Unitil Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

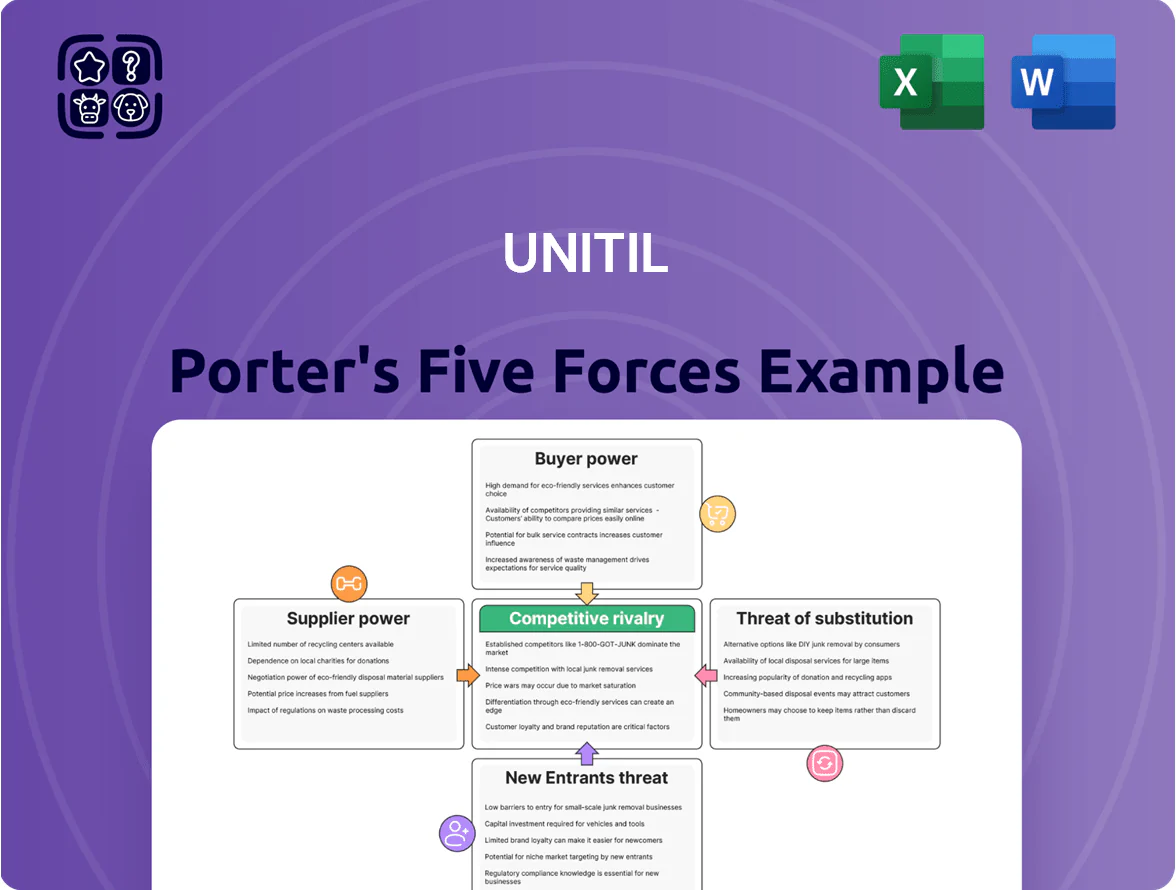

Unitil faces moderate buyer power and regulatory-driven entry barriers, while supplier influence and substitutes pose manageable risks given its regional utility scale and integrated services.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Unitil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Wholesale Energy Market Volatility

Unitil relies on wholesale New England markets for most electricity and gas; lacking material generation assets makes it exposed to spot-price swings—New England wholesale electric prices averaged about $80/MWh in 2024 vs $45/MWh in 2020, raising procurement risk.

Large regional suppliers hold bargaining power via tight capacity and fuel mix constraints, but state and FERC rules let Unitil pass fuel-cost variances to customers through trackers; regulated pass-through reduced margin squeeze in 2024.

Pipeline and Transmission Constraints

The delivery of natural gas and electricity relies on a few interstate pipelines and high-voltage transmission owners; in New England, pipeline capacity hits peak constraints—Algonquin and Tennessee pipelines saw utilization >95% in winter 2023–24—giving midstream suppliers pricing leverage during cold snaps. Unitil holds long-term firm transport and capacity contracts, limiting price negotiation; Unitil’s 2024 filing shows supply capacity cover at ~90% for peak months, raising cost and reliability exposure.

