Uniti Group Boston Consulting Group Matrix

Download Your Competitive Advantage

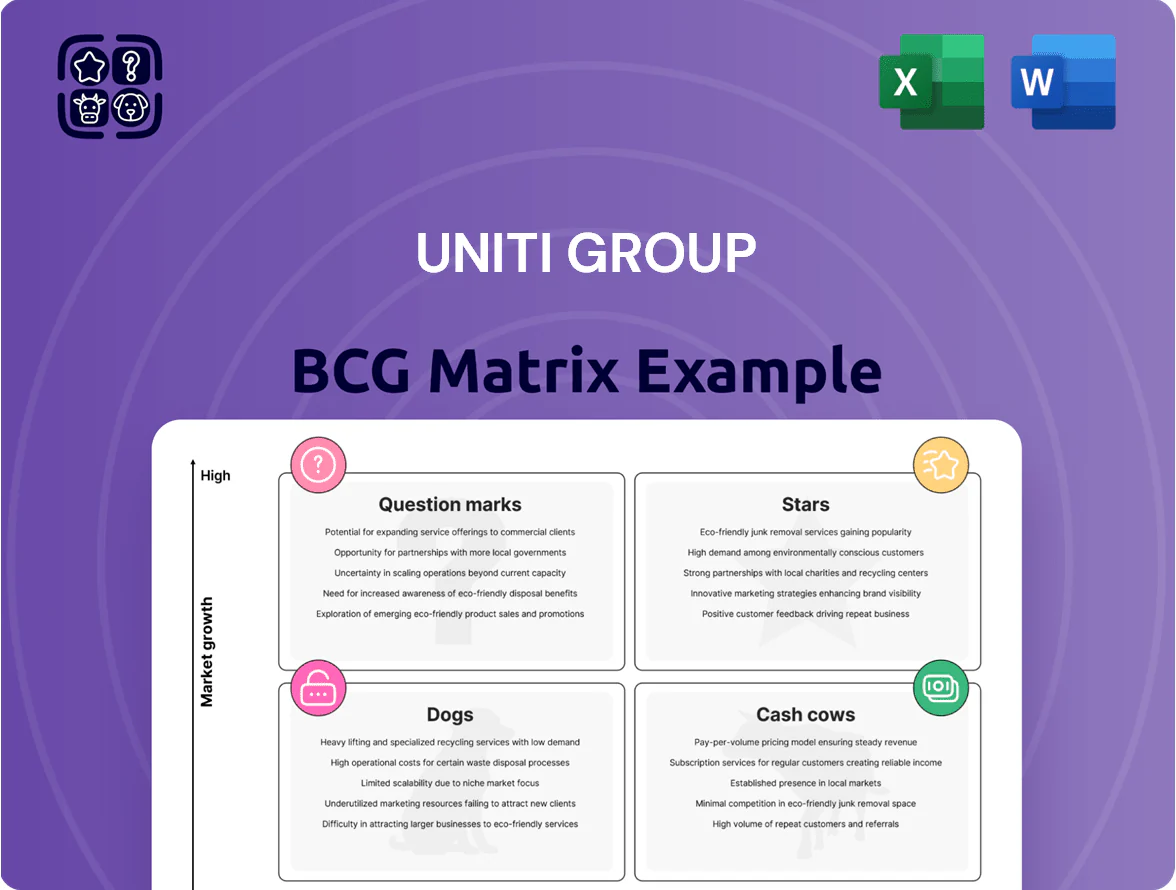

Uniti Group’s preliminary BCG Matrix snapshot highlights its fiber and fixed-wireless assets as potential Stars in growing markets while legacy copper and lower-margin services trend toward Cash Cows or Dogs; strategic capex allocation and divestment choices will determine whether question-mark initiatives become market leaders. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Fiber-to-the-Home FTTH Expansion

Following its 2025 merger, Uniti Group has become a leading FTTH provider in Tier II/III U.S. markets, serving ~1.2 million passings and claiming ~45–60% share in key clusters like the Southeast and Midwest as of Dec 31, 2025.

High entry barriers—right-of-way control and last-mile build costs averaging $1,200–$1,800 per passing—protect margins, while average ARPU for residential gigabit customers rose to ~$75/month in 2025.

Capital intensive: Uniti planned $750M–$850M in FTTH capex for 2026 to fuel rollouts; these fiber assets are the primary growth engines as Uniti shifts toward bundled services and higher lifetime customer value.

