Universal Logistics Holdings PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Universal Logistics Holdings’ strategy and risk profile—our concise PESTLE highlights key external drivers and actionable implications. Ideal for investors, strategists, and consultants seeking quick clarity; purchase the full analysis to unlock detailed data, scenario-driven insights, and ready-to-use slides for decision-making.

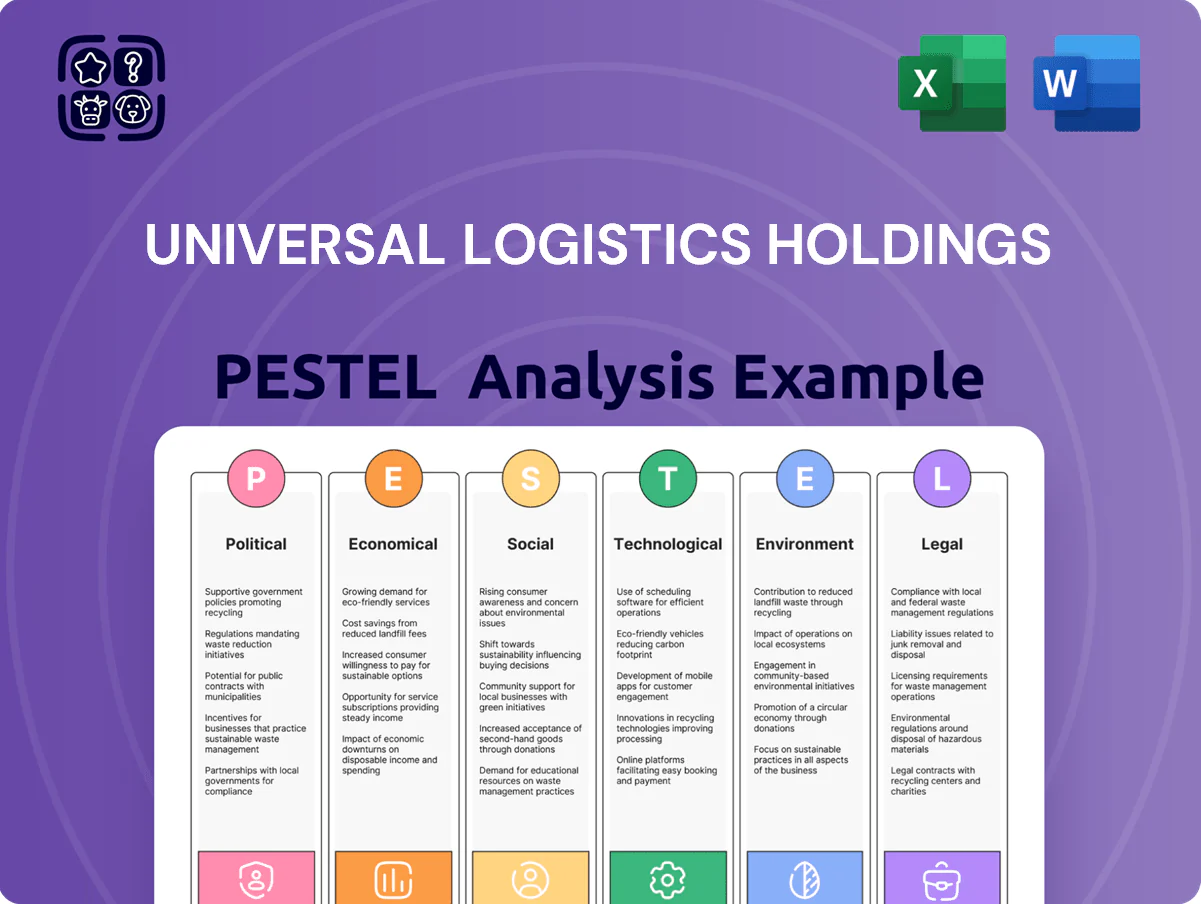

Political factors

USMCA Trade Policy Stability

The ongoing implementation of USMCA is pivotal for Universal Logistics, which handled roughly 28% of its FY2024 cross-border freight volumes between US, Mexico, and Canada, driving intermodal and truckload demand especially in automotive and industrial parts lanes.

