United Parks & Resorts Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

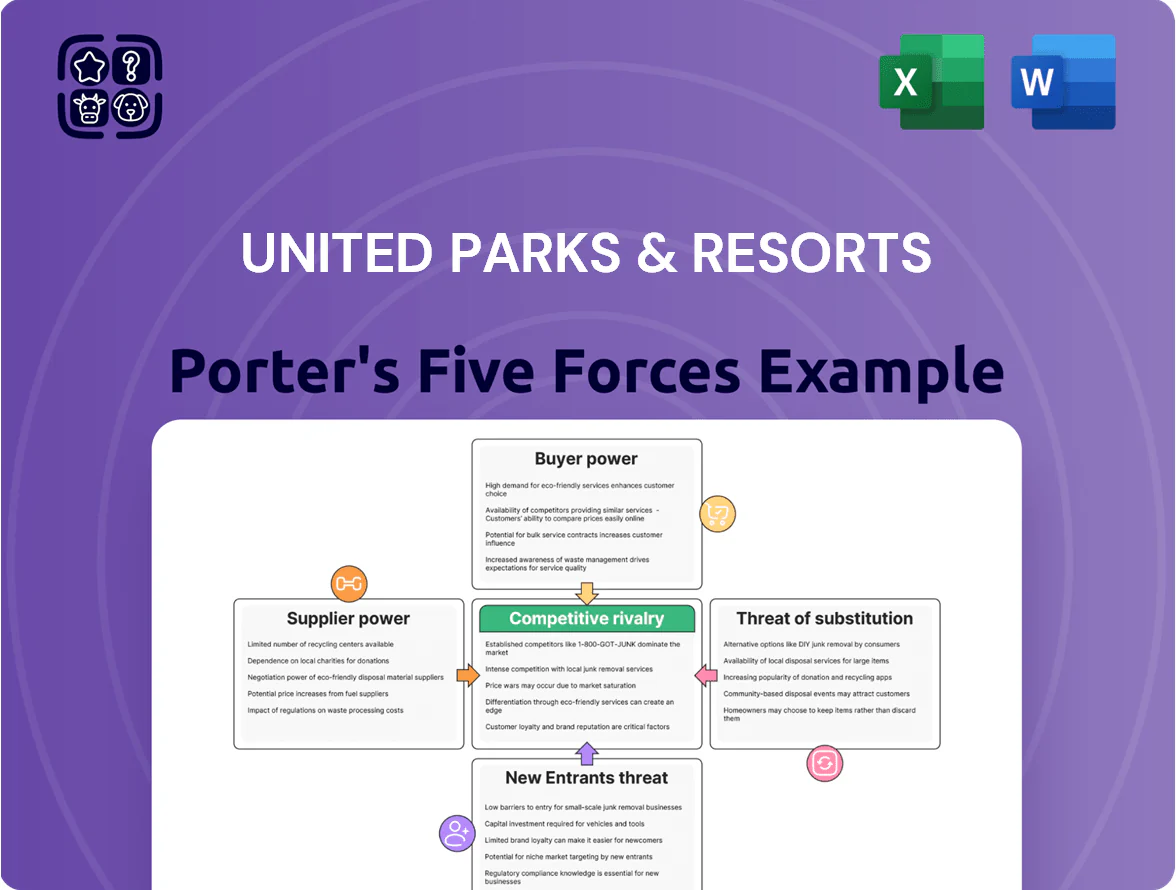

United Parks & Resorts faces moderate rivalry from established theme-park operators, rising buyer expectations, and growing substitute entertainment options, while capital-intensive barriers and selective supplier leverage shape its strategic posture; this snapshot highlights key pressure points and opportunity levers. Unlock the full Porter's Five Forces Analysis to explore granular force ratings, visuals, and actionable strategies tailored to United Parks & Resorts.

Suppliers Bargaining Power

Concentration of Specialized Ride Manufacturers

The high-end roller-coaster market is highly concentrated: by 2024 three firms—Bolliger & Mabillard (B&M), Intamin, and Vekoma—accounted for roughly 70% of top-tier installations, giving United Parks & Resorts few alternatives for marquee attractions.