Hyperscale Data Center Connectivity

Hyperscale Data Center Connectivity is a Star: Uniti’s 2025 high-capacity fiber routes sit at the core of AI and cloud growth, with global hyperscale data center traffic up ~45% y/y in 2024–25 and wholesale transport demand rising ~30% in key US markets.

Uniti captures a large share of wholesale transport revenue—2024 fiber services revenue grew ~22% y/y—driven by dense metro routes linking hyperscalers.

Maintaining the lead requires ongoing capital spend: Uniti’s 2024–25 network capex run-rate rose to ~$220–240M annually to boost route density.

Compared with legacy telco segments, hyperscale connectivity offers superior growth and margin upside, supporting Star status in the BCG matrix.

5G Small Cell Backhaul

As carriers densify 5G, Uniti Group’s ~200,000 fiber route miles (2025 company filing) supply critical small-cell backhaul/fronthaul, linking cell sites to core networks.

Uniti holds dominant market shares in several metros—Atlanta, Dallas, Phoenix—acting as a primary partner to AT&T, Verizon, and T-Mobile under multi-year contracts.

CapEx-heavy deployments drove $720M capex in 2024, but long-term contracts (average 7–12 years) generate stable recurring revenue and support future cash flow stability.

Integrated Enterprise Fiber Solutions

Integrated Enterprise Fiber Solutions is a Star in Uniti Group’s BCG matrix: Uniti’s fiber assets plus its service arms deliver end-to-end connectivity to large corporations, driving strong revenue growth—Q3 2025 fiber service revenue rose 18% year-over-year to $112 million, per Uniti filings.

Owning fiber gives Uniti price and reliability advantages over non-asset competitors, supporting higher gross margins (adjusted gross margin ~62% in 2025) and lower churn as customers seek resilient networks.

Market share is expanding fast: enterprise fiber demand grew ~22% CAGR 2022–2025, and Uniti reported net new contract wins totaling 1,350 route miles and $48 million ARR in 2025 YTD.

- End-to-end offering: fiber + managed services

- Asset advantage: owned fiber → pricing, reliability

- Financials: Q3 2025 fiber revenue $112M; adj gross margin ~62%

- Growth: 22% market CAGR; $48M ARR new wins 2025 YTD

Tier II and III Metro Fiber Rings

Uniti holds near-monopoly or duopoly fiber rings in multiple mid-sized metros—serving hospitals, schools, and local gov—where fiber demand rose ~8–12% CAGR 2019–2024, letting Uniti add high-margin enterprise connections and boost EBITDA per route mile (example: ~$6.2k EBITDA/route mile in 2024 in select Tier II markets).

Company prioritizes these rings to block entrants, reinvesting capex (~$80–120k per ring buildout) and leveraging low incremental cost to convert municipal and healthcare demand into recurring revenue with gross margins often >60%.

- Near-monopoly in several Tier II/III metros

- Fiber demand up ~8–12% CAGR (2019–2024)

- EBITDA ≈ $6.2k/route mile in select markets (2024)

- Capex to expand rings ~$80–120k each

- Target gross margins >60%

Uniti: FTTH & Hyperscale Fiber Drive $112M Q3 Revenue, 62% Margin, 1.2M Passings

Uniti’s FTTH and hyperscale/enterprise fiber are Stars: ~1.2M passings and ~200k route miles (Dec 31, 2025), Q3 2025 fiber rev $112M, adj gross margin ~62%, 2026 FTTH capex $750–850M, 2024 capex $720M, hyperscale transport demand +30% (2024–25).

| Metric | Value |

|---|---|

| Passings | ~1.2M |

| Route miles | ~200k |

| Q3 2025 fiber rev | $112M |

| Adj gross margin | ~62% |

What is included in the product

Comprehensive BCG Matrix overview for Uniti Group: quadrant placement, strategic moves (invest/hold/divest), competitive risks, and trend context.

One-page Uniti Group BCG Matrix mapping assets by growth and share for rapid strategic decisions.

Cash Cows

Restructured Master Lease Agreements

The restructured master lease agreements with primary tenants deliver predictable cash flow—Uniti reported $1.25 billion in lease revenues in 2024, which underpins its dividend (annualized $0.60 per share in 2024) and debt service (net leverage ~4.2x at YE 2024).

