Unipol Gruppo Boston Consulting Group Matrix

Unlock Strategic Clarity

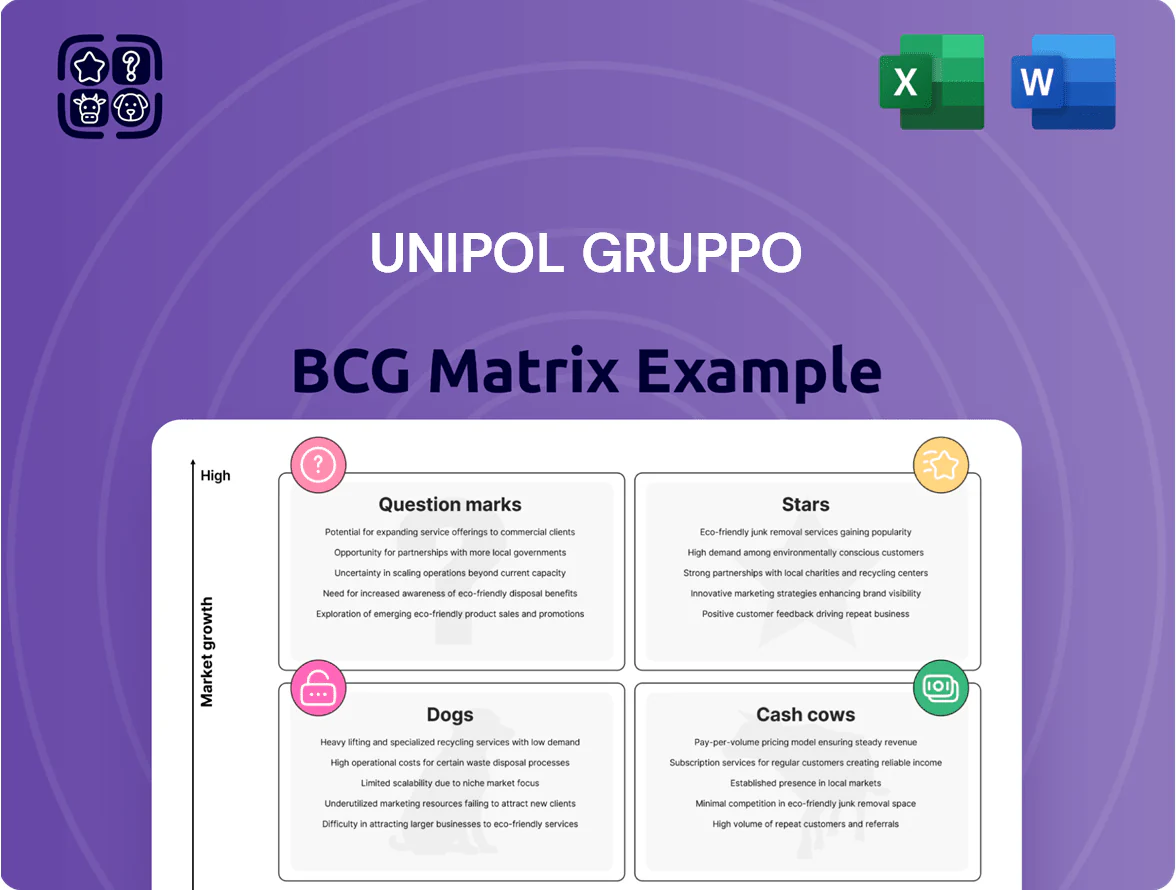

Unipol Gruppo’s BCG Matrix preview highlights how its insurance and banking segments perform across market growth and relative share, hinting at which lines are Stars driving expansion and which may be Cash Cows funding stability. This snapshot teases where resources should shift amid regulatory shifts and digital disruption. Purchase the full BCG Matrix for quadrant-by-quadrant placements, executable recommendations, and editable Word + Excel deliverables to guide confident capital and product decisions.

