Univar Solutions SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Univar Solutions sits at the crossroads of resilient distribution networks and growing demand for specialty chemicals, yet faces margin pressure, raw-material volatility, and integration challenges—our full SWOT unpacks these dynamics with actionable insights and strategic priorities. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel matrix for confident planning, pitching, and investment decisions.

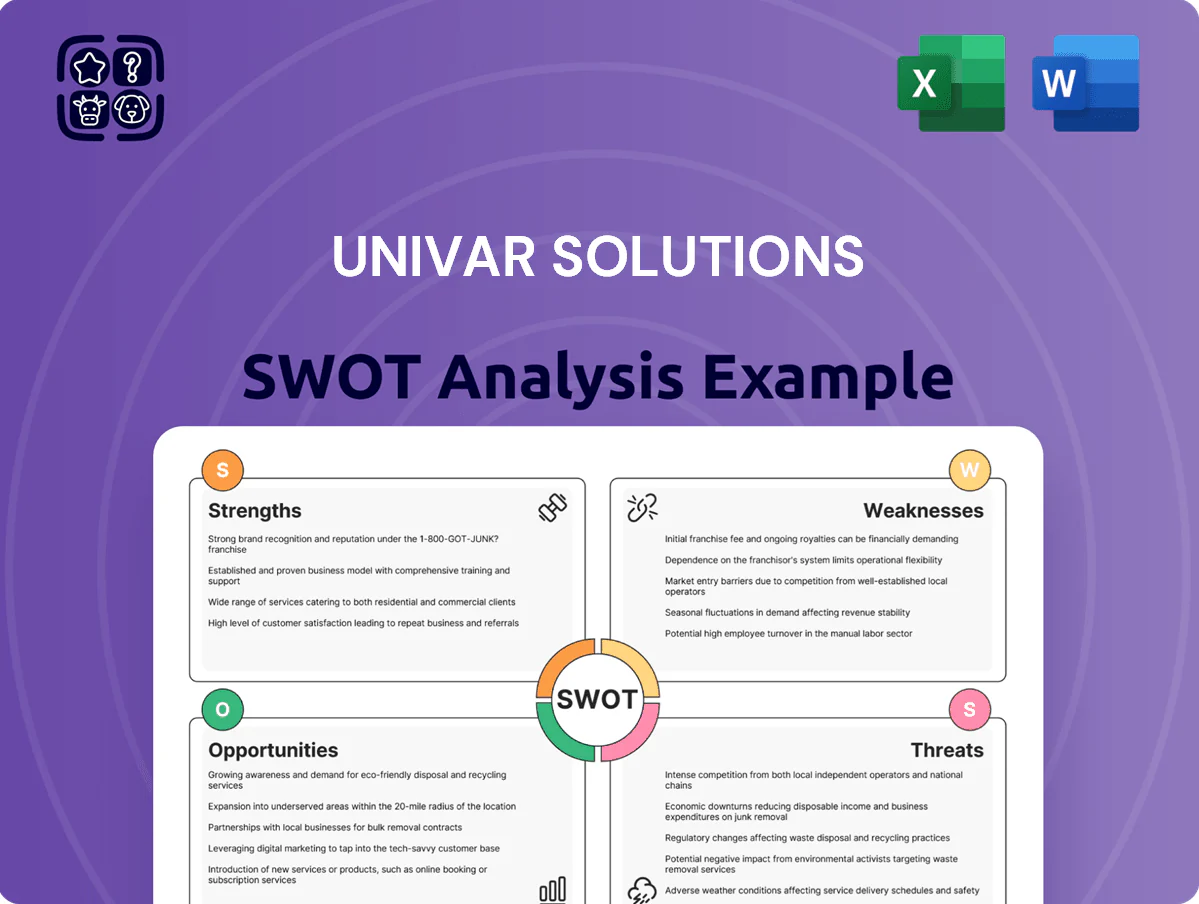

Strengths

Global Distribution Network

Univar Solutions operates one of the largest chemical distribution networks, with over 700 warehouses and 170 distribution centers across North America, Europe and emerging markets as of FY2024, enabling efficient last-mile delivery competitors find hard to match.