Specialized Infrastructure Equipment

Supplier power is high: three global firms (Siemens Energy, Schneider Electric, and ABB) account for roughly 60% of utility-grade transformers and meters, giving them pricing leverage over Unitil, which spent $48m on capex in 2024 for grid upgrades.

COVID-19 and 2021–2023 supply shocks pushed lead times for transformers to 12–20 months and raised prices ~18% by 2022–2024, reinforcing manufacturers' leverage as Unitil seeks modernization.

Unitil’s adherence to ANSI and IEEE technical standards creates high switching costs; requalifying new vendors can exceed $2m per asset class and delay projects 9–15 months, limiting Unitil’s procurement flexibility.

Skilled Labor and Union Contracts

- ~40–50% unionized field staff (2025)

- Wage premium up 8–12% (2024–25)

- Unitil sought 3.5%–5% labor cost recovery (2024 rate filings)

Regulatory and Environmental Mandates

Suppliers of environmental compliance services and carbon credits gain leverage as Massachusetts targets a 2045 net-zero economy and Maine requires 80% renewable electricity by 2030; Unitil faces higher costs to meet these rules.

Unitil must contract specialized vendors for renewable portfolio standards and emissions reductions, driving dependence on certified providers.

The small pool of certified green-energy suppliers lets them charge premiums; New England REC prices averaged about $18/MWh in 2024, squeezing margins.

- State mandates: MA net-zero 2045, ME 80% renewables by 2030

- REC price reference: ~$18/MWh (2024 New England average)

- Limited certified suppliers → premium pricing, higher compliance cost

High supplier power: surging wholesale prices, tight pipelines, vendor concentration

Supplier power is high: wholesale power/gas price volatility (NE avg $80/MWh in 2024 vs $45/MWh in 2020) and >95% pipeline winter utilization (2023–24) raise procurement risk, but regulatory pass-throughs limited margin squeeze; critical equipment vendors control ~60% market (transformer/meter suppliers) and long lead times (12–20 months) plus 40–50% unionized field staff push costs up.

| Metric | 2024–25 |

|---|---|

| NE wholesale power | $80/MWh |

| Pipeline winter util. | >95% |

| Transformer/meter market | ~60% vendors |

| Lead times | 12–20 months |

| Unionized field staff | 40–50% |

What is included in the product

Tailored Porter's Five Forces analysis for Unitil that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes, and emerging threats—supported by strategic commentary to inform investor materials, internal strategy, or academic projects.

Compact, one-sheet Unitil Porter’s Five Forces summary—quickly spot competitive pressures and make faster strategic decisions.

Customers Bargaining Power

Public Utility Commission Oversight

State public utility commissions (PUCs) stand in for customer bargaining power by vetting Unitil’s rate cases; in 2024 Unitil’s allowed ROE (return on equity) approvals averaged ~8.5% across NH, MA, and ME, capping earnings on infrastructure investments.

PUCs require prudency reviews and cost-of-service proof, which limited Unitil’s 2024 regulated gross margin growth to about 2.1% year-over-year, protecting captive customers from monopoly pricing.

Retail Energy Choice Options

Customers in Unitil’s service territories can choose competitive retail suppliers while still using Unitil’s wires, letting residential and commercial buyers shop commodity prices; as of 2024 about 30–40% of MA and NH small commercial accounts used competitive suppliers, per state reports.

This shopping caps Unitil’s influence over total bills since Unitil primarily earns distribution revenue—distribution made up roughly 45–55% of typical customer bills in 2023—so commodity churn limits margin expansion.

Industrial Load Defection

Large industrial and commercial customers have far higher bargaining power than residential users because they consume disproportionately more energy; Unitil’s top 10 industrial accounts can represent over 25% of a utility’s commercial revenue, so losing one matters. These customers can threaten load defection—relocating facilities or investing in on-site generation and storage—to avoid high rates; in 2024, US industrial solar plus storage projects grew 18% year-over-year, lowering switching costs. To retain them, Unitil routinely offers bespoke economic development rates, demand-response payments, and efficiency incentives that can cut effective rates by 5–15%.

Energy Efficiency and Demand Response

Customers using smart thermostats, rooftop solar, and LEDs cut Unitil’s volumetric sales; in 2024 US residential solar capacity grew ~25% year-over-year to 35 GW, and DOE reports demand response reduced peak load by 5–7% in some regions, directly lowering utility margins.

Conservation gives customers timing power via demand response programs; Unitil faces revenue risk as pay-per-kWh declines and fixed-cost recovery pressures rise, pressuring rate cases and ROE outcomes.

