Unilever Porter's Five Forces Analysis

Don't Miss the Bigger Picture

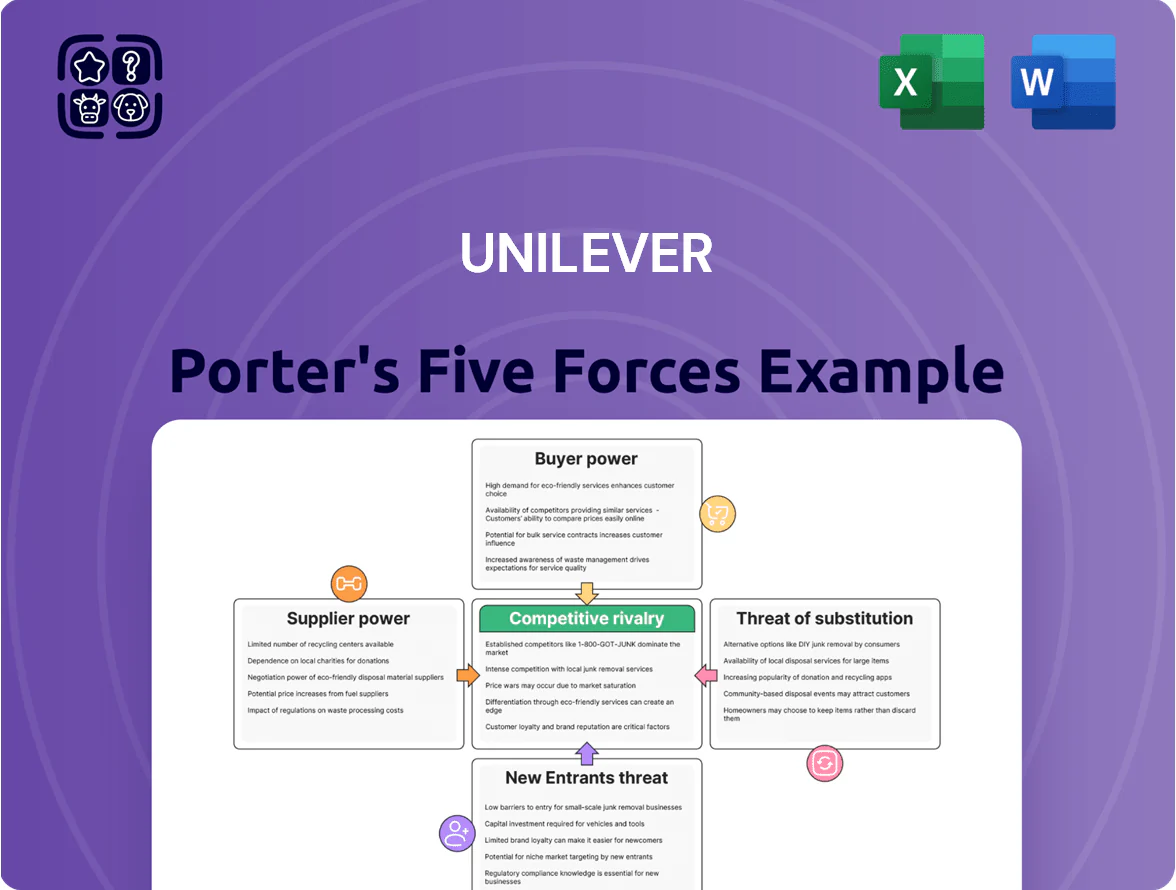

Unilever faces intense rivalry from global and local consumer goods players, moderate supplier power due to scale, strong buyer power driven by retailer consolidation, low threat of new entrants because of high brand and distribution barriers, and rising substitute threats from niche, eco-conscious brands—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Unilever’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale driven procurement leverage

Unilever runs procurement across 190+ countries and more than 70,000 suppliers, giving scale-driven leverage to push supplier margins lower; centralized buying cut input cost volatility by ~6% in 2024 and targets similar gains through 2025.

Diversified sourcing and risk management

Unilever has cut supplier power by diversifying inputs across 190+ sourcing countries and 1,000s of suppliers, reducing reliance on any single region or vendor; in 2024 sourced agricultural commodities rose 8% from South America while chemical buys widened to Asia, lowering concentration risk.

Impact of raw material price volatility

While Unilever is a major buyer, 2024–2025 commodity swings—rapeseed oil up 38% YoY in 2024 and key surfactant costs rising ~22%—have temporarily shifted leverage to suppliers, especially during short supply windows.

