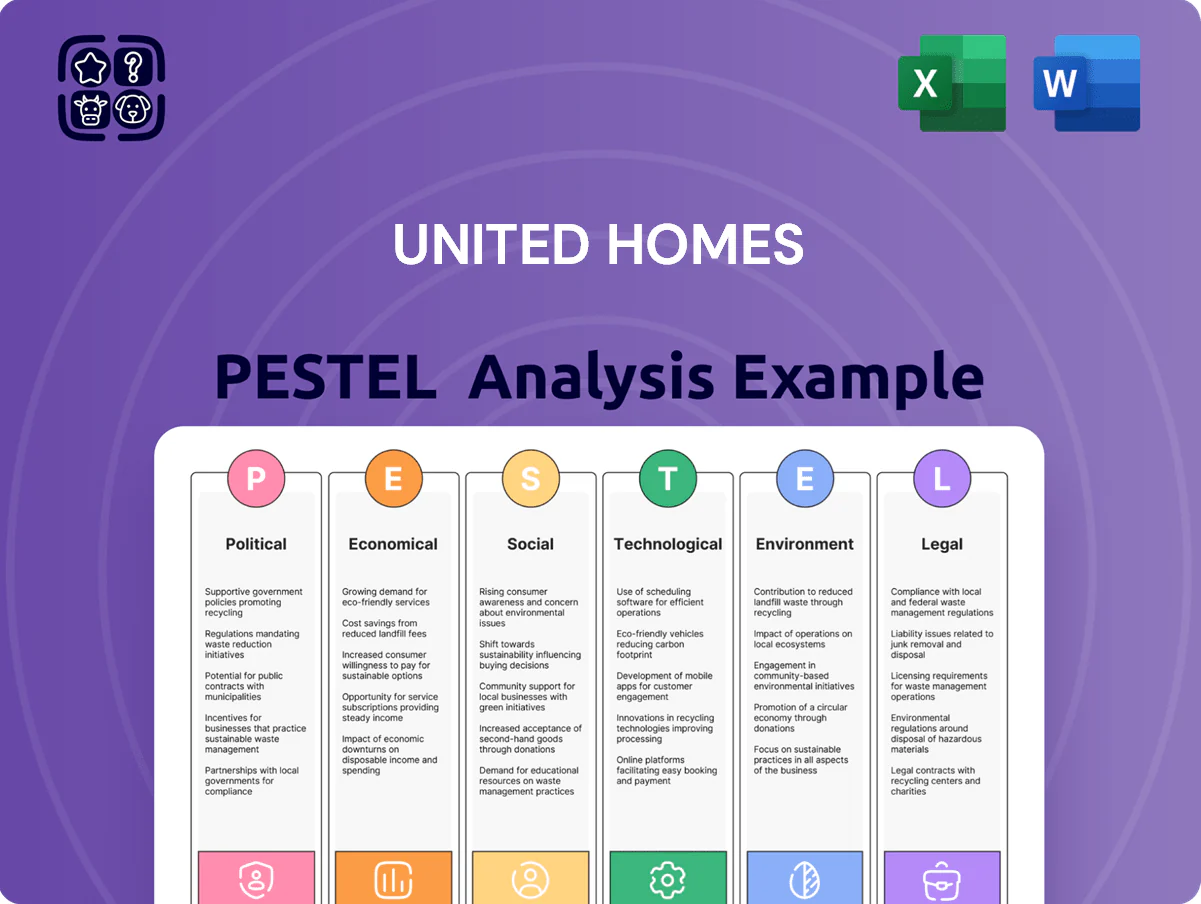

United Homes PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis of United Homes—discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape its prospects. This concise, expert report highlights risks and opportunities to inform investment or strategy decisions. Purchase the full analysis for a downloadable, editable dossier with actionable insights you can use immediately.

Political factors

Federal Housing Policy Shifts

Local Zoning and Land Use Regulations

Municipal zoning in the Southeast determines where United Homes can buy land and set density; e.g., Florida and Georgia saw 12% and 9% municipal rezoning petitions increase in 2024, tightening available parcels for suburban developments.

Local zoning boards and NIMBY opposition can delay approvals—average permitting delays rose to 6.8 months in 2024 in key markets, adding ~4–7% to project costs.

Active local political engagement and land-use monitoring are essential to keep a steady pipeline; United Homes should track >120 municipal jurisdictions across its footprint for timely site acquisition.

Infrastructure Spending and Regional Growth

State-level commitments—North Carolina budgeted $4.6bn and Georgia $3.2bn for transportation projects in 2025—boost the value of United Homes land in the Carolinas and Georgia by improving access to highways and transit hubs.

