Univest Financial Boston Consulting Group Matrix

See the Bigger Picture

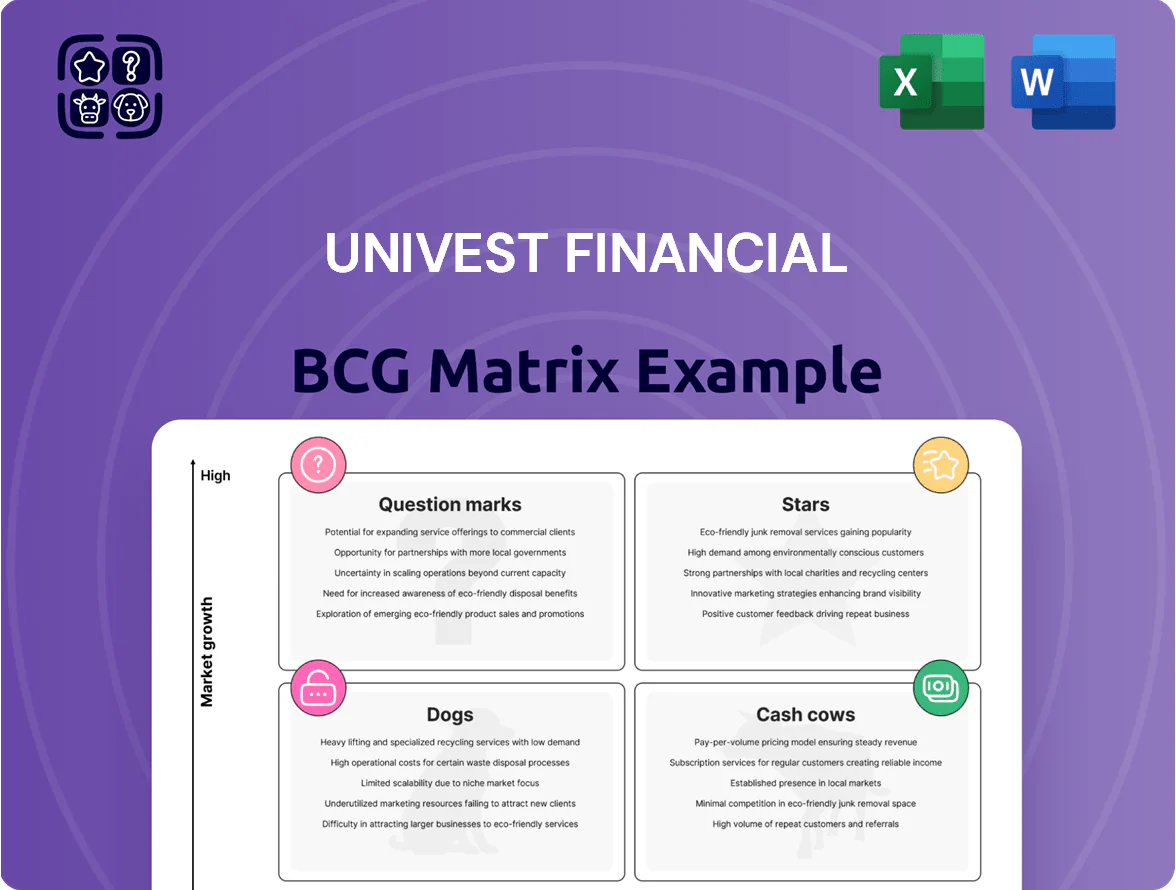

Univest Financial’s BCG Matrix preview highlights which business lines are driving growth and which may be draining capital, offering a snapshot of Stars, Cash Cows, Dogs, and Question Marks; but the full report delivers quadrant-by-quadrant placements, revenue and market-share data, and actionable strategies. Purchase the complete BCG Matrix to get a detailed Word report plus an Excel summary—ready-to-present insights that show where to allocate capital and how to sharpen competitive focus.

