UNIQA Insurance Group Marketing Mix

Get Inspired by a Complete Brand Strategy

Discover how UNIQA Insurance Group tailors product offerings, pricing tiers, distribution channels, and promotional campaigns to secure market share and customer loyalty—this concise preview highlights strategic strengths and opportunities. Get the full 4P’s Marketing Mix Analysis in an editable, presentation-ready format to save hours of research and apply actionable insights for benchmarking, strategy, or coursework. Purchase the complete report for data-driven clarity and ready-to-use templates.

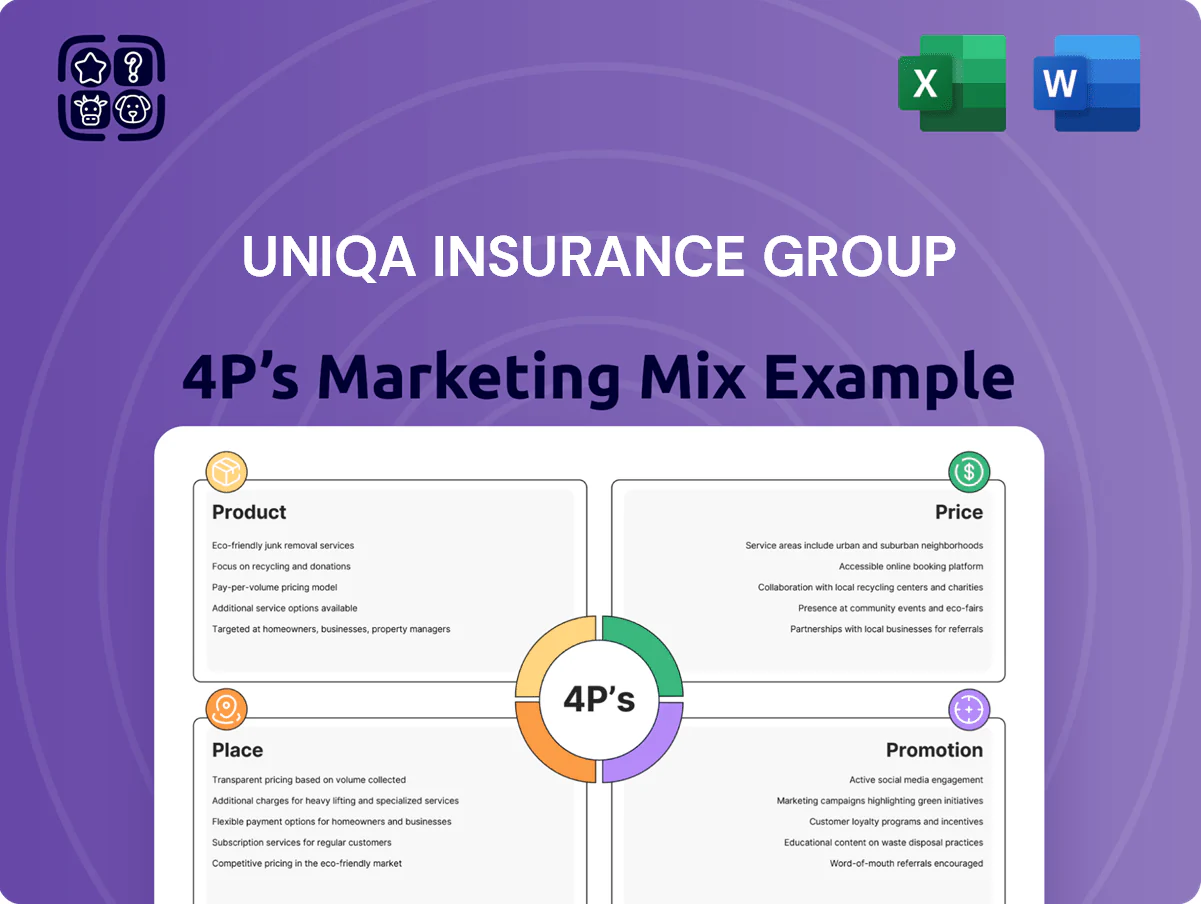

Product

Comprehensive Health and Wellness Ecosystems

UNIQA has shifted core health insurance into a prevention-first wellness ecosystem, embedding AI diagnostics and 24/7 telemedicine to reduce acute claims and boost engagement.