Public investment in utilities and multimodal links raises suburban desirability; studies show proximity to new transit can increase housing prices by 8–12%, directly benefiting United Homes’ sales velocity.

United Homes depends on these political priorities to keep remote/suburban communities accessible and marketable, aligning project timelines with announced state infrastructure rollouts through 2026.

Trade Policies and Material Tariffs

International trade relations and tariffs on imported lumber, steel, and aluminum drove US construction input prices up to 18% in 2022–2023, and a 2024 US tariff increase of 10% on certain steel imports raised costs for builders by roughly 3–5% on average.

Political shifts toward protectionism can trigger sudden supply-chain price spikes, squeezing United Homes margins if costs cannot be passed to buyers amid 2024 housing affordability pressures.

Monitoring trade agreements like USMCA and recent EU–US dialogues is vital for procurement and dynamic pricing to protect margins.

- Tariff-driven input inflation: up to 18% (2022–23)

- 2024 US steel tariff ~10% → +3–5% builder costs

- Track USMCA, EU–US talks for sourcing shifts

Government Incentives for Energy Efficiency

Federal and state tax credits and rebates—such as the 2025 Residential Clean Energy Credit offering up to 30% tax offset and state-level incentives covering 10–25% of retrofit costs—push United Homes to integrate high-efficiency HVAC, insulation, and smart meters into new designs to qualify for programs.

Noncompliance with evolving IECC/ASHRAE-based energy codes risks losing access to subsidies and financing tied to energy performance, impacting project margins and capital availability.

These mandates set minimum technology baselines—heat-pump readiness, LED lighting, and home energy management systems—raising upfront build costs by an estimated 3–6% but reducing lifecycle energy spend by 20–30%.

- 30% federal tax credit (Residential Clean Energy, 2025)

- State rebates 10–25% of retrofit costs

- Upfront build cost +3–6%, lifecycle energy savings 20–30%

- Must meet IECC/ASHRAE-based codes to qualify for funding

Federal subsidies and tax credits spur United Homes demand amid permitting and cost pressures

| Factor | Key Data (2024–25) |

|---|---|

| First-time buyer share | 42% of 2024 sales |

| Housing starts | +8% YoY (2024) |

| Permitting delay | 6.8 months (2024) |

| Steel tariff impact | +10% tariff → +3–5% costs |

| State infra budgets | NC $4.6bn; GA $3.2bn (2025) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact United Homes, with each section backed by current data and trends to highlight risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of United Homes that’s easy to drop into presentations or planning sessions, enabling quick interpretation of external risks and strategic opportunities while allowing users to add context-specific notes for team alignment.

Economic factors

Interest Rate Volatility and Mortgage Affordability

Fluctuations in the federal funds rate through 2025 kept 30-year mortgage rates between ~6.5%–7.5% in late 2024/early 2025, cutting purchasing power and shrinking eligible buyers for move-up homes by an estimated 20–30%. Lower-rate episodes historically boosted demand by 25%+, so United Homes should recalibrate financing incentives, offer rate buydowns and flexible price points to protect volumes as rate volatility persists.

Regional Employment and Income Levels

Southeast US job growth—notably 2.8% annual payroll gains in tech and manufacturing clusters in 2024—boosts demand for United Homes’ modular and single-family builds. Rising median household income in core markets (up 4.1% YoY to $64,200 in 2024) increases acceptable price points and supports higher per-unit ASPs. A regional downturn would compress sales velocity and slow inventory turnover, risking longer holding periods and margin pressure.

Inflationary Pressures on Construction Costs

Persistent inflation in labor and materials—U.S. construction wage growth ~4.5% YoY and lumber +18% since 2023—pressures United Homes’ gross margins; management reported lot development cost sensitivity despite a partial land-light model, with finished-lot per-unit costs moving 6–12% with economic cycles. Balancing input inflation against median U.S. new-home price rises (~6% YoY in 2024) is a core financial challenge.

Housing Inventory Shortages

The US existing-home inventory hit a 25-year low in 2024, with available listings down roughly 15% year-over-year, positioning new homebuilders as the primary supply source; this supports 8-12% premium pricing in high-demand metros and keeps absorption rates near historical averages of 6–8 months even amid economic uncertainty.

United Homes leverages this gap to grow in key residential corridors, reporting a 22% backlog increase and average order conversion up 18% in 2024 as buyers shift from scarce resale stock to new construction.