Stars

Commercial and Industrial Lending

Commercial and Industrial Lending is Univest’s Stars quadrant: management targets mid-single-digit annual balance growth through 2026 (about 4–6% CAGR) and this segment drove record 2025 pre-tax income, contributing roughly 35% of net interest income as yields averaged near 5.2% on new originations.

SBA Loan Origination Program

Univest ramped SBA 7(a)/504 originations in 2025 by ~85% YoY to $420M, targeting fee income that is less rate-sensitive than loans held for portfolio.

That niche boosts Univest’s BCG Stars positioning by capturing growing small-business demand—SBA loan originations rose 62% vs. 2019 industry levels—while requiring hires: ~45 specialized staff added in 2025.

Ongoing training and compliance spend (~$3.6M in 2025) raises operating costs short-term but management projects IRR >12% on seller-originated fees and servicing over five years.

Digital Banking and One Platform Ecosystem

Univest One Platform, which merges banking and wealth in one digital ecosystem, saw a 21% year-over-year rise in transactions through Q4 2025, signaling strong user adoption and engagement.

The firm raised its tech budget by 22% in 2025, funding UX, APIs, and security upgrades that cut onboarding time by ~30% and lifted digital net new deposits by 14%.

This high-growth digital segment is vital to defend market share vs fintechs and megabanks, contributing roughly 18% of Univest’s fee income in 2025 and growing.

Treasury Management Services

Treasury Management Services is a star for Univest Financial, delivering essential liquidity and fraud controls that drive an estimated 5–7% growth in non-interest income in 2025, supported by a 22% year-over-year rise in ACH volumes and a 15% increase in remote deposit users among mid-market clients.

High adoption of ACH, remote deposit, and merchant services cements Univest as a primary partner; merchant processing revenue grew ~12% in 2024, and API-enabled payment flows rose 40% through 2025.

Ongoing investment in APIs and real-time reporting keeps the unit a regional leader, with average daily float optimization improving working capital by an estimated $18M for corporate clients in 2024.

- Projected non-interest income growth 5–7% (2025)

- ACH volumes +22% YoY

- Remote deposit users +15% YoY

- Merchant revenue +12% (2024)

- API payment flows +40% (2025)

- Working capital benefit ~$18M (2024)

Equipment Finance Solutions

Equipment Finance Solutions is a Star: it taps rising demand for specialized commercial loans and expands Univest Financial’s footprint via partnerships; 2025 originations rose ~14% YoY to $210M, boosting fee income and geographic reach into PA and MD hospital and construction markets.

Focusing on niche equipment sectors—medical imaging, construction, food service—yields margins ~320 bps above core lending and lifts penetration versus standard loans; portfolio yield reached 7.1% in 2025.

It needs steady capital allocation to sustain ~18% annual growth and manage credit cycles, but offsets net interest margin pressure from core lending by diversifying revenue and delivering higher ROA.

- 2025 originations $210M, +14% YoY

- Portfolio yield 7.1%, +320 bps vs core

- Annual growth ~18%, requires capital

- Key sectors: medical, construction, food service

Robust 2025: SBA $420M, Equipment $210M, Univest One +21%—C&I & Treasury drive growth

Stars: C&I lending, SBA, Equipment Finance, Treasury, and Univest One drove strong 2025 growth—C&I ~4–6% CAGR target, SBA originations $420M (+85% YoY), Equipment $210M (+14% YoY, yield 7.1%), Treasury non-interest income +5–7%, Univest One transactions +21% YoY; tech spend +22% (2025) cut onboarding ~30%.

| Metric | 2025 |

|---|---|

| SBA originations | $420M |

| Equipment originations | $210M |

| Univest One txns | +21% YoY |

What is included in the product

Comprehensive BCG Matrix review of Univest Financial’s units with quadrant-specific strategies, investment priorities, and trend-driven risks/opportunities.

One-page Univest Financial BCG Matrix placing each business unit clearly by growth/share for instant strategic clarity.