Stars

UnipolMove and Mobility Ecosystem

UnipolMove challenged the electronic tolling monopoly and by Q3 2025 held ~28% market share in Italy’s e-toll devices, adding 1.2M active users since 2022 and €95M revenue in 2024, turning into a mobility-services leader tied to Unipol Gruppo’s 12.5M insurance customers.

Leveraging cross-sell, Unipol scaled integrated travel solutions—parking, charging, and multimodal booking—with ARR growth ~34% YoY through 2024; ongoing tech and marketing spend of ~€40M/year is needed to fend off fintech and telco entrants by late 2025.

Digital Health and Welfare Services

Unisalute drives high growth as private health demand rises in Italy; private health insurance penetration hit ~6.5% in 2024 vs 5.8% in 2021, boosting Unipol salute volumes and revenue (Unipol reported group insurance premium income €6.1bn in FY2024, with health a key contributor).

Unipol leads managed care with integrated digital booking and telemedicine; Unisalute’s telehealth consultations grew 140% between 2022–2024, supporting market-share gains in employer and retail segments.

Revenue is strong but capital intensive: annual R&D and network expansion costs for medical tech exceed €70m in 2024, so sustained capital injections are needed to keep service quality and market dominance.

Advanced Telematics and IoT Insurance

As a pioneer in black-box vehicle tech, Unipol leads with ~3.2m telematics policies at end-2024, driving lower loss ratios (approx. 8–12% improvement vs non-telematics) through pay-how-you-drive pricing.

Connected-car market growth (~CAGR 12% to 2028) boosts demand for personalized premiums and safety services; Unipol reports 28% annual uptake for value-added telematics apps in 2024.

The group spent ~€120m on data analytics and proprietary hardware in 2024, maintaining its telematics stack used in predictive risk models that cut claims frequency by ~15% year-on-year.

Strategic Bancassurance Partnerships

Through stakes and agreements with BPER Banca and Banca Popolare di Sondrio, Unipol secured a high-growth bancassurance channel, delivering 2024 bancassurance premiums of ~€4.2bn and doubling new protection sales vs 2021.

This model captures wealth-management and protection share without running a branch network, lowering distribution cost-to-premium by ~18% vs proprietary branches.

Bank-insurance synergy is a high-performing segment, linking traditional finance and modern protection and contributing ~15% of Unipol Group EBIT in 2024.

- 2024 bancassurance premiums ≈ €4.2bn

- New protection sales +100% vs 2021

- Distribution cost-to-premium −18% vs branches

- Contributed ~15% of Group EBIT in 2024

ESG-Integrated Investment Portfolios

ESG-integrated life and pension products at Unipol are high-growth stars, driven by 2024–25 investor demand: ESG funds saw €1.2bn net inflows into Unipol’s platform in 2024, lifting AUM growth by 18% year-over-year and outpacing group average.

Aligning investments with EU Green Deal targets attracts younger, ethics-focused clients—55% of new pension customers in 2024 were under 40—boosting retention but requiring ongoing regulatory updates and active marketing.

These offerings now lead Unipol’s modern expansion, while compliance costs rose 6% in 2024 for reporting and product adaptation, still offset by higher margins and premium pricing.

- 2024 ESG inflows €1.2bn

- AUM growth +18% YoY

- 55% new clients <40

- Compliance costs +6% (2024)

Unipol's growth engines: mobility, telehealth, telematics, bancassurance & €1.2bn ESG

Stars: Unipol’s mobility, health, telematics, bancassurance and ESG pensions drove high growth—UnipolMove 28% e-toll share, €95M revenue (2024); Unisalute telehealth +140% (2022–24); telematics 3.2M policies; bancassurance €4.2bn premiums (2024); ESG inflows €1.2bn (2024).

| Metric | 2024 |

|---|---|

| UnipolMove rev | €95M |

| Telematics | 3.2M policies |

| Bancassurance | €4.2bn |

| ESG inflows | €1.2bn |

What is included in the product

Comprehensive BCG Matrix for Unipol: quadrant-level insights, investment/ divestment recommendations, and trend-driven risks and advantages.

One-page Unipol Gruppo BCG Matrix placing each business unit in a quadrant for rapid strategic decisions.

