Universal Health Services Porter's Five Forces Analysis

Don't Miss the Bigger Picture

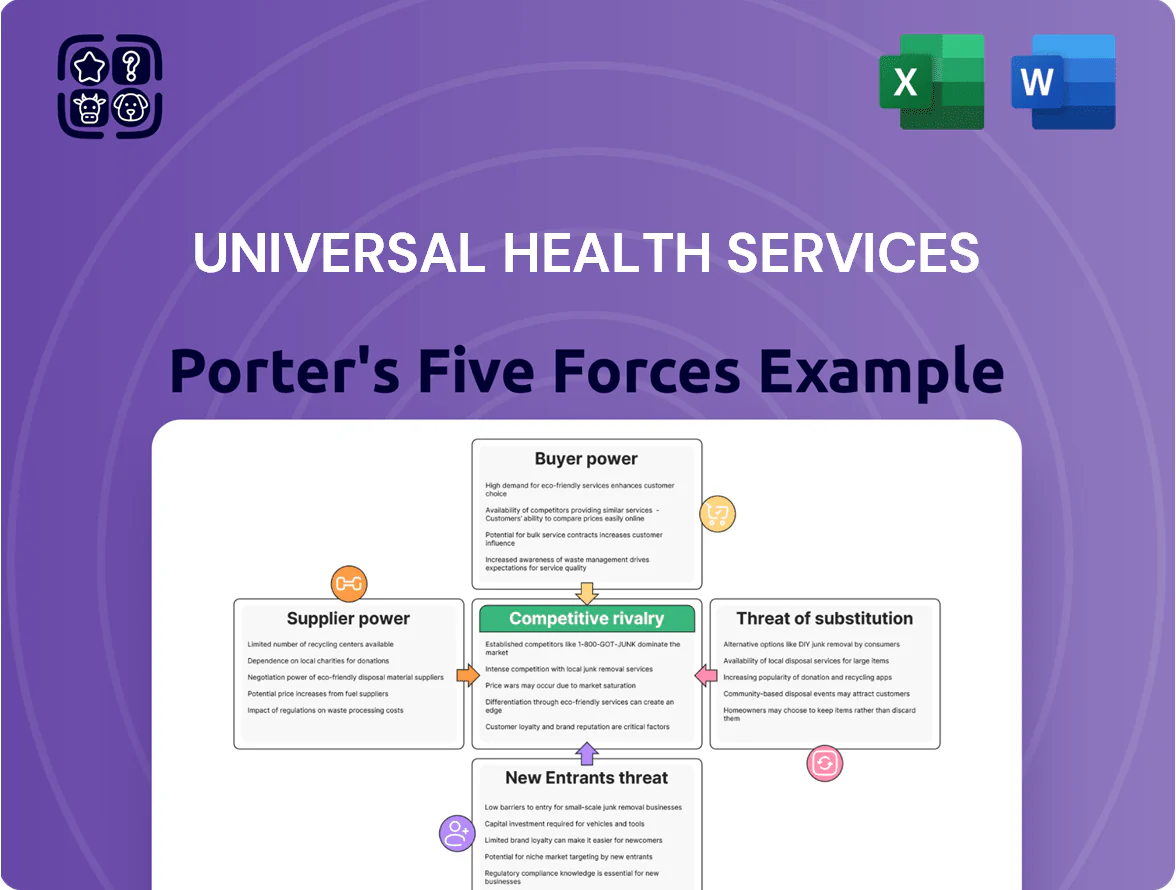

Universal Health Services faces intense competitive rivalry and regulatory pressure, with moderate supplier power and evolving payer dynamics shaping margins; potential new entrants and substitutes (telehealth, outpatient providers) add strategic risk and opportunity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Universal Health Services’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized medical labor and nursing staff

The persistent shortage of registered nurses and psychiatric specialists gives suppliers strong leverage, forcing UHS to raise wages and pay for contract staff; industry RN vacancy rates hit about 9.5% in 2024 and psychiatric positions 12–15% in high-need markets. As of late 2025, UHS reports elevated labor cost pressure—labor expense per adjusted discharge rose roughly 6–8% year-over-year—squeezing operating margins and necessitating ongoing recruitment and retention spend.

Pharmaceutical and biotechnology companies

Medical device and equipment manufacturers

Medical device suppliers—makers of diagnostic scanners, surgical robots, and behavioral-health monitors—are few and concentrated, giving them strong bargaining power over UHS; global surgical-robot sales rose 12% in 2024 to about $7.1B, tightening vendor dominance.

These vendors bind hospitals with long-term service and proprietary software contracts, creating high switching costs; maintenance can run 10–20% of device price annually.

UHS thus faces dependence for capital spending and tech upgrades, with 2024 capex for US hospital systems near $23B, much tied to such suppliers.