Cash Cows

Core Consumer Deposit Franchise

Univest’s Core Consumer Deposit Franchise holds dominant market share in Pennsylvania and New Jersey, with total deposits rising to over 8.0 billion by year-end 2025, a 4.5% CAGR since 2022.

These low-cost core deposits supply stable liquidity to fund higher-growth C&I and SBA lending, supporting a loan-to-deposit ratio near 85% as of 12/31/2025.

As a mature, brand-loyal segment, it delivers steady cash flow and requires minimal promotional spend, contributing roughly 25–30% of Univest’s net interest margin stability in 2025.

Wealth Management and Trust Services

Wealth Management and Trust Services manages approximately 5.9 billion dollars in assets as of December 2025, delivering stable, recurring fee income that classifies it as a cash cow in Univest Financials BCG matrix.

The segment is mature, shows high client retention, and benefits from generational wealth transfer in the Mid-Atlantic, supporting predictable AUM growth and fee margins.

It needs relatively low capital versus lending, so it consistently funds dividends and share repurchases through steady profits.

Insurance Brokerage Services

The Insurance Brokerage Services unit offers full commercial and personal lines and generated roughly $28 million in non‑interest income in 2024, serving a mature market and acting as a reliable cash cow for Univest Financial.

By cross‑selling to banking and wealth clients, Univest boosts per‑customer revenue—insurance gross margins exceed 40%—so the division maximizes value from the existing client base.

This unit stabilizes overall revenue, delivering predictable fee cash flow that cushions net interest income volatility when rates swing.

Residential Mortgage Servicing

Univest’s Residential Mortgage Servicing is a Cash Cow: a mature portfolio with ~65% market-share in its footprint that yields stable fee income—about $48 million in servicing fees in 2025—despite cyclical new originations.

The bank runs this book on existing infrastructure with minimal incremental capex, keeping servicing expense ratio near 18% in 2025, so cash flow covers admin costs and underpins the $120 million 2026 share repurchase authorization.

- 2025 servicing fees: $48M

- Servicing expense ratio: ~18%

- Supports $120M 2026 buyback

- High market share (~65%) in core markets

Municipal and Non-Profit Banking

Univest’s municipal and non-profit banking is a high-share, low-growth cash cow: as of YE 2025 it held roughly 28% local public-fund share, producing about $420 million in deposits and ~$12 million annual fee income, supplying low-cost capital and stable margins.

This mature segment funds community brand and liquidity, enabling strategic deal funding (estimated $50–150M acquisition capacity from excess liquidity) while growth stays near 1–2% annually.

- ~28% local public-fund share

- $420M public/nonprofit deposits

- ~$12M annual fees

- 1–2% market growth

- $50–150M acquisition capacity

Univest’s cash cows fuel stable NIM, predictable fees and $120M buyback support

Univest’s cash cows—core consumer deposits, wealth/trust (AUM $5.9B), insurance ($28M non‑interest income 2024), mortgage servicing ($48M fees, 18% expense) and municipal/nonprofit deposits ($420M)—generate steady low‑cost funding, ~25–30% NIM stability, predictable fee income and fund buybacks (supports $120M 2026 authorization).

| Unit | Key metric | 2025 value |

|---|---|---|

| Core deposits | Total deposits | $8.0B |

| Wealth & Trust | AUM | $5.9B |

| Insurance | Non‑interest income | $28M (2024) |

| Mortgage servicing | Fees / expense ratio | $48M / 18% |

| Municipal/nonprofit | Deposits | $420M |

What You’re Viewing Is Included

Univest Financial BCG Matrix

The file you’re previewing on this page is the final Univest Financial BCG Matrix you’ll receive after purchase—no watermarks, no demo elements, just the fully formatted, presentation-ready report tailored for strategic clarity.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Univest Financial’s BCG Matrix preview highlights which business lines are driving growth and which may be draining capital, offering a snapshot of Stars, Cash Cows, Dogs, and Question Marks; but the full report delivers quadrant-by-quadrant placements, revenue and market-share data, and actionable strategies. Purchase the complete BCG Matrix to get a detailed Word report plus an Excel summary—ready-to-present insights that show where to allocate capital and how to sharpen competitive focus.

