Unitil PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how regulatory shifts, market dynamics, and environmental trends are reshaping Unitil’s prospects—our PESTLE Analysis distills the external forces that matter to investors and strategists. Ready-made and research-backed, it’s ideal for modelling risk, spotting growth, and informing boardroom decisions. Purchase the full analysis to download the complete, editable report and act with confidence.

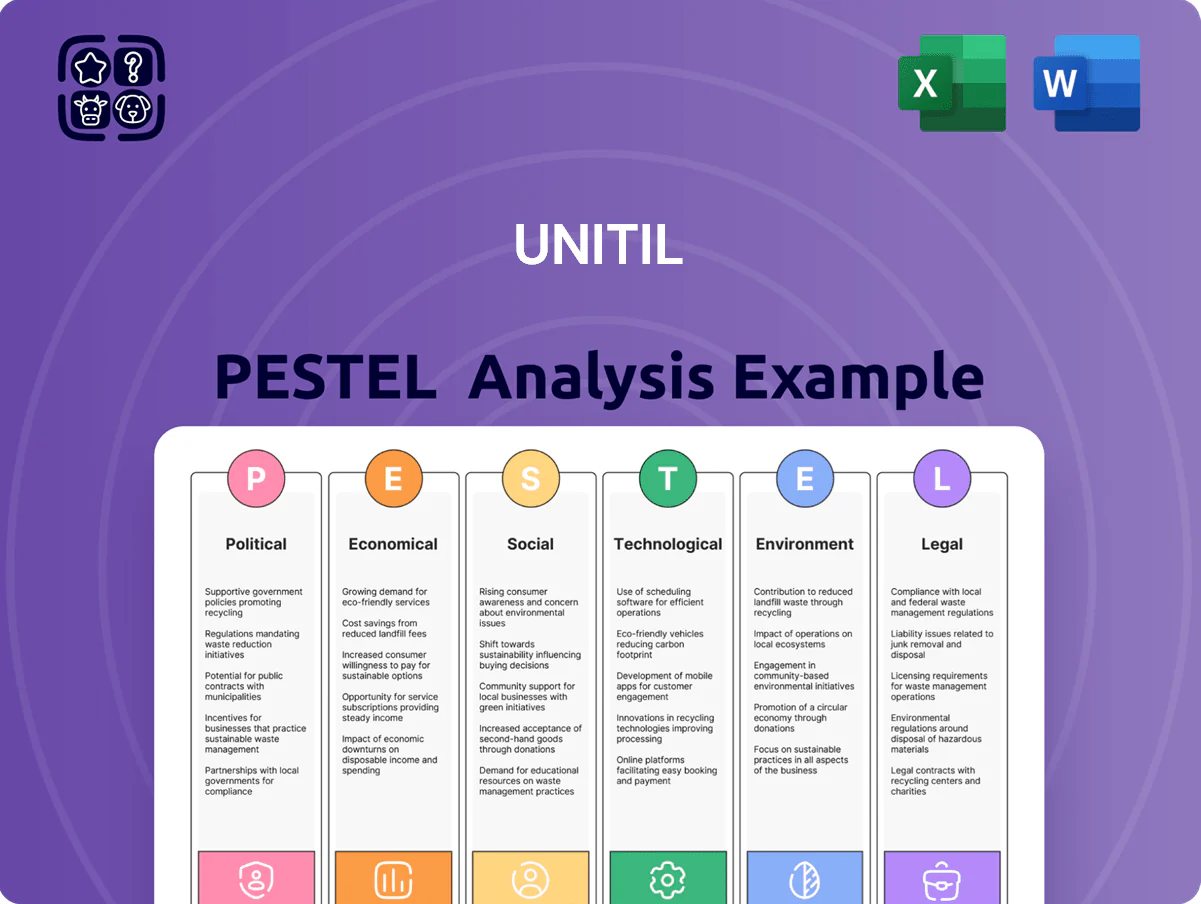

Political factors

State Regulatory Oversight

Unitil is regulated by state utility commissions in New Hampshire, Maine and Massachusetts that set rate structures and allowable returns, with the company reporting $844 million 2024 regulated revenues across its territories. Political shifts affecting commission appointments can alter regulatory philosophy on rate hikes—Massachusetts saw a 2024 commission turnover of 33%—impacting allowed ROE and recovery timelines. Unitil must lobby state legislators and maintain stakeholder engagement to secure approvals for grid upgrades and infrastructure projects averaging $120–150 million annually.

