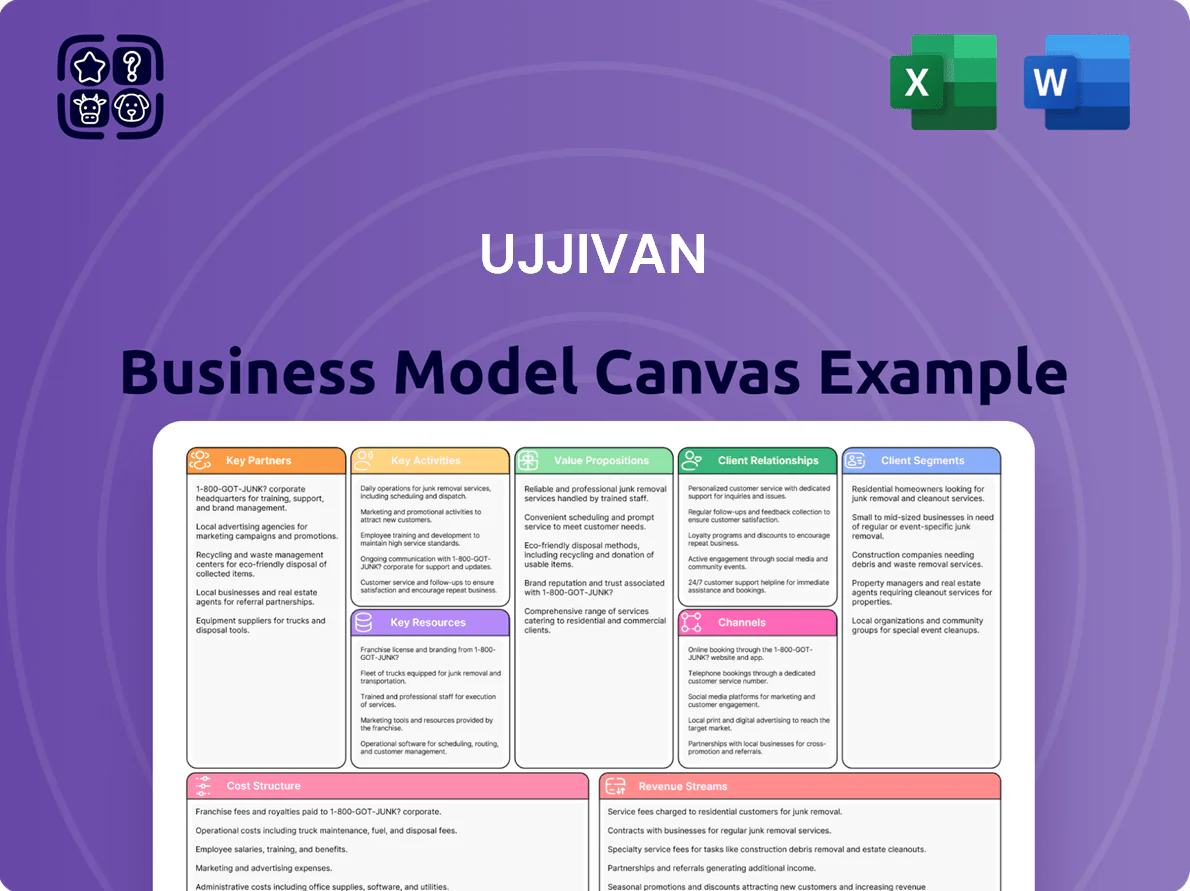

Ujjivan Business Model Canvas

Ujjivan Microfinance BMC: Customer-Centric Growth & Inclusion

Explore Ujjivan’s customer-focused microfinance engine with our concise Business Model Canvas—discover value propositions, distribution channels, and revenue levers that fuel growth in underserved markets and drive financial inclusion.

Partnerships

Fintech and Digital Payment Collaborators

Collaborations with fintechs let Ujjivan integrate instant payments and alternative credit scoring (e.g., transaction-based models), cutting onboarding time to under 10 minutes and raising digital loan approvals by 28% in 2024; third-party APIs also trimmed internal dev costs ~22%, keeping the bank competitive in India’s 2025 digital-payments market projected at $1.3 trillion.

Insurance and Third-Party Product Providers

Ujjivan partners with insurers like SBI Life and Tata AIA to sell life, health, and general policies via bancassurance, driving non‑interest income that was ~12% of FY2024 fee revenue and helping cover 1.9 million low‑income borrowers against shocks.