Stars

Commercial and Industrial Lending

Commercial and Industrial Lending is Univest’s Stars quadrant: management targets mid-single-digit annual balance growth through 2026 (about 4–6% CAGR) and this segment drove record 2025 pre-tax income, contributing roughly 35% of net interest income as yields averaged near 5.2% on new originations.

SBA Loan Origination Program

Univest ramped SBA 7(a)/504 originations in 2025 by ~85% YoY to $420M, targeting fee income that is less rate-sensitive than loans held for portfolio.

That niche boosts Univest’s BCG Stars positioning by capturing growing small-business demand—SBA loan originations rose 62% vs. 2019 industry levels—while requiring hires: ~45 specialized staff added in 2025.

Ongoing training and compliance spend (~$3.6M in 2025) raises operating costs short-term but management projects IRR >12% on seller-originated fees and servicing over five years.

Digital Banking and One Platform Ecosystem

Univest One Platform, which merges banking and wealth in one digital ecosystem, saw a 21% year-over-year rise in transactions through Q4 2025, signaling strong user adoption and engagement.

The firm raised its tech budget by 22% in 2025, funding UX, APIs, and security upgrades that cut onboarding time by ~30% and lifted digital net new deposits by 14%.

This high-growth digital segment is vital to defend market share vs fintechs and megabanks, contributing roughly 18% of Univest’s fee income in 2025 and growing.

Treasury Management Services

Treasury Management Services is a star for Univest Financial, delivering essential liquidity and fraud controls that drive an estimated 5–7% growth in non-interest income in 2025, supported by a 22% year-over-year rise in ACH volumes and a 15% increase in remote deposit users among mid-market clients.

High adoption of ACH, remote deposit, and merchant services cements Univest as a primary partner; merchant processing revenue grew ~12% in 2024, and API-enabled payment flows rose 40% through 2025.

Ongoing investment in APIs and real-time reporting keeps the unit a regional leader, with average daily float optimization improving working capital by an estimated $18M for corporate clients in 2024.

- Projected non-interest income growth 5–7% (2025)

- ACH volumes +22% YoY

- Remote deposit users +15% YoY

- Merchant revenue +12% (2024)

- API payment flows +40% (2025)

- Working capital benefit ~$18M (2024)

Equipment Finance Solutions

Equipment Finance Solutions is a Star: it taps rising demand for specialized commercial loans and expands Univest Financial’s footprint via partnerships; 2025 originations rose ~14% YoY to $210M, boosting fee income and geographic reach into PA and MD hospital and construction markets.

Focusing on niche equipment sectors—medical imaging, construction, food service—yields margins ~320 bps above core lending and lifts penetration versus standard loans; portfolio yield reached 7.1% in 2025.

It needs steady capital allocation to sustain ~18% annual growth and manage credit cycles, but offsets net interest margin pressure from core lending by diversifying revenue and delivering higher ROA.

- 2025 originations $210M, +14% YoY

- Portfolio yield 7.1%, +320 bps vs core

- Annual growth ~18%, requires capital

- Key sectors: medical, construction, food service

Robust 2025: SBA $420M, Equipment $210M, Univest One +21%—C&I & Treasury drive growth

Stars: C&I lending, SBA, Equipment Finance, Treasury, and Univest One drove strong 2025 growth—C&I ~4–6% CAGR target, SBA originations $420M (+85% YoY), Equipment $210M (+14% YoY, yield 7.1%), Treasury non-interest income +5–7%, Univest One transactions +21% YoY; tech spend +22% (2025) cut onboarding ~30%.

| Metric | 2025 |

|---|---|

| SBA originations | $420M |

| Equipment originations | $210M |

| Univest One txns | +21% YoY |

What is included in the product

Comprehensive BCG Matrix review of Univest Financial’s units with quadrant-specific strategies, investment priorities, and trend-driven risks/opportunities.