Federal Energy Policy

Federal mandates and incentives, notably the Inflation Reduction Act which authorized roughly $369 billion for energy and climate programs through 2031, accelerate grid modernization and renewable integration that directly affect Unitil’s project prioritization.

Shifts in federal administration can reallocate funding between fossil fuel support and decarbonization targets, altering expected federal grant and tax-credit availability for utility CAPEX.

Unitil must align its long-term capital investment plan—recently budgeting roughly $200–250 million annually in distribution and reliability projects—with national energy security and emissions goals to capture IRA incentives and meet regulatory expectations.

Local Government Climate Mandates

Municipal climate plans in Unitil’s New England territory increasingly limit gas growth; as of 2025 over 40 Massachusetts municipalities have adopted gas hookup restrictions or bans, pressuring demand for Unitil’s gas distribution tied to about $1.2B in regulated rate base (2024 filings).

Local ordinances accelerating electrification—Massachusetts set a 2050 net‑zero law and many towns target 2030‑2040 building electrification—force Unitil to reallocate capex toward electric heating, grid upgrades, and cross‑fuel initiatives.

To mitigate revenue risk from declining gas volumes (gas sales fell ~3% YoY in 2024 regionally), Unitil must expand electric heating programs, heat pump rebates, and pilot hydrogen/renewable natural gas projects to preserve margins and regulatory recoveries.

Interstate Energy Cooperation

Interstate energy cooperation in New England directly affects Unitil: regional transmission projects require multi-state approvals and funding, and delays raise costs—ISO-NE estimates needed transmission investments of ~$7–10 billion through 2030 to meet reliability and decarbonization goals.

Political resistance in any state can constrain supply, increasing price volatility; Unitil’s New Hampshire and Maine service territories are exposed to regional capacity tightness with winter peak reserve margins below 10% in several recent years.

- Multi-state approvals critical for transmission projects (~$7–10B regional need to 2030)

- Delays or political friction can cause supply constraints and higher customer prices

- Reserve margins under 10% in winter increase volatility risk for Unitil territories

Public Advocacy and Lobbying

Environmental advocacy groups and consumer protection organizations exert strong political pressure on Unitil, intervening in 2024-25 regulatory dockets that contested $120m of proposed grid investments and sought lower rate increases after Unitil's 2024 ROE filing (9.5%) prompted hearings.

These stakeholders frequently challenge capital plans and rate adjustments, forcing longer review timelines—median proceeding delays rose to 9 months in 2024—and pushing Unitil to adopt transparent stakeholder engagement to defend necessary upgrades for reliability.

Proactive communication and targeted lobbying help shape legislative outcomes; Unitil reported $1.3m lobbying spend in 2024 and increased community outreach to preserve support for grid-stability investments amid rising scrutiny.

- 2024 contested investments: $120m

- 2024 ROE filing cited: 9.5%

- Median regulatory delay: 9 months (2024)

- Lobbying spend: $1.3m (2024)

Regulatory and policy shifts drive Unitil ROE, capex and electrification risks/opps

Regulatory oversight in NH/ME/MA drives allowed ROE and rates (2024 ROE filing 9.5%; $844M regulated revenues). IRA funding ($369B through 2031) and MA net‑zero laws push electrification; 40+ MA towns restrict gas (2025). Unitil capex ~$200–250M/yr; contested $120M investments in 2024; lobbying $1.3M (2024); median regulatory delay 9 months (2024).

What is included in the product

Explores how external macro-environmental factors uniquely affect Unitil across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends to identify threats, opportunities, and implications for strategy and investment.

A concise, shareable Unitil PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or planning sessions to align teams and support external risk discussions.