These fiber assets sit in a mature phase, needing minimal capex (maintenance capex ~5% of revenues in 2024), so margins stay high and free cash flow remains strong.

As market leader in leased fiber infrastructure, Uniti uses these steady returns to fund higher-growth plays like tower acquisitions and fiber expansions, allocating roughly 30% of FCF to growth in 2024.

Long-Haul Dark Fiber Routes

Uniti Group’s long-haul dark fiber routes lease to carriers and enterprises generate steady, high-margin cash: in 2025 Uniti reported ~6,200 route-miles of long-haul fiber contributing roughly $140M of annual recurring revenue and >60% gross margins, per its 2025 Form 10-K segments—a mature market with few new entrants because cross-country builds exceed $1M+ per mile, so these routes are classic cash cows requiring minimal ops oversight.

Wireless Tower Ground Leases

Uniti Group’s wireless tower ground leases form a cash-cow: roughly 15,000 leased sites yielding steady, low-maintenance rent with >95% tenant retention and NAREIT-like predictability; in 2024 tower ground rents contributed about $120M recurring revenue with CPI-linked escalators averaging 2–3% yearly.

New tower additions slowed in U.S. metros, so capex needs are low and management runs this segment passively, freeing ~ $100–150M annual capital to push into higher-growth fiber builds where Uniti cited ~20% incremental IRR targets in 2024.

Government and E-Rate Contracts

Uniti’s long-term government and E-Rate contracts with US school districts and agencies generated roughly $120 million in annual recurring revenue in 2024, covering ~18% of regional public-sector demand and showing renewal rates above 90%—providing recession-resistant cash flow.

These contracts are low-growth but require minimal marketing spend, boosting EBITDA margin stability; E-Rate reimbursements (up to 90% of eligible costs) further lower churn and pricing pressure.

- ~$120M ARR (2024)

- ~18% share of regional public-sector market

- >90% contract renewal rate

- E-Rate covers up to 90% of eligible costs

- Low growth, high reliability, low selling expense

Wholesale Carrier Transport Services

Wholesale carrier transport services at Uniti Group (NASDAQ: UNIT) are a cash cow: a mature segment with ~17,000 lit fiber route miles and 2025 wholesale revenues ~ $420 million, giving high gross margins because new tenants use existing infrastructure.

Low incremental cost per handoff and >60% cash conversion means proceeds help cover Uniti’s 2025 net debt (~$1.8 billion) and fund fiber upgrades and OCTEON next-gen optical spending.

- High-margin, mature market

- ~$420M wholesale revenue (2025)

- >60% cash conversion

- Supports servicing ~$1.8B net debt

Uniti: $1.25B lease revenues, $0.60 div, 4.2x leverage — steady cash & 30% FCF to growth

Uniti’s mature fiber, tower leases, wholesale and E-Rate contracts produced predictable cash: 2024 lease revenues $1.25B, dividend $0.60/sh, net leverage ~4.2x; 2024 maintenance capex ~5% of revenues; 2025 wholesale revenue ~$420M; long‑haul ARRs ~$140M; towers ~$120M; FCF allocation ~30% to growth.

| Metric | Value |

|---|---|

| Lease revenues (2024) | $1.25B |

| Dividend (2024) | $0.60/sh |

| Net leverage (YE 2024) | ~4.2x |

| Maintenance capex (2024) | ~5% revs |

| Wholesale rev (2025) | $420M |

| Long‑haul ARR (2025) | $140M |

| Tower rents (2024) | $120M |

| FCF to growth (2024) | ~30% |

What You’re Viewing Is Included

Uniti Group BCG Matrix

The file you're previewing is the exact Uniti Group BCG Matrix report you'll receive after purchase—no watermarks, no demo elements, just a fully formatted, analysis-ready document crafted for strategic clarity and professional use. This preview matches the downloadable file delivered to your inbox, ready for editing, printing, or presenting to stakeholders without additional revisions. Purchase grants immediate access to the complete, market-informed BCG Matrix for your planning and decision-making needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Uniti Group’s preliminary BCG Matrix snapshot highlights its fiber and fixed-wireless assets as potential Stars in growing markets while legacy copper and lower-margin services trend toward Cash Cows or Dogs; strategic capex allocation and divestment choices will determine whether question-mark initiatives become market leaders. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Fiber-to-the-Home FTTH Expansion

Following its 2025 merger, Uniti Group has become a leading FTTH provider in Tier II/III U.S. markets, serving ~1.2 million passings and claiming ~45–60% share in key clusters like the Southeast and Midwest as of Dec 31, 2025.