By late 2025 Unilever increased long-term hedges and struck multi-year sourcing deals covering ~30% of vegetable-oil needs, reflecting strategic partnerships to dampen volatility.

These moves keep Unilever dominant, but the essential nature of some inputs gives suppliers a baseline influence that can spike margins short-term.

Strict sustainability and compliance standards

Unilever enforces strict environmental and social governance standards that suppliers must meet to keep contracts, shrinking the eligible vendor pool but raising switching costs.

Suppliers often invest in capital and certification to meet Unilever’s 2025 targets (net-zero by 2039, 100% recyclable packaging by 2025), so losing Unilever after those investments would be costly, binding them closer to the company.

Low switching costs for standardized inputs

For most of Unilever’s commodity inputs—palm oil, surfactants, bulk fragrances—switching suppliers is easy and low-cost, keeping supplier leverage weak; in 2024 Unilever sourced over 60% of key commodities from 100+ global vendors, limiting price pressure.

Portability of standard packaging and ingredients, plus multi-sourcing and spot-market purchases, prevents suppliers from imposing steep premiums or restrictive terms, so supplier power is low to moderate.

- Many suppliers: 100+ global vendors for core commodities

- High spot buying: significant use of commodities markets in 2024

- Low switching costs: modular packaging and standard ingredients

- Supplier power: low–moderate, limited price-setting ability

Unilever’s buying scale tempers supplier power despite 2024 commodity spike

Unilever’s scale (70,000+ suppliers, procurement in 190+ countries) keeps supplier power low–moderate; 2024 centralized buying cut input volatility ~6% while commodity shocks (rapeseed +38% YoY; surfactants +22%) raised short-term supplier leverage. ESG rules and CAPEX raise switching costs; multi-sourcing and 100+ vendors for core commodities limit price-setting.

| Metric | 2024/2025 |

|---|---|

| Suppliers | 70,000+ |

| Countries | 190+ |

| Centralized buying impact | -6% volatility 2024 |

| Rapeseed oil | +38% YoY 2024 |

| Surfactants | +22% 2024 |

| Hedged vegetable oil | ~30% by late 2025 |

What is included in the product

Unilever-specific Porter's Five Forces analysis revealing competitive intensity, buyer/supplier power, substitution threats, and entry barriers, with strategic insights on disruptive trends and implications for pricing and profitability.

A concise Porter's Five Forces snapshot for Unilever—distills supplier, buyer, rivalry, entrant, and substitute pressures into one actionable view for swift strategic decisions.

Customers Bargaining Power

Retailer concentration and shelf space control

Major chains like Walmart, Carrefour and Tesco control primary consumer access and in 2025 account for roughly 25–35% of shelf space in key markets, giving them leverage over suppliers such as Unilever.

These buyers use volume to demand lower wholesale prices, deeper promotional funding and extended payment terms, pressuring Unilever’s gross margins by an estimated 50–150 basis points on key categories in 2024–25.

Retail consolidation—top 10 retailers capturing ~60% of organized grocery sales in Europe—intensified bargaining power in 2025, forcing Unilever to negotiate trade funds and slotting fees to protect distribution.

Low switching costs for end consumers

Individual consumers face virtually zero costs switching from Unilever brands like Dove or Hellmann’s to rivals, so small price cuts or promotions can shift share quickly; NielsenIQ reported 45% of grocery shoppers in 2024 tried new brands in the prior 3 months. This low friction forces Unilever to spend: advertising was €9.2bn in 2024 and R&D €1.1bn, keeping loyalty via marketing and product innovation.

Rise of high quality private labels

Retailers expanded private labels, which by end-2025 held about 18–22% of fast-moving consumer goods (FMCG) value share in Europe and the US, up ~3–5 p.p. since 2021, offering similar quality at lower prices.

This market-share gain gives retailers bargaining power to prioritize store brands, pressuring Unilever to defend premium pricing with measurable brand value and innovation.

Influence of e-commerce and digital transparency

E-commerce growth and digital transparency let shoppers compare prices across thousands of SKUs in seconds, shrinking information gaps that once favored big firms; global online FMCG sales rose to about $800bn in 2024, boosting niche-brand discovery. Unilever responded by expanding direct-to-consumer (DTC) pilots and digital marketing—its 2024 digital sales share rose to ~12%—to keep shelf attention and margins.