Health Information Technology and EHR providers

Health Information Technology and EHR providers hold strong supplier power over Universal Health Services (UHS) because a few dominant vendors (Epic, Cerner/Oracle) control ~70–80% of US hospital EHR market share, making swaps costly and slow.

Switching platforms can cost hundreds of millions across a large system; estimates show $200–500M+ for enterprise migrations and 12–24 months of operational disruption, so vendors sustain pricing on licenses, security patches, and support.

- High vendor concentration: ~70–80% market share

- Estimated migration cost: $200–500M+ for large systems

- Typical transition time: 12–24 months

- Areas of leverage: license fees, cybersecurity updates, support

Real estate and facility construction firms

Real estate and healthcare construction firms hold elevated supplier power for Universal Health Services (UHS) because new acute-care and behavioral-health sites need contractors versed in healthcare codes and MEP (mechanical, electrical, plumbing) systems, narrowing qualified providers.

As UHS expands in high-demand US metros, it competes for a small pool of specialist developers; national hospital construction starts fell 12% in 2024, tightening capacity.

Rising input costs — construction material prices up ~6% YoY in 2024 and specialty labor shortages — can raise project budgets by 10–20%, squeezing capex and ROIC.

- Specialized contractors concentrated, raising bargaining power

- Hospital construction starts down 12% in 2024, reducing supply

- Materials +6% YoY (2024); budgets may rise 10–20%

Suppliers Squeeze UHS: Labor, Drugs, EHRs & Construction Drive Costs Up

Suppliers hold strong bargaining power over UHS via labor (RN vacancy ~9.5% in 2024; psych roles 12–15%), branded drug price inflation ~6–8% (2023–24), concentrated EHR vendors (Epic/Cerner ~70–80% share, migration $200–500M+, 12–24 months), and specialist contractors (hospital starts -12% in 2024; materials +6% YoY), all raising operating and capex costs.

| Supplier | Key metric | 2023–2025 figure |

|---|---|---|

| Labor | RN vacancy / psych roles | 9.5% / 12–15% (2024) |

| Pharma | Branded drug inflation | 6–8% YoY (2023–24) |

| EHR | Market share / migration cost | 70–80% / $200–500M+ |

| Construction | Starts change / materials | -12% starts (2024); +6% materials |

What is included in the product

Tailored Porter's Five Forces analysis for Universal Health Services highlighting competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and identifying disruptive trends and regulatory barriers that shape its pricing power and profitability.

Clear, one-sheet Porter's Five Forces for Universal Health Services—instantly visualize competitive pressure and regulatory risks to speed strategic and investment decisions.

Customers Bargaining Power

Government reimbursement agencies

Private insurance and managed care organizations

Large corporate employer groups

Individual self-pay patients

Individual self-pay patients have limited leverage in emergencies but, with 43% of US adults enrolled in high-deductible health plans in 2024, they’re more price-sensitive for elective and behavioral care.

Use of price-transparency tools rose 28% in 2023, letting patients compare procedure costs across systems, so UHS must tighten non-urgent pricing and improve patient experience to retain volume.

- 43% on high-deductible plans (2024)

- 28% rise in price-tool usage (2023)

- Focus: competitive pricing, patient experience

Behavioral health referral sources

- 65% of admissions from community referrals (2024)

- 84% average bed occupancy (2024)

- 38% referrers prioritize <72h wait times (2023)

Payer Power, Public Payers & Price Sensitivity Squeeze UHS Margins

| Metric | Value |

|---|---|

| Medicare/Medicaid share | ~50% (2024) |

| Op margin | 6.2% (2024) |

| UnitedHealth members | 52M (2024) |

| Top-5 insurer share | >70% (many states) |

| HDHP enrollment | 43% adults (2024) |

| Referrals to behavioral | 65% admissions (2024) |

What You See Is What You Get

Universal Health Services Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Universal Health Services you'll receive immediately after purchase—no surprises, no placeholders, fully formatted for download.

You're viewing the final, professionally written document; once you complete your purchase you'll get instant access to this identical file, ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Universal Health Services faces intense competitive rivalry and regulatory pressure, with moderate supplier power and evolving payer dynamics shaping margins; potential new entrants and substitutes (telehealth, outpatient providers) add strategic risk and opportunity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Universal Health Services’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized medical labor and nursing staff

The persistent shortage of registered nurses and psychiatric specialists gives suppliers strong leverage, forcing UHS to raise wages and pay for contract staff; industry RN vacancy rates hit about 9.5% in 2024 and psychiatric positions 12–15% in high-need markets. As of late 2025, UHS reports elevated labor cost pressure—labor expense per adjusted discharge rose roughly 6–8% year-over-year—squeezing operating margins and necessitating ongoing recruitment and retention spend.