The company’s fleet and warehousing assets support >98% on-time delivery in key regions and helped generate $8.6 billion in revenue in 2024, underpinning consistent service levels across diverse geographies.

Diverse Product Portfolio

Univar Solutions serves over 100,000 customers worldwide and balances commodity chemicals with high-growth specialty ingredients—specialties made up about 34% of 2024 revenue, helping offset cyclicality in any single end-market.

Technical Value-Added Services

Univar Solutions leverages 36 global solution centers and test kitchens to offer formulation, product development, and lab testing, turning distribution into technical partnership and boosting customer retention; in 2024 these services supported ~12% of commercial wins, per company disclosures.

Private Equity Backing Efficiency

- SG&A down ~12% since 2021

- Adjusted EBITDA margin 5.8% → 8.4% (FY2021→Q3 2025)

- $180m digital spend; $400m capex through 2025

- Working capital days reduced ~9 days

Strong Supplier Relationships

Univar Solutions keeps long-standing partnerships with leading chemical producers, securing reliable access to critical raw materials during disruptions; in 2024 suppliers accounted for over 60% of its $11.5B revenue, underscoring supply stability.

The company’s global scale makes it the preferred channel to reach fragmented small and midmarket customers, delivering competitive supplier pricing and early access to new products—Univar reported 12% of sales from new product introductions in 2024.

- 60% of 2024 revenue tied to core suppliers

- $11.5B total 2024 revenue

- 12% sales from new products in 2024

Univar: $11.5B scale, 34% specialties, margins up to 8.4% via digital & capex

Univar Solutions’ global network (700+ warehouses, 170 DCs) and long supplier ties drive scale, reliability and $11.5B revenue in 2024; specialties were 34% of sales, supporting margins. Private ownership cut SG&A ~12% and digital/capex ($180M/$400M through 2025) lifted adjusted EBITDA from 5.8% (FY2021) to 8.4% (Q3 2025) and trimmed working capital ~9 days.

| Metric | Value |

|---|---|

| 2024 Revenue | $11.5B |

| Specialties % | 34% |

| Adjusted EBITDA | 5.8%→8.4% |

| Digital spend | $180M |

| Capex through 2025 | $400M |

What is included in the product

Provides a concise SWOT overview of Univar Solutions, highlighting its operational strengths, strategic weaknesses, market opportunities, and external threats to assess competitive positioning and future growth prospects.

Provides a concise SWOT matrix for Univar Solutions to quickly align strategy and highlight risk/opportunity vectors for fast executive decision-making.

Weaknesses

High Debt Levels

The 2021 leveraged buyout by Apollo raised Univar Solutions’ net debt to about $5.5 billion by year-end 2021, requiring strong free cash flow to service principal and interest.

Higher mid-2020s interest rates pushed annual cash interest expense toward ~$300–350 million in 2023–2024, squeezing funds for large organic growth.

Managing leverage is core: covenant headroom and scheduled maturities (notably a $1.2B tranche due 2026) will shape long-term financial flexibility.

Exposure to Volatile Input Costs

As a distributor, Univar Solutions is highly exposed to raw-material and energy price swings driven by global commodity markets; in 2024 feedstock and freight cost variability contributed to a 6–8% gross margin volatility quarter-to-quarter. They can pass some costs to customers, but rapid spikes—like the 35% surge in methanol prices in late 2023—can squeeze margins if inventory timing is off. Inventory carrying rose 12% year-over-year in 2024, worsening timing risk. This input volatility makes consistent bottom-line growth hard to predict in unstable economies.

Complex Integration Requirements

Univar Solutions’ acquisition-led growth left a fragmented IT estate and overlapping roles after >40 deals since 2016, raising integration costs; IT consolidation projects in 2024 reportedly added ~USD 25–40m in one-time admin spending.

Disparate ERP, warehousing and compliance systems across 30+ countries cause temporary inefficiencies, slowing synergies—management noted up to 12–18 months to stabilize certain integrations.

