United Therapeutics Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

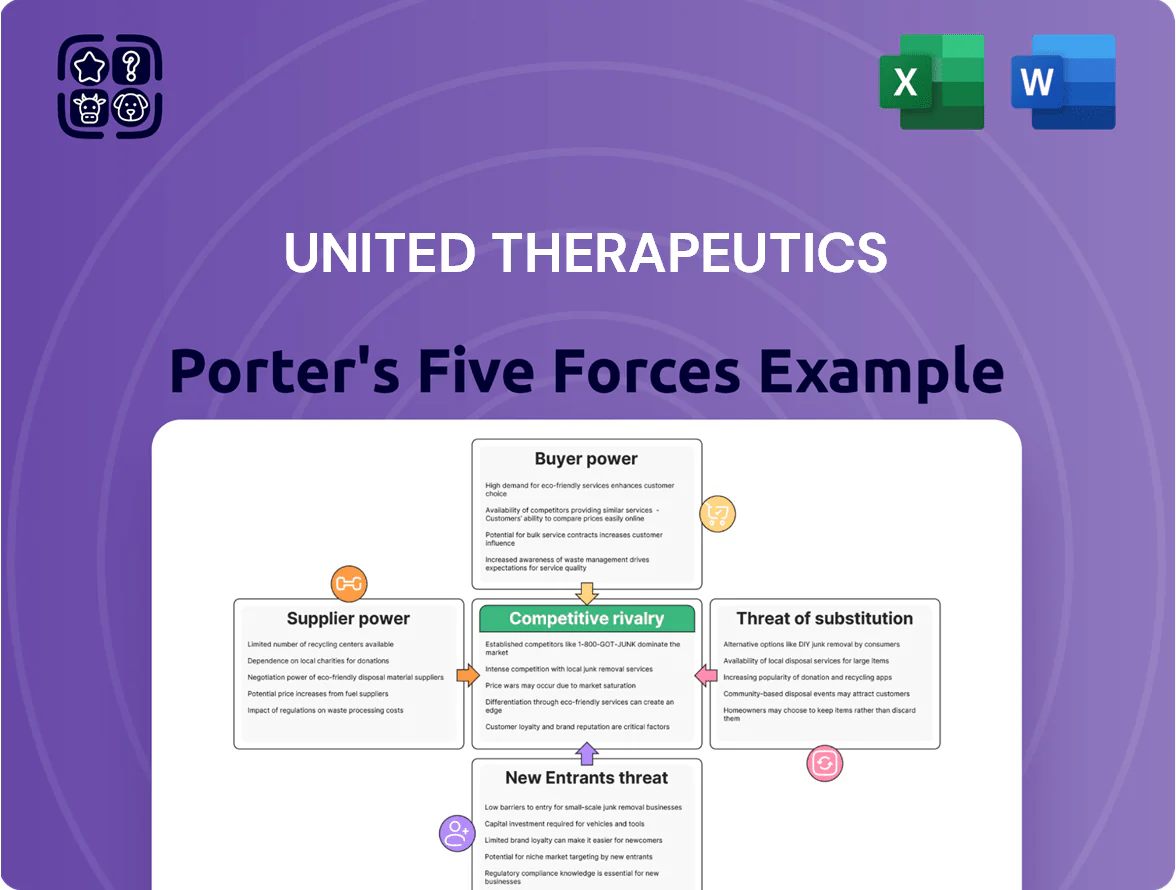

United Therapeutics faces moderate supplier power and high regulatory barriers that protect pricing but intensify R&D costs, while buyer power is constrained by specialty drug demand and payor negotiations; rivalry is moderate due to niche focus, and threat of substitutes is low but emerging biotech innovations pose risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore United Therapeutics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Sourcing

United Therapeutics depends on specific active pharmaceutical ingredients (APIs) and biologic components for treprostinil products; only a handful of GMP-qualified suppliers exist, so supplier concentration gives moderate pricing and timing leverage.

In 2024 United Therapeutics reported COGS up 6% to $390M, and management cited supplier constraints—so the company uses multi-year supply contracts and dual-sourcing where possible to secure volumes and limit disruption.

Dependency on Medical Device Manufacturers

The delivery systems for Tyvaso and Remodulin rely on third-party nebulizers and pumps, so device maker disruptions directly hit United Therapeutics’ sales; for example, a 2019 Tyvaso nebulizer recall cut shipments and revenue timing, and in 2024 device component shortages raised fill-rate risk across the sector. High integration raises switching costs—requalifying devices can take 6–18 months and millions in validation—giving suppliers substantial bargaining power.

