UMB Financial Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

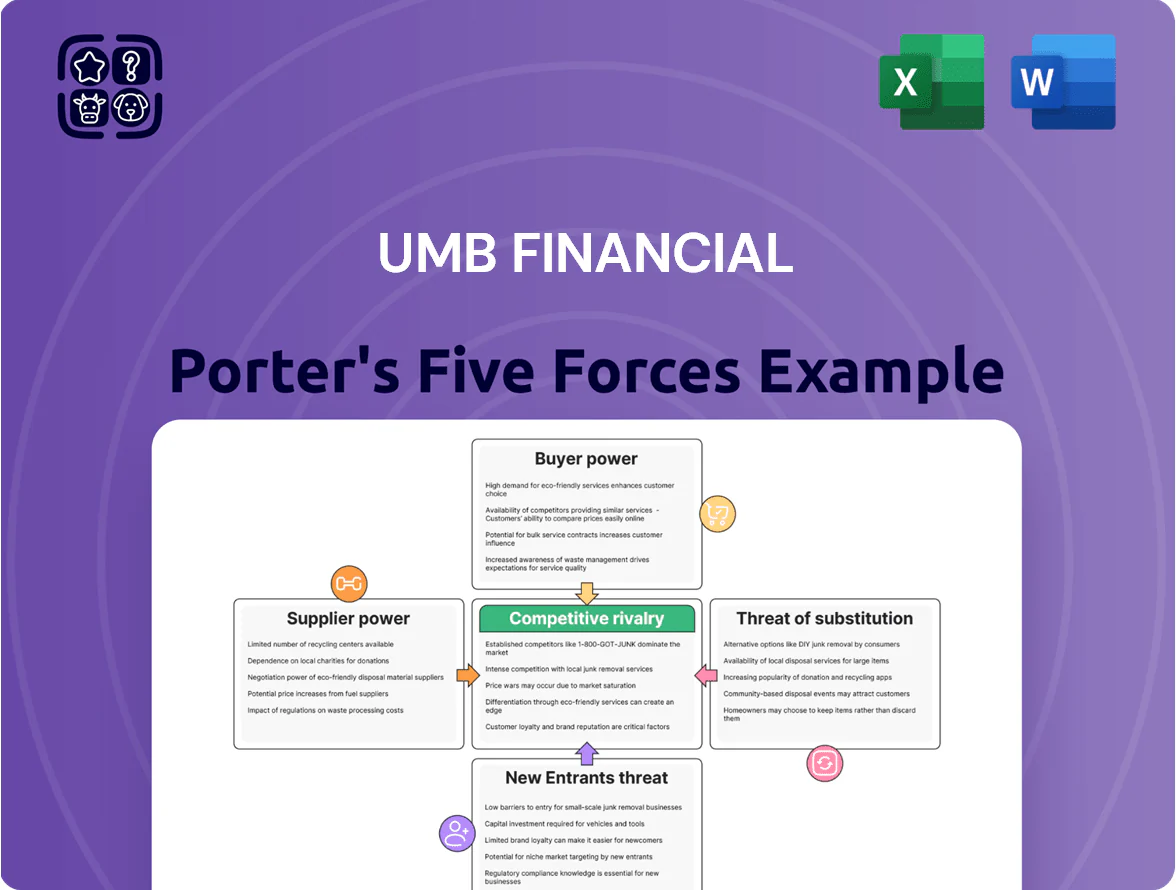

UMB Financial faces moderate buyer power and regulatory pressure, with competitive rivalry intensified by regional banks and fintech entrants; supplier and substitute threats are manageable but evolving as digital channels grow.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore UMB Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Technology and Core Banking Providers

UMB’s reliance on third-party core banking and digital platforms gives suppliers moderate power because vendors like Jack Henry and Fiserv supply mission‑critical systems, creating high switching costs and multi‑year integration projects.

As of Q4 2025, 70% of US regional banks use one of the top three core providers, concentrating influence and pricing power among a few firms.

The rising demand for AI and advanced cybersecurity—UMB spent $42m on IT security in 2024—increases vendor leverage as specialized capabilities are scarce and expensive to replicate.

Access to Diverse Funding Sources and Depositors

Depositors are UMB Financial’s primary capital suppliers, and their bargaining power rises with rate cycles and tight liquidity; in 2025, institutional deposits sought yields up ~150–200 basis points above retail, pressuring net interest margin (UMB reported NIM 2.45% in Q4 2024).

Sophisticated depositors’ demand for higher yields gives them leverage to shift balances; UMB must offer competitive term rates while keeping low-cost core deposits—core deposit ratio was ~62% in 2024—to protect profitability.

