Unit PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping Unit’s trajectory—our concise PESTLE highlights key risks and opportunities you can act on today. Ideal for investors, strategists, and consultants, the full report provides deep-dive evidence, scenario implications, and ready-to-use slides. Purchase the complete PESTLE now to get immediately actionable insights and strategic recommendations.

Political factors

Federal Energy Policy and Leasing

Federal energy policy at the end of 2025 continues to shape Unit Corporation’s outlook, with federal land-use rules and drilling-permit protocols determining access in the Mid-Continent and Permian; Bureau of Land Management oil and gas lease sales in FY2024 generated about $1.2 billion, signaling sustained federal revenue focus.

Shifts in the executive branch and a narrowly divided Congress have led to fluctuating permit timelines—average federal permitting for new wells ranged from 90 to 240 days across regions in 2024–2025—directly affecting Unit’s project kickoff schedules.

Ongoing debates over lease moratoria and tighter environmental stipulations could reduce available federal acreage in key basins by an estimated 10–15% through 2026, constraining Unit’s near-term exploration pipeline unless mitigated by state approvals or private leases.

Geopolitical Stability and Global Supply

Ongoing international tensions in late 2025 have driven Brent to average ~$95/bbl YTD and heightened volatility, influencing Unit Drilling Company to prioritize US onshore projects with a 12% increase in domestic rig allocation versus 2024.

Political instability in major producers has underscored US energy independence, boosting domestic drilling services demand and contributing to Unit Drilling’s 18% revenue share from US operations in 2025 Q3.

Strategic capital and contract decisions are now routinely indexed to geopolitical risk metrics and crude price swings, with the company modeling scenarios across a $70–$120/bbl range for 2026 planning.

Infrastructure and Pipeline Permitting

The Unit Midstream expansion depends on political backing for pipelines and gathering systems; federal and state opposition can delay projects and reduce capacity, with recent FERC pipeline approvals falling 12% in 2024 versus 2020–2023 averages. Legislative permitting reforms remain critical—industry groups cite that streamlined permits could unlock roughly 1.2 Bcf/d of additional takeaway capacity from the Anadarko Basin over five years.

Taxation and Energy Subsidies

Corporate tax rates and energy-specific credits materially affect Unit Corporation’s net income; the US federal corporate tax rate remains 21% and the Section 45Q/45V credits and state-level incentives can reduce effective tax burdens by millions annually for drilling operators.

Policy debates through end-2025 over eliminating intangible drilling cost (IDC) deductions—historically allowing immediate expensing of up to 100% of drilling costs—or imposing carbon taxes (proposed ranges $25–$50/ton CO2) pose meaningful cash-flow and NPV risk to capital planning.

Conversely, bipartisan incentives for domestic production (leasing reforms, royalty relief, and tax credits) could lower after-tax cost of new wells, improving IRRs for capital-intensive projects; recent federal leasing revenues exceeded $1.4bn in 2024, signaling continued fiscal support.

- Federal corporate tax rate: 21%

- IDC deduction at risk through 2025; potential NPV impact: high

- Carbon tax proposals: $25–$50/ton CO2

- Section 45Q/45V and state credits reduce effective tax burden

- Federal leasing revenues: $1.4bn+ in 2024

Trade Relations and Export Policies

Export of Unit Corporation's LNG and crude hinges on favorable trade agreements and federal licenses; U.S. crude exports averaged 4.8 million bpd and LNG exports hit ~13.5 Bcf/d in 2024, so shifts in tariffs or licensing can materially change reachable markets.

Political moves on trade barriers or energy diplomacy reshape TAM for Unit's commodities; in 2024 U.S. oil export revenue exceeded $250 billion, making access to overseas buyers critical for growth.

As of late 2025 policymakers prioritize balancing domestic fuel prices with export receipts, constraining liberal export expansion despite global demand recovery.

