Ultra Clean Holdings SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Ultra Clean Holdings shows strong niche leadership in semiconductor supply chains with advanced manufacturing capabilities and sticky OEM relationships, yet faces cyclical demand risk and supply-chain concentration; our full SWOT uncovers strategic levers, financial implications, and scenario-based recommendations to inform investment or operational moves—purchase the complete, editable SWOT report (Word + Excel) for ready-to-use insights and planning tools.

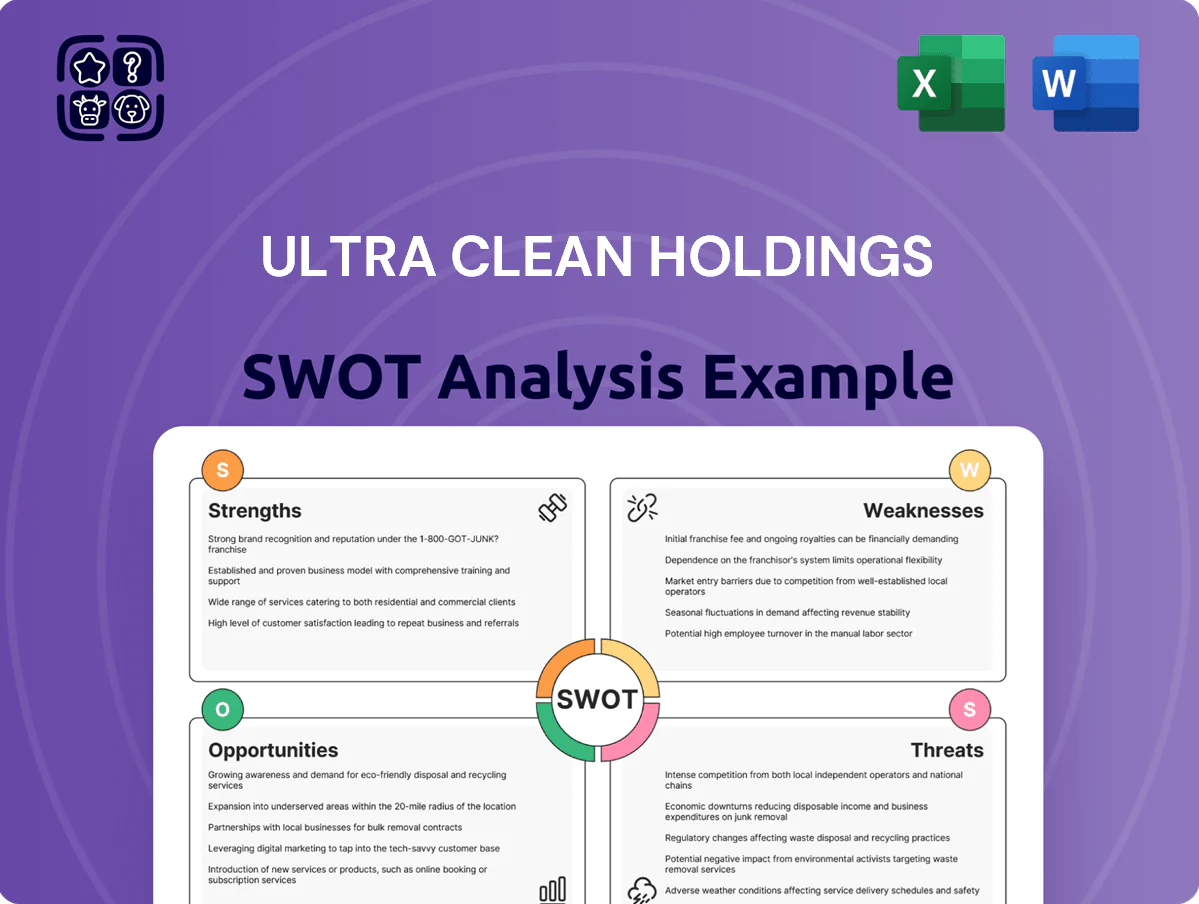

Strengths

Market Leadership in Critical Subsystems

Ultra Clean Holdings dominates as a top developer of gas and chemical delivery subsystems for semiconductors, serving >70% of leading OEMs in 2024 and generating $1.2B revenue in fiscal 2024.