- Existing listings down ~15% YoY (2024)

- Premium pricing +8–12% in top metros

- Absorption ~6–8 months

- United Homes backlog +22%, conversions +18% (2024)

Consumer Confidence and Spending Patterns

Rising consumer confidence drives willingness to take on 30-year mortgages; the Conference Board Consumer Confidence index averaged 103.0 in 2024, up from 102.9 in 2023, correlating with a 6% increase in move-up home purchases nationally.

When confidence falls, United Homes shifts toward entry-level inventory; mortgage applications dropped 8% in Q3 2024 as the 30-year fixed rate averaged 6.9%—tightening demand for luxury upgrades.

United Homes actively tracks these indicators monthly to time pivots between entry-level and luxury-tier offerings, targeting a 10–15% margin preservation during upcycles.

- Conference Board index ~103 (2024)

- Move-up purchases +6% (2024)

- 30-year fixed avg 6.9% (Q3 2024)

- Mortgage apps -8% (Q3 2024)

- Target margin preservation 10–15%

Higher rates shrink buyers but tight listings, income growth and backlogs support premiums

Mortgage rates ~6.5–7.5% (late 2024–early 2025) trim buyer pool ~20–30%; Southeast payrolls +2.8% (2024) and median household income +4.1% to $64,200 bolster demand; construction wage +4.5% YoY and lumber +18% since 2023 pressure margins; existing listings -15% (2024) support 8–12% premium pricing and UNTD backlog +22% (2024).

| Metric | Value (2024) |

|---|---|

| 30y mortgage | 6.5–7.5% |

| Median HH income | $64,200 (+4.1%) |

| Listings | -15% YoY |

| UNTD backlog | +22% |

Preview Before You Purchase

United Homes PESTLE Analysis

The preview shown here is the exact United Homes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

No placeholders or teasers: the layout, content, and insights visible in this preview are the final document you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis of United Homes—discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape its prospects. This concise, expert report highlights risks and opportunities to inform investment or strategy decisions. Purchase the full analysis for a downloadable, editable dossier with actionable insights you can use immediately.

Political factors

Federal Housing Policy Shifts

Local Zoning and Land Use Regulations

Municipal zoning in the Southeast determines where United Homes can buy land and set density; e.g., Florida and Georgia saw 12% and 9% municipal rezoning petitions increase in 2024, tightening available parcels for suburban developments.

Local zoning boards and NIMBY opposition can delay approvals—average permitting delays rose to 6.8 months in 2024 in key markets, adding ~4–7% to project costs.

Active local political engagement and land-use monitoring are essential to keep a steady pipeline; United Homes should track >120 municipal jurisdictions across its footprint for timely site acquisition.

Infrastructure Spending and Regional Growth

State-level commitments—North Carolina budgeted $4.6bn and Georgia $3.2bn for transportation projects in 2025—boost the value of United Homes land in the Carolinas and Georgia by improving access to highways and transit hubs.

Public investment in utilities and multimodal links raises suburban desirability; studies show proximity to new transit can increase housing prices by 8–12%, directly benefiting United Homes’ sales velocity.

United Homes depends on these political priorities to keep remote/suburban communities accessible and marketable, aligning project timelines with announced state infrastructure rollouts through 2026.

Trade Policies and Material Tariffs

International trade relations and tariffs on imported lumber, steel, and aluminum drove US construction input prices up to 18% in 2022–2023, and a 2024 US tariff increase of 10% on certain steel imports raised costs for builders by roughly 3–5% on average.

Political shifts toward protectionism can trigger sudden supply-chain price spikes, squeezing United Homes margins if costs cannot be passed to buyers amid 2024 housing affordability pressures.

Monitoring trade agreements like USMCA and recent EU–US dialogues is vital for procurement and dynamic pricing to protect margins.

- Tariff-driven input inflation: up to 18% (2022–23)

- 2024 US steel tariff ~10% → +3–5% builder costs

- Track USMCA, EU–US talks for sourcing shifts

Government Incentives for Energy Efficiency

Federal and state tax credits and rebates—such as the 2025 Residential Clean Energy Credit offering up to 30% tax offset and state-level incentives covering 10–25% of retrofit costs—push United Homes to integrate high-efficiency HVAC, insulation, and smart meters into new designs to qualify for programs.

Noncompliance with evolving IECC/ASHRAE-based energy codes risks losing access to subsidies and financing tied to energy performance, impacting project margins and capital availability.

These mandates set minimum technology baselines—heat-pump readiness, LED lighting, and home energy management systems—raising upfront build costs by an estimated 3–6% but reducing lifecycle energy spend by 20–30%.