Competition for Highly Skilled Financial Talent

The regional supply of specialized labor—especially in wealth management and commercial lending—directly limits UMB’s growth; Kansas City and Midwestern markets report a 12% shortfall in senior relationship managers vs. demand in 2024, per Mercer talent data.

As services go tech‑centric, demand for dual finance+data analytics pros rose 28% YoY in 2023–24, driving fierce poaching by banks and fintechs.

UMB responds with aggressive pay: median total comp for senior RMs climbed to roughly $220,000 in 2024, up 9% year-over-year, plus enhanced benefits and retention bonuses to hold top analysts and originators.

Regulatory and Compliance Oversight

Government and regulatory bodies serve as non-market suppliers of licenses and the legal framework UMB Financial needs to operate, raising supplier power as regulators tightened capital and liquidity rules across US regional banks through 2023–2025.

Heightened scrutiny and higher capital ratios forced UMB to absorb fixed compliance costs; meeting Basel-related guidance and FDIC/CID expectations increased regulatory-driven expense pressure on margins.

- Regulatory tightening 2023–2025

- Higher capital ratio targets (e.g., CET1 up vs pre-2023)

- Compliance = fixed cost pressure

Cybersecurity and Data Protection Services

As cyber threats rise, top-tier cybersecurity and breach insurance vendors command pricing power; global cybersecurity spending hit an estimated $188.3 billion in 2023 and banks often spend 10–15% of IT budgets on security, so UMB Financial must fund enterprise-grade defenses to shield $70+ billion in client assets under custody (2024 figure).

Few firms meet financial-grade standards (SOC 2, FFIEC guidelines), keeping supplier leverage high and making multi-year contracts and vendor concentration key negotiation risks for UMB.

- 2023 global security spend: $188.3B

- Typical bank security spend: 10–15% of IT budget

- UMB assets under custody: >$70B (2024)

- Few enterprise vendors → elevated supplier power

Core vendors, talent gaps, and rising yields squeeze regionals: security costs, NIM hit

Suppliers hold moderate–high power: core vendors (Jack Henry, Fiserv) create high switching costs; 70% of regionals use top-three cores (Q4 2025). Specialized AI/cyber vendors and talent shortages (12% RM shortfall, 2024) raise costs—UMB spent $42m on security in 2024; NIM pressure from depositors seeking +150–200 bps in 2025.

| Metric | Value |

|---|---|

| Core vendor share (regionals) | 70% (Q4 2025) |

| UMB IT security spend | $42m (2024) |

| Institutional deposit yield gap | +150–200 bps (2025) |

| Senior RM shortfall | 12% (2024) |

What is included in the product

Delivers a concise Porter’s Five Forces assessment of UMB Financial, highlighting competitive rivalry, customer and supplier leverage, entry barriers, and substitutes to clarify strategic risks and profitability drivers.

One-sheet Porter's Five Forces for UMB Financial—quickly spot competitive pressures and prioritize strategic actions to reduce risk and enhance margins.

Customers Bargaining Power

Low Switching Costs for Retail Banking Clients

Retail customers face low switching costs as fintechs and banks report a 35% rise in account openings via mobile apps from 2020–2024, and digital transfers (ACH, Zelle) make moving funds instant; UMB must match that ease to retain deposits.

High-yield online savings rates averaged 3.8% in 2025 versus national brick-and-mortar averages near 1.2%, pressuring UMB to offer competitive yields or features.

Mobile-first features now drive loyalty: by end-2025, 68% of retail customers cited app convenience over branch location when choosing a primary bank, so UMB’s UX is key to retention.

High Leverage of Middle Market Commercial Clients

UMB’s middle-market focus means clients often hold multiple bank relationships and $5m–$100m+ credit lines, giving them strong leverage to demand lower rates or improved covenants; industry data shows 62% of mid-market firms negotiate pricing using competing bank offers. To retain these clients, UMB must deliver tailored treasury management and advisory services—cash forecasting, receivables automation, strategic financing—so pricing pressure is offset by fee income and deeper wallet share.

Institutional Demands in Fund Services

Institutional clients using UMB for fund accounting and custody wield high bargaining power because their assets under custody often exceed $1bn per client; in 2024, top 10 institutional relationships accounted for roughly 35% of UMB’s custody balances. These clients demand volume-based pricing and bespoke reporting tied to strategy, pushing UMB to add API-driven reporting and fee tiers. If UMB lags, large clients can shift to specialized boutiques offering lower fees or niche analytics.

Information Symmetry and Financial Literacy

- Real-time data erodes information gaps

- Average advisory fee ~0.55% AUM (2024)

- ETF inflows $1.2T (2024) show price sensitivity

- UMB needs clear net-return reporting

Price Sensitivity in Wealth Management

High-net-worth clients increasingly push back on management fees as 60% of U.S. HNW investors surveyed in 2024 cited fee compression as a top concern; many benchmark performance to low-cost S&P 500 ETFs returning 18.4% in 2023–2024, raising expectations for net-of-fee outperformance.

UMB’s tailored trust and wealth offerings face pressure from robo-advisors and discount brokers that grew AUM by double digits in 2023, letting clients demand lower fees or risk-based pricing.

Personal relationships still win referrals, but they rarely cover persistent fee or performance gaps; a 2024 study found 42% of HNW clients would switch for 25–50 bps lower fees plus parity vs passive returns.

- 60% HNW fee concern (2024)

- S&P 500 ETFs +18.4% (2023–2024)

- Robo/discount AUM double-digit growth (2023)

- 42% would switch for 25–50 bps saving (2024)

Digital-savvy clients force UMB to match rates, UX & bespoke services—retain wallet share

Customers hold strong bargaining power: digital ease and real-time data (68% mobile preference, 35% rise in mobile account openings 2020–24) lower switching costs; high-yield online rates (3.8% in 2025) and advisory fee compression (~0.55% AUM in 2024) force UMB to match pricing, UX, and bespoke services for mid-market and institutional clients to retain wallet share.

| Metric | Value |

|---|---|

| Mobile preference (retail) | 68% (2025) |

| Mobile account openings | +35% (2020–24) |

| High-yield online rate | 3.8% (2025) |

| Avg advisory fee | 0.55% AUM (2024) |

Preview the Actual Deliverable

UMB Financial Porter's Five Forces Analysis

This preview shows the exact UMB Financial Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full document is professionally formatted, ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

UMB Financial faces moderate buyer power and regulatory pressure, with competitive rivalry intensified by regional banks and fintech entrants; supplier and substitute threats are manageable but evolving as digital channels grow.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore UMB Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Technology and Core Banking Providers

UMB’s reliance on third-party core banking and digital platforms gives suppliers moderate power because vendors like Jack Henry and Fiserv supply mission‑critical systems, creating high switching costs and multi‑year integration projects.

As of Q4 2025, 70% of US regional banks use one of the top three core providers, concentrating influence and pricing power among a few firms.

The rising demand for AI and advanced cybersecurity—UMB spent $42m on IT security in 2024—increases vendor leverage as specialized capabilities are scarce and expensive to replicate.

Access to Diverse Funding Sources and Depositors

Depositors are UMB Financial’s primary capital suppliers, and their bargaining power rises with rate cycles and tight liquidity; in 2025, institutional deposits sought yields up ~150–200 basis points above retail, pressuring net interest margin (UMB reported NIM 2.45% in Q4 2024).

Sophisticated depositors’ demand for higher yields gives them leverage to shift balances; UMB must offer competitive term rates while keeping low-cost core deposits—core deposit ratio was ~62% in 2024—to protect profitability.

Competition for Highly Skilled Financial Talent

The regional supply of specialized labor—especially in wealth management and commercial lending—directly limits UMB’s growth; Kansas City and Midwestern markets report a 12% shortfall in senior relationship managers vs. demand in 2024, per Mercer talent data.

As services go tech‑centric, demand for dual finance+data analytics pros rose 28% YoY in 2023–24, driving fierce poaching by banks and fintechs.

UMB responds with aggressive pay: median total comp for senior RMs climbed to roughly $220,000 in 2024, up 9% year-over-year, plus enhanced benefits and retention bonuses to hold top analysts and originators.

Regulatory and Compliance Oversight

Government and regulatory bodies serve as non-market suppliers of licenses and the legal framework UMB Financial needs to operate, raising supplier power as regulators tightened capital and liquidity rules across US regional banks through 2023–2025.

Heightened scrutiny and higher capital ratios forced UMB to absorb fixed compliance costs; meeting Basel-related guidance and FDIC/CID expectations increased regulatory-driven expense pressure on margins.

- Regulatory tightening 2023–2025

- Higher capital ratio targets (e.g., CET1 up vs pre-2023)

- Compliance = fixed cost pressure

Cybersecurity and Data Protection Services

As cyber threats rise, top-tier cybersecurity and breach insurance vendors command pricing power; global cybersecurity spending hit an estimated $188.3 billion in 2023 and banks often spend 10–15% of IT budgets on security, so UMB Financial must fund enterprise-grade defenses to shield $70+ billion in client assets under custody (2024 figure).

Few firms meet financial-grade standards (SOC 2, FFIEC guidelines), keeping supplier leverage high and making multi-year contracts and vendor concentration key negotiation risks for UMB.