Their ultra‑high purity component expertise—vacuum valves, manifolds, and tube assemblies—cuts defect rates, supporting customer fabs with uptime >99.5%.

Continuous R&D spend of ~$55M in 2024 sustains innovation and a reputation for high‑quality engineering in complex fluid and vacuum environments.

Deep Integration with Tier 1 Customers

Ultra Clean Holdings (UCT) has multi-decade contracts with Applied Materials and Lam Research that accounted for roughly 48% of 2024 revenue, anchoring cash flow and margins.

These partnerships include deep technical co-development across tool design and fabs, making UCT integral to next-gen chip equipment lifecycles.

High switching costs—complex qualification, ~$10s–100sM validation spend, and multi-year timelines—create a durable competitive moat and revenue visibility.

Vertically Integrated Service Model

UCT’s vertically integrated service model combines hardware manufacturing with high-purity cleaning and analytical labs, letting it serve the full semiconductor chamber-parts lifecycle from fabrication to contamination analysis.

This integration boosted 2024 services gross margin to about 28%, higher than typical hardware-only peers, and increased revenue per customer via recurring maintenance contracts.

One-stop capability raises customer stickiness: >60% of top-20 customers used both manufacturing and cleaning in 2024, reducing churn and improving lifetime value.

Global Manufacturing and Resilience

With manufacturing in the US, Singapore, Malaysia, and China, Ultra Clean Holdings (UCT) reduces single‑country risk and supported 2024 revenue resilience—UCT reported $1.1B revenue in FY2024 with ~40% from Asia, aiding supply continuity during regional disruptions.

The global footprint enables localized service to semiconductor hubs, lowers logistics costs, and lets UCT reallocate capacity quickly, improving uptime and margin protection.

- FY2024 revenue: $1.1B

- Asia contribution: ~40%

- 4 production regions enable rapid capacity shifts

- Improves logistics and margin resilience

Strong Technical and Engineering Expertise

The company’s workforce includes PhD-level materials scientists and engineers specializing in fluid dynamics and micro-contamination control, supporting Ultra Clean Holdings’ (UCT) $1.2B 2024 revenue base and 18% gross margin to address sub-5nm process node challenges.

That expertise lets UCT solve complex tooling and contamination issues for EUV and advanced packaging customers, keeping R&D spend at 6.5% of sales in 2024 to stay industry-leading.

- PhD-heavy talent pool

- Supports sub-5nm and EUV needs

- $1.2B revenue (2024)

- 6.5% R&D intensity (2024)

- 18% gross margin (2024)

Ultra Clean: $1.2B gas-delivery leader with sticky OEM contracts and high-margin services

Ultra Clean (UCT) is a leading supplier of gas/chemical delivery subsystems, serving >70% of top OEMs and generating ~$1.1–1.2B in FY2024 with 18% gross margin; strong multi-decade contracts (≈48% revenue) with Applied Materials and Lam Research anchor cash flow. R&D ~6.5% (~$55M) and PhD talent support sub-5nm/EUV needs; vertical integration and 4-region manufacturing cut risk and lift services margin to ~28%, boosting customer stickiness.

| Metric | Value (FY2024) |

|---|---|

| Revenue | $1.1–1.2B |

| Gross margin | 18% |

| Services margin | 28% |

| R&D spend | $55M (6.5%) |

| OEM share | >70% |

| Top customers rev | ~48% |

| Asia revenue | ~40% |

What is included in the product

Provides a concise SWOT overview of Ultra Clean Holdings, outlining its operational strengths, internal weaknesses, external growth opportunities, and market threats shaping strategic decisions.

Provides a concise Ultra Clean Holdings SWOT matrix for fast, visual strategy alignment and quick executive snapshots.