- 30% federal tax credit (Residential Clean Energy, 2025)

- State rebates 10–25% of retrofit costs

- Upfront build cost +3–6%, lifecycle energy savings 20–30%

- Must meet IECC/ASHRAE-based codes to qualify for funding

Federal subsidies and tax credits spur United Homes demand amid permitting and cost pressures

| Factor | Key Data (2024–25) |

|---|---|

| First-time buyer share | 42% of 2024 sales |

| Housing starts | +8% YoY (2024) |

| Permitting delay | 6.8 months (2024) |

| Steel tariff impact | +10% tariff → +3–5% costs |

| State infra budgets | NC $4.6bn; GA $3.2bn (2025) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact United Homes, with each section backed by current data and trends to highlight risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of United Homes that’s easy to drop into presentations or planning sessions, enabling quick interpretation of external risks and strategic opportunities while allowing users to add context-specific notes for team alignment.

Economic factors

Interest Rate Volatility and Mortgage Affordability

Fluctuations in the federal funds rate through 2025 kept 30-year mortgage rates between ~6.5%–7.5% in late 2024/early 2025, cutting purchasing power and shrinking eligible buyers for move-up homes by an estimated 20–30%. Lower-rate episodes historically boosted demand by 25%+, so United Homes should recalibrate financing incentives, offer rate buydowns and flexible price points to protect volumes as rate volatility persists.

Regional Employment and Income Levels

Southeast US job growth—notably 2.8% annual payroll gains in tech and manufacturing clusters in 2024—boosts demand for United Homes’ modular and single-family builds. Rising median household income in core markets (up 4.1% YoY to $64,200 in 2024) increases acceptable price points and supports higher per-unit ASPs. A regional downturn would compress sales velocity and slow inventory turnover, risking longer holding periods and margin pressure.

Inflationary Pressures on Construction Costs

Persistent inflation in labor and materials—U.S. construction wage growth ~4.5% YoY and lumber +18% since 2023—pressures United Homes’ gross margins; management reported lot development cost sensitivity despite a partial land-light model, with finished-lot per-unit costs moving 6–12% with economic cycles. Balancing input inflation against median U.S. new-home price rises (~6% YoY in 2024) is a core financial challenge.

Housing Inventory Shortages

The US existing-home inventory hit a 25-year low in 2024, with available listings down roughly 15% year-over-year, positioning new homebuilders as the primary supply source; this supports 8-12% premium pricing in high-demand metros and keeps absorption rates near historical averages of 6–8 months even amid economic uncertainty.

United Homes leverages this gap to grow in key residential corridors, reporting a 22% backlog increase and average order conversion up 18% in 2024 as buyers shift from scarce resale stock to new construction.

- Existing listings down ~15% YoY (2024)

- Premium pricing +8–12% in top metros

- Absorption ~6–8 months

- United Homes backlog +22%, conversions +18% (2024)

Consumer Confidence and Spending Patterns

Rising consumer confidence drives willingness to take on 30-year mortgages; the Conference Board Consumer Confidence index averaged 103.0 in 2024, up from 102.9 in 2023, correlating with a 6% increase in move-up home purchases nationally.

When confidence falls, United Homes shifts toward entry-level inventory; mortgage applications dropped 8% in Q3 2024 as the 30-year fixed rate averaged 6.9%—tightening demand for luxury upgrades.

United Homes actively tracks these indicators monthly to time pivots between entry-level and luxury-tier offerings, targeting a 10–15% margin preservation during upcycles.

- Conference Board index ~103 (2024)

- Move-up purchases +6% (2024)

- 30-year fixed avg 6.9% (Q3 2024)

- Mortgage apps -8% (Q3 2024)

- Target margin preservation 10–15%

Higher rates shrink buyers but tight listings, income growth and backlogs support premiums

Mortgage rates ~6.5–7.5% (late 2024–early 2025) trim buyer pool ~20–30%; Southeast payrolls +2.8% (2024) and median household income +4.1% to $64,200 bolster demand; construction wage +4.5% YoY and lumber +18% since 2023 pressure margins; existing listings -15% (2024) support 8–12% premium pricing and UNTD backlog +22% (2024).

| Metric | Value (2024) |

|---|---|

| 30y mortgage | 6.5–7.5% |

| Median HH income | $64,200 (+4.1%) |

| Listings | -15% YoY |

| UNTD backlog | +22% |

Preview Before You Purchase

United Homes PESTLE Analysis

The preview shown here is the exact United Homes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

No placeholders or teasers: the layout, content, and insights visible in this preview are the final document you’ll download immediately after payment.