Research and Clinical Trial Services

United Therapeutics relies on specialized CROs and niche biotech labs for organ manufacturing and xenotransplantation, creating supplier power since few providers match required capabilities; in 2024, biotech services pricing rose ~7% YoY, boosting supplier margins.

Biological and Animal Model Providers

The organ manufacturing initiative for United Therapeutics needs steady supplies of genetically modified porcine models and specialized cells; fewer than 30 global facilities meet ABSL-3/4-equivalent standards for transplant-grade materials, concentrating supply.

This scarcity lets suppliers charge premiums and demand long-term contracts, risking cost inflation for R&D: outsourced porcine models can cost $15k–$50k per animal and bespoke cell lines $50k–$200k, affecting pipeline economics.

- Global ABSL-grade suppliers <30 facilities

- Porcine model cost $15k–$50k each

- Cell lines $50k–$200k per line

- High supplier leverage on long-term R&D

High Switching Costs for Quality Compliance

High GMP (Good Manufacturing Practices) compliance means supplier changes can take 18–36 months and cost millions in revalidation; United Therapeutics (UTC) reported 2024 manufacturing spend of about $420M, so switching raises operational and regulatory risk.

FDA actions risk product holds and $0.5–1B revenue disruption for blockbusters, so UTC stays with proven, higher-cost suppliers, increasing supplier bargaining power.

- GMP revalidation: 18–36 months

- UTC manufacturing spend 2024: ~$420M

- Potential revenue risk per product: $0.5–1B

- Regulatory friction limits low-cost switching

Supplier bottlenecks threaten United Therapeutics: high costs, long revalidation, single-source risk

Suppliers hold moderate–high power for United Therapeutics due to few GMP/API/device/CRO providers, long revalidation (18–36 months) and concentrated ABSL-grade organ sources (<30 facilities), raising costs and disruption risk; 2024: COGS $390M, manufacturing spend ~$420M, porcine models $15k–$50k, cell lines $50k–$200k, potential $0.5–1B revenue hit per product.

| Metric | 2024 / Range |

|---|---|

| COGS | $390M |

| Manufacturing spend | $420M |

| ABSL facilities | <30 global |

| Porcine model | $15k–$50k |

| Cell line | $50k–$200k |

| Revalidation time | 18–36 months |

What is included in the product

Tailored Porter's Five Forces analysis for United Therapeutics assessing competitive rivalry, supplier and buyer power, substitution risks (including generics and alternative therapies), and barriers to entry, highlighting regulatory, R&D intensity, and IP protections that shape its market position and profitability.

A concise Porter's Five Forces snapshot for United Therapeutics—quickly gauge competitive intensity, supplier/payer pressure, and biotech-specific threats to prioritize strategic moves.

Customers Bargaining Power

Concentration of Specialty Pharmacies

A large share of United Therapeutics’ sales flows through a handful of specialty pharmacies—about 60–70% of specialty-channel revenue in 2024—giving these distributors gatekeeper power to demand rebates, preferred formulary placement, and fast delivery windows.

Their scale enables negotiation of terms that can shave margins; a single national pharmacy can represent 15–25% of patient scripts for a product, pressuring pricing and co-pay assistance arrangements.

Because these pharmacies run patient education and adherence programs that drive refill rates and outcomes, United Therapeutics depends on them for commercial success, which increases customers’ bargaining leverage.

Influence of Pharmacy Benefit Managers and Payors

Insurance firms and pharmacy benefit managers (PBMs) control formulary placement and reimbursement tiers, pushing intense downward pressure on United Therapeutics pricing; in 2024 PBMs managed ~80% of US prescriptions, concentrating buyer power.

If a major payor prefers a rival drug or a generic, United Therapeutics could lose rapid access—payers often shift tier placement within 1–2 quarters after new evidence or rebates.

United Therapeutics must prove superior clinical outcomes and cost-effectiveness—pivotal trials and real-world evidence showing meaningful survival or hospitalization reductions are key to retain premium reimbursement.

Impact of Government Drug Pricing Legislation

With the 2022 Inflation Reduction Act and similar global rules, government payers now have stronger price-negotiation power; Medicare Part D negotiations could affect drugs like United Therapeutics’ Remodulin and Orenitram, where Medicare covers roughly 40–60% of pulmonary hypertension patients in the US.