Business Correspondents and Field Agents

Strategic alliances with ~28,000 Business Correspondents (BCs) and field agents extend Ujjivan’s reach into remote areas, letting the bank avoid branch capex while serving last-mile customers; BCs handle cash deposits, withdrawals and basic accounts, supporting Ujjivan’s ~6.5 million active customers across semi-urban and rural India as of FY2024.

Regulatory and Industry Bodies

Active engagement with the Reserve Bank of India and the Small Finance Bank Association keeps Ujjivan aligned with evolving rules; as of FY2024 Ujjivan SFB reported a CRAR (capital to risk-weighted assets) of 19.6%, helping meet RBI capital adequacy norms.

These partnerships help navigate priority sector lending targets (40% for domestic banks); strong regulator ties boost institutional credibility and reduce regulatory friction, supporting steady operations and deposit growth (+12% YoY in FY2024).

- CRAR 19.6% (FY2024)

- Priority sector target 40%

- Deposit growth +12% YoY (FY2024)

Technology and Infrastructure Vendors

The bank relies on specialized IT vendors to run its core banking system and cloud infrastructure, delivering 99.95% uptime and PCI-DSS-level security to handle ~35 million annual transactions as of FY 2024.

These partners supply hardware/software updates and threat monitoring, reducing breach incidents by ~40% year-over-year and enabling scalable operations to support projected customer growth to ~6.5 million by 2026.

- 99.95% uptime

- ~35M transactions (FY2024)

- ~40% fewer breaches YoY

- Target ~6.5M customers by 2026

Partnership-fueled growth: 6.5M users, 35M txns, +12% deposits, 28% digital approvals

Key partnerships (fintechs, insurers, 28,000 BCs, IT vendors, RBI/SFBA) cut onboarding <10 mins, raised digital approvals +28% (2024), drove non‑interest income ~12% of fee revenue (FY2024), supported 6.5M active customers and 35M transactions (FY2024), CRAR 19.6%, deposits +12% YoY; uptime 99.95%, breaches -40% YoY.

| Metric | Value |

|---|---|

| Active customers | 6.5M (FY2024) |

| Transactions | 35M (FY2024) |

| CRAR | 19.6% (FY2024) |

| Deposit growth | +12% YoY (FY2024) |

What is included in the product

A comprehensive Business Model Canvas for Ujjivan Microfinance that maps customer segments, value propositions, channels, revenue streams, and key partners, reflecting real-world operations and strategic priorities.

High-level view of Ujjivan’s business model with editable cells, condensing its microfinance-to-banking strategy into a digestible one-page snapshot for quick review and team collaboration.

Activities

Micro-loan Disbursement and Portfolio Management

This core activity targets underserved borrowers via field agents and digital outreach, using traditional credit checks plus alternative data (mobile, bill payments, psychometric scores) to underwrite loans; Ujjivan Small Finance Bank reported a gross NPA of 1.34% and PCR 71.8% as of FY2024, reflecting disciplined underwriting. The bank handles lifecycle tasks—disbursement, EMI collection via group meetings or digital channels, and portfolio monitoring—to sustain ~97% recovery rates in stable months.

Deposit Mobilization and Liability Management

Ujjivan builds a granular deposit base via competitive savings and fixed-deposit rates, converting micro-borrowers to savers—retail deposits grew to 58% of liabilities by FY2024 (Dec 2024 data), lowering wholesale funding needs.

Daily liability management balances deposit cost against advance yields to protect NIMs; Ujjivan reported a NIM of 5.1% in FY2024, so funding mix and cost control are monitored continuously.

Digital Transformation and Platform Maintenance

Ujjivan prioritises continuous improvement of digital channels like the Hello Ujjivan app, adding voice and visual cues to aid semi-literate and first-time users; app active users rose to ~1.2 million by Dec 2025, a 35% YoY increase. Maintaining scalable cloud infra and 99.9% uptime supports its strategy to be a digital-first small finance bank, with digital transactions reaching ~48% of total volume in FY2025.

Regulatory Compliance and Risk Mitigation

The bank enforces continuous monitoring for KYC, AML, and priority sector lending rules from the Reserve Bank of India, with 2024 internal audits covering 100% of branches and reducing reportable compliance incidents by 28% year-on-year.

Risk assessments identify default hotspots early; credit-risk reviews cut NPA migration by 15 bps in FY2024, protecting the banking licence and depositor trust.