- Dependence on federal export licenses and trade pacts

- 2024: ~4.8 million bpd crude exports, ~13.5 Bcf/d LNG

- 2024 U.S. oil export revenue > $250B

- Late-2025: policy focus on domestic price vs export revenue

Policy, permits, taxes and exports tighten U.S. upstream capex, acreage and NPV

Federal policy, permitting delays (90–240 days in 2024–25), lease sales ($1.2–1.4bn FY2024), tax rate 21%, credits (45Q/45V) and IDC risk, carbon tax proposals $25–$50/ton, export volumes (~4.8m bpd crude, ~13.5 Bcf/d LNG 2024) and geopolitical-driven Brent ~$95/bbl YTD late‑2025, together constrain acreage, capex timing, and NPV sensitivity.

| Metric | Value (2024–25) |

|---|---|

| Permitting | 90–240 days |

| Federal leasing | $1.2–1.4bn |

| Brent | ~$95/bbl YTD |

| Crude exports | ~4.8m bpd |

| LNG exports | ~13.5 Bcf/d |

What is included in the product

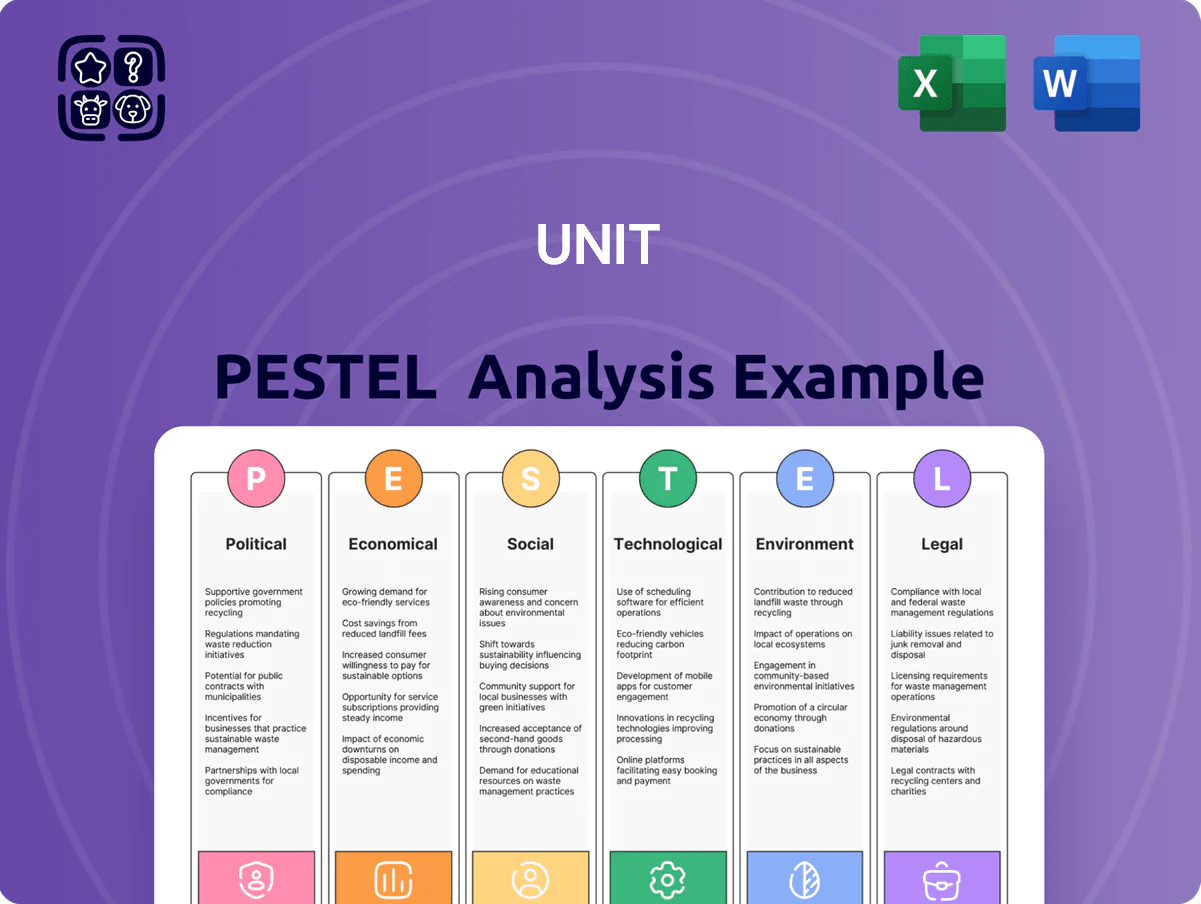

Explores how external macro-environmental factors uniquely affect the Unit across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and current trends to reveal actionable threats and opportunities.