Cash Cows

Motor Third-Party Liability Insurance

Motor Third-Party Liability Insurance is Unipol Gruppo’s cash cow, covering ~35% of Italy’s motor TP market and generating roughly €2.1bn EBITDA in FY2024; market maturity keeps growth ~1–2% annually but renewal rates near 78% ensure steady cash flow.

General Non-Life Property Insurance

Unipol dominates Italian non-life property insurance for homes and businesses—fire, theft and liability—with roughly 22% market share in household property lines as of 2025, high brand loyalty, and stable retention rates near 85%.

The segment’s low annual premium growth (~1–2% CAGR) needs little new infrastructure, enabling underwriting margins above 12% and strong operating cash flow.

Cash from this business services Unipol’s net debt (group net debt €3.4bn at YE 2024) and funds digital R&D—€75m allocated in 2024 to customer-facing platforms and automation.

Traditional Life Insurance and Pension Funds

Unipol Gruppo’s traditional life insurance and pension funds manage roughly €60 billion in reserves (2024 IFRS figures), delivering stable, long-term capital and predictable asset management fees amid Italy’s aging population.

New policy growth is muted—single-digit annual inflows—yet persistently low lapse rates sustain liquidity and yield generation for the group.

This cash cow reliably funds Question Marks investments, supporting riskier M&A and digital projects without stressing capital ratios.

Extensive Physical Agency Network

With ~3,000 agencies across Italy (Unipol Gruppo, 2024), Unipol’s extensive physical network is a cash cow: upfront branch capex is amortized and agencies now deliver high-margin insurance sales and cross-sells (motor, life, bancassurance), boosting group FY2024 net inflows by an estimated €1.2–1.5bn vs digital channels.

The mature network sustains market share (~22% retail P&C by premium, IVASS 2024) with minimal incremental spend; unit acquisition costs fall below digital-only startups, so ROI on each agency remains high and stable.

- ~3,000 agencies nationwide (2024)

- ~22% retail P&C market share (IVASS 2024)

- Estimated €1.2–1.5bn incremental net inflows (FY2024)

- Lower unit acquisition cost vs digital startups

Real Estate Asset Management

Unipol’s Real Estate Asset Management owns prime commercial and residential assets in Milan, Rome, and Bologna that delivered ~€210m net rental income and ~3.6% like-for-like yield in 2024, supplying steady cash and long-term capital appreciation.

As a mature unit it needs routine upkeep only, generates large cash surpluses (free cash flow ~€160m in 2024), and bolsters Unipol’s balance sheet to fund opportunistic M&A.

- 2024 net rental income €210m

- Like-for-like yield 3.6% (2024)

- Free cash flow €160m (2024)

- Key markets: Milan, Rome, Bologna

Diversified cash cows: €2.1bn Motor, €60bn Life, €160m RE FCF, strong P&C & agencies

Key cash cows: Motor TP (€2.1bn EBITDA FY2024, ~35% market), Retail P&C (22% market share, 85% retention), Life reserves (€60bn, stable fees), Agencies (~3,000, €1.2–1.5bn incremental inflows FY2024), Real Estate (net rent €210m, FCF €160m 2024).

| Asset | Key metric | 2024 |

|---|---|---|

| Motor TP | EBITDA / market share | €2.1bn / 35% |

| Retail P&C | Market share / retention | 22% / 85% |

| Life reserves | Assets under management | €60bn |

| Agencies | Count / net inflows | ~3,000 / €1.2–1.5bn |

| Real Estate | Net rent / FCF | €210m / €160m |

What You’re Viewing Is Included

Unipol Gruppo BCG Matrix

The file you're previewing on this page is the final Unipol Gruppo BCG Matrix you'll receive after purchase—no watermarks, no demo content—just the fully formatted, ready-to-use strategic report designed for clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Unipol Gruppo’s BCG Matrix preview highlights how its insurance and banking segments perform across market growth and relative share, hinting at which lines are Stars driving expansion and which may be Cash Cows funding stability. This snapshot teases where resources should shift amid regulatory shifts and digital disruption. Purchase the full BCG Matrix for quadrant-by-quadrant placements, executable recommendations, and editable Word + Excel deliverables to guide confident capital and product decisions.