Pharmaceutical and biotechnology companies

Medical device and equipment manufacturers

Medical device suppliers—makers of diagnostic scanners, surgical robots, and behavioral-health monitors—are few and concentrated, giving them strong bargaining power over UHS; global surgical-robot sales rose 12% in 2024 to about $7.1B, tightening vendor dominance.

These vendors bind hospitals with long-term service and proprietary software contracts, creating high switching costs; maintenance can run 10–20% of device price annually.

UHS thus faces dependence for capital spending and tech upgrades, with 2024 capex for US hospital systems near $23B, much tied to such suppliers.

Health Information Technology and EHR providers

Health Information Technology and EHR providers hold strong supplier power over Universal Health Services (UHS) because a few dominant vendors (Epic, Cerner/Oracle) control ~70–80% of US hospital EHR market share, making swaps costly and slow.

Switching platforms can cost hundreds of millions across a large system; estimates show $200–500M+ for enterprise migrations and 12–24 months of operational disruption, so vendors sustain pricing on licenses, security patches, and support.

- High vendor concentration: ~70–80% market share

- Estimated migration cost: $200–500M+ for large systems

- Typical transition time: 12–24 months

- Areas of leverage: license fees, cybersecurity updates, support

Real estate and facility construction firms

Real estate and healthcare construction firms hold elevated supplier power for Universal Health Services (UHS) because new acute-care and behavioral-health sites need contractors versed in healthcare codes and MEP (mechanical, electrical, plumbing) systems, narrowing qualified providers.

As UHS expands in high-demand US metros, it competes for a small pool of specialist developers; national hospital construction starts fell 12% in 2024, tightening capacity.

Rising input costs — construction material prices up ~6% YoY in 2024 and specialty labor shortages — can raise project budgets by 10–20%, squeezing capex and ROIC.

- Specialized contractors concentrated, raising bargaining power

- Hospital construction starts down 12% in 2024, reducing supply

- Materials +6% YoY (2024); budgets may rise 10–20%

Suppliers Squeeze UHS: Labor, Drugs, EHRs & Construction Drive Costs Up

Suppliers hold strong bargaining power over UHS via labor (RN vacancy ~9.5% in 2024; psych roles 12–15%), branded drug price inflation ~6–8% (2023–24), concentrated EHR vendors (Epic/Cerner ~70–80% share, migration $200–500M+, 12–24 months), and specialist contractors (hospital starts -12% in 2024; materials +6% YoY), all raising operating and capex costs.

| Supplier | Key metric | 2023–2025 figure |

|---|---|---|

| Labor | RN vacancy / psych roles | 9.5% / 12–15% (2024) |

| Pharma | Branded drug inflation | 6–8% YoY (2023–24) |

| EHR | Market share / migration cost | 70–80% / $200–500M+ |

| Construction | Starts change / materials | -12% starts (2024); +6% materials |

What is included in the product

Tailored Porter's Five Forces analysis for Universal Health Services highlighting competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and identifying disruptive trends and regulatory barriers that shape its pricing power and profitability.

Clear, one-sheet Porter's Five Forces for Universal Health Services—instantly visualize competitive pressure and regulatory risks to speed strategic and investment decisions.

Customers Bargaining Power

Government reimbursement agencies

Private insurance and managed care organizations

Large corporate employer groups

Individual self-pay patients

Individual self-pay patients have limited leverage in emergencies but, with 43% of US adults enrolled in high-deductible health plans in 2024, they’re more price-sensitive for elective and behavioral care.

Use of price-transparency tools rose 28% in 2023, letting patients compare procedure costs across systems, so UHS must tighten non-urgent pricing and improve patient experience to retain volume.

- 43% on high-deductible plans (2024)

- 28% rise in price-tool usage (2023)

- Focus: competitive pricing, patient experience

Behavioral health referral sources

- 65% of admissions from community referrals (2024)

- 84% average bed occupancy (2024)

- 38% referrers prioritize <72h wait times (2023)

Payer Power, Public Payers & Price Sensitivity Squeeze UHS Margins

| Metric | Value |

|---|---|

| Medicare/Medicaid share | ~50% (2024) |

| Op margin | 6.2% (2024) |

| UnitedHealth members | 52M (2024) |

| Top-5 insurer share | >70% (many states) |

| HDHP enrollment | 43% adults (2024) |

| Referrals to behavioral | 65% admissions (2024) |

What You See Is What You Get

Universal Health Services Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Universal Health Services you'll receive immediately after purchase—no surprises, no placeholders, fully formatted for download.

You're viewing the final, professionally written document; once you complete your purchase you'll get instant access to this identical file, ready for use.