- 100% branches audited in 2024

- 28% drop in reportable incidents YoY

- NPA migration reduced 15 basis points FY2024

- Regular KYC/AML sweeps and PSL tracking

Financial Literacy and Community Outreach

Ujjivan runs large-scale financial literacy drives that in 2024 reached ~1.2 million clients across urban poor segments, raising formal savings uptake by 18% and cutting delinquency among trained borrowers by 9% year-over-year.

These outreach sessions act as first contact points, converting education into loyalty: trained households show 22% higher cross-sell rates and 14% larger average deposit balances.

- Reached ~1.2M clients in 2024

- Savings uptake +18% post-training

- Delinquency -9% among trained borrowers

- Cross-sell rate +22% vs untrained

- Avg deposit +14% for trained households

Digitally-driven lender: strong recovery, low NPAs, 58% retail deposits, 1.2M app users

Core activities: field and digital sourcing, alternative-data underwriting, disbursement/collection, deposit mobilisation, digital channel ops, compliance and risk monitoring, and large-scale financial literacy—supporting FY2024 metrics: gross NPA 1.34%, PCR 71.8%, NIM 5.1%, retail deposits 58% of liabilities, ~97% recovery, app users ~1.2M (Dec 2025), digital tx ~48% (FY2025).

| Metric | Value |

|---|---|

| Gross NPA (FY2024) | 1.34% |

| PCR (FY2024) | 71.8% |

| NIM (FY2024) | 5.1% |

| Retail deposits (FY2024) | 58% |

| Recovery rate | ~97% |

| App users (Dec 2025) | ~1.2M |

| Digital tx (FY2025) | ~48% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Ujjivan Business Model Canvas—not a mockup or sample—and shows the exact content and layout included in the final deliverable.

When you purchase, you’ll receive this same fully editable file, formatted and structured identically, ready for presentation, analysis, or customization.

No placeholders or hidden sections—what you see in the preview is what you will download and use immediately after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ujjivan Microfinance BMC: Customer-Centric Growth & Inclusion

Explore Ujjivan’s customer-focused microfinance engine with our concise Business Model Canvas—discover value propositions, distribution channels, and revenue levers that fuel growth in underserved markets and drive financial inclusion.

Partnerships

Fintech and Digital Payment Collaborators

Collaborations with fintechs let Ujjivan integrate instant payments and alternative credit scoring (e.g., transaction-based models), cutting onboarding time to under 10 minutes and raising digital loan approvals by 28% in 2024; third-party APIs also trimmed internal dev costs ~22%, keeping the bank competitive in India’s 2025 digital-payments market projected at $1.3 trillion.

Insurance and Third-Party Product Providers

Ujjivan partners with insurers like SBI Life and Tata AIA to sell life, health, and general policies via bancassurance, driving non‑interest income that was ~12% of FY2024 fee revenue and helping cover 1.9 million low‑income borrowers against shocks.

Business Correspondents and Field Agents

Strategic alliances with ~28,000 Business Correspondents (BCs) and field agents extend Ujjivan’s reach into remote areas, letting the bank avoid branch capex while serving last-mile customers; BCs handle cash deposits, withdrawals and basic accounts, supporting Ujjivan’s ~6.5 million active customers across semi-urban and rural India as of FY2024.

Regulatory and Industry Bodies

Active engagement with the Reserve Bank of India and the Small Finance Bank Association keeps Ujjivan aligned with evolving rules; as of FY2024 Ujjivan SFB reported a CRAR (capital to risk-weighted assets) of 19.6%, helping meet RBI capital adequacy norms.

These partnerships help navigate priority sector lending targets (40% for domestic banks); strong regulator ties boost institutional credibility and reduce regulatory friction, supporting steady operations and deposit growth (+12% YoY in FY2024).

- CRAR 19.6% (FY2024)

- Priority sector target 40%

- Deposit growth +12% YoY (FY2024)

Technology and Infrastructure Vendors

The bank relies on specialized IT vendors to run its core banking system and cloud infrastructure, delivering 99.95% uptime and PCI-DSS-level security to handle ~35 million annual transactions as of FY 2024.

These partners supply hardware/software updates and threat monitoring, reducing breach incidents by ~40% year-over-year and enabling scalable operations to support projected customer growth to ~6.5 million by 2026.

