United Airlines Holdings PESTLE Analysis

Your Competitive Advantage Starts with This Report

Navigate the turbulence facing United Airlines Holdings with a concise PESTLE snapshot—covering regulatory pressures, economic cycles, shifting consumer behavior, tech disruption, environmental mandates, and legal risks—to inform smarter investment and strategic moves; purchase the full PESTLE for granular, ready-to-use insights and downloadable files that accelerate decision-making.

Political factors

Geopolitical instability and global route access

Ongoing volatility in Eastern Europe and the Middle East constrains United Airlines’ access to high-yield routes, with 2024 data showing transatlantic and Middle East-capacity reductions of up to 8% on specific corridors. Sanctions and airspace closures forced reroutes that increased block hours by 3–6% and lifted fuel burn per affected flight by around 5–10%, raising operating costs materially given jet fuel accounted for ~19% of 2024 CASM. United maintains a diplomatic monitoring unit and scenario plans to limit network disruption and preserve revenue on premium international flows.

Governmental oversight of aviation safety and manufacturing

Following recent aerospace supply-chain defects, the FAA has stepped up oversight of maintenance and fleet integration, increasing inspections by an estimated 15% industry-wide in 2024; United faces greater regulatory pressure as it expands, risking delivery delays or groundings that could affect revenue—United reported $46.8B in 2024 revenue and a 2024 capex plan of ~$6–7B, which may rise to cover compliance costs—and must maintain transparency and close collaboration with federal authorities to protect operating certificates and public trust.

International trade policies and cargo demand

Changes in US trade agreements and tariffs with China and the EU materially affect United's cargo performance; US goods trade with China fell 8.6% in 2024 vs 2023, pressuring transpacific freight volumes handled by airlines.

As a carrier of high-value goods, United is vulnerable to protectionist measures—global air cargo tonnage slipped 3.2% in 2024—reducing yield and load factors on international routes.

Management must quickly reallocate cargo capacity to regions with favorable trade terms; United Cargo reported a 12% year-over-year revenue increase in Q3 2025 when shifting capacity to stronger Atlantic lanes after tariff shifts.

Infrastructure investment and airport modernization

The pace of government-funded projects at Newark, O'Hare and SFO directly affects United's gate throughput and on-time performance; O'Hare's $8.5bn expansion and SFO's $6.9bn program target capacity gains that could cut delays materially for United's hub operations.

Federal allocations for airport expansion and NextGen ATC upgrades (FAA FY2025 budget ~$21bn) shape congestion; slower disbursement risks higher taxi times and increased fuel/irregular operation costs for United.

United lobbies for modernization under its United Next plan, citing potential savings: reduced ground delays could improve turn times and save tens of millions annually in operational costs and fuel at major hubs.

- O'Hare expansion ~$8.5bn; SFO upgrades ~$6.9bn

- FAA FY2025 budget ~21bn impacts ATC/NextGen timing

- Modernization could save United tens of millions yearly via reduced delays

Labor relations and federal mediation

The airline sector is highly unionized; United faces collective bargaining with pilots, flight attendants and ground staff that materially affect labor costs—labor represented ~23% of 2024 operating expenses for major US carriers, pressuring margins.

Under the Railway Labor Act, federal mediation and intervention by the National Mediation Board often activate during disputes; NMB posture in 2024–25 shaped negotiation timelines and strike risks.

United must weigh pilot pay rises (recent contracts boosted pilot pay by mid‑teens %) and attendant raises against sustaining free cash flow and its 2024 net leverage targets.

- High union density => significant cost pass‑through risk

- RLA/NMB mediation can extend talks and limit strike options

- Recent pilot/attendant raises up ~10–15% increase pressure on margins

- Impacts on United’s liquidity and leverage management (2024 net debt/EBITDAR trends)

Political, regulatory, and labor shocks squeeze United: higher costs, delayed growth

Political risks—geopolitical airspace closures (8% route cuts), FAA inspection increases (~15% industry‑wide), trade/tariff shifts (US‑China trade −8.6% in 2024) and strong union bargaining (labor ~23% of ops)—raise United’s operating costs, delay fleet/expansion plans (2024 revenue $46.8B; capex $6–7B) and pressure cargo yields; mitigation includes diplomatic monitoring, regulatory collaboration and capacity reallocation.