Economic factors

Interest Rate Environment

As a capital-intensive utility, Unitil is highly sensitive to interest-rate moves; the US 10-year Treasury rose from ~3.5% in Jan 2024 to ~4.2% by Dec 2024, lifting corporate borrowing costs and raising financing expense on multi-year infrastructure projects.

Higher rates increase debt-servicing costs—Unitil’s long-term debt of ~$650M (2024) faces more expensive refinancing, compressing margins if rate pass-through to customers lags regulatory timelines.

Investors watch the Fed: after 2022–2023 hikes, by end‑2024 markets priced fewer cuts, reducing Unitil’s dividend yield attractiveness versus 10-year Treasuries (yield ~4.2%), affecting stock valuation.

Regional Economic Health

Regional economic health in New Hampshire, Maine, and Massachusetts directly affects Unitil’s load and revenues; 2024 state GDP growth estimates: MA 2.1%, NH 1.3%, ME 1.0%, with metro Boston driving commercial demand.

Economic downturns reduce industrial and commercial consumption—Unitil’s 2023 weather-normalized throughput fell ~1.8% year-over-year during softer industrial activity.

Conversely, strong housing starts (New England single-family permits up ~4% in 2024) and population gains increase distribution capex and customer additions, pressuring capital deployment.

Energy Commodity Price Volatility

Fluctuations in natural gas and wholesale electricity prices are generally passed to Unitil customers; winter 2023–24 saw U.S. Henry Hub gas average ~$3.50/MMBtu vs 2022 peaks >$9, and high prices historically cut consumption—retail kWh/meter fell ~2–4% in spike years. Extreme spikes raise bad-debt risk; U.S. utility arrears rose to ~5.5% in 2022. Unitil uses hedging and forward contracts to smooth margins, but global LNG markets and geopolitics chiefly drive commodity cost swings.

Inflationary Pressure on Operations

Persistent inflation raised Unitil's input costs—wages rose ~4.1% y/y and material prices (steel, transformers) up 6–12% in 2024—pressuring O&M and capital maintenance for its distribution network.

Although regulators permit cost recovery via rate cases, average regulatory lag of 12–24 months compressed short-term cash flow and increased working capital needs in 2024.

Unitil must accelerate cost controls, pursue productivity gains and targeted CAPEX prioritization to protect margins and credit metrics during inflationary periods.

- Wage inflation ~4.1% (2024)

- Material cost rise 6–12% (2024)

- Regulatory lag ~12–24 months

- Actions: cost controls, efficiency, CAPEX reprioritization

Capital Market Access

Unitil depends on steady equity and debt access to fund its $300–400 million multi-year capital program; a credit downgrade could raise borrowing costs above its 2024 average long-term debt rate near 4.0%, tightening liquidity.

Economic instability or higher rates would limit funding for grid upgrades and gas infrastructure, making a strong balance sheet critical to retain investment-grade access amid 2024–25 market volatility.

- 2024 capex plan: ~$300–400M

- 2024 long-term debt rate: ~4.0%

- Credit health key to avoid higher spreads and liquidity constraints

Unitil faces rising costs and rate pressure; strong credit crucial as recovery lags

Unitil faces higher financing costs (2024 long‑term debt ~$650M, avg rate ~4.0%) and inflationary input pressures (wages +4.1%, materials +6–12%), while regional GDP (MA 2.1%, NH 1.3%, ME 1.0%) and housing (+4% permits) drive demand; regulatory lag (12–24 months) delays cost recovery, making cost control and strong credit essential.

| Metric | 2024 |

|---|---|

| Long-term debt | ~$650M |

| Avg debt rate | ~4.0% |

| Wage inflation | +4.1% |

| Material costs | +6–12% |

| Capex plan | $300–400M |

Full Version Awaits

Unitil PESTLE Analysis

The preview shown here is the exact Unitil PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the final file you’ll be able to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how regulatory shifts, market dynamics, and environmental trends are reshaping Unitil’s prospects—our PESTLE Analysis distills the external forces that matter to investors and strategists. Ready-made and research-backed, it’s ideal for modelling risk, spotting growth, and informing boardroom decisions. Purchase the full analysis to download the complete, editable report and act with confidence.