Stable rules of origin and dispute mechanisms support predictable cargo flows; however, late-2025 monitoring is essential as a 2024–25 rise in regional protectionist measures correlated with a 7% tariff-sensitive modal shift in the sector.

Federal Infrastructure Investment

Federal infrastructure investment—notably the Bipartisan Infrastructure Law’s $110B for roads and bridges and $17B for ports through 2021–2026—directly affects Universal Logistics’ network efficiency; upgraded highways and ports can cut transit times and lower maintenance costs for its asset-heavy fleet, improving utilization rates and margins. Delays or withheld funding risk congestion in corridors like I-95 and the Ports of Los Angeles/Long Beach, raising fuel and dwell costs.

Labor Regulation and Union Influence

Political shifts on labor rights and unionization raise labor cost risks for Universal Logistics, where drivers and warehouse staff form a large portion of operating expenses; a 2024 BLS report showed transport and warehousing wage growth at 4.3% year-over-year, pressuring margins. Evolving federal stances on collective bargaining and worker classification could increase benefits and payroll taxes, affecting the company’s ~$2.1bn 2024 operating costs. As of 2025, intensified political pressure to strengthen protections influences contracting and workforce mix decisions.

Cross-Border Customs and Security

Strict customs enforcement and enhanced border security between the US, Mexico, and Canada can slow Universal Logistics’ cross-border lanes, with U.S. CBP processing delays rising 12% in 2024 at key ports of entry, impacting transit times for NAFTA trade corridors.

Political choices on staffing and deployment of inspection technology—CBP budget rose to $19.8B in FY2024—directly affect Universal’s brokerage efficiency and cost of compliance for clients.

Geopolitical tensions or security alerts have caused episodic closures and average dwell-time spikes of 18% in 2023–2024, risking just-in-time schedules for manufacturing customers.

- Customs strictness ↑ → transit delays; CBP delays +12% (2024)

- Staffing/tech funding (CBP $19.8B FY2024) → brokerage efficiency

- Tensions → dwell-time +18% (2023–2024) → JIT disruption

Corporate Tax Policy Shifts

- Projected federal rate scenarios 21%–25% affecting net margin forecasts

- Up to 30% tax credits for zero‑emission heavy vehicles in some jurisdictions

- State surtaxes in major lanes increase localized tax burden

- Alignment of CAPEX/fleet renewal timeline by end‑2025 required

USMCA lifts intermodal volumes but tariffs, CBP delays and wage/tax pressure margins

Political factors: USMCA-driven cross-border volumes (~28% of FY2024) boost intermodal demand but rising protectionism (2024–25) caused a 7% tariff-sensitive modal shift; infrastructure funding (BIL: $110B roads/bridges, $17B ports through 2026) cuts transit costs if delivered; CBP delays +12% (2024) and $19.8B CBP budget affect brokerage efficiency; transport wage growth 4.3% (2024) and federal tax scenarios (21%–25%) pressure margins.

| Metric | Value |

|---|---|

| Cross-border share FY2024 | ~28% |

| Modal shift (tariff-sensitive) | +7% (2024–25) |

| CBP delays | +12% (2024) |

| Ports/Roads funding | $17B / $110B (thru 2026) |

| Wage growth (transport) | 4.3% (2024) |

| CBP budget FY2024 | $19.8B |

| Federal tax scenarios | 21%–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Universal Logistics Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to the logistics and transportation sector.

A concise PESTLE snapshot tailored for Universal Logistics Holdings that highlights external risks and opportunities by category, ready to drop into presentations or share across teams for fast strategic alignment.

Economic factors

Interest Rate Environment

The Federal Reserve's policy rate, which averaged about 5.25–5.50% through 2024 and stayed elevated into 2025, raises Universal Logistics Holdings' cost of debt and increases financing costs for capital-intensive fleet and equipment upgrades.