By end-2025 these services cover about 1.2 million policyholders across Central and Eastern Europe, with AI triage reducing unnecessary ER visits by an estimated 18% and telehealth consultations rising 45% year-on-year.

This proactive health-partner model increases retention—UNIQA reported a 3.5 percentage-point rise in health-policy renewal rates in 2024—and targets growing private care demand while aiming to lower combined medical costs.

Flexible Life and Unit-Linked Pension Plans

UNIQA’s life portfolio centers on unit-linked plans that let policyholders tap capital market returns while keeping adjustable protection; as of 2024 UNIQA reported roughly EUR 1.2bn in unit-linked reserves, up 6% year-on-year. These policies offer premium flexibility and pause options so customers can adjust contributions across life stages—useful given EU pension dependency ratios rising toward 3 in 2050. The product targets long-term wealth accumulation and private pension top-ups to offset demographic shifts and declining public pension replacement rates.

Digital-First Property and Casualty Solutions

UNIQA Insurance Group’s Digital-First Property and Casualty solutions offer modular, mobile-managed coverage across homes, autos, and personal liability, with 60% of retail policies purchasable via app as of 2025; terms are simplified and average digital claim settlement dropped to 3.2 days in 2024. Integration with smart-home sensors and telematics enables personalized premiums—up to 25% premium discounts—and proactive loss prevention, reducing claim frequency by ~18% in pilot markets.

Tailored Corporate and Industrial Risk Management

UNIQA offers tailored corporate and industrial insurance for complex risks, liability, and employee benefits, backed by in-house risk engineering that reduces loss frequency; in 2024 UNIQA Group reported commercial premiums of ~€1.1bn, with corporate lines growing ~6% year-on-year.

By 2025 UNIQA emphasizes cyber insurance and business interruption cover—cyber accounted for ~8% of commercial product launches in 2024—and provides scenario modeling to quantify interruption losses and downtime risk.

Sustainable and ESG-Integrated Insurance Products

UNIQA offers discounted premiums for energy-efficient buildings and electric vehicle insurance, plus ESG-only investment funds, aligning products with its 2030 climate targets and EU Taxonomy rules.

In 2024 UNIQA reported over 150,000 green-policy holders and EUR 420m in ESG assets under management, boosting appeal to socially conscious investors and reducing insured carbon exposure.

- Discounts for energy-efficient buildings

- EV-specific insurance

- ESG-only investment funds (EUR 420m, 2024)

- 150,000+ green-policy holders (2024)

UNIQA pivots to prevention-first health, digital P&C growth and €1.2bn unit-linked reserves

UNIQA’s product mix shifts to prevention-first health services (1.2M users by 2025; AI triage −18% ER visits), EUR 1.2bn unit-linked life reserves (2024, +6% YoY), digital P&C with 60% app sales and 3.2-day claim settlement (2024), and commercial premiums ~€1.1bn (2024, +6% YoY); ESG: 150k green policyholders and EUR 420m AUM (2024).

| Metric | Value |

|---|---|

| Health users (2025) | 1.2M |

| Unit-linked reserves (2024) | €1.2bn |

| P&C app sales (2025) | 60% |

| Digital claim days (2024) | 3.2 |

| Commercial premiums (2024) | €1.1bn |

| Green policyholders (2024) | 150k |

| ESG AUM (2024) | €420m |

What is included in the product

Delivers a concise, company-specific deep dive into UNIQA Insurance Group’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to ground analysis.

Condenses UNIQA Insurance Group’s 4P marketing insights into a concise, leadership-ready one-pager that clarifies product positioning, pricing strategy, distribution channels, and promotional priorities to speed decision-making and align teams.

Place

Strategic Bancassurance through Raiffeisen Bank

The long-standing Raiffeisen Bank partnership remains a cornerstone of UNIQA’s distribution across Austria and CEE, channeling roughly 28% of UNIQA Group’s 2024 gross written premiums (about EUR 1.1bn) through bancassurance; it reaches customers at key financial decision points within a trusted bank setting. The model creates a seamless handoff from banking to insurance for retail and SME clients, boosting cross-sell rates by ~14 percentage points versus direct channels and lifting persistency.