High entry barriers—right-of-way control and last-mile build costs averaging $1,200–$1,800 per passing—protect margins, while average ARPU for residential gigabit customers rose to ~$75/month in 2025.

Capital intensive: Uniti planned $750M–$850M in FTTH capex for 2026 to fuel rollouts; these fiber assets are the primary growth engines as Uniti shifts toward bundled services and higher lifetime customer value.

Hyperscale Data Center Connectivity

Hyperscale Data Center Connectivity is a Star: Uniti’s 2025 high-capacity fiber routes sit at the core of AI and cloud growth, with global hyperscale data center traffic up ~45% y/y in 2024–25 and wholesale transport demand rising ~30% in key US markets.

Uniti captures a large share of wholesale transport revenue—2024 fiber services revenue grew ~22% y/y—driven by dense metro routes linking hyperscalers.

Maintaining the lead requires ongoing capital spend: Uniti’s 2024–25 network capex run-rate rose to ~$220–240M annually to boost route density.

Compared with legacy telco segments, hyperscale connectivity offers superior growth and margin upside, supporting Star status in the BCG matrix.

5G Small Cell Backhaul

As carriers densify 5G, Uniti Group’s ~200,000 fiber route miles (2025 company filing) supply critical small-cell backhaul/fronthaul, linking cell sites to core networks.

Uniti holds dominant market shares in several metros—Atlanta, Dallas, Phoenix—acting as a primary partner to AT&T, Verizon, and T-Mobile under multi-year contracts.

CapEx-heavy deployments drove $720M capex in 2024, but long-term contracts (average 7–12 years) generate stable recurring revenue and support future cash flow stability.

Integrated Enterprise Fiber Solutions

Integrated Enterprise Fiber Solutions is a Star in Uniti Group’s BCG matrix: Uniti’s fiber assets plus its service arms deliver end-to-end connectivity to large corporations, driving strong revenue growth—Q3 2025 fiber service revenue rose 18% year-over-year to $112 million, per Uniti filings.

Owning fiber gives Uniti price and reliability advantages over non-asset competitors, supporting higher gross margins (adjusted gross margin ~62% in 2025) and lower churn as customers seek resilient networks.

Market share is expanding fast: enterprise fiber demand grew ~22% CAGR 2022–2025, and Uniti reported net new contract wins totaling 1,350 route miles and $48 million ARR in 2025 YTD.

- End-to-end offering: fiber + managed services

- Asset advantage: owned fiber → pricing, reliability

- Financials: Q3 2025 fiber revenue $112M; adj gross margin ~62%

- Growth: 22% market CAGR; $48M ARR new wins 2025 YTD

Tier II and III Metro Fiber Rings

Uniti holds near-monopoly or duopoly fiber rings in multiple mid-sized metros—serving hospitals, schools, and local gov—where fiber demand rose ~8–12% CAGR 2019–2024, letting Uniti add high-margin enterprise connections and boost EBITDA per route mile (example: ~$6.2k EBITDA/route mile in 2024 in select Tier II markets).

Company prioritizes these rings to block entrants, reinvesting capex (~$80–120k per ring buildout) and leveraging low incremental cost to convert municipal and healthcare demand into recurring revenue with gross margins often >60%.

- Near-monopoly in several Tier II/III metros

- Fiber demand up ~8–12% CAGR (2019–2024)

- EBITDA ≈ $6.2k/route mile in select markets (2024)

- Capex to expand rings ~$80–120k each

- Target gross margins >60%

Uniti: FTTH & Hyperscale Fiber Drive $112M Q3 Revenue, 62% Margin, 1.2M Passings

Uniti’s FTTH and hyperscale/enterprise fiber are Stars: ~1.2M passings and ~200k route miles (Dec 31, 2025), Q3 2025 fiber rev $112M, adj gross margin ~62%, 2026 FTTH capex $750–850M, 2024 capex $720M, hyperscale transport demand +30% (2024–25).

| Metric | Value |

|---|---|

| Passings | ~1.2M |

| Route miles | ~200k |

| Q3 2025 fiber rev | $112M |

| Adj gross margin | ~62% |

What is included in the product

Comprehensive BCG Matrix overview for Uniti Group: quadrant placement, strategic moves (invest/hold/divest), competitive risks, and trend context.