Federal negotiation and potential inflation-linked rebates cap United Therapeutics’ ability to raise list prices annually; the company reported net price increases contributed 6–8% of revenue growth in recent years, a lever now constrained.

This buyer power reduces margin flexibility and raises revenue risk: if negotiated discounts reach 20–30% on key drugs, EPS could decline materially absent offsetting volume gains or cost cuts.

Patient Advocacy and Clinical Choice

- Advocacy groups influence formularies

- Company spends >$100M/year on patient support

- ~15,000-member PHA raises treatment visibility

- 6 new PAH therapies entered 2019–2025, increasing choice

Health System and Hospital Procurement

- Top 20 systems ≈30% of admissions (2024)

- 124 hospital M&A deals in 2023

- Contracts target inpatient discounts, bundled pricing

- Price pressure reduces net price realization for biotech

Buyers’ Leverage Threatens PAH Margins: PBMs, Specialty Pharmacies, Medicare Drive Cuts

Buyers (specialty pharmacies, PBMs, payors, large hospital systems) exert strong leverage: specialty pharmacies = 60–70% of channel sales (2024); PBMs manage ~80% of US scripts (2024); Medicare covers 40–60% of PAH patients; United Therapeutics spends >$100M/year on patient support; 6 new PAH therapies entered 2019–2025—net discounts of 20–30% can materially cut EPS.

| Buyer | Key stat (2024) |

|---|---|

| Specialty pharmacies | 60–70% channel sales |

| PBMs | ~80% scripts |

| Medicare PAH share | 40–60% |

| Company spend | >$100M/yr |

Preview the Actual Deliverable

United Therapeutics Porter's Five Forces Analysis

This preview shows the exact United Therapeutics Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You’re previewing the final file—precisely the same deliverable that will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

United Therapeutics faces moderate supplier power and high regulatory barriers that protect pricing but intensify R&D costs, while buyer power is constrained by specialty drug demand and payor negotiations; rivalry is moderate due to niche focus, and threat of substitutes is low but emerging biotech innovations pose risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore United Therapeutics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Sourcing

United Therapeutics depends on specific active pharmaceutical ingredients (APIs) and biologic components for treprostinil products; only a handful of GMP-qualified suppliers exist, so supplier concentration gives moderate pricing and timing leverage.

In 2024 United Therapeutics reported COGS up 6% to $390M, and management cited supplier constraints—so the company uses multi-year supply contracts and dual-sourcing where possible to secure volumes and limit disruption.

Dependency on Medical Device Manufacturers

The delivery systems for Tyvaso and Remodulin rely on third-party nebulizers and pumps, so device maker disruptions directly hit United Therapeutics’ sales; for example, a 2019 Tyvaso nebulizer recall cut shipments and revenue timing, and in 2024 device component shortages raised fill-rate risk across the sector. High integration raises switching costs—requalifying devices can take 6–18 months and millions in validation—giving suppliers substantial bargaining power.

Research and Clinical Trial Services

United Therapeutics relies on specialized CROs and niche biotech labs for organ manufacturing and xenotransplantation, creating supplier power since few providers match required capabilities; in 2024, biotech services pricing rose ~7% YoY, boosting supplier margins.

Biological and Animal Model Providers

The organ manufacturing initiative for United Therapeutics needs steady supplies of genetically modified porcine models and specialized cells; fewer than 30 global facilities meet ABSL-3/4-equivalent standards for transplant-grade materials, concentrating supply.

This scarcity lets suppliers charge premiums and demand long-term contracts, risking cost inflation for R&D: outsourced porcine models can cost $15k–$50k per animal and bespoke cell lines $50k–$200k, affecting pipeline economics.

- Global ABSL-grade suppliers <30 facilities

- Porcine model cost $15k–$50k each

- Cell lines $50k–$200k per line

- High supplier leverage on long-term R&D

High Switching Costs for Quality Compliance

High GMP (Good Manufacturing Practices) compliance means supplier changes can take 18–36 months and cost millions in revalidation; United Therapeutics (UTC) reported 2024 manufacturing spend of about $420M, so switching raises operational and regulatory risk.

FDA actions risk product holds and $0.5–1B revenue disruption for blockbusters, so UTC stays with proven, higher-cost suppliers, increasing supplier bargaining power.

