United Homes Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

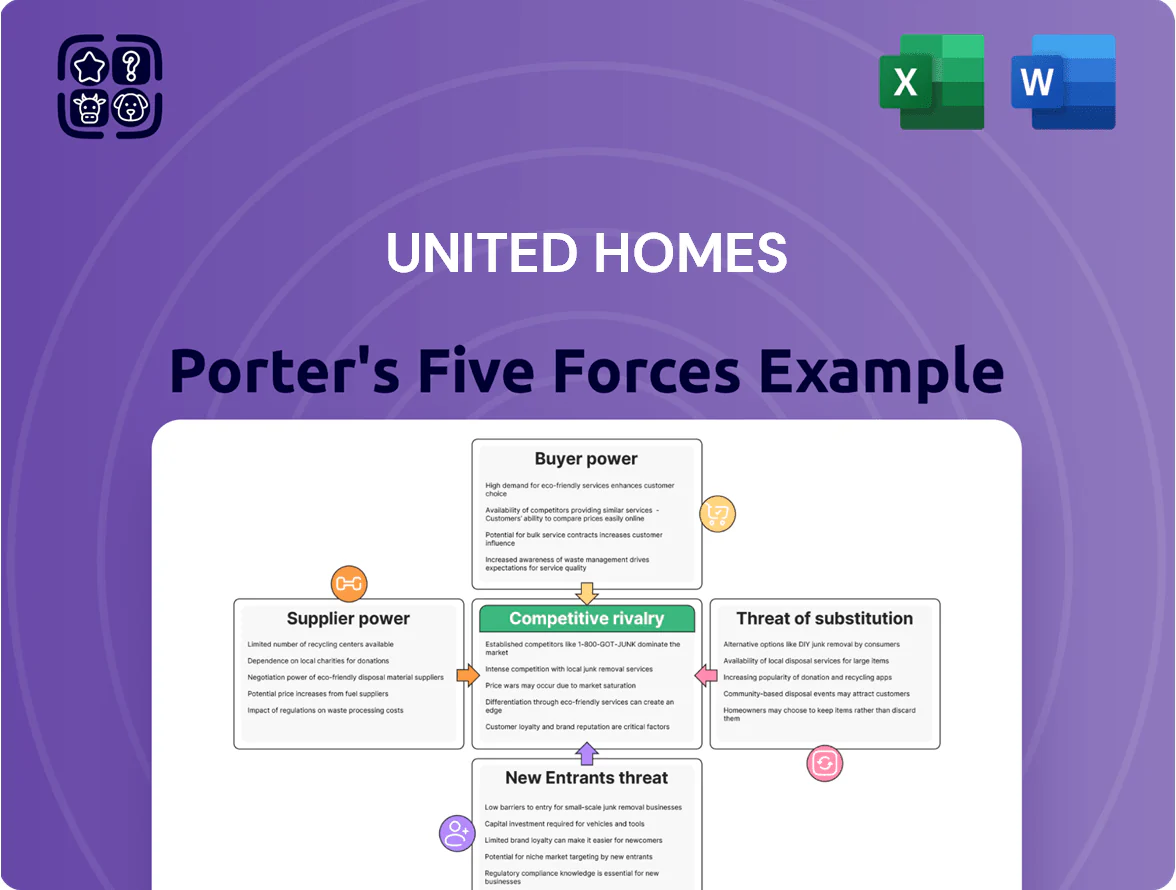

United Homes faces moderate competitive rivalry driven by regional developers and price-sensitive buyers, while supplier leverage and regulatory hurdles shape construction costs and timelines.

Buyer power and substitute threats (rentals, modular housing) pressure margins, but scale, brand recognition, and land access provide defensible advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore United Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled Labor Scarcity

Skilled labor scarcity in the Southeast leaves electricians, plumbers, and carpenters in short supply, with the Bureau of Labor Statistics reporting a 6.8% year-over-year shortfall in construction trades in 2024; subcontractors therefore can demand 8–15% higher wages and stricter pay terms. This gives suppliers leverage to push up United Homes Group’s labor costs and delay projects if capacity isn’t secured. United Homes must offer competitive pay, prompt payments, and retained subcontractor agreements to lock capacity. Maintaining these relationships reduces schedule and margin risk.

Material Cost Volatility

Suppliers of lumber, concrete, and steel hold moderate power because global commodity prices set benchmarks; lumber futures rose ~18% in 2024, and US construction steel prices were up 9% year-over-year as of Q3 2025.