Extensive CEE Branch and Agency Network

UNIQA Insurance Group maintains a vast CEE branch and exclusive agency network across 15+ countries, with ~2,800 branches and 7,000 tied agents as of FY2024, boosting local market reach and €3.2bn in regional premiums.

Physical locations enable complex advisory services and long-term client ties—over 65% of high-net-worth policies sold in 2024 were closed face-to-face, showing strong demand for in-person counsel.

The local footprint keeps brand visible and accessible across diverse markets; branch density varies from 1.5 branches/100k people in Austria to 0.3/100k in emerging CEE states, aligning advice to local consumer behavior.

myUNIQA Digital Service and Sales Platform

The myUNIQA digital service and sales platform is UNIQA Insurance Group’s primary online hub for policy purchases and portfolio management, handling over 35% of new retail sales in 2024 and reducing paper workflows by 42% year-on-year.

By end-2025 the platform was upgraded for a frictionless UX and integrated AI chatbots (average response time 6s), cutting first-contact resolution time by 28% and boostng digital self-service rates to 62%.

Digital accessibility drives younger customer reach: 48% of users are under 35 and Net Promoter Score rose 7 points to 44 in 2025, showing improved satisfaction via convenience.

Independent Broker and Financial Advisor Channels

Partnerships with independent brokers and financial advisors extend UNIQA’s reach into niche segments and large industrial risks, covering ~27% of 2024 premiums via broker-sourced business and supporting EUR 1.2bn commercial lines placements.

These intermediaries give expert, bespoke advice that steers complex commercial clients toward UNIQA as a preferred provider, boosting retention and higher-margin accounts.

This multi-channel strategy ensures UNIQA presence across all major professional advice networks, with broker channel growth of 6.5% YoY in 2024.

- 27% of premiums via brokers (2024)

- EUR 1.2bn commercial placements

- Broker channel +6.5% YoY (2024)

Embedded Insurance and Third-Party Integrations

UNIQA embeds insurance at point-of-sale via integrations with travel platforms, car dealers, and e-commerce, capturing demand when purchase intent is highest and boosting conversion rates; in 2024 embedded sales contributed roughly 6% of new business volume, up from 2% in 2021.

This channel diversifies distribution, adding annuity-like revenue streams and lowering acquisition cost per policy by ~30% versus traditional sales through agents, per UNIQA digital channel reports 2023–24.

UNIQA: Omni‑channel strength—bancassurance, agents, brokers & digital driving growth

UNIQA’s multi-channel Place mixes bancassurance (28% GWP, ~€1.1bn 2024), 2,800 branches/7,000 agents across 15+ CEE markets (€3.2bn regional premiums 2024), brokers (27% premiums, €1.2bn commercial, +6.5% YoY) and digital myUNIQA (35% new retail sales 2024; 62% self-service 2025); embedded sales ~6% new business (2024), acquisition cost ~30% lower vs agents.

| Channel | Key metric | 2024/2025 |

|---|---|---|

| Bancassurance | Share / EUR | 28% / ~€1.1bn (2024) |

| Branches & agents | Network / Regional premiums | ~2,800 / 7,000 agents; €3.2bn (2024) |

| Brokers | Share / Commercial | 27%; €1.2bn; +6.5% YoY (2024) |

| Digital myUNIQA | New sales / Self-service | 35% new retail sales (2024); 62% self-service (2025) |

| Embedded | Share / Cost | ~6% new business (2024); -30% acquisition cost vs agents |

Preview the Actual Deliverable

UNIQA Insurance Group 4P's Marketing Mix Analysis

The preview shown here is the actual UNIQA Insurance Group 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Get Inspired by a Complete Brand Strategy

Discover how UNIQA Insurance Group tailors product offerings, pricing tiers, distribution channels, and promotional campaigns to secure market share and customer loyalty—this concise preview highlights strategic strengths and opportunities. Get the full 4P’s Marketing Mix Analysis in an editable, presentation-ready format to save hours of research and apply actionable insights for benchmarking, strategy, or coursework. Purchase the complete report for data-driven clarity and ready-to-use templates.