- 2023 global security spend: $188.3B

- Typical bank security spend: 10–15% of IT budget

- UMB assets under custody: >$70B (2024)

- Few enterprise vendors → elevated supplier power

Core vendors, talent gaps, and rising yields squeeze regionals: security costs, NIM hit

Suppliers hold moderate–high power: core vendors (Jack Henry, Fiserv) create high switching costs; 70% of regionals use top-three cores (Q4 2025). Specialized AI/cyber vendors and talent shortages (12% RM shortfall, 2024) raise costs—UMB spent $42m on security in 2024; NIM pressure from depositors seeking +150–200 bps in 2025.

| Metric | Value |

|---|---|

| Core vendor share (regionals) | 70% (Q4 2025) |

| UMB IT security spend | $42m (2024) |

| Institutional deposit yield gap | +150–200 bps (2025) |

| Senior RM shortfall | 12% (2024) |

What is included in the product

Delivers a concise Porter’s Five Forces assessment of UMB Financial, highlighting competitive rivalry, customer and supplier leverage, entry barriers, and substitutes to clarify strategic risks and profitability drivers.

One-sheet Porter's Five Forces for UMB Financial—quickly spot competitive pressures and prioritize strategic actions to reduce risk and enhance margins.

Customers Bargaining Power

Low Switching Costs for Retail Banking Clients

Retail customers face low switching costs as fintechs and banks report a 35% rise in account openings via mobile apps from 2020–2024, and digital transfers (ACH, Zelle) make moving funds instant; UMB must match that ease to retain deposits.

High-yield online savings rates averaged 3.8% in 2025 versus national brick-and-mortar averages near 1.2%, pressuring UMB to offer competitive yields or features.

Mobile-first features now drive loyalty: by end-2025, 68% of retail customers cited app convenience over branch location when choosing a primary bank, so UMB’s UX is key to retention.

High Leverage of Middle Market Commercial Clients

UMB’s middle-market focus means clients often hold multiple bank relationships and $5m–$100m+ credit lines, giving them strong leverage to demand lower rates or improved covenants; industry data shows 62% of mid-market firms negotiate pricing using competing bank offers. To retain these clients, UMB must deliver tailored treasury management and advisory services—cash forecasting, receivables automation, strategic financing—so pricing pressure is offset by fee income and deeper wallet share.

Institutional Demands in Fund Services

Institutional clients using UMB for fund accounting and custody wield high bargaining power because their assets under custody often exceed $1bn per client; in 2024, top 10 institutional relationships accounted for roughly 35% of UMB’s custody balances. These clients demand volume-based pricing and bespoke reporting tied to strategy, pushing UMB to add API-driven reporting and fee tiers. If UMB lags, large clients can shift to specialized boutiques offering lower fees or niche analytics.

Information Symmetry and Financial Literacy

- Real-time data erodes information gaps

- Average advisory fee ~0.55% AUM (2024)

- ETF inflows $1.2T (2024) show price sensitivity

- UMB needs clear net-return reporting

Price Sensitivity in Wealth Management

High-net-worth clients increasingly push back on management fees as 60% of U.S. HNW investors surveyed in 2024 cited fee compression as a top concern; many benchmark performance to low-cost S&P 500 ETFs returning 18.4% in 2023–2024, raising expectations for net-of-fee outperformance.

UMB’s tailored trust and wealth offerings face pressure from robo-advisors and discount brokers that grew AUM by double digits in 2023, letting clients demand lower fees or risk-based pricing.

Personal relationships still win referrals, but they rarely cover persistent fee or performance gaps; a 2024 study found 42% of HNW clients would switch for 25–50 bps lower fees plus parity vs passive returns.

- 60% HNW fee concern (2024)

- S&P 500 ETFs +18.4% (2023–2024)

- Robo/discount AUM double-digit growth (2023)

- 42% would switch for 25–50 bps saving (2024)

Digital-savvy clients force UMB to match rates, UX & bespoke services—retain wallet share

Customers hold strong bargaining power: digital ease and real-time data (68% mobile preference, 35% rise in mobile account openings 2020–24) lower switching costs; high-yield online rates (3.8% in 2025) and advisory fee compression (~0.55% AUM in 2024) force UMB to match pricing, UX, and bespoke services for mid-market and institutional clients to retain wallet share.

| Metric | Value |

|---|---|

| Mobile preference (retail) | 68% (2025) |

| Mobile account openings | +35% (2020–24) |

| High-yield online rate | 3.8% (2025) |

| Avg advisory fee | 0.55% AUM (2024) |

Preview the Actual Deliverable

UMB Financial Porter's Five Forces Analysis

This preview shows the exact UMB Financial Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full document is professionally formatted, ready for download and use the moment you buy.