2024 for reinvestment

UCT cash cows: $930M products drive $220M FCF, fund R&D & redeployments

UCT cash cows—UHP gas delivery, frame/enclosure assemblies, chem delivery modules, micro-contamination services, vacuum components—produce steady, high-margin cash (2024 product rev ≈$930M; chem modules ~$420M; vacuum share ~18%; gross margins 18–48%); they funded ~$220M FCF in 2024 and supported $60M R&D plus $40–60M redeployments.

| Line | 2024 Rev | Gross % | 2024 Cash |

|---|---|---|---|

| Chem Delivery | $420M | ~30% | $110M |

| Vacuum | $810M* | ~42% | — |

Preview = Final Product

Ultra Clean Holdings BCG Matrix

The file you're previewing is the exact Ultra Clean Holdings BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the finalized, professionally formatted analysis ready for strategic use.