| Metric | 2024/2025 Figure |

|---|---|

| Revenue (2024) | $46.8B |

| Capex plan (2024) | $6–7B |

| Labor % of ops | ~23% |

| FAA FY2025 budget | $21B |

| US‑China trade change 2024 | −8.6% |

What is included in the product

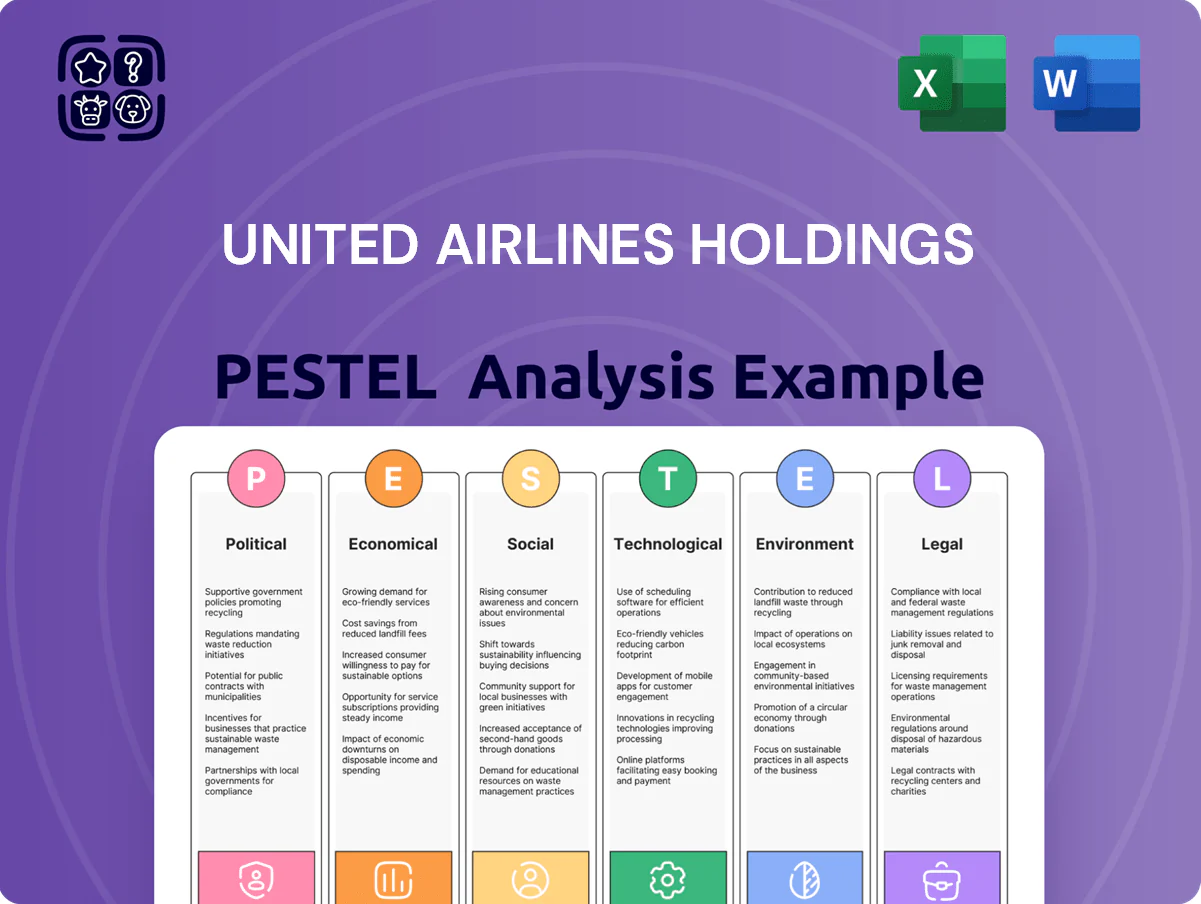

Explores how external macro-environmental factors uniquely affect United Airlines Holdings across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current trends and data to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

Condenses United Airlines Holdings' PESTLE into a clean, editable summary—segmented by political, economic, social, technological, legal, and environmental factors—so teams can quickly assess external risks, align strategy, and drop concise insights into presentations or planning decks.