- Online FMCG sales ≈ $800bn (2024)

- Unilever digital sales ≈ 12% (2024)

- Instant price comparison lowers switching costs

- DTC and digital ads key to retaining customers

Consumer demand for ethical and sustainable products

Modern buyers increasingly choose brands on environmental and social grounds; 61% of global consumers said they prefer sustainable products in 2024 (NielsenIQ), pushing Unilever to target net-zero by 2039 and 100% recyclable or reusable packaging by 2025.

This demand gives consumers leverage to require transparency and sustainable packaging; failing to meet expectations risks rapid brand erosion—Unilever reported a 3% volume decline in regions where sustainability claims were questioned in 2023.

- 61% of consumers prefer sustainable products (2024)

- Unilever net-zero by 2039, 100% recyclable packaging target 2025

- 3% volume decline in markets after sustainability controversies (2023)

Retailer dominance and e‑commerce squeeze force Unilever to concede margins

Customers hold high bargaining power: top retailers (Walmart, Carrefour, Tesco) control 25–35% shelf space in key markets (2025) and top 10 retailers capture ~60% grocery sales in Europe (2025), forcing Unilever to concede 50–150 bps margin on key categories via lower net prices and trade funds; e-commerce ($800bn FMCG, 2024) and 61% sustainability preference (2024) further raise switching and transparency pressures.

| Metric | Value |

|---|---|

| Top retailers shelf share | 25–35% (2025) |

| Top-10 grocery share Europe | ~60% (2025) |

| Margin pressure | 50–150 bps (2024–25) |

| Online FMCG sales | $800bn (2024) |

| Consumers preferring sustainable | 61% (2024) |

Preview the Actual Deliverable

Unilever Porter's Five Forces Analysis

This preview shows the exact Unilever Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download after purchase, with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Unilever faces intense rivalry from global and local consumer goods players, moderate supplier power due to scale, strong buyer power driven by retailer consolidation, low threat of new entrants because of high brand and distribution barriers, and rising substitute threats from niche, eco-conscious brands—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Unilever’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale driven procurement leverage

Unilever runs procurement across 190+ countries and more than 70,000 suppliers, giving scale-driven leverage to push supplier margins lower; centralized buying cut input cost volatility by ~6% in 2024 and targets similar gains through 2025.

Diversified sourcing and risk management

Unilever has cut supplier power by diversifying inputs across 190+ sourcing countries and 1,000s of suppliers, reducing reliance on any single region or vendor; in 2024 sourced agricultural commodities rose 8% from South America while chemical buys widened to Asia, lowering concentration risk.

Impact of raw material price volatility

While Unilever is a major buyer, 2024–2025 commodity swings—rapeseed oil up 38% YoY in 2024 and key surfactant costs rising ~22%—have temporarily shifted leverage to suppliers, especially during short supply windows.

By late 2025 Unilever increased long-term hedges and struck multi-year sourcing deals covering ~30% of vegetable-oil needs, reflecting strategic partnerships to dampen volatility.

These moves keep Unilever dominant, but the essential nature of some inputs gives suppliers a baseline influence that can spike margins short-term.

Strict sustainability and compliance standards

Unilever enforces strict environmental and social governance standards that suppliers must meet to keep contracts, shrinking the eligible vendor pool but raising switching costs.

Suppliers often invest in capital and certification to meet Unilever’s 2025 targets (net-zero by 2039, 100% recyclable packaging by 2025), so losing Unilever after those investments would be costly, binding them closer to the company.

Low switching costs for standardized inputs

For most of Unilever’s commodity inputs—palm oil, surfactants, bulk fragrances—switching suppliers is easy and low-cost, keeping supplier leverage weak; in 2024 Unilever sourced over 60% of key commodities from 100+ global vendors, limiting price pressure.

Portability of standard packaging and ingredients, plus multi-sourcing and spot-market purchases, prevents suppliers from imposing steep premiums or restrictive terms, so supplier power is low to moderate.