Political factors

State Regulatory Oversight

Unitil is regulated by state utility commissions in New Hampshire, Maine and Massachusetts that set rate structures and allowable returns, with the company reporting $844 million 2024 regulated revenues across its territories. Political shifts affecting commission appointments can alter regulatory philosophy on rate hikes—Massachusetts saw a 2024 commission turnover of 33%—impacting allowed ROE and recovery timelines. Unitil must lobby state legislators and maintain stakeholder engagement to secure approvals for grid upgrades and infrastructure projects averaging $120–150 million annually.

Federal Energy Policy

Federal mandates and incentives, notably the Inflation Reduction Act which authorized roughly $369 billion for energy and climate programs through 2031, accelerate grid modernization and renewable integration that directly affect Unitil’s project prioritization.

Shifts in federal administration can reallocate funding between fossil fuel support and decarbonization targets, altering expected federal grant and tax-credit availability for utility CAPEX.

Unitil must align its long-term capital investment plan—recently budgeting roughly $200–250 million annually in distribution and reliability projects—with national energy security and emissions goals to capture IRA incentives and meet regulatory expectations.

Local Government Climate Mandates

Municipal climate plans in Unitil’s New England territory increasingly limit gas growth; as of 2025 over 40 Massachusetts municipalities have adopted gas hookup restrictions or bans, pressuring demand for Unitil’s gas distribution tied to about $1.2B in regulated rate base (2024 filings).

Local ordinances accelerating electrification—Massachusetts set a 2050 net‑zero law and many towns target 2030‑2040 building electrification—force Unitil to reallocate capex toward electric heating, grid upgrades, and cross‑fuel initiatives.

To mitigate revenue risk from declining gas volumes (gas sales fell ~3% YoY in 2024 regionally), Unitil must expand electric heating programs, heat pump rebates, and pilot hydrogen/renewable natural gas projects to preserve margins and regulatory recoveries.

Interstate Energy Cooperation

Interstate energy cooperation in New England directly affects Unitil: regional transmission projects require multi-state approvals and funding, and delays raise costs—ISO-NE estimates needed transmission investments of ~$7–10 billion through 2030 to meet reliability and decarbonization goals.

Political resistance in any state can constrain supply, increasing price volatility; Unitil’s New Hampshire and Maine service territories are exposed to regional capacity tightness with winter peak reserve margins below 10% in several recent years.

- Multi-state approvals critical for transmission projects (~$7–10B regional need to 2030)

- Delays or political friction can cause supply constraints and higher customer prices

- Reserve margins under 10% in winter increase volatility risk for Unitil territories

Public Advocacy and Lobbying

Environmental advocacy groups and consumer protection organizations exert strong political pressure on Unitil, intervening in 2024-25 regulatory dockets that contested $120m of proposed grid investments and sought lower rate increases after Unitil's 2024 ROE filing (9.5%) prompted hearings.

These stakeholders frequently challenge capital plans and rate adjustments, forcing longer review timelines—median proceeding delays rose to 9 months in 2024—and pushing Unitil to adopt transparent stakeholder engagement to defend necessary upgrades for reliability.

Proactive communication and targeted lobbying help shape legislative outcomes; Unitil reported $1.3m lobbying spend in 2024 and increased community outreach to preserve support for grid-stability investments amid rising scrutiny.

- 2024 contested investments: $120m

- 2024 ROE filing cited: 9.5%

- Median regulatory delay: 9 months (2024)

- Lobbying spend: $1.3m (2024)

Regulatory and policy shifts drive Unitil ROE, capex and electrification risks/opps

Regulatory oversight in NH/ME/MA drives allowed ROE and rates (2024 ROE filing 9.5%; $844M regulated revenues). IRA funding ($369B through 2031) and MA net‑zero laws push electrification; 40+ MA towns restrict gas (2025). Unitil capex ~$200–250M/yr; contested $120M investments in 2024; lobbying $1.3M (2024); median regulatory delay 9 months (2024).