If full synergy realization falls short of the ~USD 75–100m target per major deal, incremental units may remain margin-dilutive and depress consolidated EBITDA conversion.

Dependence on Industrial Production

A large share of Univar Solutions’ 2024 revenue—about $9.6 billion of total $11.1 billion—tracks industrial production, tying results to manufacturing cycles.

During recessions, demand for chemicals in automotive and construction can drop 15–30% year-over-year, making Univar’s volumes and margins highly cyclical.

This macro sensitivity raised leverage risk after 2023–24 M&A and pushed adjusted net debt/EBITDA toward 3.0x in 2024, limiting financial flexibility.

- ~86% 2024 revenue linked to industrial end-markets

- Auto/construction demand swings ±15–30%

- Adjusted net debt/EBITDA ≈ 3.0x (2024)

Thin Profit Margins

High leverage, thin margins and commodity volatility pressure cash flow and 2026 maturities

High leverage from Apollo’s 2021 LBO (net debt ≈ $5.5B end-2021; adjusted net debt/EBITDA ≈ 3.0x in 2024) forces heavy cash interest (~$300–350M in 2023–24) and tight covenant/maturity pressure (notably $1.2B due 2026), while commodity-driven input and freight volatility (6–8% gross margin swing; inventory +12% YoY) plus low adjusted EBITDA margin (~6.1%) make profits highly cyclical and integration-sensitive.

| Metric | Value (2024) |

|---|---|

| Revenue tied to industrial markets | $9.6B of $11.1B |

| Adjusted EBITDA margin | ~6.1% |

| Net margin | ~1.8% |

| Adjusted net debt/EBITDA | ≈3.0x |

| Annual cash interest | ~$300–350M |

| Inventory change | +12% YoY |

Preview the Actual Deliverable

Univar Solutions SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and reflects the same structured, editable file unlocked after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Univar Solutions sits at the crossroads of resilient distribution networks and growing demand for specialty chemicals, yet faces margin pressure, raw-material volatility, and integration challenges—our full SWOT unpacks these dynamics with actionable insights and strategic priorities. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel matrix for confident planning, pitching, and investment decisions.

Strengths

Global Distribution Network

Univar Solutions operates one of the largest chemical distribution networks, with over 700 warehouses and 170 distribution centers across North America, Europe and emerging markets as of FY2024, enabling efficient last-mile delivery competitors find hard to match.

The company’s fleet and warehousing assets support >98% on-time delivery in key regions and helped generate $8.6 billion in revenue in 2024, underpinning consistent service levels across diverse geographies.

Diverse Product Portfolio

Univar Solutions serves over 100,000 customers worldwide and balances commodity chemicals with high-growth specialty ingredients—specialties made up about 34% of 2024 revenue, helping offset cyclicality in any single end-market.

Technical Value-Added Services

Univar Solutions leverages 36 global solution centers and test kitchens to offer formulation, product development, and lab testing, turning distribution into technical partnership and boosting customer retention; in 2024 these services supported ~12% of commercial wins, per company disclosures.

Private Equity Backing Efficiency

- SG&A down ~12% since 2021

- Adjusted EBITDA margin 5.8% → 8.4% (FY2021→Q3 2025)

- $180m digital spend; $400m capex through 2025

- Working capital days reduced ~9 days

Strong Supplier Relationships

Univar Solutions keeps long-standing partnerships with leading chemical producers, securing reliable access to critical raw materials during disruptions; in 2024 suppliers accounted for over 60% of its $11.5B revenue, underscoring supply stability.

The company’s global scale makes it the preferred channel to reach fragmented small and midmarket customers, delivering competitive supplier pricing and early access to new products—Univar reported 12% of sales from new product introductions in 2024.