Land Availability and Acquisition

The limited pool of finished lots in high-growth Southeast markets concentrates bargaining power: top 10 regional developers controlled about 62% of available permitted lots in 2024, letting sellers push prices up ~18% YoY in prime corridors.

Competition for scarce sites forces higher upfront land premiums and tougher contract terms; United Homes Group uses a land-light model to reduce exposure, but persistent permit scarcity keeps supplier leverage elevated.

Consolidation of Building Product Manufacturers

Dominant HVAC, appliance and window makers—top firms hold ~60–70% market share—can set price floors and extend lead times when housing starts rise, as seen in 2021–24 supply tightness that pushed component prices up 8–12% annually.

United Homes Group faces margin pressure if it cannot pass these higher input costs to buyers; long lead times also force inventory build or project delays, raising working capital needs and carrying costs.

- Top suppliers control ~60–70% market share

- Component prices rose 8–12% p.a. during 2021–24

- Extended lead times increase inventory and delay costs

- Margins squeeze if costs aren’t passed to buyers

Localized Subcontractor Dependence

In United Homes Group’s regional markets, typically 3–5 large subcontractors handle major community builds, concentrating local supply and raising supplier bargaining power during bids; in 2024 average subcontractor markup reached 12–18% on materials and labor in those regions.

The company must trade off lower costs versus reliability and quality—choosing a smaller bidder can cut prices 4–6% but raises schedule risk; long-term preferred contracts reduced overruns by 22% in recent projects.

- 3–5 dominant subcontractors per region

- 12–18% average subcontractor markup (2024)

- 4–6% savings vs higher schedule risk

- Preferred contracts cut overruns 22%

Supplier squeeze: rising materials, tight trades, concentrated components raise costs

Suppliers hold moderate-to-high power: skilled trades short by 6.8% (2024), subcontractor markups 12–18% (2024), top component makers 60–70% share, lumber +18% (2024), steel +9% (Q3 2025); lead times and scarce lots (top 10 developers 62% of permitted lots, 2024) raise costs and working capital needs; preferred contracts cut overruns 22%.

| Metric | Value |

|---|---|

| Skilled trade shortfall (2024) | 6.8% |

| Subcontractor markup (2024) | 12–18% |

| Component makers share | 60–70% |

| Lumber price change (2024) | +18% |

| Steel change (Q3 2025) | +9% |

What is included in the product

Tailored exclusively for United Homes, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats that affect its pricing power and market positioning.

Clear, one-sheet Porter's Five Forces for United Homes—ideal for quick strategic decisions and slide-ready summaries.

Customers Bargaining Power

Mortgage Rate Sensitivity

Homebuyers in late 2025 remain highly rate-sensitive: a 1 percentage-point rise in a 30-year mortgage cuts purchasing power by about 10%, per Freddie Mac data, pushing buyers to demand concessions.

When rates sit above 6.5% buyers gain leverage to insist on price cuts or mortgage rate buy-downs; builders often grant 0.5–1.0% buy-downs to close deals.

United Homes Group routinely offers such incentives to protect sales velocity and avoid inventory piling up—its Q3 2025 closings fell 12% when incentive offers dropped below market median.

Access to Digital Comparison Tools

Modern buyers use platforms like Zillow, Redfin, and builder portals to compare floor plans, prices, and amenities in seconds; 2024 data shows 81% of homebuyers researched online during their search, raising transparency. This shrinks information asymmetry that once favored builders and lets buyers walk away if a nearby developer offers better specs or a 3–8% lower price per sq ft.

Inventory Levels of Existing Homes

Higher inventory of resale homes raises buyers’ bargaining power: US existing-home inventory rose to 1.07 million units in Dec 2025 (NAR), up 18% year-over-year, giving buyers more choices and enabling price concessions from United Homes Group.

Demand for Entry-Level Affordability

A large share of United Homes Group buyers are first-time purchasers limited by debt-to-income rules, so price sensitivity is extreme: surveys in 2024 show 62% of UK first-time buyers would walk away if prices rose 5% or more.

That dynamic gives customers high bargaining power—if prices exceed a narrow threshold set by mortgage affordability, transactions collapse—forcing strict cost discipline and targeted entry-level pricing.