Weaknesses

High Customer Concentration Risk

About 70% of Ultra Clean Holdings' (UCT) revenue came from its top three customers in FY2024, exposing the firm to outsized risk from any single partner's spending cycle.

If a major customer trims orders or shifts suppliers, UCT could see double-digit revenue declines within quarters; FY2024 gross margin of ~16% would quickly compress.

Relationships are strong, but the concentrated client mix and limited diversification remain a key structural weakness for UCT going into 2025.

Exposure to Semiconductor Industry Cyclicality

The company’s financial health tracks semiconductor capital expenditure cycles—an industry that saw fab capex fall about 18% in 2023 after a 2021–22 boom—so UCT revenue can swing sharply with chipmakers’ spend. During downturns, orders for cleanroom filters and tool components can drop over 40% in quarters, creating notable revenue volatility for UCT. This cyclicality complicates long-term planning, cash-flow smoothing, and consistent growth for management and investors.

Sensitivity to Raw Material Price Fluctuations

UCT depends on specialized inputs like high-grade stainless steel and advanced polymers; global stainless scrap prices rose ~18% in 2024, increasing input risk.

If UCT cannot pass costs to customers quickly, gross margins (36.4% in FY2024) could compress materially; a 10% input spike could cut EBIT by ~2–3 ppt.

Complex inventories raise obsolescence and carrying costs—days inventory outstanding was ~78 in 2024—heightening write-down risk during demand slumps.

Significant Capital Expenditure Requirements

Significant capital needs force Ultra Clean Holdings (UCT) to keep investing in advanced fabs and cleaning lines; management reported capital expenditures of $146.6 million in FY2024, about 11% of revenue, and guided similar levels for 2025.

Heavy capex strains cash flow when revenue dips—UCT’s free cash flow swung negative $32M in H1 2024—so upgrades and expansions demand disciplined, often costly allocation and raise funding risk.

- FY2024 capex $146.6M (≈11% of revenue)

- H1 2024 free cash flow −$32M

- Ongoing upgrades raise funding and execution risk

Operational Dependence on Skilled Labor

The precision in ultra-high-purity manufacturing makes Ultra Clean Holdings (UCT) highly dependent on a specialized workforce, a segment reported as tight industry-wide with US semiconductor skilled labor shortages estimated at ~70,000 workers in 2024.

Rising wages pushed UCT’s SG&A up 6% in FY2024, and intense competition for talent can further inflate operating costs and margins.

Loss of key engineers could delay production and slow innovation, risking revenue tied to major OEM contracts.

- Skilled-labor shortfall ~70,000 (US, 2024)

- SG&A +6% (UCT FY2024)

- Key-person risk → production/innovation delays

High customer concentration, rising costs and heavy capex threaten UCT's cash flow

Customer concentration (top 3 ≈70% FY2024) and semiconductor capex cyclicality (fab capex −18% in 2023) expose UCT to sharp revenue swings; FY2024 gross margin ~16% and EBIT sensitivity means double-digit order drops compress profits quickly. High input cost pressure (stainless scrap +18% in 2024), inventory days ~78, and heavy capex ($146.6M, ≈11% revenue FY2024) strain cash flow (H1 2024 FCF −$32M). Skilled-labor shortfall (~70,000 US, 2024) raises wage and execution risk.

| Metric | Value |

|---|---|

| Top‑3 customers | ≈70% (FY2024) |

| Gross margin | ~16% (FY2024) |

| Capex | $146.6M (≈11% rev, FY2024) |

| FCF | −$32M (H1 2024) |

| Inventory days | ~78 (2024) |

| Stainless scrap | +18% (2024) |

| Skilled‑labor gap | ~70,000 US (2024) |

What You See Is What You Get

Ultra Clean Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. Buy now to unlock the complete, detailed Ultra Clean Holdings analysis for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Ultra Clean Holdings shows strong niche leadership in semiconductor supply chains with advanced manufacturing capabilities and sticky OEM relationships, yet faces cyclical demand risk and supply-chain concentration; our full SWOT uncovers strategic levers, financial implications, and scenario-based recommendations to inform investment or operational moves—purchase the complete, editable SWOT report (Word + Excel) for ready-to-use insights and planning tools.

