Unisys SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Unisys combines deep legacy expertise in secure IT services with growing cloud and cybersecurity offerings, yet faces legacy perception, competitive pressure from major cloud providers, and margin constraints—critical factors for investors and strategists to weigh; discover how these dynamics translate to actionable risks and opportunities. Purchase the full SWOT analysis for a research-backed, editable report and Excel deliverable to inform decisions and pitches.

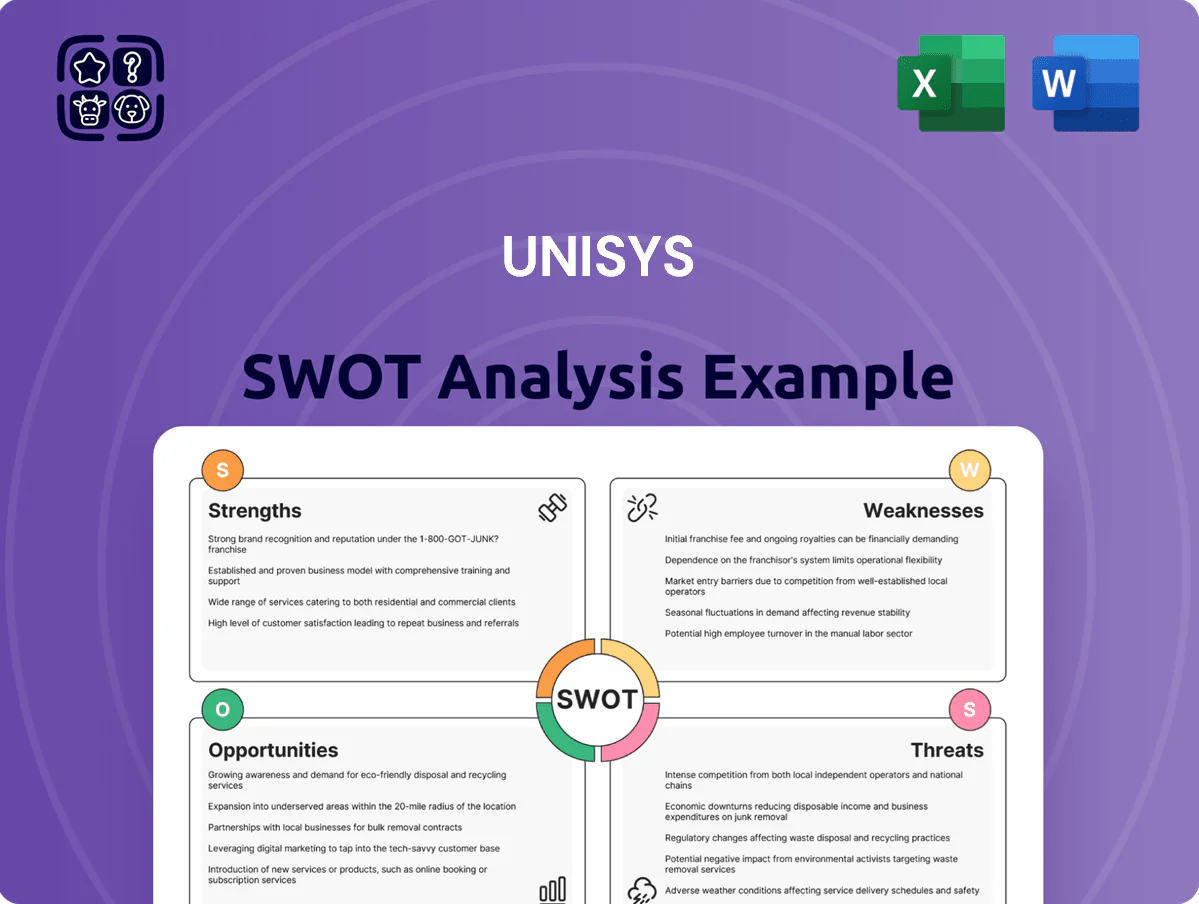

Strengths

Deeply Embedded Public Sector Relationships

Unisys holds multi-decade contracts with federal, state, and local agencies worldwide, generating roughly 30% of 2024 revenue and providing steady, predictable cash flows.