Product

Comprehensive Health and Wellness Ecosystems

UNIQA has shifted core health insurance into a prevention-first wellness ecosystem, embedding AI diagnostics and 24/7 telemedicine to reduce acute claims and boost engagement.

By end-2025 these services cover about 1.2 million policyholders across Central and Eastern Europe, with AI triage reducing unnecessary ER visits by an estimated 18% and telehealth consultations rising 45% year-on-year.

This proactive health-partner model increases retention—UNIQA reported a 3.5 percentage-point rise in health-policy renewal rates in 2024—and targets growing private care demand while aiming to lower combined medical costs.

Flexible Life and Unit-Linked Pension Plans

UNIQA’s life portfolio centers on unit-linked plans that let policyholders tap capital market returns while keeping adjustable protection; as of 2024 UNIQA reported roughly EUR 1.2bn in unit-linked reserves, up 6% year-on-year. These policies offer premium flexibility and pause options so customers can adjust contributions across life stages—useful given EU pension dependency ratios rising toward 3 in 2050. The product targets long-term wealth accumulation and private pension top-ups to offset demographic shifts and declining public pension replacement rates.

Digital-First Property and Casualty Solutions

UNIQA Insurance Group’s Digital-First Property and Casualty solutions offer modular, mobile-managed coverage across homes, autos, and personal liability, with 60% of retail policies purchasable via app as of 2025; terms are simplified and average digital claim settlement dropped to 3.2 days in 2024. Integration with smart-home sensors and telematics enables personalized premiums—up to 25% premium discounts—and proactive loss prevention, reducing claim frequency by ~18% in pilot markets.

Tailored Corporate and Industrial Risk Management

UNIQA offers tailored corporate and industrial insurance for complex risks, liability, and employee benefits, backed by in-house risk engineering that reduces loss frequency; in 2024 UNIQA Group reported commercial premiums of ~€1.1bn, with corporate lines growing ~6% year-on-year.

By 2025 UNIQA emphasizes cyber insurance and business interruption cover—cyber accounted for ~8% of commercial product launches in 2024—and provides scenario modeling to quantify interruption losses and downtime risk.

Sustainable and ESG-Integrated Insurance Products

UNIQA offers discounted premiums for energy-efficient buildings and electric vehicle insurance, plus ESG-only investment funds, aligning products with its 2030 climate targets and EU Taxonomy rules.

In 2024 UNIQA reported over 150,000 green-policy holders and EUR 420m in ESG assets under management, boosting appeal to socially conscious investors and reducing insured carbon exposure.

- Discounts for energy-efficient buildings

- EV-specific insurance

- ESG-only investment funds (EUR 420m, 2024)

- 150,000+ green-policy holders (2024)

UNIQA pivots to prevention-first health, digital P&C growth and €1.2bn unit-linked reserves

UNIQA’s product mix shifts to prevention-first health services (1.2M users by 2025; AI triage −18% ER visits), EUR 1.2bn unit-linked life reserves (2024, +6% YoY), digital P&C with 60% app sales and 3.2-day claim settlement (2024), and commercial premiums ~€1.1bn (2024, +6% YoY); ESG: 150k green policyholders and EUR 420m AUM (2024).

| Metric | Value |

|---|---|

| Health users (2025) | 1.2M |

| Unit-linked reserves (2024) | €1.2bn |

| P&C app sales (2025) | 60% |

| Digital claim days (2024) | 3.2 |

| Commercial premiums (2024) | €1.1bn |

| Green policyholders (2024) | 150k |

| ESG AUM (2024) | €420m |

What is included in the product

Delivers a concise, company-specific deep dive into UNIQA Insurance Group’s Product, Price, Place, and Promotion strategies, using real brand practices and competitive context to ground analysis.

Condenses UNIQA Insurance Group’s 4P marketing insights into a concise, leadership-ready one-pager that clarifies product positioning, pricing strategy, distribution channels, and promotional priorities to speed decision-making and align teams.

