UNIQA Insurance Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore UNIQA Insurance Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Concentration

Global reinsurers Munich Re and Swiss Re control roughly 40–50% of global facultative and treaty capacity, giving them strong leverage to set catastrophic pricing that directly affects UNIQA’s risk-transfer costs and margins.

In 2024, catastrophe reinsurance rates rose ~35% on average; if reinsurers push premiums higher, UNIQA must absorb costs or raise premiums, risking competitiveness and policyholder churn.

Dependence on Specialized Technology Providers

The shift to digital platforms makes UNIQA heavily reliant on major cloud and software vendors, who hold high bargaining power because services are specialized and switching costs are steep; global cloud market concentration: AWS, Microsoft Azure, Google Cloud held ~64% of IaaS/PaaS in 2024. Long-term contracts (often 3–7 years) and integration of proprietary AI tools lock in vendors and raise exit costs. In 2024 UNIQA disclosed c.€120m IT spend, amplifying supplier influence.

Competition for Actuarial and Data Science Talent

The supply of senior actuaries and data scientists in Europe is tight—Eurostat data show STEM specialist vacancies up 18% in 2024—forcing UNIQA to compete with banks and Big Tech for about 40–60k EUR entry salaries and 120–180k EUR for senior hires in 2025 markets like Vienna.

Scarcity lets specialists and niche recruiters extract premium pay and signing bonuses; industry reports in 2024 cite median signing bonuses of 10–15% for analytics roles.

Higher bargaining power raises UNIQA’s operating costs and talent churn risk, pushing the firm toward retention spend, remote hiring, or partnerships with universities to secure pipeline talent.

Influence of Financial Capital Markets

UNIQA depends on capital markets to fund operations and to earn returns on a €22.4bn investment portfolio (FY2024) needed to cover future liabilities; low yields cut investment income and raise reserve strain.

Central bank policy and global growth drove 2024 ECB rates to 3.75% and shaped bond spreads; tighter rates help yield but pressure asset valuations and credit costs.

Solvency II requires UNIQA to hold capital buffers—own funds coverage fell to 205% in 2024—so market access and rates remain a tangible supplier power and vulnerability.

- €22.4bn investment portfolio (FY2024)

- Own funds coverage ~205% (2024)

- ECB policy rate 3.75% (end-2024)

Healthcare and Service Provider Networks

UNIQA depends on private hospitals, clinics and repair shops for health and motor claims; in Austria and CEE markets a handful of top providers can set fees, raising supplier bargaining power and claims costs.

Keeping provider rates in check is critical: UNIQA reported a 2024 combined ratio of ~97.5% and a health loss ratio near 74%, so network costs materially affect profitability and customer satisfaction.

- Concentration: few high-quality providers in key regions

- Impact: higher fees raise combined ratio

- 2024 metrics: combined ratio ~97.5%, health loss ratio ~74%

UNIQA faces supplier concentration risks despite solid capital and underwriting

Suppliers (reinsurers, cloud providers, talent, hospitals, capital markets) hold strong bargaining power vs UNIQA—reinsurance concentration (Munich Re/Swiss Re ~40–50%), cloud share (AWS/MS/Google ~64% IaaS/PaaS, 2024), €22.4bn invest. portfolio (FY2024), own funds 205% (2024), combined ratio ~97.5%, health loss ratio ~74% (2024).