What is included in the product

Explores how external macro-environmental factors uniquely affect Unitil across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region-specific trends to identify threats, opportunities, and implications for strategy and investment.

A concise, shareable Unitil PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or planning sessions to align teams and support external risk discussions.

Economic factors

Interest Rate Environment

As a capital-intensive utility, Unitil is highly sensitive to interest-rate moves; the US 10-year Treasury rose from ~3.5% in Jan 2024 to ~4.2% by Dec 2024, lifting corporate borrowing costs and raising financing expense on multi-year infrastructure projects.

Higher rates increase debt-servicing costs—Unitil’s long-term debt of ~$650M (2024) faces more expensive refinancing, compressing margins if rate pass-through to customers lags regulatory timelines.

Investors watch the Fed: after 2022–2023 hikes, by end‑2024 markets priced fewer cuts, reducing Unitil’s dividend yield attractiveness versus 10-year Treasuries (yield ~4.2%), affecting stock valuation.

Regional Economic Health

Regional economic health in New Hampshire, Maine, and Massachusetts directly affects Unitil’s load and revenues; 2024 state GDP growth estimates: MA 2.1%, NH 1.3%, ME 1.0%, with metro Boston driving commercial demand.

Economic downturns reduce industrial and commercial consumption—Unitil’s 2023 weather-normalized throughput fell ~1.8% year-over-year during softer industrial activity.

Conversely, strong housing starts (New England single-family permits up ~4% in 2024) and population gains increase distribution capex and customer additions, pressuring capital deployment.

Energy Commodity Price Volatility

Fluctuations in natural gas and wholesale electricity prices are generally passed to Unitil customers; winter 2023–24 saw U.S. Henry Hub gas average ~$3.50/MMBtu vs 2022 peaks >$9, and high prices historically cut consumption—retail kWh/meter fell ~2–4% in spike years. Extreme spikes raise bad-debt risk; U.S. utility arrears rose to ~5.5% in 2022. Unitil uses hedging and forward contracts to smooth margins, but global LNG markets and geopolitics chiefly drive commodity cost swings.

Inflationary Pressure on Operations

Persistent inflation raised Unitil's input costs—wages rose ~4.1% y/y and material prices (steel, transformers) up 6–12% in 2024—pressuring O&M and capital maintenance for its distribution network.

Although regulators permit cost recovery via rate cases, average regulatory lag of 12–24 months compressed short-term cash flow and increased working capital needs in 2024.

Unitil must accelerate cost controls, pursue productivity gains and targeted CAPEX prioritization to protect margins and credit metrics during inflationary periods.

- Wage inflation ~4.1% (2024)

- Material cost rise 6–12% (2024)

- Regulatory lag ~12–24 months

- Actions: cost controls, efficiency, CAPEX reprioritization

Capital Market Access

Unitil depends on steady equity and debt access to fund its $300–400 million multi-year capital program; a credit downgrade could raise borrowing costs above its 2024 average long-term debt rate near 4.0%, tightening liquidity.

Economic instability or higher rates would limit funding for grid upgrades and gas infrastructure, making a strong balance sheet critical to retain investment-grade access amid 2024–25 market volatility.

- 2024 capex plan: ~$300–400M

- 2024 long-term debt rate: ~4.0%

- Credit health key to avoid higher spreads and liquidity constraints

Unitil faces rising costs and rate pressure; strong credit crucial as recovery lags

Unitil faces higher financing costs (2024 long‑term debt ~$650M, avg rate ~4.0%) and inflationary input pressures (wages +4.1%, materials +6–12%), while regional GDP (MA 2.1%, NH 1.3%, ME 1.0%) and housing (+4% permits) drive demand; regulatory lag (12–24 months) delays cost recovery, making cost control and strong credit essential.

| Metric | 2024 |

|---|---|

| Long-term debt | ~$650M |

| Avg debt rate | ~4.0% |

| Wage inflation | +4.1% |

| Material costs | +6–12% |

| Capex plan | $300–400M |

Full Version Awaits

Unitil PESTLE Analysis

The preview shown here is the exact Unitil PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the final file you’ll be able to download immediately after payment.