- 2024 US residential solar +25% (to ~35 GW)

- Demand response peak reduction 5–7%

- Volumetric sales decline → higher fixed-cost per kWh

Community Choice Aggregation

Municipalities in Unitil’s service area can form community choice aggregation (CCA) pools to buy power for residents, concentrating bargaining power across thousands of accounts and often securing rates 5–10% below default service or higher renewable mixes; Massachusetts and New Hampshire CCAs captured ~12% of eligible load in 2024, pressuring utilities to match offers.

Regulation, competition & DERs cap Unitil’s margins and pricing power

PUCs cap Unitil’s pricing power (2024 allowed ROE ~8.5%), limiting distribution-margin growth (~2.1% y/y in 2024). Competitive retail suppliers and CCAs (≈12% load in MA/NH, 2024) and commodity shopping (30–40% small commercial choice) constrain bill markup. Large industrial customers (>25% commercial rev concentrated) and DERs (US residential solar +25% to ~35 GW, 2024) raise switching risk and lower volumetric sales.

| Metric | 2024 |

|---|---|

| Allowed ROE | ~8.5% |

| Regulated gross margin growth | ~2.1% y/y |

| CCA load (MA/NH) | ~12% |

| Small commercial on competitive suppliers | 30–40% |

| US residential solar capacity | ~35 GW (+25%) |

Full Version Awaits

Unitil Porter's Five Forces Analysis

This preview shows the exact Unitil Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

You're looking at the actual, fully formatted document; once you complete your purchase, you’ll get instant access to this same file ready for download and use.

No mockups or samples—the deliverable shown is the complete, professional analysis you’ll be able to download after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Unitil faces moderate buyer power and regulatory-driven entry barriers, while supplier influence and substitutes pose manageable risks given its regional utility scale and integrated services.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Unitil’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Wholesale Energy Market Volatility

Unitil relies on wholesale New England markets for most electricity and gas; lacking material generation assets makes it exposed to spot-price swings—New England wholesale electric prices averaged about $80/MWh in 2024 vs $45/MWh in 2020, raising procurement risk.

Large regional suppliers hold bargaining power via tight capacity and fuel mix constraints, but state and FERC rules let Unitil pass fuel-cost variances to customers through trackers; regulated pass-through reduced margin squeeze in 2024.

Pipeline and Transmission Constraints

The delivery of natural gas and electricity relies on a few interstate pipelines and high-voltage transmission owners; in New England, pipeline capacity hits peak constraints—Algonquin and Tennessee pipelines saw utilization >95% in winter 2023–24—giving midstream suppliers pricing leverage during cold snaps. Unitil holds long-term firm transport and capacity contracts, limiting price negotiation; Unitil’s 2024 filing shows supply capacity cover at ~90% for peak months, raising cost and reliability exposure.

Specialized Infrastructure Equipment

Supplier power is high: three global firms (Siemens Energy, Schneider Electric, and ABB) account for roughly 60% of utility-grade transformers and meters, giving them pricing leverage over Unitil, which spent $48m on capex in 2024 for grid upgrades.

COVID-19 and 2021–2023 supply shocks pushed lead times for transformers to 12–20 months and raised prices ~18% by 2022–2024, reinforcing manufacturers' leverage as Unitil seeks modernization.

Unitil’s adherence to ANSI and IEEE technical standards creates high switching costs; requalifying new vendors can exceed $2m per asset class and delay projects 9–15 months, limiting Unitil’s procurement flexibility.

Skilled Labor and Union Contracts

- ~40–50% unionized field staff (2025)

- Wage premium up 8–12% (2024–25)

- Unitil sought 3.5%–5% labor cost recovery (2024 rate filings)

Regulatory and Environmental Mandates

Suppliers of environmental compliance services and carbon credits gain leverage as Massachusetts targets a 2045 net-zero economy and Maine requires 80% renewable electricity by 2030; Unitil faces higher costs to meet these rules.

Unitil must contract specialized vendors for renewable portfolio standards and emissions reductions, driving dependence on certified providers.

The small pool of certified green-energy suppliers lets them charge premiums; New England REC prices averaged about $18/MWh in 2024, squeezing margins.