Place

Strategic Bancassurance through Raiffeisen Bank

The long-standing Raiffeisen Bank partnership remains a cornerstone of UNIQA’s distribution across Austria and CEE, channeling roughly 28% of UNIQA Group’s 2024 gross written premiums (about EUR 1.1bn) through bancassurance; it reaches customers at key financial decision points within a trusted bank setting. The model creates a seamless handoff from banking to insurance for retail and SME clients, boosting cross-sell rates by ~14 percentage points versus direct channels and lifting persistency.

Extensive CEE Branch and Agency Network

UNIQA Insurance Group maintains a vast CEE branch and exclusive agency network across 15+ countries, with ~2,800 branches and 7,000 tied agents as of FY2024, boosting local market reach and €3.2bn in regional premiums.

Physical locations enable complex advisory services and long-term client ties—over 65% of high-net-worth policies sold in 2024 were closed face-to-face, showing strong demand for in-person counsel.

The local footprint keeps brand visible and accessible across diverse markets; branch density varies from 1.5 branches/100k people in Austria to 0.3/100k in emerging CEE states, aligning advice to local consumer behavior.

myUNIQA Digital Service and Sales Platform

The myUNIQA digital service and sales platform is UNIQA Insurance Group’s primary online hub for policy purchases and portfolio management, handling over 35% of new retail sales in 2024 and reducing paper workflows by 42% year-on-year.

By end-2025 the platform was upgraded for a frictionless UX and integrated AI chatbots (average response time 6s), cutting first-contact resolution time by 28% and boostng digital self-service rates to 62%.

Digital accessibility drives younger customer reach: 48% of users are under 35 and Net Promoter Score rose 7 points to 44 in 2025, showing improved satisfaction via convenience.

Independent Broker and Financial Advisor Channels

Partnerships with independent brokers and financial advisors extend UNIQA’s reach into niche segments and large industrial risks, covering ~27% of 2024 premiums via broker-sourced business and supporting EUR 1.2bn commercial lines placements.

These intermediaries give expert, bespoke advice that steers complex commercial clients toward UNIQA as a preferred provider, boosting retention and higher-margin accounts.

This multi-channel strategy ensures UNIQA presence across all major professional advice networks, with broker channel growth of 6.5% YoY in 2024.

- 27% of premiums via brokers (2024)

- EUR 1.2bn commercial placements

- Broker channel +6.5% YoY (2024)

Embedded Insurance and Third-Party Integrations

UNIQA embeds insurance at point-of-sale via integrations with travel platforms, car dealers, and e-commerce, capturing demand when purchase intent is highest and boosting conversion rates; in 2024 embedded sales contributed roughly 6% of new business volume, up from 2% in 2021.

This channel diversifies distribution, adding annuity-like revenue streams and lowering acquisition cost per policy by ~30% versus traditional sales through agents, per UNIQA digital channel reports 2023–24.

UNIQA: Omni‑channel strength—bancassurance, agents, brokers & digital driving growth

UNIQA’s multi-channel Place mixes bancassurance (28% GWP, ~€1.1bn 2024), 2,800 branches/7,000 agents across 15+ CEE markets (€3.2bn regional premiums 2024), brokers (27% premiums, €1.2bn commercial, +6.5% YoY) and digital myUNIQA (35% new retail sales 2024; 62% self-service 2025); embedded sales ~6% new business (2024), acquisition cost ~30% lower vs agents.

| Channel | Key metric | 2024/2025 |

|---|---|---|

| Bancassurance | Share / EUR | 28% / ~€1.1bn (2024) |

| Branches & agents | Network / Regional premiums | ~2,800 / 7,000 agents; €3.2bn (2024) |

| Brokers | Share / Commercial | 27%; €1.2bn; +6.5% YoY (2024) |

| Digital myUNIQA | New sales / Self-service | 35% new retail sales (2024); 62% self-service (2025) |

| Embedded | Share / Cost | ~6% new business (2024); -30% acquisition cost vs agents |

Preview the Actual Deliverable

UNIQA Insurance Group 4P's Marketing Mix Analysis

The preview shown here is the actual UNIQA Insurance Group 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.