One-page Uniti Group BCG Matrix mapping assets by growth and share for rapid strategic decisions.

Cash Cows

Restructured Master Lease Agreements

The restructured master lease agreements with primary tenants deliver predictable cash flow—Uniti reported $1.25 billion in lease revenues in 2024, which underpins its dividend (annualized $0.60 per share in 2024) and debt service (net leverage ~4.2x at YE 2024).

These fiber assets sit in a mature phase, needing minimal capex (maintenance capex ~5% of revenues in 2024), so margins stay high and free cash flow remains strong.

As market leader in leased fiber infrastructure, Uniti uses these steady returns to fund higher-growth plays like tower acquisitions and fiber expansions, allocating roughly 30% of FCF to growth in 2024.

Long-Haul Dark Fiber Routes

Uniti Group’s long-haul dark fiber routes lease to carriers and enterprises generate steady, high-margin cash: in 2025 Uniti reported ~6,200 route-miles of long-haul fiber contributing roughly $140M of annual recurring revenue and >60% gross margins, per its 2025 Form 10-K segments—a mature market with few new entrants because cross-country builds exceed $1M+ per mile, so these routes are classic cash cows requiring minimal ops oversight.

Wireless Tower Ground Leases

Uniti Group’s wireless tower ground leases form a cash-cow: roughly 15,000 leased sites yielding steady, low-maintenance rent with >95% tenant retention and NAREIT-like predictability; in 2024 tower ground rents contributed about $120M recurring revenue with CPI-linked escalators averaging 2–3% yearly.

New tower additions slowed in U.S. metros, so capex needs are low and management runs this segment passively, freeing ~ $100–150M annual capital to push into higher-growth fiber builds where Uniti cited ~20% incremental IRR targets in 2024.

Government and E-Rate Contracts

Uniti’s long-term government and E-Rate contracts with US school districts and agencies generated roughly $120 million in annual recurring revenue in 2024, covering ~18% of regional public-sector demand and showing renewal rates above 90%—providing recession-resistant cash flow.

These contracts are low-growth but require minimal marketing spend, boosting EBITDA margin stability; E-Rate reimbursements (up to 90% of eligible costs) further lower churn and pricing pressure.

- ~$120M ARR (2024)

- ~18% share of regional public-sector market

- >90% contract renewal rate

- E-Rate covers up to 90% of eligible costs

- Low growth, high reliability, low selling expense

Wholesale Carrier Transport Services

Wholesale carrier transport services at Uniti Group (NASDAQ: UNIT) are a cash cow: a mature segment with ~17,000 lit fiber route miles and 2025 wholesale revenues ~ $420 million, giving high gross margins because new tenants use existing infrastructure.

Low incremental cost per handoff and >60% cash conversion means proceeds help cover Uniti’s 2025 net debt (~$1.8 billion) and fund fiber upgrades and OCTEON next-gen optical spending.

- High-margin, mature market

- ~$420M wholesale revenue (2025)

- >60% cash conversion

- Supports servicing ~$1.8B net debt

Uniti: $1.25B lease revenues, $0.60 div, 4.2x leverage — steady cash & 30% FCF to growth

Uniti’s mature fiber, tower leases, wholesale and E-Rate contracts produced predictable cash: 2024 lease revenues $1.25B, dividend $0.60/sh, net leverage ~4.2x; 2024 maintenance capex ~5% of revenues; 2025 wholesale revenue ~$420M; long‑haul ARRs ~$140M; towers ~$120M; FCF allocation ~30% to growth.

| Metric | Value |

|---|---|

| Lease revenues (2024) | $1.25B |

| Dividend (2024) | $0.60/sh |

| Net leverage (YE 2024) | ~4.2x |

| Maintenance capex (2024) | ~5% revs |

| Wholesale rev (2025) | $420M |

| Long‑haul ARR (2025) | $140M |

| Tower rents (2024) | $120M |

| FCF to growth (2024) | ~30% |

What You’re Viewing Is Included

Uniti Group BCG Matrix

The file you're previewing is the exact Uniti Group BCG Matrix report you'll receive after purchase—no watermarks, no demo elements, just a fully formatted, analysis-ready document crafted for strategic clarity and professional use. This preview matches the downloadable file delivered to your inbox, ready for editing, printing, or presenting to stakeholders without additional revisions. Purchase grants immediate access to the complete, market-informed BCG Matrix for your planning and decision-making needs.