Economic factors

Jet fuel price volatility and hedging strategies

Fuel is one of United’s largest and most volatile costs, accounting for about 20% of operating expenses in 2024, as jet fuel tracks global crude swings—Brent averaged roughly $86/bbl in 2024 versus $71/bbl in 2023, pressuring margins. United uses hedging and operational measures; as of Q4 2024 it maintained hedges covering a portion of consumption to cap near-term exposure. The carrier is investing in fleet renewal—51 Boeing 787s/A321neos on order—and optimizing flight paths and weight reductions to boost efficiency and blunt price spikes.

Interest rate environment and capital expenditure

The Federal Reserve's rate hikes through 2022–2024 lifted corporate borrowing costs; a 5.25–5.50% fed funds target in 2024 raised yields, meaning United’s financing for its ~500-aircraft order backlog faces higher debt service costs compared with prior low-rate years.

Higher interest expense amplifies capex funding needs as United retires older frames and takes dozens of Boeing 737/787 and Airbus A320-family jets, pressuring free cash flow and requiring disciplined balance sheet management to preserve its investment-grade access.

Inflationary pressure on labor and operational costs

Persistently high global inflation—U.S. CPI at 3.4% year-over-year in Dec 2025 and global supply-chain inflation still elevated—raises United’s labor and operational costs, including wage inflation for its 94,000 employees and pricier maintenance parts and catering. United must balance passing costs into fares—average domestic yields rose ~12% in 2024—with avoiding demand erosion after 2024 passenger revenue grew 18%. Strategic cost management, fleet productivity gains, and fuel-efficient scheduling remain essential to protect margins amid rising unit costs.

Currency exchange rate fluctuations

As a global carrier with ~34% of 2024 revenue sourced internationally, United is exposed to a strong U.S. dollar that can suppress foreign demand and make travel pricier for non‑USD customers, while a weak dollar raises costs for overseas operations and airport fees.

United uses currency hedges and geographic diversification to smooth FX impacts; in 2024 it reported a net favorable FX hedge position of about $120 million affecting operating results.

- ~34% 2024 revenue international

- Strong USD reduces foreign demand

- Weak USD increases international operating costs

- 2024 FX hedge benefit ≈ $120M

Global GDP growth and business travel recovery

United's profitability tracks global GDP and corporate travel: in 2024 business travel revenue remained ~20-25% below 2019 levels per IATA, constraining high-margin yields despite leisure demand recovery.

Full rebound of international business travel—especially between US, Europe, and Asia—remains critical for long-term growth; IMF projected 2025 global GDP growth at 3.1% (Jan 2025).

Economic shocks in London, New York or Hong Kong quickly cut premium bookings, forcing United to trim transatlantic/Asia capacity and use dynamic pricing to protect margins.

- Business travel 2024: ~20–25% below 2019 (IATA)

- IMF 2025 global GDP growth: 3.1%

- Premium yield sensitivity → capacity/pricing adjustments on major routes

Higher fuel, rates and wages squeeze United’s margins as biz travel lags recovery

Fuel (≈20% of 2024 OPEX; Brent avg $86/bbl in 2024) and higher interest rates (fed funds 5.25–5.50% in 2024) pressure margins and capex costs for United’s ~500-aircraft backlog; wage and supply inflation (U.S. CPI 3.4% Dec 2025) raise operating costs while strong USD and FX dynamics (2024 FX hedge benefit ≈ $120M) affect international demand; business travel remains ~20–25% below 2019, limiting high-yield recovery.

| Metric | 2024/2025 |

|---|---|

| Fuel share of OPEX | ≈20% |

| Brent avg | $86/bbl (2024) |

| Fed funds | 5.25–5.50% (2024) |

| FX hedge benefit | ≈$120M (2024) |

| Business travel vs 2019 | ≈20–25% below (2024) |

What You See Is What You Get

United Airlines Holdings PESTLE Analysis

The preview shown here is the exact United Airlines Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

No placeholders or teasers—this is the real, final file you’ll be able to download immediately after checkout, containing the same content, layout, and structure visible in the preview.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Navigate the turbulence facing United Airlines Holdings with a concise PESTLE snapshot—covering regulatory pressures, economic cycles, shifting consumer behavior, tech disruption, environmental mandates, and legal risks—to inform smarter investment and strategic moves; purchase the full PESTLE for granular, ready-to-use insights and downloadable files that accelerate decision-making.