- 99.95% uptime

- ~35M transactions (FY2024)

- ~40% fewer breaches YoY

- Target ~6.5M customers by 2026

Partnership-fueled growth: 6.5M users, 35M txns, +12% deposits, 28% digital approvals

Key partnerships (fintechs, insurers, 28,000 BCs, IT vendors, RBI/SFBA) cut onboarding <10 mins, raised digital approvals +28% (2024), drove non‑interest income ~12% of fee revenue (FY2024), supported 6.5M active customers and 35M transactions (FY2024), CRAR 19.6%, deposits +12% YoY; uptime 99.95%, breaches -40% YoY.

| Metric | Value |

|---|---|

| Active customers | 6.5M (FY2024) |

| Transactions | 35M (FY2024) |

| CRAR | 19.6% (FY2024) |

| Deposit growth | +12% YoY (FY2024) |

What is included in the product

A comprehensive Business Model Canvas for Ujjivan Microfinance that maps customer segments, value propositions, channels, revenue streams, and key partners, reflecting real-world operations and strategic priorities.

High-level view of Ujjivan’s business model with editable cells, condensing its microfinance-to-banking strategy into a digestible one-page snapshot for quick review and team collaboration.

Activities

Micro-loan Disbursement and Portfolio Management

This core activity targets underserved borrowers via field agents and digital outreach, using traditional credit checks plus alternative data (mobile, bill payments, psychometric scores) to underwrite loans; Ujjivan Small Finance Bank reported a gross NPA of 1.34% and PCR 71.8% as of FY2024, reflecting disciplined underwriting. The bank handles lifecycle tasks—disbursement, EMI collection via group meetings or digital channels, and portfolio monitoring—to sustain ~97% recovery rates in stable months.

Deposit Mobilization and Liability Management

Ujjivan builds a granular deposit base via competitive savings and fixed-deposit rates, converting micro-borrowers to savers—retail deposits grew to 58% of liabilities by FY2024 (Dec 2024 data), lowering wholesale funding needs.

Daily liability management balances deposit cost against advance yields to protect NIMs; Ujjivan reported a NIM of 5.1% in FY2024, so funding mix and cost control are monitored continuously.

Digital Transformation and Platform Maintenance

Ujjivan prioritises continuous improvement of digital channels like the Hello Ujjivan app, adding voice and visual cues to aid semi-literate and first-time users; app active users rose to ~1.2 million by Dec 2025, a 35% YoY increase. Maintaining scalable cloud infra and 99.9% uptime supports its strategy to be a digital-first small finance bank, with digital transactions reaching ~48% of total volume in FY2025.

Regulatory Compliance and Risk Mitigation

The bank enforces continuous monitoring for KYC, AML, and priority sector lending rules from the Reserve Bank of India, with 2024 internal audits covering 100% of branches and reducing reportable compliance incidents by 28% year-on-year.

Risk assessments identify default hotspots early; credit-risk reviews cut NPA migration by 15 bps in FY2024, protecting the banking licence and depositor trust.

- 100% branches audited in 2024

- 28% drop in reportable incidents YoY

- NPA migration reduced 15 basis points FY2024

- Regular KYC/AML sweeps and PSL tracking

Financial Literacy and Community Outreach

Ujjivan runs large-scale financial literacy drives that in 2024 reached ~1.2 million clients across urban poor segments, raising formal savings uptake by 18% and cutting delinquency among trained borrowers by 9% year-over-year.

These outreach sessions act as first contact points, converting education into loyalty: trained households show 22% higher cross-sell rates and 14% larger average deposit balances.

- Reached ~1.2M clients in 2024

- Savings uptake +18% post-training

- Delinquency -9% among trained borrowers

- Cross-sell rate +22% vs untrained

- Avg deposit +14% for trained households

Digitally-driven lender: strong recovery, low NPAs, 58% retail deposits, 1.2M app users

Core activities: field and digital sourcing, alternative-data underwriting, disbursement/collection, deposit mobilisation, digital channel ops, compliance and risk monitoring, and large-scale financial literacy—supporting FY2024 metrics: gross NPA 1.34%, PCR 71.8%, NIM 5.1%, retail deposits 58% of liabilities, ~97% recovery, app users ~1.2M (Dec 2025), digital tx ~48% (FY2025).

| Metric | Value |

|---|---|

| Gross NPA (FY2024) | 1.34% |

| PCR (FY2024) | 71.8% |

| NIM (FY2024) | 5.1% |

| Retail deposits (FY2024) | 58% |

| Recovery rate | ~97% |

| App users (Dec 2025) | ~1.2M |

| Digital tx (FY2025) | ~48% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Ujjivan Business Model Canvas—not a mockup or sample—and shows the exact content and layout included in the final deliverable.

When you purchase, you’ll receive this same fully editable file, formatted and structured identically, ready for presentation, analysis, or customization.

No placeholders or hidden sections—what you see in the preview is what you will download and use immediately after purchase.