- Many suppliers: 100+ global vendors for core commodities

- High spot buying: significant use of commodities markets in 2024

- Low switching costs: modular packaging and standard ingredients

- Supplier power: low–moderate, limited price-setting ability

Unilever’s buying scale tempers supplier power despite 2024 commodity spike

Unilever’s scale (70,000+ suppliers, procurement in 190+ countries) keeps supplier power low–moderate; 2024 centralized buying cut input volatility ~6% while commodity shocks (rapeseed +38% YoY; surfactants +22%) raised short-term supplier leverage. ESG rules and CAPEX raise switching costs; multi-sourcing and 100+ vendors for core commodities limit price-setting.

| Metric | 2024/2025 |

|---|---|

| Suppliers | 70,000+ |

| Countries | 190+ |

| Centralized buying impact | -6% volatility 2024 |

| Rapeseed oil | +38% YoY 2024 |

| Surfactants | +22% 2024 |

| Hedged vegetable oil | ~30% by late 2025 |

What is included in the product

Unilever-specific Porter's Five Forces analysis revealing competitive intensity, buyer/supplier power, substitution threats, and entry barriers, with strategic insights on disruptive trends and implications for pricing and profitability.

A concise Porter's Five Forces snapshot for Unilever—distills supplier, buyer, rivalry, entrant, and substitute pressures into one actionable view for swift strategic decisions.

Customers Bargaining Power

Retailer concentration and shelf space control

Major chains like Walmart, Carrefour and Tesco control primary consumer access and in 2025 account for roughly 25–35% of shelf space in key markets, giving them leverage over suppliers such as Unilever.

These buyers use volume to demand lower wholesale prices, deeper promotional funding and extended payment terms, pressuring Unilever’s gross margins by an estimated 50–150 basis points on key categories in 2024–25.

Retail consolidation—top 10 retailers capturing ~60% of organized grocery sales in Europe—intensified bargaining power in 2025, forcing Unilever to negotiate trade funds and slotting fees to protect distribution.

Low switching costs for end consumers

Individual consumers face virtually zero costs switching from Unilever brands like Dove or Hellmann’s to rivals, so small price cuts or promotions can shift share quickly; NielsenIQ reported 45% of grocery shoppers in 2024 tried new brands in the prior 3 months. This low friction forces Unilever to spend: advertising was €9.2bn in 2024 and R&D €1.1bn, keeping loyalty via marketing and product innovation.

Rise of high quality private labels

Retailers expanded private labels, which by end-2025 held about 18–22% of fast-moving consumer goods (FMCG) value share in Europe and the US, up ~3–5 p.p. since 2021, offering similar quality at lower prices.

This market-share gain gives retailers bargaining power to prioritize store brands, pressuring Unilever to defend premium pricing with measurable brand value and innovation.

Influence of e-commerce and digital transparency

E-commerce growth and digital transparency let shoppers compare prices across thousands of SKUs in seconds, shrinking information gaps that once favored big firms; global online FMCG sales rose to about $800bn in 2024, boosting niche-brand discovery. Unilever responded by expanding direct-to-consumer (DTC) pilots and digital marketing—its 2024 digital sales share rose to ~12%—to keep shelf attention and margins.

- Online FMCG sales ≈ $800bn (2024)

- Unilever digital sales ≈ 12% (2024)

- Instant price comparison lowers switching costs

- DTC and digital ads key to retaining customers

Consumer demand for ethical and sustainable products

Modern buyers increasingly choose brands on environmental and social grounds; 61% of global consumers said they prefer sustainable products in 2024 (NielsenIQ), pushing Unilever to target net-zero by 2039 and 100% recyclable or reusable packaging by 2025.

This demand gives consumers leverage to require transparency and sustainable packaging; failing to meet expectations risks rapid brand erosion—Unilever reported a 3% volume decline in regions where sustainability claims were questioned in 2023.

- 61% of consumers prefer sustainable products (2024)

- Unilever net-zero by 2039, 100% recyclable packaging target 2025

- 3% volume decline in markets after sustainability controversies (2023)

Retailer dominance and e‑commerce squeeze force Unilever to concede margins

Customers hold high bargaining power: top retailers (Walmart, Carrefour, Tesco) control 25–35% shelf space in key markets (2025) and top 10 retailers capture ~60% grocery sales in Europe (2025), forcing Unilever to concede 50–150 bps margin on key categories via lower net prices and trade funds; e-commerce ($800bn FMCG, 2024) and 61% sustainability preference (2024) further raise switching and transparency pressures.

| Metric | Value |

|---|---|

| Top retailers shelf share | 25–35% (2025) |

| Top-10 grocery share Europe | ~60% (2025) |

| Margin pressure | 50–150 bps (2024–25) |

| Online FMCG sales | $800bn (2024) |

| Consumers preferring sustainable | 61% (2024) |

Preview the Actual Deliverable

Unilever Porter's Five Forces Analysis

This preview shows the exact Unilever Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download after purchase, with no placeholders or samples.