Political factors

Geopolitical instability and global route access

Ongoing volatility in Eastern Europe and the Middle East constrains United Airlines’ access to high-yield routes, with 2024 data showing transatlantic and Middle East-capacity reductions of up to 8% on specific corridors. Sanctions and airspace closures forced reroutes that increased block hours by 3–6% and lifted fuel burn per affected flight by around 5–10%, raising operating costs materially given jet fuel accounted for ~19% of 2024 CASM. United maintains a diplomatic monitoring unit and scenario plans to limit network disruption and preserve revenue on premium international flows.

Governmental oversight of aviation safety and manufacturing

Following recent aerospace supply-chain defects, the FAA has stepped up oversight of maintenance and fleet integration, increasing inspections by an estimated 15% industry-wide in 2024; United faces greater regulatory pressure as it expands, risking delivery delays or groundings that could affect revenue—United reported $46.8B in 2024 revenue and a 2024 capex plan of ~$6–7B, which may rise to cover compliance costs—and must maintain transparency and close collaboration with federal authorities to protect operating certificates and public trust.

International trade policies and cargo demand

Changes in US trade agreements and tariffs with China and the EU materially affect United's cargo performance; US goods trade with China fell 8.6% in 2024 vs 2023, pressuring transpacific freight volumes handled by airlines.

As a carrier of high-value goods, United is vulnerable to protectionist measures—global air cargo tonnage slipped 3.2% in 2024—reducing yield and load factors on international routes.

Management must quickly reallocate cargo capacity to regions with favorable trade terms; United Cargo reported a 12% year-over-year revenue increase in Q3 2025 when shifting capacity to stronger Atlantic lanes after tariff shifts.

Infrastructure investment and airport modernization

The pace of government-funded projects at Newark, O'Hare and SFO directly affects United's gate throughput and on-time performance; O'Hare's $8.5bn expansion and SFO's $6.9bn program target capacity gains that could cut delays materially for United's hub operations.

Federal allocations for airport expansion and NextGen ATC upgrades (FAA FY2025 budget ~$21bn) shape congestion; slower disbursement risks higher taxi times and increased fuel/irregular operation costs for United.

United lobbies for modernization under its United Next plan, citing potential savings: reduced ground delays could improve turn times and save tens of millions annually in operational costs and fuel at major hubs.

- O'Hare expansion ~$8.5bn; SFO upgrades ~$6.9bn

- FAA FY2025 budget ~21bn impacts ATC/NextGen timing

- Modernization could save United tens of millions yearly via reduced delays

Labor relations and federal mediation

The airline sector is highly unionized; United faces collective bargaining with pilots, flight attendants and ground staff that materially affect labor costs—labor represented ~23% of 2024 operating expenses for major US carriers, pressuring margins.

Under the Railway Labor Act, federal mediation and intervention by the National Mediation Board often activate during disputes; NMB posture in 2024–25 shaped negotiation timelines and strike risks.

United must weigh pilot pay rises (recent contracts boosted pilot pay by mid‑teens %) and attendant raises against sustaining free cash flow and its 2024 net leverage targets.

- High union density => significant cost pass‑through risk

- RLA/NMB mediation can extend talks and limit strike options

- Recent pilot/attendant raises up ~10–15% increase pressure on margins

- Impacts on United’s liquidity and leverage management (2024 net debt/EBITDAR trends)

Political, regulatory, and labor shocks squeeze United: higher costs, delayed growth

Political risks—geopolitical airspace closures (8% route cuts), FAA inspection increases (~15% industry‑wide), trade/tariff shifts (US‑China trade −8.6% in 2024) and strong union bargaining (labor ~23% of ops)—raise United’s operating costs, delay fleet/expansion plans (2024 revenue $46.8B; capex $6–7B) and pressure cargo yields; mitigation includes diplomatic monitoring, regulatory collaboration and capacity reallocation.

| Metric | 2024/2025 Figure |

|---|---|

| Revenue (2024) | $46.8B |

| Capex plan (2024) | $6–7B |

| Labor % of ops | ~23% |

| FAA FY2025 budget | $21B |

| US‑China trade change 2024 | −8.6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect United Airlines Holdings across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current trends and data to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

Condenses United Airlines Holdings' PESTLE into a clean, editable summary—segmented by political, economic, social, technological, legal, and environmental factors—so teams can quickly assess external risks, align strategy, and drop concise insights into presentations or planning decks.