- 62% of first-time buyers exit at ≥5% price rise

- Median UK first‑time buyer deposit 2024: £38,000

- DTI caps often at 4.5x income, limiting price flexibility

Buyer Incentives and Concessions

Buyers expect upgrades, closing-cost help, or design-center credits; nationally 2024 data showed incentives averaged about 3.2% of home price, shifting leverage to consumers who shop multiple builders for best packages.

United Homes Group must balance concessions to protect margins—if average incentive equals 3% on a $400,000 home, that’s $12,000 off gross; careful targeting and standardized concession tiers limit margin erosion.

- Average incentive 3.2% of price (2024)

- $12,000 impact on $400,000 sale at 3%

- Use tiered concessions to protect margins

Buyers Hold Power: United Homes Offers ~3% Incentives to Maintain Sales Velocity

Buyers hold high bargaining power: rate sensitivity (1ppt rise ≈10% purchasing power hit, Freddie Mac), high resale inventory (1.07M units Dec 2025, NAR), heavy online search (81% 2024), and first-time buyer price elasticity (62% walk away at ≥5% price rise) force United Homes to offer ~3% incentives (~$12,000 on $400k) or tiered concessions to protect velocity and margins.

| Metric | Value |

|---|---|

| Mortgage rate sensitivity | 1ppt → ≈10% buying power |

| Existing-home inventory Dec 2025 | 1.07M units (NAR) |

| Online research 2024 | 81% |

| First-time buyers walk away | 62% at ≥5% price rise |

| Avg incentive 2024 | 3.2% (~$12k on $400k) |

Preview Before You Purchase

United Homes Porter's Five Forces Analysis

This preview shows the exact United Homes Porter’s Five Forces Analysis you’ll receive immediately after purchase—complete, professionally formatted, and ready for use with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

United Homes faces moderate competitive rivalry driven by regional developers and price-sensitive buyers, while supplier leverage and regulatory hurdles shape construction costs and timelines.

Buyer power and substitute threats (rentals, modular housing) pressure margins, but scale, brand recognition, and land access provide defensible advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore United Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled Labor Scarcity

Skilled labor scarcity in the Southeast leaves electricians, plumbers, and carpenters in short supply, with the Bureau of Labor Statistics reporting a 6.8% year-over-year shortfall in construction trades in 2024; subcontractors therefore can demand 8–15% higher wages and stricter pay terms. This gives suppliers leverage to push up United Homes Group’s labor costs and delay projects if capacity isn’t secured. United Homes must offer competitive pay, prompt payments, and retained subcontractor agreements to lock capacity. Maintaining these relationships reduces schedule and margin risk.

Material Cost Volatility

Suppliers of lumber, concrete, and steel hold moderate power because global commodity prices set benchmarks; lumber futures rose ~18% in 2024, and US construction steel prices were up 9% year-over-year as of Q3 2025.

Land Availability and Acquisition

The limited pool of finished lots in high-growth Southeast markets concentrates bargaining power: top 10 regional developers controlled about 62% of available permitted lots in 2024, letting sellers push prices up ~18% YoY in prime corridors.

Competition for scarce sites forces higher upfront land premiums and tougher contract terms; United Homes Group uses a land-light model to reduce exposure, but persistent permit scarcity keeps supplier leverage elevated.

Consolidation of Building Product Manufacturers

Dominant HVAC, appliance and window makers—top firms hold ~60–70% market share—can set price floors and extend lead times when housing starts rise, as seen in 2021–24 supply tightness that pushed component prices up 8–12% annually.

United Homes Group faces margin pressure if it cannot pass these higher input costs to buyers; long lead times also force inventory build or project delays, raising working capital needs and carrying costs.

- Top suppliers control ~60–70% market share

- Component prices rose 8–12% p.a. during 2021–24

- Extended lead times increase inventory and delay costs

- Margins squeeze if costs aren’t passed to buyers

Localized Subcontractor Dependence

In United Homes Group’s regional markets, typically 3–5 large subcontractors handle major community builds, concentrating local supply and raising supplier bargaining power during bids; in 2024 average subcontractor markup reached 12–18% on materials and labor in those regions.

The company must trade off lower costs versus reliability and quality—choosing a smaller bidder can cut prices 4–6% but raises schedule risk; long-term preferred contracts reduced overruns by 22% in recent projects.