Condenses the full PESTLE into a clean, shareable summary organized by category for quick reference in meetings or presentations, and includes editable notes so teams can adapt insights to their region or business line.

Economic factors

Commodity Price Volatility

Unit Corporation’s revenues and operating cash flow remain tightly linked to crude oil, natural gas, and NGL prices; in Q3 2025 lower realized prices pushed adjusted EBITDA down ~18% year‑over‑year, highlighting sensitivity to WTI and Henry Hub movements.

Late‑2025 volatility—WTI swinging between ~$70–$95/bbl and Henry Hub ranging $2.5–$4.5/MMBtu amid OPEC+ cuts and demand shifts—forces a flexible CAPEX plan to preserve liquidity.

Active hedging of production volumes is essential: companies in the sector report hedged protection covering ~40–60% of near‑term volumes, limiting downside from sudden benchmark drops.

Interest Rate Environment

The cost of debt remains a key constraint for Unit Corporation as it manages capital structure and funds exploration; average corporate borrowing costs rose to roughly 6.2% in 2025 versus 4.1% in 2021, raising financing costs for rig upgrades and midstream expansion. Higher rates have increased interest expense, with long-term debt yields for energy peers near 6–7% in H1 2025. Management and investors closely track central bank signals to time large investments and debt refinancing.

Labor Market Dynamics

The oil and gas sector faces a tight labor market for petroleum engineers and rig crews, with Bureau of Labor Statistics data showing petroleum engineer employment grew 3.2% in 2024 while vacancy rates for skilled rig roles exceeded 7% in major basins.

Wage inflation late 2025 pushed Unit Drilling operating wages up ~9–11% year-over-year, raising segment OPEX by an estimated 6%.

Remote areas like the Anadarko Basin now require premium pay and enhanced benefits; market surveys in 2025 report compensation packages 12–18% above national averages to secure talent.

Inflationary Pressures on Services

Inflation raised costs for specialized equipment, steel casings (U.S. steel up ~12% in 2024) and third-party oilfield services (service cost index up ~9% YoY in 2024), pressuring Unit Corporation’s E&P margins; managing supplier contracts and pass-through pricing is critical to retain EBITDA margins near 2024 levels (~18–20%).

Supply-chain disruptions eased toward late 2025 but persistent lead-time volatility requires proactive procurement, buffer inventories and multi-sourcing to avoid capex delays on wells where average completion costs rose ~8% in 2024.

- Steel casings +12% (2024)

- Service cost index +9% YoY (2024)

- Completion costs +8% (2024)

- Target EBITDA margin preservation 18–20%

Global Energy Demand Growth

- Global energy demand +6% (2023–2030, BP)

- Natural gas demand +8% by 2025 vs 2020 (IEA)

- Gas price range 2024: $7–9/MMBtu

- Recommend mid-single-digit production growth alignment

Q3 2025 EBITDA -18%: price swings, higher debt & rising input costs squeeze margins

Unit’s revenues and EBITDA remain highly price‑sensitive with Q3 2025 EBITDA down ~18% y/y as WTI ranged ~$70–$95/bbl and Henry Hub $2.5–$4.5/MMBtu; hedges typically cover 40–60% near‑term volumes. Higher debt costs (avg borrowing ~6.2% in 2025) and wage inflation (+9–11% drilling wages) raised OPEX and interest expense, while 2024 supplier cost increases (steel +12%, service index +9%, completion costs +8%) compress margins.

| Metric | Value |

|---|---|

| Q3 2025 EBITDA change | -18% y/y |

| WTI range late‑2025 | $70–$95/bbl |

| Henry Hub range | $2.5–$4.5/MMBtu |

| Avg borrowing cost 2025 | ~6.2% |

| Hedge coverage | 40–60% |

| Steel price change 2024 | +12% |

| Service cost index 2024 | +9% YoY |

Full Version Awaits

Unit PESTLE Analysis

The preview shown here is the exact Unit PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll download immediately after payment.

What you see is the final, deliverable document—clear, comprehensive, and prepared for immediate application in your strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping Unit’s trajectory—our concise PESTLE highlights key risks and opportunities you can act on today. Ideal for investors, strategists, and consultants, the full report provides deep-dive evidence, scenario implications, and ready-to-use slides. Purchase the complete PESTLE now to get immediately actionable insights and strategic recommendations.