| Metric | Value |

|---|---|

| Reinsurers share | 40–50% |

| Cloud IaaS/PaaS | ~64% (2024) |

| Investments | €22.4bn (FY2024) |

| Own funds | 205% (2024) |

| Combined ratio | ~97.5% (2024) |

| Health loss ratio | ~74% (2024) |

What is included in the product

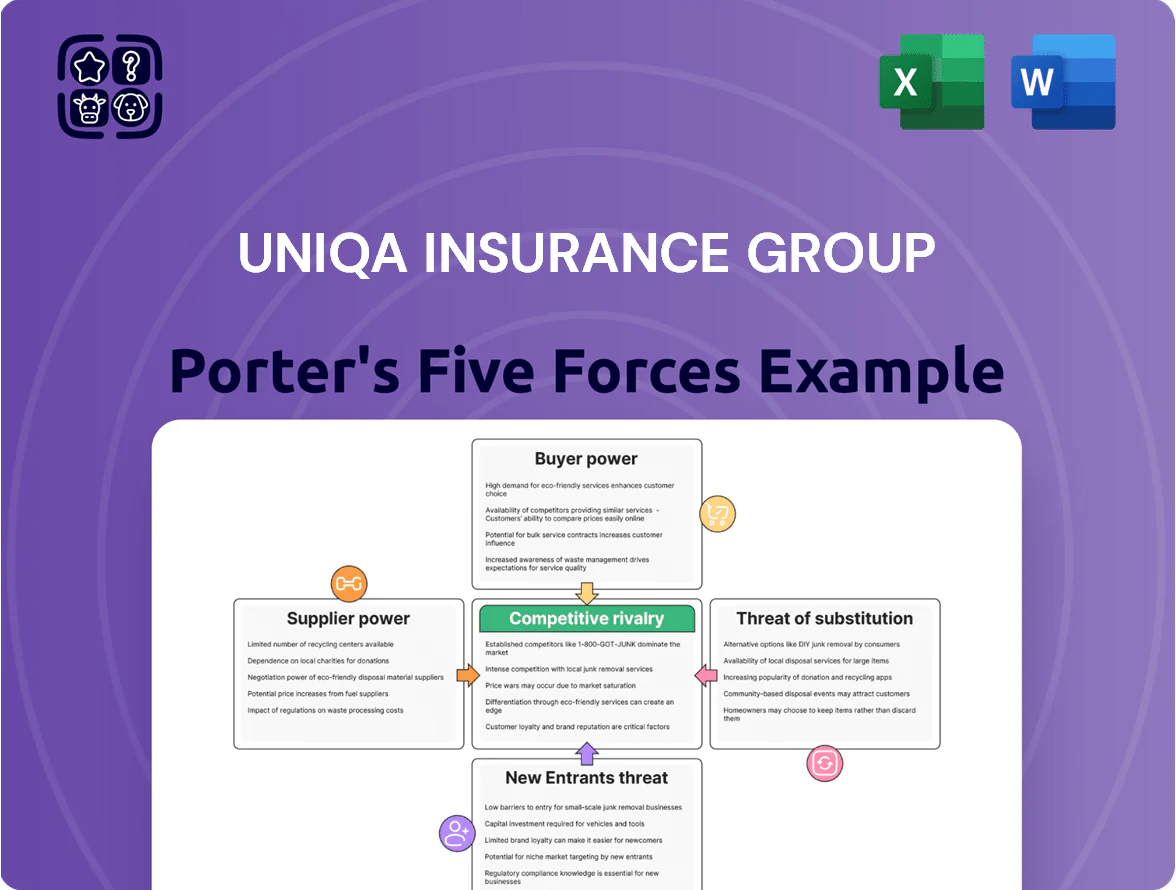

Tailored Porter's Five Forces analysis for UNIQA Insurance Group that uncovers competitive drivers, buyer and supplier influence, barriers to entry, substitutes, and disruptive threats to market share—fully editable for reports and strategy work.

Compact Porter's Five Forces snapshot for UNIQA—quickly highlights competitive threats and bargaining pressures to streamline strategic decisions and reduce analysis time.

Customers Bargaining Power

Price Transparency Through Digital Aggregators

Price transparency from online aggregators lets retail buyers compare UNIQA Insurance Group (Austria-based UNIQA Insurance Group AG) with rivals in real time, and in 2024 EU aggregator traffic rose ~18% year-over-year, boosting shopper switching. This transparency raised price sensitivity; standardized motor and household policies now face pressure to match lowest offers, cutting UNIQA’s ability to sustain premium pricing. In 2023 study, 42% of EU consumers switched insurers after price comparison, so customers can find and move to the cheapest provider with little effort.

Influence of Independent Brokers and Intermediaries

Low Switching Costs for Standardized Products

In P&C lines like motor and household, switching costs are low: most UNIQA policies are annual and regulators plus digital onboarding cut admin friction, so EU switching rate for motor insurance hit ~12% in 2024 (EY, 2025), pushing UNIQA to invest in CX and loyalty—customer retention fell 0.6ppt to 84.2% in 2024 if onboarding >14 days.

Negotiation Power of Large Corporate Clients

Large corporate clients supply high-volume premiums—UNIQA reported €3.1bn commercial premiums in 2024—but negotiate bespoke terms and demand discounts, pressuring margins.

They run competitive tenders; in Central Europe 2023 data shows 60% of corporate renewals used auctions, forcing insurers to undercut each other.

The option to self-insure or switch carriers raises renewal leverage; loss of one large account can cut commercial premiums by multiple percentage points.