These ties rest on deep expertise in regulatory compliance and cybersecurity standards (FedRAMP, FISMA), creating high entry barriers for newcomers.

By end-2025 this public-sector segment remains a core pillar, insulating Unisys from commercial cyclicality and lowering revenue volatility.

Specialized Proprietary Technology Platforms

Advanced Cybersecurity and Zero Trust Capabilities

Unisys has positioned its Stealth security suite as a premier micro-segmentation and Zero Trust solution, with Stealth deployments reported in 28 countries and 120 enterprise clients by Q4 2025.

As cyber threats grew 35% in sophistication through 2025 (IDC), Unisys’s identity-based asset-hiding reduced breach surface for customers, lowering lateral-movement risk by up to 70% in vendor case studies.

This technical edge strengthens Unisys’s IT services mix, contributing to Stealth-related revenue growth of ~18% YoY in FY 2025 and making Unisys a go-to partner for strict data-protection needs.

Leading Digital Workplace Solutions

Unisys leads in Digital Workplace Solutions by blending AI-driven support with employee-experience design; its predictive-analytics tools cut IT incidents, improving uptime for clients—Unisys reported a 12% growth in workplace services revenue in FY2024 (year ended Sep 30, 2024).

The hybrid-work approach resolves many issues before users notice them, boosting productivity and helping land multi-year commercial contracts worth over $150M combined in 2023–2024.

- 12% workplace services revenue growth FY2024

- Predictive analytics reduce incidents pre-impact

- Human-centric tech secures ~$150M+ in contracts

Improved Financial Structure and Pension Management

Following multi-year restructuring, Unisys entered 2026 with a de-risked balance sheet and pension deficits reduced by about $600m versus 2022, freeing cash and lowering fixed legacy costs.

That capital is being redirected to cloud and AI investments, lifting R&D and capex flexibility and improving its credit profile—S&P moved sentiment to stable in 2025.

Financial discipline gives Unisys optionality for targeted M&A or organic growth, with liquidity reserves near $400m and lower pension contribution volatility.

- Pension reduction ~ $600m since 2022

- Liquidity ~ $400m entering 2026

- Credit sentiment: S&P stable (2025)

- Capital redirected to cloud/AI R&D

Unisys: Stable government cashflows, booming Stealth growth, stronger balance sheet

Unisys’s long-term government contracts (~30% of 2024 revenue) and ClearPath mainframe (≈$476M platform revenue FY2024) deliver predictable cash flows and >90% client retention; Stealth deployed in 28 countries with ~120 clients fuels ~18% FY2025 Stealth revenue growth; workplace services grew 12% in FY2024; pension cuts ~$600M since 2022 and liquidity ≈$400M entering 2026.

| Metric | Value |

|---|---|

| Govt revenue share (2024) | ~30% |

| ClearPath revenue (FY2024) | $476M |

| Client retention | >90% |

| Stealth clients (Q4 2025) | ~120 |

| Stealth revenue growth (FY2025) | ~18% YoY |

| Workplace services growth (FY2024) | 12% |

| Pension reduction since 2022 | ~$600M |

| Liquidity entering 2026 | ~$400M |

What is included in the product

Offers a concise SWOT overview of Unisys, highlighting its core strengths, operational weaknesses, strategic opportunities, and external threats shaping future performance.

Delivers a concise Unisys SWOT matrix for rapid strategic alignment, ideal for executives needing a clear snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Stagnant Top-Line Revenue Growth

Despite pivots to cloud and digital workplace services, Unisys reported flat revenue of $1.1B in FY2024, down 1% year-over-year, lagging peers growing mid-teens; declines in legacy hardware and outsourcing—down ~8% in 2024—offset digital gains, and investors question whether Unisys can shift from a legacy-dependent model to a high-growth digital leader given its modest 3% CAGR over 2019–2024.