Strengths

Market Leadership in Critical Subsystems

Ultra Clean Holdings dominates as a top developer of gas and chemical delivery subsystems for semiconductors, serving >70% of leading OEMs in 2024 and generating $1.2B revenue in fiscal 2024.

Their ultra‑high purity component expertise—vacuum valves, manifolds, and tube assemblies—cuts defect rates, supporting customer fabs with uptime >99.5%.

Continuous R&D spend of ~$55M in 2024 sustains innovation and a reputation for high‑quality engineering in complex fluid and vacuum environments.

Deep Integration with Tier 1 Customers

Ultra Clean Holdings (UCT) has multi-decade contracts with Applied Materials and Lam Research that accounted for roughly 48% of 2024 revenue, anchoring cash flow and margins.

These partnerships include deep technical co-development across tool design and fabs, making UCT integral to next-gen chip equipment lifecycles.

High switching costs—complex qualification, ~$10s–100sM validation spend, and multi-year timelines—create a durable competitive moat and revenue visibility.

Vertically Integrated Service Model

UCT’s vertically integrated service model combines hardware manufacturing with high-purity cleaning and analytical labs, letting it serve the full semiconductor chamber-parts lifecycle from fabrication to contamination analysis.

This integration boosted 2024 services gross margin to about 28%, higher than typical hardware-only peers, and increased revenue per customer via recurring maintenance contracts.

One-stop capability raises customer stickiness: >60% of top-20 customers used both manufacturing and cleaning in 2024, reducing churn and improving lifetime value.

Global Manufacturing and Resilience

With manufacturing in the US, Singapore, Malaysia, and China, Ultra Clean Holdings (UCT) reduces single‑country risk and supported 2024 revenue resilience—UCT reported $1.1B revenue in FY2024 with ~40% from Asia, aiding supply continuity during regional disruptions.

The global footprint enables localized service to semiconductor hubs, lowers logistics costs, and lets UCT reallocate capacity quickly, improving uptime and margin protection.

- FY2024 revenue: $1.1B

- Asia contribution: ~40%

- 4 production regions enable rapid capacity shifts

- Improves logistics and margin resilience

Strong Technical and Engineering Expertise

The company’s workforce includes PhD-level materials scientists and engineers specializing in fluid dynamics and micro-contamination control, supporting Ultra Clean Holdings’ (UCT) $1.2B 2024 revenue base and 18% gross margin to address sub-5nm process node challenges.

That expertise lets UCT solve complex tooling and contamination issues for EUV and advanced packaging customers, keeping R&D spend at 6.5% of sales in 2024 to stay industry-leading.

- PhD-heavy talent pool

- Supports sub-5nm and EUV needs

- $1.2B revenue (2024)

- 6.5% R&D intensity (2024)

- 18% gross margin (2024)

Ultra Clean: $1.2B gas-delivery leader with sticky OEM contracts and high-margin services

Ultra Clean (UCT) is a leading supplier of gas/chemical delivery subsystems, serving >70% of top OEMs and generating ~$1.1–1.2B in FY2024 with 18% gross margin; strong multi-decade contracts (≈48% revenue) with Applied Materials and Lam Research anchor cash flow. R&D ~6.5% (~$55M) and PhD talent support sub-5nm/EUV needs; vertical integration and 4-region manufacturing cut risk and lift services margin to ~28%, boosting customer stickiness.

| Metric | Value (FY2024) |

|---|---|

| Revenue | $1.1–1.2B |

| Gross margin | 18% |

| Services margin | 28% |

| R&D spend | $55M (6.5%) |

| OEM share | >70% |

| Top customers rev | ~48% |

| Asia revenue | ~40% |

What is included in the product

Provides a concise SWOT overview of Ultra Clean Holdings, outlining its operational strengths, internal weaknesses, external growth opportunities, and market threats shaping strategic decisions.