- 3–5 dominant subcontractors per region

- 12–18% average subcontractor markup (2024)

- 4–6% savings vs higher schedule risk

- Preferred contracts cut overruns 22%

Supplier squeeze: rising materials, tight trades, concentrated components raise costs

Suppliers hold moderate-to-high power: skilled trades short by 6.8% (2024), subcontractor markups 12–18% (2024), top component makers 60–70% share, lumber +18% (2024), steel +9% (Q3 2025); lead times and scarce lots (top 10 developers 62% of permitted lots, 2024) raise costs and working capital needs; preferred contracts cut overruns 22%.

| Metric | Value |

|---|---|

| Skilled trade shortfall (2024) | 6.8% |

| Subcontractor markup (2024) | 12–18% |

| Component makers share | 60–70% |

| Lumber price change (2024) | +18% |

| Steel change (Q3 2025) | +9% |

What is included in the product

Tailored exclusively for United Homes, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats that affect its pricing power and market positioning.

Clear, one-sheet Porter's Five Forces for United Homes—ideal for quick strategic decisions and slide-ready summaries.

Customers Bargaining Power

Mortgage Rate Sensitivity

Homebuyers in late 2025 remain highly rate-sensitive: a 1 percentage-point rise in a 30-year mortgage cuts purchasing power by about 10%, per Freddie Mac data, pushing buyers to demand concessions.

When rates sit above 6.5% buyers gain leverage to insist on price cuts or mortgage rate buy-downs; builders often grant 0.5–1.0% buy-downs to close deals.

United Homes Group routinely offers such incentives to protect sales velocity and avoid inventory piling up—its Q3 2025 closings fell 12% when incentive offers dropped below market median.

Access to Digital Comparison Tools

Modern buyers use platforms like Zillow, Redfin, and builder portals to compare floor plans, prices, and amenities in seconds; 2024 data shows 81% of homebuyers researched online during their search, raising transparency. This shrinks information asymmetry that once favored builders and lets buyers walk away if a nearby developer offers better specs or a 3–8% lower price per sq ft.

Inventory Levels of Existing Homes

Higher inventory of resale homes raises buyers’ bargaining power: US existing-home inventory rose to 1.07 million units in Dec 2025 (NAR), up 18% year-over-year, giving buyers more choices and enabling price concessions from United Homes Group.

Demand for Entry-Level Affordability

A large share of United Homes Group buyers are first-time purchasers limited by debt-to-income rules, so price sensitivity is extreme: surveys in 2024 show 62% of UK first-time buyers would walk away if prices rose 5% or more.

That dynamic gives customers high bargaining power—if prices exceed a narrow threshold set by mortgage affordability, transactions collapse—forcing strict cost discipline and targeted entry-level pricing.

- 62% of first-time buyers exit at ≥5% price rise

- Median UK first‑time buyer deposit 2024: £38,000

- DTI caps often at 4.5x income, limiting price flexibility

Buyer Incentives and Concessions

Buyers expect upgrades, closing-cost help, or design-center credits; nationally 2024 data showed incentives averaged about 3.2% of home price, shifting leverage to consumers who shop multiple builders for best packages.

United Homes Group must balance concessions to protect margins—if average incentive equals 3% on a $400,000 home, that’s $12,000 off gross; careful targeting and standardized concession tiers limit margin erosion.

- Average incentive 3.2% of price (2024)

- $12,000 impact on $400,000 sale at 3%

- Use tiered concessions to protect margins

Buyers Hold Power: United Homes Offers ~3% Incentives to Maintain Sales Velocity

Buyers hold high bargaining power: rate sensitivity (1ppt rise ≈10% purchasing power hit, Freddie Mac), high resale inventory (1.07M units Dec 2025, NAR), heavy online search (81% 2024), and first-time buyer price elasticity (62% walk away at ≥5% price rise) force United Homes to offer ~3% incentives (~$12,000 on $400k) or tiered concessions to protect velocity and margins.

| Metric | Value |

|---|---|

| Mortgage rate sensitivity | 1ppt → ≈10% buying power |

| Existing-home inventory Dec 2025 | 1.07M units (NAR) |

| Online research 2024 | 81% |

| First-time buyers walk away | 62% at ≥5% price rise |

| Avg incentive 2024 | 3.2% (~$12k on $400k) |

Preview Before You Purchase

United Homes Porter's Five Forces Analysis

This preview shows the exact United Homes Porter’s Five Forces Analysis you’ll receive immediately after purchase—complete, professionally formatted, and ready for use with no placeholders or mockups.