These suppliers' proprietary engineering and 99%+ safety incident-free records for major projects let them command price premiums; recent headline coasters cost $15–30m each, pressuring capital budgets.

Limited vendor options also shift schedule risk to buyers: delivery lead times often run 18–36 months, constraining park restart and marketing timelines.

Animal Care and Veterinary Specialization

Maintaining marine and terrestrial collections forces United Parks & Resorts to buy niche medical supplies, specialty organic diets, and expert veterinary consulting; fewer than 10 global suppliers meet killer whale/dolphin/manatee needs, giving them pricing power that can raise animal-health costs by 12–18% annually and push conservation-compliance spend above $4.5M per major park per year.

Utility and Energy Dependence

Theme parks, especially water-heavy sites like SeaWorld and Discovery Cove, consume vast electricity and water-filtration resources—SeaWorld Orlando reported 2024 utility costs near $28m across parks, highlighting scale.

United Parks & Resorts often relies on regional utility monopolies for power and water, leaving little room to negotiate rates and increasing supplier bargaining power.

Energy price swings feed directly into margins; a 10% rise in electricity rates can cut operating profit by ~2–3% for comparable parks, since substitutes are limited.

Geographic Real Estate and Land Constraints

Suppliers of land and long-term leases in prime hubs like Orlando, San Diego, and San Antonio wield strong leverage as development tightens; average Orlando land prices rose ~18% in 2024, pushing parcel scarcity and costs up for theme operators.

United Parks often must negotiate with municipalities or private developers who know the company’s locational dependence, raising leasing premiums and zoning concession demands that compress project IRRs.

Here’s the quick math: a 20% land-cost jump can cut a park’s NPV by ~10% on typical 20-year cash flows.

- Prime-hub scarcity increases supplier leverage

- Orlando 2024 land price +18% (example)

- Higher lease/zoning costs lower project IRR

- 20% land cost rise ≈ 10% NPV cut

Labor Market Dynamics

The company depends on large seasonal and specialized crews—ride ops to marine biologists—and a tight 2024–25 U.S. labor market raised wages: hospitality wages grew 6.8% year-over-year in 2024, forcing United Parks & Resorts to increase pay and benefits to retain staff.

Pressure is worst in Florida where three major operators compete for the same talent pool, driving turnover up and labor costs higher by an estimated 4–7% versus noncoastal locations.

- Seasonal/specialized roles = high supplier power

- Hospitality wages +6.8% (2024)

- Florida labor premium ≈ +4–7%

- Raises, benefits needed to hold service levels

Supplier oligopolies, rising costs and land/labor squeeze erode park margins

Suppliers hold strong leverage: three coaster firms (B&M, Intamin, Vekoma) ≈70% market share (2024), marquee coasters cost $15–30m, lead times 18–36 months; niche marine suppliers <10 global vendors, animal-health costs +12–18% y/y and conservation spend >$4.5M/major park; utilities/land/seasonal labor (hospitality wages +6.8% in 2024; Orlando land +18% 2024) compress margins.

| Category | 2024/2025 Metric |

|---|---|

| Coaster suppliers | 3 firms ≈70% share; $15–30M each |

| Coaster lead time | 18–36 months |

| Marine suppliers | <10 global vendors; animal-health +12–18% y/y |

| Conservation spend | >$4.5M per major park/yr |

| Utilities | SeaWorld parks ≈$28M utilities (2024) |

| Land prices | Orlando +18% (2024) |

| Labor | Hospitality wages +6.8% (2024); FL premium +4–7% |

What is included in the product

Tailored exclusively for United Parks & Resorts, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats—delivering strategic insights to assess pricing, profitability, and market positioning.

Quickly assess United Parks & Resorts’ competitive pressures with a one-sheet Porter’s Five Forces summary—ideal for boardrooms and pitch decks.

Customers Bargaining Power

Low Switching Costs for Families

Price Sensitivity and Promotional Reliance

Influence of Online Reviews and Social Media

In the digital age a single viral video on animal welfare can cut bookings sharply; 2024 data show travel review sites influence 81% of leisure choices and a 1-star decline on TripAdvisor can lower occupancy by ~5–7% within 90 days.