Higher rates have weighed on industrial production and U.S. retail sales—freight volumes fell 2.1% year-over-year in parts of 2024—pressuring spot rates and utilization across Universal's network.

Managing interest expense—long-term debt was roughly $600 million as of FY2024—remains critical for preserving liquidity, covenant headroom, and a healthy balance sheet as macro conditions evolve in 2025.

Industrial Production Cycles

Universal Logistics’ revenue is closely linked to automotive and heavy industry output; US industrial production fell 0.1% month-over-month in Dec 2025 and manufacturing hours slipped 1.2% YoY, pressuring demand for specialized logistics and dedicated contract carriage.

In 2025 Universal reported 12% of revenue from automotive-dedicated contracts; a sustained manufacturing downturn could cut utilization and margins, forcing shift toward consumer staples and retail lanes where Q4 2025 retail freight volumes rose ~3.5% YoY.

Fuel Price Volatility

Diesel averaged about 3.90 USD/gal in 2024 with spikes to 4.50 USD/gal in Q3, directly driving Universal Logistics Holdings operating costs; fuel surcharges recover part of this but rapid spikes compressed brokerage margins by an estimated 2–3 percentage points in 2024.

Inflationary Labor Costs

Persistent wage inflation in logistics—US driver median pay rose about 8% in 2024 and warehouse wages climbed ~6%—squeezes Universal Logistics Holdings margins as competition for qualified drivers and staff remains intense.

Universal must balance higher compensation with client cost-efficiency, while 2024 capital expenditures near industry averages (automation investments up ~12%) to boost labor productivity across its network.

- Driver pay up ~8% (2024); warehouse wages ~6% (2024)

- Automation capex growth ~12% (2024) to offset labor costs

- Margin pressure from rising labor costs vs. client pricing sensitivity

Consumer Spending and E-commerce

Consumer demand drives intermodal and LTL volume; US retail sales rose 3.5% y/y in 2025 (Dec), supporting brokerage and warehousing for retail clients.

Continued e-commerce growth—online share ~18% of US retail sales in 2024—forces Universal to scale fulfillment and last-mile capabilities to manage higher parcel and split-shipment flows.

Household real disposable income trends and monthly retail sales are key indicators used to forecast demand for Universal’s brokerage, warehousing, and drayage services.

- Retail sales 2025 (Dec) +3.5% y/y

- US e-commerce share ~18% in 2024

- Household real disposable income guides demand forecasts

High rates, rising costs squeeze Universal as retail freight shifts and automation rises

Elevated Fed rates (~5.25–5.50% through 2024 into 2025) raise Universal’s debt servicing costs and capex financing needs; long-term debt ~600M (FY2024).

Freight volumes weakened (−2.1% YoY parts of 2024) while retail freight rose ~3.5% YoY (Dec 2025), shifting demand toward retail lanes and warehousing.

Diesel averaged ~$3.90/gal (2024) with spikes to $4.50/gal; driver pay +8% and warehouse wages +6% (2024) compress margins despite ~12% automation capex growth.

| Metric | Value |

|---|---|

| Fed policy rate | 5.25–5.50% |

| Long-term debt (FY2024) | $600M |

| Freight volume change (2024) | −2.1% YoY |

| Retail freight (Dec 2025) | +3.5% YoY |

| Diesel avg (2024) | $3.90/gal |

| Driver pay (2024) | +8% |

| Automation capex growth (2024) | +12% |

What You See Is What You Get

Universal Logistics Holdings PESTLE Analysis

The preview shown here is the exact Universal Logistics Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

What you’re previewing is the real file with complete content and layout; there are no placeholders or teasers, and you’ll be able to download this same document immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Universal Logistics Holdings’ strategy and risk profile—our concise PESTLE highlights key external drivers and actionable implications. Ideal for investors, strategists, and consultants seeking quick clarity; purchase the full analysis to unlock detailed data, scenario-driven insights, and ready-to-use slides for decision-making.