- €3.1bn UNIQA commercial premiums (2024)

- 60% corporate renewals via tenders (Central Europe, 2023)

- Self-insurance option increases walk-away leverage

Demand for Personalized and Digital Experiences

Modern consumers demand flexible, on-demand insurance and seamless mobile interactions; 73% of European customers expect fully digital service, per 2024 McKinsey data, so UNIQA risks churn if its app and personalization lag.

If UNIQA cannot match insurtechs that reduced acquisition costs by 20–30% in 2023 and offer modular cover, customers will push faster tech adoption and pricing transparency.

- 73% of Europeans expect full digital service (McKinsey 2024)

- Insurtechs cut acquisition costs 20–30% (2023)

- High churn risk if personalization lags

Customers Drive Change: Digital Demand, Rising Aggregators & Broker-Powered Discounts

Customers hold strong bargaining power: retail price transparency and 18% YoY aggregator traffic growth (2024) raise switching; brokers channel ~45% of premiums and pushed UNIQA broker commission to ~21% (2024); corporate tenders hit 60% (Central Europe, 2023) and €3.1bn commercial premiums (2024) face tender-driven discounts; 73% of Europeans expect full digital service (McKinsey 2024).

| Metric | Value |

|---|---|

| Aggregator traffic growth (2024) | +18% |

| Brokers share of premiums (2024) | ~45% |

| Broker commission ratio (2024) | ~21% |

| Corporate premiums (2024) | €3.1bn |

| Corporate tenders (CE, 2023) | 60% |

| Digital expectation (EU, 2024) | 73% |

Same Document Delivered

UNIQA Insurance Group Porter's Five Forces Analysis

This preview shows the exact UNIQA Insurance Group Porter's Five Forces analysis you'll receive—no samples or placeholders—providing ready-to-use insights on competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore UNIQA Insurance Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Concentration

Global reinsurers Munich Re and Swiss Re control roughly 40–50% of global facultative and treaty capacity, giving them strong leverage to set catastrophic pricing that directly affects UNIQA’s risk-transfer costs and margins.

In 2024, catastrophe reinsurance rates rose ~35% on average; if reinsurers push premiums higher, UNIQA must absorb costs or raise premiums, risking competitiveness and policyholder churn.

Dependence on Specialized Technology Providers

The shift to digital platforms makes UNIQA heavily reliant on major cloud and software vendors, who hold high bargaining power because services are specialized and switching costs are steep; global cloud market concentration: AWS, Microsoft Azure, Google Cloud held ~64% of IaaS/PaaS in 2024. Long-term contracts (often 3–7 years) and integration of proprietary AI tools lock in vendors and raise exit costs. In 2024 UNIQA disclosed c.€120m IT spend, amplifying supplier influence.

Competition for Actuarial and Data Science Talent

The supply of senior actuaries and data scientists in Europe is tight—Eurostat data show STEM specialist vacancies up 18% in 2024—forcing UNIQA to compete with banks and Big Tech for about 40–60k EUR entry salaries and 120–180k EUR for senior hires in 2025 markets like Vienna.

Scarcity lets specialists and niche recruiters extract premium pay and signing bonuses; industry reports in 2024 cite median signing bonuses of 10–15% for analytics roles.

Higher bargaining power raises UNIQA’s operating costs and talent churn risk, pushing the firm toward retention spend, remote hiring, or partnerships with universities to secure pipeline talent.

Influence of Financial Capital Markets

UNIQA depends on capital markets to fund operations and to earn returns on a €22.4bn investment portfolio (FY2024) needed to cover future liabilities; low yields cut investment income and raise reserve strain.

Central bank policy and global growth drove 2024 ECB rates to 3.75% and shaped bond spreads; tighter rates help yield but pressure asset valuations and credit costs.

Solvency II requires UNIQA to hold capital buffers—own funds coverage fell to 205% in 2024—so market access and rates remain a tangible supplier power and vulnerability.

- €22.4bn investment portfolio (FY2024)

- Own funds coverage ~205% (2024)

- ECB policy rate 3.75% (end-2024)

Healthcare and Service Provider Networks

UNIQA depends on private hospitals, clinics and repair shops for health and motor claims; in Austria and CEE markets a handful of top providers can set fees, raising supplier bargaining power and claims costs.

Keeping provider rates in check is critical: UNIQA reported a 2024 combined ratio of ~97.5% and a health loss ratio near 74%, so network costs materially affect profitability and customer satisfaction.