Guests and influencers use TripAdvisor, Instagram, and TikTok to pressure United Parks & Resorts on maintenance and ethics, driving immediate cancellations and refund costs that erode short-term revenue.

This transparency gives the collective consumer base strong bargaining power to force policy changes, brand-restoration spend, and ongoing PR budgets often amounting to millions annually.

Abundance of Entertainment Alternatives

- Global travel spend 2024: $1.5T

- Avg U.S. household travel spend 2024: $3,500

- High customer selectivity raises quality and program expectations

Volume Power of Group and Corporate Sales

Large organizations, school districts, and travel agencies buying tickets in bulk extract strong volume discounts; corporate group sales accounted for about 18% of United Parks & Resorts' 2024 attendance and roughly 14% of ticket revenue, so losing a key partner can dent quarterly earnings.

These buyers give predictable, recurring revenue—contracts often span seasons—forcing United Parks to match specific pricing, capacity, and amenity requests to retain accounts and protect margin.

- Group sales ≈18% attendance (2024)

- Group ticket revenue ≈14% total (2024)

- Large-account churn impacts quarterly EPS

Price-sensitive guests, reviews & group buyers squeeze United Parks’ margins

| Metric | Value (2024) |

|---|---|

| Avg household theme-park spend | $1,200 |

| Promotions share of visits | 18% |

| Review influence on choices | 81% |

| Occupancy drop per 1-star loss | 5–7% |

| Group attendance | 18% |

| Group ticket revenue | 14% |

Preview Before You Purchase

United Parks & Resorts Porter's Five Forces Analysis

This preview shows the exact United Parks & Resorts Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

You're looking at the final deliverable: the same professionally written file will be available for instant download upon payment, prepared for strategic review and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

United Parks & Resorts faces moderate rivalry from established theme-park operators, rising buyer expectations, and growing substitute entertainment options, while capital-intensive barriers and selective supplier leverage shape its strategic posture; this snapshot highlights key pressure points and opportunity levers. Unlock the full Porter's Five Forces Analysis to explore granular force ratings, visuals, and actionable strategies tailored to United Parks & Resorts.

Suppliers Bargaining Power

Concentration of Specialized Ride Manufacturers

The high-end roller-coaster market is highly concentrated: by 2024 three firms—Bolliger & Mabillard (B&M), Intamin, and Vekoma—accounted for roughly 70% of top-tier installations, giving United Parks & Resorts few alternatives for marquee attractions.

These suppliers' proprietary engineering and 99%+ safety incident-free records for major projects let them command price premiums; recent headline coasters cost $15–30m each, pressuring capital budgets.

Limited vendor options also shift schedule risk to buyers: delivery lead times often run 18–36 months, constraining park restart and marketing timelines.

Animal Care and Veterinary Specialization

Maintaining marine and terrestrial collections forces United Parks & Resorts to buy niche medical supplies, specialty organic diets, and expert veterinary consulting; fewer than 10 global suppliers meet killer whale/dolphin/manatee needs, giving them pricing power that can raise animal-health costs by 12–18% annually and push conservation-compliance spend above $4.5M per major park per year.

Utility and Energy Dependence

Theme parks, especially water-heavy sites like SeaWorld and Discovery Cove, consume vast electricity and water-filtration resources—SeaWorld Orlando reported 2024 utility costs near $28m across parks, highlighting scale.

United Parks & Resorts often relies on regional utility monopolies for power and water, leaving little room to negotiate rates and increasing supplier bargaining power.

Energy price swings feed directly into margins; a 10% rise in electricity rates can cut operating profit by ~2–3% for comparable parks, since substitutes are limited.

Geographic Real Estate and Land Constraints

Suppliers of land and long-term leases in prime hubs like Orlando, San Diego, and San Antonio wield strong leverage as development tightens; average Orlando land prices rose ~18% in 2024, pushing parcel scarcity and costs up for theme operators.

United Parks often must negotiate with municipalities or private developers who know the company’s locational dependence, raising leasing premiums and zoning concession demands that compress project IRRs.

Here’s the quick math: a 20% land-cost jump can cut a park’s NPV by ~10% on typical 20-year cash flows.