Stars

UnipolMove and Mobility Ecosystem

UnipolMove challenged the electronic tolling monopoly and by Q3 2025 held ~28% market share in Italy’s e-toll devices, adding 1.2M active users since 2022 and €95M revenue in 2024, turning into a mobility-services leader tied to Unipol Gruppo’s 12.5M insurance customers.

Leveraging cross-sell, Unipol scaled integrated travel solutions—parking, charging, and multimodal booking—with ARR growth ~34% YoY through 2024; ongoing tech and marketing spend of ~€40M/year is needed to fend off fintech and telco entrants by late 2025.

Digital Health and Welfare Services

Unisalute drives high growth as private health demand rises in Italy; private health insurance penetration hit ~6.5% in 2024 vs 5.8% in 2021, boosting Unipol salute volumes and revenue (Unipol reported group insurance premium income €6.1bn in FY2024, with health a key contributor).

Unipol leads managed care with integrated digital booking and telemedicine; Unisalute’s telehealth consultations grew 140% between 2022–2024, supporting market-share gains in employer and retail segments.

Revenue is strong but capital intensive: annual R&D and network expansion costs for medical tech exceed €70m in 2024, so sustained capital injections are needed to keep service quality and market dominance.

Advanced Telematics and IoT Insurance

As a pioneer in black-box vehicle tech, Unipol leads with ~3.2m telematics policies at end-2024, driving lower loss ratios (approx. 8–12% improvement vs non-telematics) through pay-how-you-drive pricing.

Connected-car market growth (~CAGR 12% to 2028) boosts demand for personalized premiums and safety services; Unipol reports 28% annual uptake for value-added telematics apps in 2024.

The group spent ~€120m on data analytics and proprietary hardware in 2024, maintaining its telematics stack used in predictive risk models that cut claims frequency by ~15% year-on-year.

Strategic Bancassurance Partnerships

Through stakes and agreements with BPER Banca and Banca Popolare di Sondrio, Unipol secured a high-growth bancassurance channel, delivering 2024 bancassurance premiums of ~€4.2bn and doubling new protection sales vs 2021.

This model captures wealth-management and protection share without running a branch network, lowering distribution cost-to-premium by ~18% vs proprietary branches.

Bank-insurance synergy is a high-performing segment, linking traditional finance and modern protection and contributing ~15% of Unipol Group EBIT in 2024.

- 2024 bancassurance premiums ≈ €4.2bn

- New protection sales +100% vs 2021

- Distribution cost-to-premium −18% vs branches

- Contributed ~15% of Group EBIT in 2024

ESG-Integrated Investment Portfolios

ESG-integrated life and pension products at Unipol are high-growth stars, driven by 2024–25 investor demand: ESG funds saw €1.2bn net inflows into Unipol’s platform in 2024, lifting AUM growth by 18% year-over-year and outpacing group average.

Aligning investments with EU Green Deal targets attracts younger, ethics-focused clients—55% of new pension customers in 2024 were under 40—boosting retention but requiring ongoing regulatory updates and active marketing.

These offerings now lead Unipol’s modern expansion, while compliance costs rose 6% in 2024 for reporting and product adaptation, still offset by higher margins and premium pricing.

- 2024 ESG inflows €1.2bn

- AUM growth +18% YoY

- 55% new clients <40

- Compliance costs +6% (2024)

Unipol's growth engines: mobility, telehealth, telematics, bancassurance & €1.2bn ESG

Stars: Unipol’s mobility, health, telematics, bancassurance and ESG pensions drove high growth—UnipolMove 28% e-toll share, €95M revenue (2024); Unisalute telehealth +140% (2022–24); telematics 3.2M policies; bancassurance €4.2bn premiums (2024); ESG inflows €1.2bn (2024).

| Metric | 2024 |

|---|---|

| UnipolMove rev | €95M |

| Telematics | 3.2M policies |

| Bancassurance | €4.2bn |

| ESG inflows | €1.2bn |

What is included in the product

Comprehensive BCG Matrix for Unipol: quadrant-level insights, investment/ divestment recommendations, and trend-driven risks and advantages.