Provides a concise Ultra Clean Holdings SWOT matrix for fast, visual strategy alignment and quick executive snapshots.

Weaknesses

High Customer Concentration Risk

About 70% of Ultra Clean Holdings' (UCT) revenue came from its top three customers in FY2024, exposing the firm to outsized risk from any single partner's spending cycle.

If a major customer trims orders or shifts suppliers, UCT could see double-digit revenue declines within quarters; FY2024 gross margin of ~16% would quickly compress.

Relationships are strong, but the concentrated client mix and limited diversification remain a key structural weakness for UCT going into 2025.

Exposure to Semiconductor Industry Cyclicality

The company’s financial health tracks semiconductor capital expenditure cycles—an industry that saw fab capex fall about 18% in 2023 after a 2021–22 boom—so UCT revenue can swing sharply with chipmakers’ spend. During downturns, orders for cleanroom filters and tool components can drop over 40% in quarters, creating notable revenue volatility for UCT. This cyclicality complicates long-term planning, cash-flow smoothing, and consistent growth for management and investors.

Sensitivity to Raw Material Price Fluctuations

UCT depends on specialized inputs like high-grade stainless steel and advanced polymers; global stainless scrap prices rose ~18% in 2024, increasing input risk.

If UCT cannot pass costs to customers quickly, gross margins (36.4% in FY2024) could compress materially; a 10% input spike could cut EBIT by ~2–3 ppt.

Complex inventories raise obsolescence and carrying costs—days inventory outstanding was ~78 in 2024—heightening write-down risk during demand slumps.

Significant Capital Expenditure Requirements

Significant capital needs force Ultra Clean Holdings (UCT) to keep investing in advanced fabs and cleaning lines; management reported capital expenditures of $146.6 million in FY2024, about 11% of revenue, and guided similar levels for 2025.

Heavy capex strains cash flow when revenue dips—UCT’s free cash flow swung negative $32M in H1 2024—so upgrades and expansions demand disciplined, often costly allocation and raise funding risk.

- FY2024 capex $146.6M (≈11% of revenue)

- H1 2024 free cash flow −$32M

- Ongoing upgrades raise funding and execution risk

Operational Dependence on Skilled Labor

The precision in ultra-high-purity manufacturing makes Ultra Clean Holdings (UCT) highly dependent on a specialized workforce, a segment reported as tight industry-wide with US semiconductor skilled labor shortages estimated at ~70,000 workers in 2024.

Rising wages pushed UCT’s SG&A up 6% in FY2024, and intense competition for talent can further inflate operating costs and margins.

Loss of key engineers could delay production and slow innovation, risking revenue tied to major OEM contracts.

- Skilled-labor shortfall ~70,000 (US, 2024)

- SG&A +6% (UCT FY2024)

- Key-person risk → production/innovation delays

High customer concentration, rising costs and heavy capex threaten UCT's cash flow

Customer concentration (top 3 ≈70% FY2024) and semiconductor capex cyclicality (fab capex −18% in 2023) expose UCT to sharp revenue swings; FY2024 gross margin ~16% and EBIT sensitivity means double-digit order drops compress profits quickly. High input cost pressure (stainless scrap +18% in 2024), inventory days ~78, and heavy capex ($146.6M, ≈11% revenue FY2024) strain cash flow (H1 2024 FCF −$32M). Skilled-labor shortfall (~70,000 US, 2024) raises wage and execution risk.

| Metric | Value |

|---|---|

| Top‑3 customers | ≈70% (FY2024) |

| Gross margin | ~16% (FY2024) |

| Capex | $146.6M (≈11% rev, FY2024) |

| FCF | −$32M (H1 2024) |

| Inventory days | ~78 (2024) |

| Stainless scrap | +18% (2024) |

| Skilled‑labor gap | ~70,000 US (2024) |

What You See Is What You Get

Ultra Clean Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. Buy now to unlock the complete, detailed Ultra Clean Holdings analysis for download.