- Prime-hub scarcity increases supplier leverage

- Orlando 2024 land price +18% (example)

- Higher lease/zoning costs lower project IRR

- 20% land cost rise ≈ 10% NPV cut

Labor Market Dynamics

The company depends on large seasonal and specialized crews—ride ops to marine biologists—and a tight 2024–25 U.S. labor market raised wages: hospitality wages grew 6.8% year-over-year in 2024, forcing United Parks & Resorts to increase pay and benefits to retain staff.

Pressure is worst in Florida where three major operators compete for the same talent pool, driving turnover up and labor costs higher by an estimated 4–7% versus noncoastal locations.

- Seasonal/specialized roles = high supplier power

- Hospitality wages +6.8% (2024)

- Florida labor premium ≈ +4–7%

- Raises, benefits needed to hold service levels

Supplier oligopolies, rising costs and land/labor squeeze erode park margins

Suppliers hold strong leverage: three coaster firms (B&M, Intamin, Vekoma) ≈70% market share (2024), marquee coasters cost $15–30m, lead times 18–36 months; niche marine suppliers <10 global vendors, animal-health costs +12–18% y/y and conservation spend >$4.5M/major park; utilities/land/seasonal labor (hospitality wages +6.8% in 2024; Orlando land +18% 2024) compress margins.

| Category | 2024/2025 Metric |

|---|---|

| Coaster suppliers | 3 firms ≈70% share; $15–30M each |

| Coaster lead time | 18–36 months |

| Marine suppliers | <10 global vendors; animal-health +12–18% y/y |

| Conservation spend | >$4.5M per major park/yr |

| Utilities | SeaWorld parks ≈$28M utilities (2024) |

| Land prices | Orlando +18% (2024) |

| Labor | Hospitality wages +6.8% (2024); FL premium +4–7% |

What is included in the product

Tailored exclusively for United Parks & Resorts, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats—delivering strategic insights to assess pricing, profitability, and market positioning.

Quickly assess United Parks & Resorts’ competitive pressures with a one-sheet Porter’s Five Forces summary—ideal for boardrooms and pitch decks.

Customers Bargaining Power

Low Switching Costs for Families

Price Sensitivity and Promotional Reliance

Influence of Online Reviews and Social Media

In the digital age a single viral video on animal welfare can cut bookings sharply; 2024 data show travel review sites influence 81% of leisure choices and a 1-star decline on TripAdvisor can lower occupancy by ~5–7% within 90 days.

Guests and influencers use TripAdvisor, Instagram, and TikTok to pressure United Parks & Resorts on maintenance and ethics, driving immediate cancellations and refund costs that erode short-term revenue.

This transparency gives the collective consumer base strong bargaining power to force policy changes, brand-restoration spend, and ongoing PR budgets often amounting to millions annually.

Abundance of Entertainment Alternatives

- Global travel spend 2024: $1.5T

- Avg U.S. household travel spend 2024: $3,500

- High customer selectivity raises quality and program expectations

Volume Power of Group and Corporate Sales

Large organizations, school districts, and travel agencies buying tickets in bulk extract strong volume discounts; corporate group sales accounted for about 18% of United Parks & Resorts' 2024 attendance and roughly 14% of ticket revenue, so losing a key partner can dent quarterly earnings.

These buyers give predictable, recurring revenue—contracts often span seasons—forcing United Parks to match specific pricing, capacity, and amenity requests to retain accounts and protect margin.

- Group sales ≈18% attendance (2024)

- Group ticket revenue ≈14% total (2024)

- Large-account churn impacts quarterly EPS

Price-sensitive guests, reviews & group buyers squeeze United Parks’ margins

| Metric | Value (2024) |

|---|---|

| Avg household theme-park spend | $1,200 |

| Promotions share of visits | 18% |

| Review influence on choices | 81% |

| Occupancy drop per 1-star loss | 5–7% |

| Group attendance | 18% |

| Group ticket revenue | 14% |

Preview Before You Purchase

United Parks & Resorts Porter's Five Forces Analysis

This preview shows the exact United Parks & Resorts Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

You're looking at the final deliverable: the same professionally written file will be available for instant download upon payment, prepared for strategic review and decision-making.