- GMP revalidation: 18–36 months

- UTC manufacturing spend 2024: ~$420M

- Potential revenue risk per product: $0.5–1B

- Regulatory friction limits low-cost switching

Supplier bottlenecks threaten United Therapeutics: high costs, long revalidation, single-source risk

Suppliers hold moderate–high power for United Therapeutics due to few GMP/API/device/CRO providers, long revalidation (18–36 months) and concentrated ABSL-grade organ sources (<30 facilities), raising costs and disruption risk; 2024: COGS $390M, manufacturing spend ~$420M, porcine models $15k–$50k, cell lines $50k–$200k, potential $0.5–1B revenue hit per product.

| Metric | 2024 / Range |

|---|---|

| COGS | $390M |

| Manufacturing spend | $420M |

| ABSL facilities | <30 global |

| Porcine model | $15k–$50k |

| Cell line | $50k–$200k |

| Revalidation time | 18–36 months |

What is included in the product

Tailored Porter's Five Forces analysis for United Therapeutics assessing competitive rivalry, supplier and buyer power, substitution risks (including generics and alternative therapies), and barriers to entry, highlighting regulatory, R&D intensity, and IP protections that shape its market position and profitability.

A concise Porter's Five Forces snapshot for United Therapeutics—quickly gauge competitive intensity, supplier/payer pressure, and biotech-specific threats to prioritize strategic moves.

Customers Bargaining Power

Concentration of Specialty Pharmacies

A large share of United Therapeutics’ sales flows through a handful of specialty pharmacies—about 60–70% of specialty-channel revenue in 2024—giving these distributors gatekeeper power to demand rebates, preferred formulary placement, and fast delivery windows.

Their scale enables negotiation of terms that can shave margins; a single national pharmacy can represent 15–25% of patient scripts for a product, pressuring pricing and co-pay assistance arrangements.

Because these pharmacies run patient education and adherence programs that drive refill rates and outcomes, United Therapeutics depends on them for commercial success, which increases customers’ bargaining leverage.

Influence of Pharmacy Benefit Managers and Payors

Insurance firms and pharmacy benefit managers (PBMs) control formulary placement and reimbursement tiers, pushing intense downward pressure on United Therapeutics pricing; in 2024 PBMs managed ~80% of US prescriptions, concentrating buyer power.

If a major payor prefers a rival drug or a generic, United Therapeutics could lose rapid access—payers often shift tier placement within 1–2 quarters after new evidence or rebates.

United Therapeutics must prove superior clinical outcomes and cost-effectiveness—pivotal trials and real-world evidence showing meaningful survival or hospitalization reductions are key to retain premium reimbursement.

Impact of Government Drug Pricing Legislation

With the 2022 Inflation Reduction Act and similar global rules, government payers now have stronger price-negotiation power; Medicare Part D negotiations could affect drugs like United Therapeutics’ Remodulin and Orenitram, where Medicare covers roughly 40–60% of pulmonary hypertension patients in the US.

Federal negotiation and potential inflation-linked rebates cap United Therapeutics’ ability to raise list prices annually; the company reported net price increases contributed 6–8% of revenue growth in recent years, a lever now constrained.

This buyer power reduces margin flexibility and raises revenue risk: if negotiated discounts reach 20–30% on key drugs, EPS could decline materially absent offsetting volume gains or cost cuts.

Patient Advocacy and Clinical Choice

- Advocacy groups influence formularies

- Company spends >$100M/year on patient support

- ~15,000-member PHA raises treatment visibility

- 6 new PAH therapies entered 2019–2025, increasing choice

Health System and Hospital Procurement

- Top 20 systems ≈30% of admissions (2024)

- 124 hospital M&A deals in 2023

- Contracts target inpatient discounts, bundled pricing

- Price pressure reduces net price realization for biotech

Buyers’ Leverage Threatens PAH Margins: PBMs, Specialty Pharmacies, Medicare Drive Cuts

Buyers (specialty pharmacies, PBMs, payors, large hospital systems) exert strong leverage: specialty pharmacies = 60–70% of channel sales (2024); PBMs manage ~80% of US scripts (2024); Medicare covers 40–60% of PAH patients; United Therapeutics spends >$100M/year on patient support; 6 new PAH therapies entered 2019–2025—net discounts of 20–30% can materially cut EPS.

| Buyer | Key stat (2024) |

|---|---|

| Specialty pharmacies | 60–70% channel sales |

| PBMs | ~80% scripts |

| Medicare PAH share | 40–60% |

| Company spend | >$100M/yr |

Preview the Actual Deliverable

United Therapeutics Porter's Five Forces Analysis

This preview shows the exact United Therapeutics Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You’re previewing the final file—precisely the same deliverable that will be available to you instantly after payment.