- Concentration: few high-quality providers in key regions

- Impact: higher fees raise combined ratio

- 2024 metrics: combined ratio ~97.5%, health loss ratio ~74%

UNIQA faces supplier concentration risks despite solid capital and underwriting

Suppliers (reinsurers, cloud providers, talent, hospitals, capital markets) hold strong bargaining power vs UNIQA—reinsurance concentration (Munich Re/Swiss Re ~40–50%), cloud share (AWS/MS/Google ~64% IaaS/PaaS, 2024), €22.4bn invest. portfolio (FY2024), own funds 205% (2024), combined ratio ~97.5%, health loss ratio ~74% (2024).

| Metric | Value |

|---|---|

| Reinsurers share | 40–50% |

| Cloud IaaS/PaaS | ~64% (2024) |

| Investments | €22.4bn (FY2024) |

| Own funds | 205% (2024) |

| Combined ratio | ~97.5% (2024) |

| Health loss ratio | ~74% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for UNIQA Insurance Group that uncovers competitive drivers, buyer and supplier influence, barriers to entry, substitutes, and disruptive threats to market share—fully editable for reports and strategy work.

Compact Porter's Five Forces snapshot for UNIQA—quickly highlights competitive threats and bargaining pressures to streamline strategic decisions and reduce analysis time.

Customers Bargaining Power

Price Transparency Through Digital Aggregators

Price transparency from online aggregators lets retail buyers compare UNIQA Insurance Group (Austria-based UNIQA Insurance Group AG) with rivals in real time, and in 2024 EU aggregator traffic rose ~18% year-over-year, boosting shopper switching. This transparency raised price sensitivity; standardized motor and household policies now face pressure to match lowest offers, cutting UNIQA’s ability to sustain premium pricing. In 2023 study, 42% of EU consumers switched insurers after price comparison, so customers can find and move to the cheapest provider with little effort.

Influence of Independent Brokers and Intermediaries

Low Switching Costs for Standardized Products

In P&C lines like motor and household, switching costs are low: most UNIQA policies are annual and regulators plus digital onboarding cut admin friction, so EU switching rate for motor insurance hit ~12% in 2024 (EY, 2025), pushing UNIQA to invest in CX and loyalty—customer retention fell 0.6ppt to 84.2% in 2024 if onboarding >14 days.

Negotiation Power of Large Corporate Clients

Large corporate clients supply high-volume premiums—UNIQA reported €3.1bn commercial premiums in 2024—but negotiate bespoke terms and demand discounts, pressuring margins.

They run competitive tenders; in Central Europe 2023 data shows 60% of corporate renewals used auctions, forcing insurers to undercut each other.

The option to self-insure or switch carriers raises renewal leverage; loss of one large account can cut commercial premiums by multiple percentage points.

- €3.1bn UNIQA commercial premiums (2024)

- 60% corporate renewals via tenders (Central Europe, 2023)

- Self-insurance option increases walk-away leverage

Demand for Personalized and Digital Experiences

Modern consumers demand flexible, on-demand insurance and seamless mobile interactions; 73% of European customers expect fully digital service, per 2024 McKinsey data, so UNIQA risks churn if its app and personalization lag.

If UNIQA cannot match insurtechs that reduced acquisition costs by 20–30% in 2023 and offer modular cover, customers will push faster tech adoption and pricing transparency.

- 73% of Europeans expect full digital service (McKinsey 2024)

- Insurtechs cut acquisition costs 20–30% (2023)

- High churn risk if personalization lags

Customers Drive Change: Digital Demand, Rising Aggregators & Broker-Powered Discounts

Customers hold strong bargaining power: retail price transparency and 18% YoY aggregator traffic growth (2024) raise switching; brokers channel ~45% of premiums and pushed UNIQA broker commission to ~21% (2024); corporate tenders hit 60% (Central Europe, 2023) and €3.1bn commercial premiums (2024) face tender-driven discounts; 73% of Europeans expect full digital service (McKinsey 2024).

| Metric | Value |

|---|---|

| Aggregator traffic growth (2024) | +18% |

| Brokers share of premiums (2024) | ~45% |

| Broker commission ratio (2024) | ~21% |

| Corporate premiums (2024) | €3.1bn |

| Corporate tenders (CE, 2023) | 60% |

| Digital expectation (EU, 2024) | 73% |

Same Document Delivered

UNIQA Insurance Group Porter's Five Forces Analysis

This preview shows the exact UNIQA Insurance Group Porter's Five Forces analysis you'll receive—no samples or placeholders—providing ready-to-use insights on competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications.