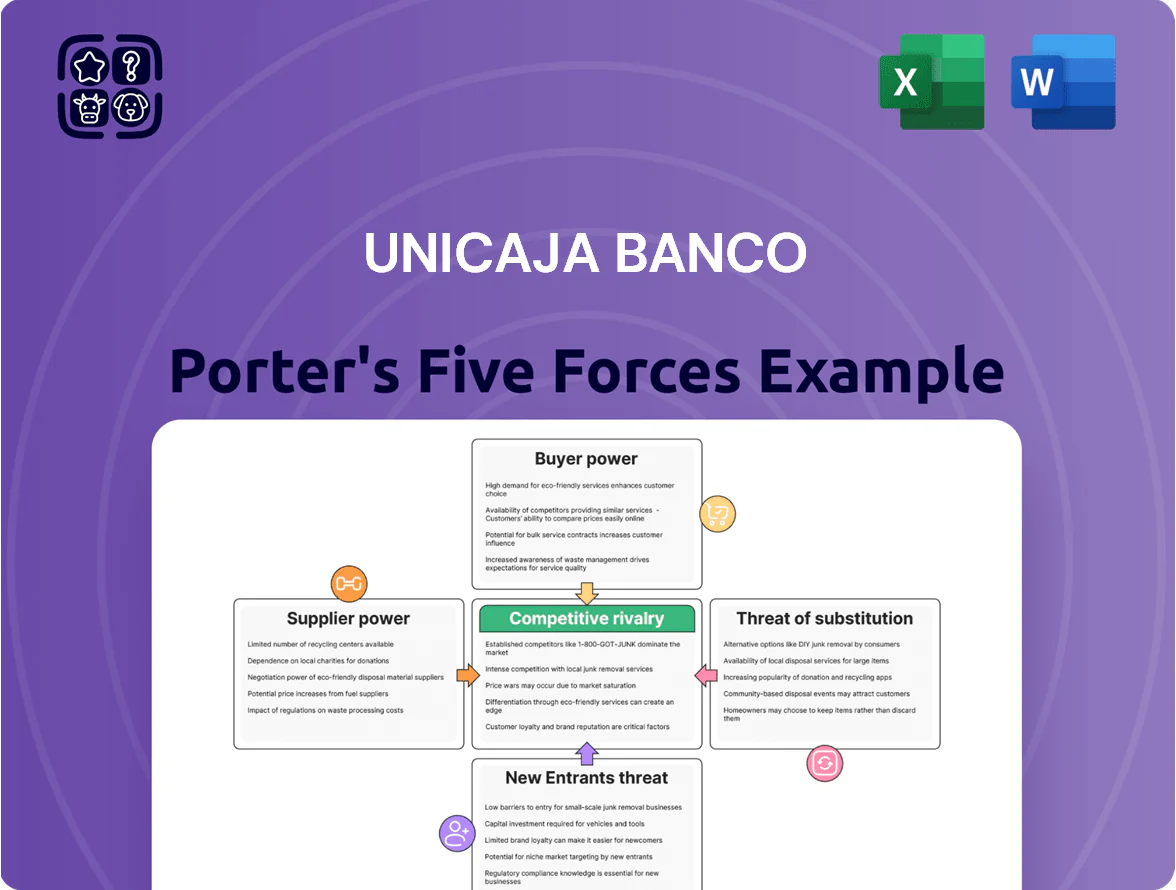

Unicaja Banco Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Unicaja Banco faces moderate buyer power and regulatory pressures, balanced by strong regional brand presence and scale advantages, while digital entrants and fintechs create an accelerating substitute threat that management must counter with innovation and cost discipline. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Unicaja Banco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital Providers and Depositors

Individual and corporate depositors are Unicaja Banco’s main capital suppliers; as of Q4 2025 retail deposits made up about 68% of funding and sight deposits €22.4bn. Their bargaining power is moderate because customers can shift to high-yield accounts or neobanks if rates lag—Spain’s online savings rates rose to 1.8% median in 2025. Still, Unicaja’s stable core deposits in Andalusia and Castilla-La Mancha limit sudden outflows.

Technology and Digital Infrastructure Vendors

Unicaja Banco depends on third-party core-banking, cloud, and cybersecurity vendors, creating high supplier power because switching costs exceed €50–100m for core system migrations and migrations can take 18–36 months. In 2024 Spanish banks spent ~0.8–1.2% of assets on IT; Unicaja must match peers while containing costs to avoid lagging larger European rivals that invest €200–400m yearly in digital platforms.

Human Capital and Specialized Labor

Limited supply of data science, AI, and compliance experts in Spain gives these workers and specialist recruiters leverage over pay and perks; Unicaja Banco faces average tech hire salary premiums of 20–35% versus general banking roles as of 2025.

Regulatory and Central Bank Influence

The European Central Bank (ECB) is a key supplier of liquidity and sets wholesale funding costs; its deposit facility rate of 3.75% and main refinancing rate of 4.00% (Dec 2025 target range references) directly affect Unicaja Banco’s net interest margin and the cost of the loans it funds.

ECB reserve requirements and macroprudential rules force Unicaja to hold more high-quality liquid assets, raising funding costs and compressing return on assets; supervisors (ECB/SAN) can restrict dividends or require capital buffers, so regulators effectively control the institutional framework.

- ECB policy rates: 4.00% (refi), 3.75% (deposit)

- Higher reserve/liquidity rules ↑ funding cost, ↓ NIM

- Supervisors can impose capital/dividend limits

- Regulatory power > unilateral supplier influence

Rating Agencies and Credit Markets

Institutional investors and rating agencies enable Unicaja Banco to access wholesale debt; as of 2025 the bank held €2.5bn senior debt outstanding, so ratings moves matter.

A downgrade would raise bond yields—past EMU bank downgrades lifted spreads by 150–300bps—cutting net interest margin and profits.

To avoid that, Unicaja keeps CET1 around 12.5% (2025 target) and publishes quarterly IFRS accounts and liquidity ratios.

- €2.5bn senior debt outstanding (2025)

- CET1 ~12.5% target (2025)

- Rating shifts can add 150–300bps to bond spreads

- Requires transparent IFRS reporting and strict capital buffers

Unicaja: Strong low‑cost deposits vs. neo‑bank churn, tech costs and ECB constraints

Suppliers’ bargaining power is mixed: retail deposits (68% of funding; sight deposits €22.4bn, Q4 2025) give Unicaja stable, low-cost funding, but customers can switch to neobanks if rates lag (median online savings 1.8% in 2025). Tech/core-banking vendors and scarce AI/compliance talent raise switching costs (~€50–100m) and wage premiums (20–35%). ECB policy (refi 4.00%, deposit 3.75%) and regulators strongly constrain funding and capital.

| Item | Value (2025) |

|---|---|

| Retail deposits share | 68% |

| Sight deposits | €22.4bn |

| Online savings median | 1.8% |

| Core IT migration cost | €50–100m |

| Tech hire premium | 20–35% |

| ECB refi / deposit | 4.00% / 3.75% |

What is included in the product

Tailored Porter's Five Forces assessment for Unicaja Banco, uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes, and emerging threats with strategic commentary and industry context.

A concise Porter's Five Forces snapshot for Unicaja Banco—ideal for quick strategic decisions and boardroom use.

Customers Bargaining Power

Low Switching Costs for Retail Clients

In 2025 Spain’s open banking and account portability rules let retail clients switch banks in days, and 38% of Spanish adults said they’d consider switching for lower fees or better apps (2024 Banco de España survey). Low switching costs raise customer bargaining power, so Unicaja Banco must boost loyalty programs and hyper-local branch services to retain clients and counter neobank churn.

Price Sensitivity in Mortgage and Loan Markets

Borrowers wield strong bargaining power as digital comparison platforms (e.g., Rastreator, 2024) show Spain’s average mortgage rates fell to 2.1% in 2024, letting customers shop for lowest APRs. Mortgages are core for Unicaja Banco, so competitive pressure forces margin compression—Unicaja’s net interest margin was 1.15% in 2024, below national peer average of 1.35%. Clients often present rival offers to secure better terms on personal and commercial loans.

Corporate Client Negotiating Leverage

Large corporates and institutions control high-volume flows—Unicaja saw corporate deposits of €8.2bn in 2024—so they can demand tailored products and fee cuts.

These clients use multiple banks; in Spain 68% of firms had three+ banking relationships in 2023, letting them play lenders off each other.

To keep these accounts Unicaja must provide advanced treasury, FX and M&A advisory; losing one €500m client can cut net interest income materially.

Demand for Digital and User-Centric Experiences

Modern customers expect seamless mobile integration and 24/7 access, which shifts power to providers with the best user experience; 83% of Spanish retail bank customers used mobile banking in 2024, so UX drives retention.

If Unicaja’s app lags fintechs, customers can move primary banking elsewhere—Spain saw a 12% rise in fintech account switches in 2023—forcing churn risk.

This trend forces ongoing investment: Unicaja must fund UI/UX upgrades and personalized digital marketing; digital transformation budgets in European banks averaged 10–15% of IT spend in 2024.

- 83% mobile banking usage (Spain, 2024)

- 12% fintech account switches (Spain, 2023)

- 10–15% of IT spend on digital transformation (Europe, 2024)

Impact of Financial Literacy and Transparency

Greater access to financial data lets Spanish retail investors and advisers compare fees and fund returns; by 2024 62% of Spanish adults used online banking, raising scrutiny on opaque charges.

That transparency trims Unicaja Banco’s margin leeway from hidden fees and weak funds; the bank reported €36.7bn AUM in 2024, so retention depends on performance.

Unicaja must show clear value—lower fees, net returns above peers, and transparent reporting—to keep assets under management.

- 62% online banking use in Spain (2024)

- €36.7bn AUM (Unicaja, 2024)

- Lower opaque fees → narrower margins

- Performance + transparency = retention

Unicaja must boost UX, loyalty & advisory to stem fee-driven churn of 38%

Customer bargaining power is high: 38% would switch for fees/apps (Banco de España, 2024), 83% used mobile banking (2024), fintech switches rose 12% (2023), and Unicaja NIM was 1.15% vs peer 1.35% (2024). To retain clients Unicaja must invest in UX, loyalty and advisory for €36.7bn AUM (2024).

| Metric | Value |

|---|---|

| Switch intent | 38% (2024) |

| Mobile use | 83% (2024) |

| Fintech switches | 12% (2023) |

| NIM | 1.15% (Unicaja, 2024) |

| AUM | €36.7bn (2024) |

Same Document Delivered

Unicaja Banco Porter's Five Forces Analysis

This preview shows the exact Unicaja Banco Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups; it’s fully formatted and ready for use. The document displayed here is the complete, professionally written file covering competitive rivalry, threat of new entrants, supplier and buyer power, and substitutes, available for instant download upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Unicaja Banco faces moderate buyer power and regulatory pressures, balanced by strong regional brand presence and scale advantages, while digital entrants and fintechs create an accelerating substitute threat that management must counter with innovation and cost discipline. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Unicaja Banco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital Providers and Depositors

Individual and corporate depositors are Unicaja Banco’s main capital suppliers; as of Q4 2025 retail deposits made up about 68% of funding and sight deposits €22.4bn. Their bargaining power is moderate because customers can shift to high-yield accounts or neobanks if rates lag—Spain’s online savings rates rose to 1.8% median in 2025. Still, Unicaja’s stable core deposits in Andalusia and Castilla-La Mancha limit sudden outflows.

Technology and Digital Infrastructure Vendors

Unicaja Banco depends on third-party core-banking, cloud, and cybersecurity vendors, creating high supplier power because switching costs exceed €50–100m for core system migrations and migrations can take 18–36 months. In 2024 Spanish banks spent ~0.8–1.2% of assets on IT; Unicaja must match peers while containing costs to avoid lagging larger European rivals that invest €200–400m yearly in digital platforms.

Human Capital and Specialized Labor

Limited supply of data science, AI, and compliance experts in Spain gives these workers and specialist recruiters leverage over pay and perks; Unicaja Banco faces average tech hire salary premiums of 20–35% versus general banking roles as of 2025.

Regulatory and Central Bank Influence

The European Central Bank (ECB) is a key supplier of liquidity and sets wholesale funding costs; its deposit facility rate of 3.75% and main refinancing rate of 4.00% (Dec 2025 target range references) directly affect Unicaja Banco’s net interest margin and the cost of the loans it funds.

ECB reserve requirements and macroprudential rules force Unicaja to hold more high-quality liquid assets, raising funding costs and compressing return on assets; supervisors (ECB/SAN) can restrict dividends or require capital buffers, so regulators effectively control the institutional framework.

- ECB policy rates: 4.00% (refi), 3.75% (deposit)

- Higher reserve/liquidity rules ↑ funding cost, ↓ NIM

- Supervisors can impose capital/dividend limits

- Regulatory power > unilateral supplier influence

Rating Agencies and Credit Markets

Institutional investors and rating agencies enable Unicaja Banco to access wholesale debt; as of 2025 the bank held €2.5bn senior debt outstanding, so ratings moves matter.

A downgrade would raise bond yields—past EMU bank downgrades lifted spreads by 150–300bps—cutting net interest margin and profits.

To avoid that, Unicaja keeps CET1 around 12.5% (2025 target) and publishes quarterly IFRS accounts and liquidity ratios.