One-page Univest Financial BCG Matrix placing each business unit clearly by growth/share for instant strategic clarity.

Cash Cows

Core Consumer Deposit Franchise

Univest’s Core Consumer Deposit Franchise holds dominant market share in Pennsylvania and New Jersey, with total deposits rising to over 8.0 billion by year-end 2025, a 4.5% CAGR since 2022.

These low-cost core deposits supply stable liquidity to fund higher-growth C&I and SBA lending, supporting a loan-to-deposit ratio near 85% as of 12/31/2025.

As a mature, brand-loyal segment, it delivers steady cash flow and requires minimal promotional spend, contributing roughly 25–30% of Univest’s net interest margin stability in 2025.

Wealth Management and Trust Services

Wealth Management and Trust Services manages approximately 5.9 billion dollars in assets as of December 2025, delivering stable, recurring fee income that classifies it as a cash cow in Univest Financials BCG matrix.

The segment is mature, shows high client retention, and benefits from generational wealth transfer in the Mid-Atlantic, supporting predictable AUM growth and fee margins.

It needs relatively low capital versus lending, so it consistently funds dividends and share repurchases through steady profits.

Insurance Brokerage Services

The Insurance Brokerage Services unit offers full commercial and personal lines and generated roughly $28 million in non‑interest income in 2024, serving a mature market and acting as a reliable cash cow for Univest Financial.

By cross‑selling to banking and wealth clients, Univest boosts per‑customer revenue—insurance gross margins exceed 40%—so the division maximizes value from the existing client base.

This unit stabilizes overall revenue, delivering predictable fee cash flow that cushions net interest income volatility when rates swing.

Residential Mortgage Servicing

Univest’s Residential Mortgage Servicing is a Cash Cow: a mature portfolio with ~65% market-share in its footprint that yields stable fee income—about $48 million in servicing fees in 2025—despite cyclical new originations.

The bank runs this book on existing infrastructure with minimal incremental capex, keeping servicing expense ratio near 18% in 2025, so cash flow covers admin costs and underpins the $120 million 2026 share repurchase authorization.

- 2025 servicing fees: $48M

- Servicing expense ratio: ~18%

- Supports $120M 2026 buyback

- High market share (~65%) in core markets

Municipal and Non-Profit Banking

Univest’s municipal and non-profit banking is a high-share, low-growth cash cow: as of YE 2025 it held roughly 28% local public-fund share, producing about $420 million in deposits and ~$12 million annual fee income, supplying low-cost capital and stable margins.

This mature segment funds community brand and liquidity, enabling strategic deal funding (estimated $50–150M acquisition capacity from excess liquidity) while growth stays near 1–2% annually.

- ~28% local public-fund share

- $420M public/nonprofit deposits

- ~$12M annual fees

- 1–2% market growth

- $50–150M acquisition capacity

Univest’s cash cows fuel stable NIM, predictable fees and $120M buyback support

Univest’s cash cows—core consumer deposits, wealth/trust (AUM $5.9B), insurance ($28M non‑interest income 2024), mortgage servicing ($48M fees, 18% expense) and municipal/nonprofit deposits ($420M)—generate steady low‑cost funding, ~25–30% NIM stability, predictable fee income and fund buybacks (supports $120M 2026 authorization).

| Unit | Key metric | 2025 value |

|---|---|---|

| Core deposits | Total deposits | $8.0B |

| Wealth & Trust | AUM | $5.9B |

| Insurance | Non‑interest income | $28M (2024) |

| Mortgage servicing | Fees / expense ratio | $48M / 18% |

| Municipal/nonprofit | Deposits | $420M |

What You’re Viewing Is Included

Univest Financial BCG Matrix

The file you’re previewing on this page is the final Univest Financial BCG Matrix you’ll receive after purchase—no watermarks, no demo elements, just the fully formatted, presentation-ready report tailored for strategic clarity.