Political factors

USMCA Trade Policy Stability

The ongoing implementation of USMCA is pivotal for Universal Logistics, which handled roughly 28% of its FY2024 cross-border freight volumes between US, Mexico, and Canada, driving intermodal and truckload demand especially in automotive and industrial parts lanes.

Stable rules of origin and dispute mechanisms support predictable cargo flows; however, late-2025 monitoring is essential as a 2024–25 rise in regional protectionist measures correlated with a 7% tariff-sensitive modal shift in the sector.

Federal Infrastructure Investment

Federal infrastructure investment—notably the Bipartisan Infrastructure Law’s $110B for roads and bridges and $17B for ports through 2021–2026—directly affects Universal Logistics’ network efficiency; upgraded highways and ports can cut transit times and lower maintenance costs for its asset-heavy fleet, improving utilization rates and margins. Delays or withheld funding risk congestion in corridors like I-95 and the Ports of Los Angeles/Long Beach, raising fuel and dwell costs.

Labor Regulation and Union Influence

Political shifts on labor rights and unionization raise labor cost risks for Universal Logistics, where drivers and warehouse staff form a large portion of operating expenses; a 2024 BLS report showed transport and warehousing wage growth at 4.3% year-over-year, pressuring margins. Evolving federal stances on collective bargaining and worker classification could increase benefits and payroll taxes, affecting the company’s ~$2.1bn 2024 operating costs. As of 2025, intensified political pressure to strengthen protections influences contracting and workforce mix decisions.

Cross-Border Customs and Security

Strict customs enforcement and enhanced border security between the US, Mexico, and Canada can slow Universal Logistics’ cross-border lanes, with U.S. CBP processing delays rising 12% in 2024 at key ports of entry, impacting transit times for NAFTA trade corridors.

Political choices on staffing and deployment of inspection technology—CBP budget rose to $19.8B in FY2024—directly affect Universal’s brokerage efficiency and cost of compliance for clients.

Geopolitical tensions or security alerts have caused episodic closures and average dwell-time spikes of 18% in 2023–2024, risking just-in-time schedules for manufacturing customers.

- Customs strictness ↑ → transit delays; CBP delays +12% (2024)

- Staffing/tech funding (CBP $19.8B FY2024) → brokerage efficiency

- Tensions → dwell-time +18% (2023–2024) → JIT disruption

Corporate Tax Policy Shifts

- Projected federal rate scenarios 21%–25% affecting net margin forecasts

- Up to 30% tax credits for zero‑emission heavy vehicles in some jurisdictions

- State surtaxes in major lanes increase localized tax burden

- Alignment of CAPEX/fleet renewal timeline by end‑2025 required

USMCA lifts intermodal volumes but tariffs, CBP delays and wage/tax pressure margins

Political factors: USMCA-driven cross-border volumes (~28% of FY2024) boost intermodal demand but rising protectionism (2024–25) caused a 7% tariff-sensitive modal shift; infrastructure funding (BIL: $110B roads/bridges, $17B ports through 2026) cuts transit costs if delivered; CBP delays +12% (2024) and $19.8B CBP budget affect brokerage efficiency; transport wage growth 4.3% (2024) and federal tax scenarios (21%–25%) pressure margins.

| Metric | Value |

|---|---|

| Cross-border share FY2024 | ~28% |

| Modal shift (tariff-sensitive) | +7% (2024–25) |

| CBP delays | +12% (2024) |

| Ports/Roads funding | $17B / $110B (thru 2026) |

| Wage growth (transport) | 4.3% (2024) |

| CBP budget FY2024 | $19.8B |

| Federal tax scenarios | 21%–25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Universal Logistics Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to the logistics and transportation sector.

A concise PESTLE snapshot tailored for Universal Logistics Holdings that highlights external risks and opportunities by category, ready to drop into presentations or share across teams for fast strategic alignment.

Economic factors

Interest Rate Environment

The Federal Reserve's policy rate, which averaged about 5.25–5.50% through 2024 and stayed elevated into 2025, raises Universal Logistics Holdings' cost of debt and increases financing costs for capital-intensive fleet and equipment upgrades.

Higher rates have weighed on industrial production and U.S. retail sales—freight volumes fell 2.1% year-over-year in parts of 2024—pressuring spot rates and utilization across Universal's network.

Managing interest expense—long-term debt was roughly $600 million as of FY2024—remains critical for preserving liquidity, covenant headroom, and a healthy balance sheet as macro conditions evolve in 2025.

Industrial Production Cycles

Universal Logistics’ revenue is closely linked to automotive and heavy industry output; US industrial production fell 0.1% month-over-month in Dec 2025 and manufacturing hours slipped 1.2% YoY, pressuring demand for specialized logistics and dedicated contract carriage.

In 2025 Universal reported 12% of revenue from automotive-dedicated contracts; a sustained manufacturing downturn could cut utilization and margins, forcing shift toward consumer staples and retail lanes where Q4 2025 retail freight volumes rose ~3.5% YoY.

Fuel Price Volatility

Diesel averaged about 3.90 USD/gal in 2024 with spikes to 4.50 USD/gal in Q3, directly driving Universal Logistics Holdings operating costs; fuel surcharges recover part of this but rapid spikes compressed brokerage margins by an estimated 2–3 percentage points in 2024.

Inflationary Labor Costs

Persistent wage inflation in logistics—US driver median pay rose about 8% in 2024 and warehouse wages climbed ~6%—squeezes Universal Logistics Holdings margins as competition for qualified drivers and staff remains intense.

Universal must balance higher compensation with client cost-efficiency, while 2024 capital expenditures near industry averages (automation investments up ~12%) to boost labor productivity across its network.

- Driver pay up ~8% (2024); warehouse wages ~6% (2024)

- Automation capex growth ~12% (2024) to offset labor costs

- Margin pressure from rising labor costs vs. client pricing sensitivity

Consumer Spending and E-commerce

Consumer demand drives intermodal and LTL volume; US retail sales rose 3.5% y/y in 2025 (Dec), supporting brokerage and warehousing for retail clients.

Continued e-commerce growth—online share ~18% of US retail sales in 2024—forces Universal to scale fulfillment and last-mile capabilities to manage higher parcel and split-shipment flows.

Household real disposable income trends and monthly retail sales are key indicators used to forecast demand for Universal’s brokerage, warehousing, and drayage services.

- Retail sales 2025 (Dec) +3.5% y/y

- US e-commerce share ~18% in 2024

- Household real disposable income guides demand forecasts

High rates, rising costs squeeze Universal as retail freight shifts and automation rises

Elevated Fed rates (~5.25–5.50% through 2024 into 2025) raise Universal’s debt servicing costs and capex financing needs; long-term debt ~600M (FY2024).

Freight volumes weakened (−2.1% YoY parts of 2024) while retail freight rose ~3.5% YoY (Dec 2025), shifting demand toward retail lanes and warehousing.

Diesel averaged ~$3.90/gal (2024) with spikes to $4.50/gal; driver pay +8% and warehouse wages +6% (2024) compress margins despite ~12% automation capex growth.

| Metric | Value |

|---|---|

| Fed policy rate | 5.25–5.50% |

| Long-term debt (FY2024) | $600M |

| Freight volume change (2024) | −2.1% YoY |

| Retail freight (Dec 2025) | +3.5% YoY |

| Diesel avg (2024) | $3.90/gal |

| Driver pay (2024) | +8% |

| Automation capex growth (2024) | +12% |

What You See Is What You Get

Universal Logistics Holdings PESTLE Analysis

The preview shown here is the exact Universal Logistics Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

What you’re previewing is the real file with complete content and layout; there are no placeholders or teasers, and you’ll be able to download this same document immediately after checkout.