- €2.5bn senior debt outstanding (2025)

- CET1 ~12.5% target (2025)

- Rating shifts can add 150–300bps to bond spreads

- Requires transparent IFRS reporting and strict capital buffers

Unicaja: Strong low‑cost deposits vs. neo‑bank churn, tech costs and ECB constraints

Suppliers’ bargaining power is mixed: retail deposits (68% of funding; sight deposits €22.4bn, Q4 2025) give Unicaja stable, low-cost funding, but customers can switch to neobanks if rates lag (median online savings 1.8% in 2025). Tech/core-banking vendors and scarce AI/compliance talent raise switching costs (~€50–100m) and wage premiums (20–35%). ECB policy (refi 4.00%, deposit 3.75%) and regulators strongly constrain funding and capital.

| Item | Value (2025) |

|---|---|

| Retail deposits share | 68% |

| Sight deposits | €22.4bn |

| Online savings median | 1.8% |

| Core IT migration cost | €50–100m |

| Tech hire premium | 20–35% |

| ECB refi / deposit | 4.00% / 3.75% |

What is included in the product

Tailored Porter's Five Forces assessment for Unicaja Banco, uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes, and emerging threats with strategic commentary and industry context.

A concise Porter's Five Forces snapshot for Unicaja Banco—ideal for quick strategic decisions and boardroom use.

Customers Bargaining Power

Low Switching Costs for Retail Clients

In 2025 Spain’s open banking and account portability rules let retail clients switch banks in days, and 38% of Spanish adults said they’d consider switching for lower fees or better apps (2024 Banco de España survey). Low switching costs raise customer bargaining power, so Unicaja Banco must boost loyalty programs and hyper-local branch services to retain clients and counter neobank churn.

Price Sensitivity in Mortgage and Loan Markets

Borrowers wield strong bargaining power as digital comparison platforms (e.g., Rastreator, 2024) show Spain’s average mortgage rates fell to 2.1% in 2024, letting customers shop for lowest APRs. Mortgages are core for Unicaja Banco, so competitive pressure forces margin compression—Unicaja’s net interest margin was 1.15% in 2024, below national peer average of 1.35%. Clients often present rival offers to secure better terms on personal and commercial loans.

Corporate Client Negotiating Leverage

Large corporates and institutions control high-volume flows—Unicaja saw corporate deposits of €8.2bn in 2024—so they can demand tailored products and fee cuts.

These clients use multiple banks; in Spain 68% of firms had three+ banking relationships in 2023, letting them play lenders off each other.

To keep these accounts Unicaja must provide advanced treasury, FX and M&A advisory; losing one €500m client can cut net interest income materially.

Demand for Digital and User-Centric Experiences

Modern customers expect seamless mobile integration and 24/7 access, which shifts power to providers with the best user experience; 83% of Spanish retail bank customers used mobile banking in 2024, so UX drives retention.

If Unicaja’s app lags fintechs, customers can move primary banking elsewhere—Spain saw a 12% rise in fintech account switches in 2023—forcing churn risk.

This trend forces ongoing investment: Unicaja must fund UI/UX upgrades and personalized digital marketing; digital transformation budgets in European banks averaged 10–15% of IT spend in 2024.

- 83% mobile banking usage (Spain, 2024)

- 12% fintech account switches (Spain, 2023)

- 10–15% of IT spend on digital transformation (Europe, 2024)

Impact of Financial Literacy and Transparency

Greater access to financial data lets Spanish retail investors and advisers compare fees and fund returns; by 2024 62% of Spanish adults used online banking, raising scrutiny on opaque charges.

That transparency trims Unicaja Banco’s margin leeway from hidden fees and weak funds; the bank reported €36.7bn AUM in 2024, so retention depends on performance.

Unicaja must show clear value—lower fees, net returns above peers, and transparent reporting—to keep assets under management.

- 62% online banking use in Spain (2024)

- €36.7bn AUM (Unicaja, 2024)

- Lower opaque fees → narrower margins

- Performance + transparency = retention

Unicaja must boost UX, loyalty & advisory to stem fee-driven churn of 38%

Customer bargaining power is high: 38% would switch for fees/apps (Banco de España, 2024), 83% used mobile banking (2024), fintech switches rose 12% (2023), and Unicaja NIM was 1.15% vs peer 1.35% (2024). To retain clients Unicaja must invest in UX, loyalty and advisory for €36.7bn AUM (2024).

| Metric | Value |

|---|---|

| Switch intent | 38% (2024) |

| Mobile use | 83% (2024) |

| Fintech switches | 12% (2023) |

| NIM | 1.15% (Unicaja, 2024) |

| AUM | €36.7bn (2024) |

Same Document Delivered

Unicaja Banco Porter's Five Forces Analysis

This preview shows the exact Unicaja Banco Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups; it’s fully formatted and ready for use. The document displayed here is the complete, professionally written file covering competitive rivalry, threat of new entrants, supplier and buyer power, and substitutes, available for instant download upon payment.