Political factors

Federal Energy Policy and Leasing

Federal energy policy at the end of 2025 continues to shape Unit Corporation’s outlook, with federal land-use rules and drilling-permit protocols determining access in the Mid-Continent and Permian; Bureau of Land Management oil and gas lease sales in FY2024 generated about $1.2 billion, signaling sustained federal revenue focus.

Shifts in the executive branch and a narrowly divided Congress have led to fluctuating permit timelines—average federal permitting for new wells ranged from 90 to 240 days across regions in 2024–2025—directly affecting Unit’s project kickoff schedules.

Ongoing debates over lease moratoria and tighter environmental stipulations could reduce available federal acreage in key basins by an estimated 10–15% through 2026, constraining Unit’s near-term exploration pipeline unless mitigated by state approvals or private leases.

Geopolitical Stability and Global Supply

Ongoing international tensions in late 2025 have driven Brent to average ~$95/bbl YTD and heightened volatility, influencing Unit Drilling Company to prioritize US onshore projects with a 12% increase in domestic rig allocation versus 2024.

Political instability in major producers has underscored US energy independence, boosting domestic drilling services demand and contributing to Unit Drilling’s 18% revenue share from US operations in 2025 Q3.

Strategic capital and contract decisions are now routinely indexed to geopolitical risk metrics and crude price swings, with the company modeling scenarios across a $70–$120/bbl range for 2026 planning.

Infrastructure and Pipeline Permitting

The Unit Midstream expansion depends on political backing for pipelines and gathering systems; federal and state opposition can delay projects and reduce capacity, with recent FERC pipeline approvals falling 12% in 2024 versus 2020–2023 averages. Legislative permitting reforms remain critical—industry groups cite that streamlined permits could unlock roughly 1.2 Bcf/d of additional takeaway capacity from the Anadarko Basin over five years.

Taxation and Energy Subsidies

Corporate tax rates and energy-specific credits materially affect Unit Corporation’s net income; the US federal corporate tax rate remains 21% and the Section 45Q/45V credits and state-level incentives can reduce effective tax burdens by millions annually for drilling operators.

Policy debates through end-2025 over eliminating intangible drilling cost (IDC) deductions—historically allowing immediate expensing of up to 100% of drilling costs—or imposing carbon taxes (proposed ranges $25–$50/ton CO2) pose meaningful cash-flow and NPV risk to capital planning.

Conversely, bipartisan incentives for domestic production (leasing reforms, royalty relief, and tax credits) could lower after-tax cost of new wells, improving IRRs for capital-intensive projects; recent federal leasing revenues exceeded $1.4bn in 2024, signaling continued fiscal support.

- Federal corporate tax rate: 21%

- IDC deduction at risk through 2025; potential NPV impact: high

- Carbon tax proposals: $25–$50/ton CO2

- Section 45Q/45V and state credits reduce effective tax burden

- Federal leasing revenues: $1.4bn+ in 2024

Trade Relations and Export Policies

Export of Unit Corporation's LNG and crude hinges on favorable trade agreements and federal licenses; U.S. crude exports averaged 4.8 million bpd and LNG exports hit ~13.5 Bcf/d in 2024, so shifts in tariffs or licensing can materially change reachable markets.

Political moves on trade barriers or energy diplomacy reshape TAM for Unit's commodities; in 2024 U.S. oil export revenue exceeded $250 billion, making access to overseas buyers critical for growth.

As of late 2025 policymakers prioritize balancing domestic fuel prices with export receipts, constraining liberal export expansion despite global demand recovery.

- Dependence on federal export licenses and trade pacts

- 2024: ~4.8 million bpd crude exports, ~13.5 Bcf/d LNG

- 2024 U.S. oil export revenue > $250B

- Late-2025: policy focus on domestic price vs export revenue

Policy, permits, taxes and exports tighten U.S. upstream capex, acreage and NPV

Federal policy, permitting delays (90–240 days in 2024–25), lease sales ($1.2–1.4bn FY2024), tax rate 21%, credits (45Q/45V) and IDC risk, carbon tax proposals $25–$50/ton, export volumes (~4.8m bpd crude, ~13.5 Bcf/d LNG 2024) and geopolitical-driven Brent ~$95/bbl YTD late‑2025, together constrain acreage, capex timing, and NPV sensitivity.

| Metric | Value (2024–25) |

|---|---|

| Permitting | 90–240 days |

| Federal leasing | $1.2–1.4bn |

| Brent | ~$95/bbl YTD |

| Crude exports | ~4.8m bpd |

| LNG exports | ~13.5 Bcf/d |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Unit across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and current trends to reveal actionable threats and opportunities.