- State mandates: MA net-zero 2045, ME 80% renewables by 2030

- REC price reference: ~$18/MWh (2024 New England average)

- Limited certified suppliers → premium pricing, higher compliance cost

High supplier power: surging wholesale prices, tight pipelines, vendor concentration

Supplier power is high: wholesale power/gas price volatility (NE avg $80/MWh in 2024 vs $45/MWh in 2020) and >95% pipeline winter utilization (2023–24) raise procurement risk, but regulatory pass-throughs limited margin squeeze; critical equipment vendors control ~60% market (transformer/meter suppliers) and long lead times (12–20 months) plus 40–50% unionized field staff push costs up.

| Metric | 2024–25 |

|---|---|

| NE wholesale power | $80/MWh |

| Pipeline winter util. | >95% |

| Transformer/meter market | ~60% vendors |

| Lead times | 12–20 months |

| Unionized field staff | 40–50% |

What is included in the product

Tailored Porter's Five Forces analysis for Unitil that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes, and emerging threats—supported by strategic commentary to inform investor materials, internal strategy, or academic projects.

Compact, one-sheet Unitil Porter’s Five Forces summary—quickly spot competitive pressures and make faster strategic decisions.

Customers Bargaining Power

Public Utility Commission Oversight

State public utility commissions (PUCs) stand in for customer bargaining power by vetting Unitil’s rate cases; in 2024 Unitil’s allowed ROE (return on equity) approvals averaged ~8.5% across NH, MA, and ME, capping earnings on infrastructure investments.

PUCs require prudency reviews and cost-of-service proof, which limited Unitil’s 2024 regulated gross margin growth to about 2.1% year-over-year, protecting captive customers from monopoly pricing.

Retail Energy Choice Options

Customers in Unitil’s service territories can choose competitive retail suppliers while still using Unitil’s wires, letting residential and commercial buyers shop commodity prices; as of 2024 about 30–40% of MA and NH small commercial accounts used competitive suppliers, per state reports.

This shopping caps Unitil’s influence over total bills since Unitil primarily earns distribution revenue—distribution made up roughly 45–55% of typical customer bills in 2023—so commodity churn limits margin expansion.

Industrial Load Defection

Large industrial and commercial customers have far higher bargaining power than residential users because they consume disproportionately more energy; Unitil’s top 10 industrial accounts can represent over 25% of a utility’s commercial revenue, so losing one matters. These customers can threaten load defection—relocating facilities or investing in on-site generation and storage—to avoid high rates; in 2024, US industrial solar plus storage projects grew 18% year-over-year, lowering switching costs. To retain them, Unitil routinely offers bespoke economic development rates, demand-response payments, and efficiency incentives that can cut effective rates by 5–15%.

Energy Efficiency and Demand Response

Customers using smart thermostats, rooftop solar, and LEDs cut Unitil’s volumetric sales; in 2024 US residential solar capacity grew ~25% year-over-year to 35 GW, and DOE reports demand response reduced peak load by 5–7% in some regions, directly lowering utility margins.

Conservation gives customers timing power via demand response programs; Unitil faces revenue risk as pay-per-kWh declines and fixed-cost recovery pressures rise, pressuring rate cases and ROE outcomes.

- 2024 US residential solar +25% (to ~35 GW)

- Demand response peak reduction 5–7%

- Volumetric sales decline → higher fixed-cost per kWh

Community Choice Aggregation

Municipalities in Unitil’s service area can form community choice aggregation (CCA) pools to buy power for residents, concentrating bargaining power across thousands of accounts and often securing rates 5–10% below default service or higher renewable mixes; Massachusetts and New Hampshire CCAs captured ~12% of eligible load in 2024, pressuring utilities to match offers.

Regulation, competition & DERs cap Unitil’s margins and pricing power

PUCs cap Unitil’s pricing power (2024 allowed ROE ~8.5%), limiting distribution-margin growth (~2.1% y/y in 2024). Competitive retail suppliers and CCAs (≈12% load in MA/NH, 2024) and commodity shopping (30–40% small commercial choice) constrain bill markup. Large industrial customers (>25% commercial rev concentrated) and DERs (US residential solar +25% to ~35 GW, 2024) raise switching risk and lower volumetric sales.

| Metric | 2024 |

|---|---|

| Allowed ROE | ~8.5% |

| Regulated gross margin growth | ~2.1% y/y |

| CCA load (MA/NH) | ~12% |

| Small commercial on competitive suppliers | 30–40% |

| US residential solar capacity | ~35 GW (+25%) |

Full Version Awaits

Unitil Porter's Five Forces Analysis

This preview shows the exact Unitil Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

You're looking at the actual, fully formatted document; once you complete your purchase, you’ll get instant access to this same file ready for download and use.

No mockups or samples—the deliverable shown is the complete, professional analysis you’ll be able to download after payment.