Limited Market Share Relative to Global Tier-One Competitors

Unisys holds a modest global share versus tier-one rivals; Accenture reported $64.1B revenue (FY2024), IBM $60.5B (FY2024), TCS $27.9B (FY2024) while Unisys posted $1.2B (FY2024), limiting its economies of scale, marketing reach, and global delivery footprint.

Dependence on a Concentrated Client Base

Legacy Brand Perception Challenges

Geographic Concentration in Mature Markets

Unisys generated about 78% of revenue in North America and Europe in FY2024 (company filing, 2024), exposing it to mature, competitive IT markets with slower growth than emerging regions.

Lack of deep penetration in Asia-Pacific, Latin America, and Africa means missed access to markets growing 4–6%+ annually in 2024, raising sensitivity to regional downturns and capping upside.

- 78% revenue from NA/Europe (FY2024)

- Limited APAC/LatAm/Africa presence

- Emerging markets grew ~4–6% GDP in 2024

- Higher exposure to local downturns

Unisys $1.1B FY24: Flat growth, concentrated services and limited global scale

Unisys posted $1.1B revenue in FY2024 (flat, -1% YoY) with ~40% services revenue from a few large government/financial clients, 78% revenue from NA/Europe, headcount -6% (2024), and limited APAC/LatAm presence versus peers (Accenture $64.1B, IBM $60.5B FY2024), constraining scale, talent, and growth.

| Metric | 2024 |

|---|---|

| Revenue | $1.1B |

| Services concentration | ~40% |

| NA/Europe | 78% |

| Headcount | -6% |

Same Document Delivered

Unisys SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final analysis file. Purchase unlocks the complete, editable version with full detail and structure ready for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Unisys combines deep legacy expertise in secure IT services with growing cloud and cybersecurity offerings, yet faces legacy perception, competitive pressure from major cloud providers, and margin constraints—critical factors for investors and strategists to weigh; discover how these dynamics translate to actionable risks and opportunities. Purchase the full SWOT analysis for a research-backed, editable report and Excel deliverable to inform decisions and pitches.

Strengths

Deeply Embedded Public Sector Relationships

Unisys holds multi-decade contracts with federal, state, and local agencies worldwide, generating roughly 30% of 2024 revenue and providing steady, predictable cash flows.

These ties rest on deep expertise in regulatory compliance and cybersecurity standards (FedRAMP, FISMA), creating high entry barriers for newcomers.

By end-2025 this public-sector segment remains a core pillar, insulating Unisys from commercial cyclicality and lowering revenue volatility.

Specialized Proprietary Technology Platforms

Advanced Cybersecurity and Zero Trust Capabilities

Unisys has positioned its Stealth security suite as a premier micro-segmentation and Zero Trust solution, with Stealth deployments reported in 28 countries and 120 enterprise clients by Q4 2025.

As cyber threats grew 35% in sophistication through 2025 (IDC), Unisys’s identity-based asset-hiding reduced breach surface for customers, lowering lateral-movement risk by up to 70% in vendor case studies.

This technical edge strengthens Unisys’s IT services mix, contributing to Stealth-related revenue growth of ~18% YoY in FY 2025 and making Unisys a go-to partner for strict data-protection needs.

Leading Digital Workplace Solutions

Unisys leads in Digital Workplace Solutions by blending AI-driven support with employee-experience design; its predictive-analytics tools cut IT incidents, improving uptime for clients—Unisys reported a 12% growth in workplace services revenue in FY2024 (year ended Sep 30, 2024).

The hybrid-work approach resolves many issues before users notice them, boosting productivity and helping land multi-year commercial contracts worth over $150M combined in 2023–2024.

- 12% workplace services revenue growth FY2024

- Predictive analytics reduce incidents pre-impact

- Human-centric tech secures ~$150M+ in contracts

Improved Financial Structure and Pension Management

Following multi-year restructuring, Unisys entered 2026 with a de-risked balance sheet and pension deficits reduced by about $600m versus 2022, freeing cash and lowering fixed legacy costs.