Condenses the full PESTLE into a clean, shareable summary organized by category for quick reference in meetings or presentations, and includes editable notes so teams can adapt insights to their region or business line.

Economic factors

Commodity Price Volatility

Unit Corporation’s revenues and operating cash flow remain tightly linked to crude oil, natural gas, and NGL prices; in Q3 2025 lower realized prices pushed adjusted EBITDA down ~18% year‑over‑year, highlighting sensitivity to WTI and Henry Hub movements.

Late‑2025 volatility—WTI swinging between ~$70–$95/bbl and Henry Hub ranging $2.5–$4.5/MMBtu amid OPEC+ cuts and demand shifts—forces a flexible CAPEX plan to preserve liquidity.

Active hedging of production volumes is essential: companies in the sector report hedged protection covering ~40–60% of near‑term volumes, limiting downside from sudden benchmark drops.

Interest Rate Environment

The cost of debt remains a key constraint for Unit Corporation as it manages capital structure and funds exploration; average corporate borrowing costs rose to roughly 6.2% in 2025 versus 4.1% in 2021, raising financing costs for rig upgrades and midstream expansion. Higher rates have increased interest expense, with long-term debt yields for energy peers near 6–7% in H1 2025. Management and investors closely track central bank signals to time large investments and debt refinancing.

Labor Market Dynamics

The oil and gas sector faces a tight labor market for petroleum engineers and rig crews, with Bureau of Labor Statistics data showing petroleum engineer employment grew 3.2% in 2024 while vacancy rates for skilled rig roles exceeded 7% in major basins.

Wage inflation late 2025 pushed Unit Drilling operating wages up ~9–11% year-over-year, raising segment OPEX by an estimated 6%.

Remote areas like the Anadarko Basin now require premium pay and enhanced benefits; market surveys in 2025 report compensation packages 12–18% above national averages to secure talent.

Inflationary Pressures on Services

Inflation raised costs for specialized equipment, steel casings (U.S. steel up ~12% in 2024) and third-party oilfield services (service cost index up ~9% YoY in 2024), pressuring Unit Corporation’s E&P margins; managing supplier contracts and pass-through pricing is critical to retain EBITDA margins near 2024 levels (~18–20%).

Supply-chain disruptions eased toward late 2025 but persistent lead-time volatility requires proactive procurement, buffer inventories and multi-sourcing to avoid capex delays on wells where average completion costs rose ~8% in 2024.

- Steel casings +12% (2024)

- Service cost index +9% YoY (2024)

- Completion costs +8% (2024)

- Target EBITDA margin preservation 18–20%

Global Energy Demand Growth

- Global energy demand +6% (2023–2030, BP)

- Natural gas demand +8% by 2025 vs 2020 (IEA)

- Gas price range 2024: $7–9/MMBtu

- Recommend mid-single-digit production growth alignment

Q3 2025 EBITDA -18%: price swings, higher debt & rising input costs squeeze margins

Unit’s revenues and EBITDA remain highly price‑sensitive with Q3 2025 EBITDA down ~18% y/y as WTI ranged ~$70–$95/bbl and Henry Hub $2.5–$4.5/MMBtu; hedges typically cover 40–60% near‑term volumes. Higher debt costs (avg borrowing ~6.2% in 2025) and wage inflation (+9–11% drilling wages) raised OPEX and interest expense, while 2024 supplier cost increases (steel +12%, service index +9%, completion costs +8%) compress margins.

| Metric | Value |

|---|---|

| Q3 2025 EBITDA change | -18% y/y |

| WTI range late‑2025 | $70–$95/bbl |

| Henry Hub range | $2.5–$4.5/MMBtu |

| Avg borrowing cost 2025 | ~6.2% |

| Hedge coverage | 40–60% |

| Steel price change 2024 | +12% |

| Service cost index 2024 | +9% YoY |

Full Version Awaits

Unit PESTLE Analysis

The preview shown here is the exact Unit PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll download immediately after payment.

What you see is the final, deliverable document—clear, comprehensive, and prepared for immediate application in your strategic decision-making.