Economic factors

Jet fuel price volatility and hedging strategies

Fuel is one of United’s largest and most volatile costs, accounting for about 20% of operating expenses in 2024, as jet fuel tracks global crude swings—Brent averaged roughly $86/bbl in 2024 versus $71/bbl in 2023, pressuring margins. United uses hedging and operational measures; as of Q4 2024 it maintained hedges covering a portion of consumption to cap near-term exposure. The carrier is investing in fleet renewal—51 Boeing 787s/A321neos on order—and optimizing flight paths and weight reductions to boost efficiency and blunt price spikes.

Interest rate environment and capital expenditure

The Federal Reserve's rate hikes through 2022–2024 lifted corporate borrowing costs; a 5.25–5.50% fed funds target in 2024 raised yields, meaning United’s financing for its ~500-aircraft order backlog faces higher debt service costs compared with prior low-rate years.

Higher interest expense amplifies capex funding needs as United retires older frames and takes dozens of Boeing 737/787 and Airbus A320-family jets, pressuring free cash flow and requiring disciplined balance sheet management to preserve its investment-grade access.

Inflationary pressure on labor and operational costs

Persistently high global inflation—U.S. CPI at 3.4% year-over-year in Dec 2025 and global supply-chain inflation still elevated—raises United’s labor and operational costs, including wage inflation for its 94,000 employees and pricier maintenance parts and catering. United must balance passing costs into fares—average domestic yields rose ~12% in 2024—with avoiding demand erosion after 2024 passenger revenue grew 18%. Strategic cost management, fleet productivity gains, and fuel-efficient scheduling remain essential to protect margins amid rising unit costs.

Currency exchange rate fluctuations

As a global carrier with ~34% of 2024 revenue sourced internationally, United is exposed to a strong U.S. dollar that can suppress foreign demand and make travel pricier for non‑USD customers, while a weak dollar raises costs for overseas operations and airport fees.

United uses currency hedges and geographic diversification to smooth FX impacts; in 2024 it reported a net favorable FX hedge position of about $120 million affecting operating results.

- ~34% 2024 revenue international

- Strong USD reduces foreign demand

- Weak USD increases international operating costs

- 2024 FX hedge benefit ≈ $120M

Global GDP growth and business travel recovery

United's profitability tracks global GDP and corporate travel: in 2024 business travel revenue remained ~20-25% below 2019 levels per IATA, constraining high-margin yields despite leisure demand recovery.

Full rebound of international business travel—especially between US, Europe, and Asia—remains critical for long-term growth; IMF projected 2025 global GDP growth at 3.1% (Jan 2025).

Economic shocks in London, New York or Hong Kong quickly cut premium bookings, forcing United to trim transatlantic/Asia capacity and use dynamic pricing to protect margins.

- Business travel 2024: ~20–25% below 2019 (IATA)

- IMF 2025 global GDP growth: 3.1%

- Premium yield sensitivity → capacity/pricing adjustments on major routes

Higher fuel, rates and wages squeeze United’s margins as biz travel lags recovery

Fuel (≈20% of 2024 OPEX; Brent avg $86/bbl in 2024) and higher interest rates (fed funds 5.25–5.50% in 2024) pressure margins and capex costs for United’s ~500-aircraft backlog; wage and supply inflation (U.S. CPI 3.4% Dec 2025) raise operating costs while strong USD and FX dynamics (2024 FX hedge benefit ≈ $120M) affect international demand; business travel remains ~20–25% below 2019, limiting high-yield recovery.

| Metric | 2024/2025 |

|---|---|

| Fuel share of OPEX | ≈20% |

| Brent avg | $86/bbl (2024) |

| Fed funds | 5.25–5.50% (2024) |

| FX hedge benefit | ≈$120M (2024) |

| Business travel vs 2019 | ≈20–25% below (2024) |

What You See Is What You Get

United Airlines Holdings PESTLE Analysis

The preview shown here is the exact United Airlines Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

No placeholders or teasers—this is the real, final file you’ll be able to download immediately after checkout, containing the same content, layout, and structure visible in the preview.