One-page Unipol Gruppo BCG Matrix placing each business unit in a quadrant for rapid strategic decisions.

Cash Cows

Motor Third-Party Liability Insurance

Motor Third-Party Liability Insurance is Unipol Gruppo’s cash cow, covering ~35% of Italy’s motor TP market and generating roughly €2.1bn EBITDA in FY2024; market maturity keeps growth ~1–2% annually but renewal rates near 78% ensure steady cash flow.

General Non-Life Property Insurance

Unipol dominates Italian non-life property insurance for homes and businesses—fire, theft and liability—with roughly 22% market share in household property lines as of 2025, high brand loyalty, and stable retention rates near 85%.

The segment’s low annual premium growth (~1–2% CAGR) needs little new infrastructure, enabling underwriting margins above 12% and strong operating cash flow.

Cash from this business services Unipol’s net debt (group net debt €3.4bn at YE 2024) and funds digital R&D—€75m allocated in 2024 to customer-facing platforms and automation.

Traditional Life Insurance and Pension Funds

Unipol Gruppo’s traditional life insurance and pension funds manage roughly €60 billion in reserves (2024 IFRS figures), delivering stable, long-term capital and predictable asset management fees amid Italy’s aging population.

New policy growth is muted—single-digit annual inflows—yet persistently low lapse rates sustain liquidity and yield generation for the group.

This cash cow reliably funds Question Marks investments, supporting riskier M&A and digital projects without stressing capital ratios.

Extensive Physical Agency Network

With ~3,000 agencies across Italy (Unipol Gruppo, 2024), Unipol’s extensive physical network is a cash cow: upfront branch capex is amortized and agencies now deliver high-margin insurance sales and cross-sells (motor, life, bancassurance), boosting group FY2024 net inflows by an estimated €1.2–1.5bn vs digital channels.

The mature network sustains market share (~22% retail P&C by premium, IVASS 2024) with minimal incremental spend; unit acquisition costs fall below digital-only startups, so ROI on each agency remains high and stable.

- ~3,000 agencies nationwide (2024)

- ~22% retail P&C market share (IVASS 2024)

- Estimated €1.2–1.5bn incremental net inflows (FY2024)

- Lower unit acquisition cost vs digital startups

Real Estate Asset Management

Unipol’s Real Estate Asset Management owns prime commercial and residential assets in Milan, Rome, and Bologna that delivered ~€210m net rental income and ~3.6% like-for-like yield in 2024, supplying steady cash and long-term capital appreciation.

As a mature unit it needs routine upkeep only, generates large cash surpluses (free cash flow ~€160m in 2024), and bolsters Unipol’s balance sheet to fund opportunistic M&A.

- 2024 net rental income €210m

- Like-for-like yield 3.6% (2024)

- Free cash flow €160m (2024)

- Key markets: Milan, Rome, Bologna

Diversified cash cows: €2.1bn Motor, €60bn Life, €160m RE FCF, strong P&C & agencies

Key cash cows: Motor TP (€2.1bn EBITDA FY2024, ~35% market), Retail P&C (22% market share, 85% retention), Life reserves (€60bn, stable fees), Agencies (~3,000, €1.2–1.5bn incremental inflows FY2024), Real Estate (net rent €210m, FCF €160m 2024).

| Asset | Key metric | 2024 |

|---|---|---|

| Motor TP | EBITDA / market share | €2.1bn / 35% |

| Retail P&C | Market share / retention | 22% / 85% |

| Life reserves | Assets under management | €60bn |

| Agencies | Count / net inflows | ~3,000 / €1.2–1.5bn |

| Real Estate | Net rent / FCF | €210m / €160m |

What You’re Viewing Is Included

Unipol Gruppo BCG Matrix

The file you're previewing on this page is the final Unipol Gruppo BCG Matrix you'll receive after purchase—no watermarks, no demo content—just the fully formatted, ready-to-use strategic report designed for clarity and professional presentation.