- 60% of 2024 revenue tied to core suppliers

- $11.5B total 2024 revenue

- 12% sales from new products in 2024

Univar: $11.5B scale, 34% specialties, margins up to 8.4% via digital & capex

Univar Solutions’ global network (700+ warehouses, 170 DCs) and long supplier ties drive scale, reliability and $11.5B revenue in 2024; specialties were 34% of sales, supporting margins. Private ownership cut SG&A ~12% and digital/capex ($180M/$400M through 2025) lifted adjusted EBITDA from 5.8% (FY2021) to 8.4% (Q3 2025) and trimmed working capital ~9 days.

| Metric | Value |

|---|---|

| 2024 Revenue | $11.5B |

| Specialties % | 34% |

| Adjusted EBITDA | 5.8%→8.4% |

| Digital spend | $180M |

| Capex through 2025 | $400M |

What is included in the product

Provides a concise SWOT overview of Univar Solutions, highlighting its operational strengths, strategic weaknesses, market opportunities, and external threats to assess competitive positioning and future growth prospects.

Provides a concise SWOT matrix for Univar Solutions to quickly align strategy and highlight risk/opportunity vectors for fast executive decision-making.

Weaknesses

High Debt Levels

The 2021 leveraged buyout by Apollo raised Univar Solutions’ net debt to about $5.5 billion by year-end 2021, requiring strong free cash flow to service principal and interest.

Higher mid-2020s interest rates pushed annual cash interest expense toward ~$300–350 million in 2023–2024, squeezing funds for large organic growth.

Managing leverage is core: covenant headroom and scheduled maturities (notably a $1.2B tranche due 2026) will shape long-term financial flexibility.

Exposure to Volatile Input Costs

As a distributor, Univar Solutions is highly exposed to raw-material and energy price swings driven by global commodity markets; in 2024 feedstock and freight cost variability contributed to a 6–8% gross margin volatility quarter-to-quarter. They can pass some costs to customers, but rapid spikes—like the 35% surge in methanol prices in late 2023—can squeeze margins if inventory timing is off. Inventory carrying rose 12% year-over-year in 2024, worsening timing risk. This input volatility makes consistent bottom-line growth hard to predict in unstable economies.

Complex Integration Requirements

Univar Solutions’ acquisition-led growth left a fragmented IT estate and overlapping roles after >40 deals since 2016, raising integration costs; IT consolidation projects in 2024 reportedly added ~USD 25–40m in one-time admin spending.

Disparate ERP, warehousing and compliance systems across 30+ countries cause temporary inefficiencies, slowing synergies—management noted up to 12–18 months to stabilize certain integrations.

If full synergy realization falls short of the ~USD 75–100m target per major deal, incremental units may remain margin-dilutive and depress consolidated EBITDA conversion.

Dependence on Industrial Production

A large share of Univar Solutions’ 2024 revenue—about $9.6 billion of total $11.1 billion—tracks industrial production, tying results to manufacturing cycles.

During recessions, demand for chemicals in automotive and construction can drop 15–30% year-over-year, making Univar’s volumes and margins highly cyclical.

This macro sensitivity raised leverage risk after 2023–24 M&A and pushed adjusted net debt/EBITDA toward 3.0x in 2024, limiting financial flexibility.

- ~86% 2024 revenue linked to industrial end-markets

- Auto/construction demand swings ±15–30%

- Adjusted net debt/EBITDA ≈ 3.0x (2024)

Thin Profit Margins

High leverage, thin margins and commodity volatility pressure cash flow and 2026 maturities

High leverage from Apollo’s 2021 LBO (net debt ≈ $5.5B end-2021; adjusted net debt/EBITDA ≈ 3.0x in 2024) forces heavy cash interest (~$300–350M in 2023–24) and tight covenant/maturity pressure (notably $1.2B due 2026), while commodity-driven input and freight volatility (6–8% gross margin swing; inventory +12% YoY) plus low adjusted EBITDA margin (~6.1%) make profits highly cyclical and integration-sensitive.

| Metric | Value (2024) |

|---|---|

| Revenue tied to industrial markets | $9.6B of $11.1B |

| Adjusted EBITDA margin | ~6.1% |

| Net margin | ~1.8% |

| Adjusted net debt/EBITDA | ≈3.0x |

| Annual cash interest | ~$300–350M |

| Inventory change | +12% YoY |

Preview the Actual Deliverable

Univar Solutions SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and reflects the same structured, editable file unlocked after payment.