That capital is being redirected to cloud and AI investments, lifting R&D and capex flexibility and improving its credit profile—S&P moved sentiment to stable in 2025.

Financial discipline gives Unisys optionality for targeted M&A or organic growth, with liquidity reserves near $400m and lower pension contribution volatility.

- Pension reduction ~ $600m since 2022

- Liquidity ~ $400m entering 2026

- Credit sentiment: S&P stable (2025)

- Capital redirected to cloud/AI R&D

Unisys: Stable government cashflows, booming Stealth growth, stronger balance sheet

Unisys’s long-term government contracts (~30% of 2024 revenue) and ClearPath mainframe (≈$476M platform revenue FY2024) deliver predictable cash flows and >90% client retention; Stealth deployed in 28 countries with ~120 clients fuels ~18% FY2025 Stealth revenue growth; workplace services grew 12% in FY2024; pension cuts ~$600M since 2022 and liquidity ≈$400M entering 2026.

| Metric | Value |

|---|---|

| Govt revenue share (2024) | ~30% |

| ClearPath revenue (FY2024) | $476M |

| Client retention | >90% |

| Stealth clients (Q4 2025) | ~120 |

| Stealth revenue growth (FY2025) | ~18% YoY |

| Workplace services growth (FY2024) | 12% |

| Pension reduction since 2022 | ~$600M |

| Liquidity entering 2026 | ~$400M |

What is included in the product

Offers a concise SWOT overview of Unisys, highlighting its core strengths, operational weaknesses, strategic opportunities, and external threats shaping future performance.

Delivers a concise Unisys SWOT matrix for rapid strategic alignment, ideal for executives needing a clear snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Stagnant Top-Line Revenue Growth

Despite pivots to cloud and digital workplace services, Unisys reported flat revenue of $1.1B in FY2024, down 1% year-over-year, lagging peers growing mid-teens; declines in legacy hardware and outsourcing—down ~8% in 2024—offset digital gains, and investors question whether Unisys can shift from a legacy-dependent model to a high-growth digital leader given its modest 3% CAGR over 2019–2024.

Limited Market Share Relative to Global Tier-One Competitors

Unisys holds a modest global share versus tier-one rivals; Accenture reported $64.1B revenue (FY2024), IBM $60.5B (FY2024), TCS $27.9B (FY2024) while Unisys posted $1.2B (FY2024), limiting its economies of scale, marketing reach, and global delivery footprint.

Dependence on a Concentrated Client Base

Legacy Brand Perception Challenges

Geographic Concentration in Mature Markets

Unisys generated about 78% of revenue in North America and Europe in FY2024 (company filing, 2024), exposing it to mature, competitive IT markets with slower growth than emerging regions.

Lack of deep penetration in Asia-Pacific, Latin America, and Africa means missed access to markets growing 4–6%+ annually in 2024, raising sensitivity to regional downturns and capping upside.

- 78% revenue from NA/Europe (FY2024)

- Limited APAC/LatAm/Africa presence

- Emerging markets grew ~4–6% GDP in 2024

- Higher exposure to local downturns

Unisys $1.1B FY24: Flat growth, concentrated services and limited global scale

Unisys posted $1.1B revenue in FY2024 (flat, -1% YoY) with ~40% services revenue from a few large government/financial clients, 78% revenue from NA/Europe, headcount -6% (2024), and limited APAC/LatAm presence versus peers (Accenture $64.1B, IBM $60.5B FY2024), constraining scale, talent, and growth.

| Metric | 2024 |

|---|---|

| Revenue | $1.1B |

| Services concentration | ~40% |

| NA/Europe | 78% |

| Headcount | -6% |

Same Document Delivered

Unisys SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final analysis file. Purchase unlocks the complete, editable version with full detail and structure ready for immediate use.