United Overseas Bank Porter's Five Forces Analysis

From Overview to Strategy Blueprint

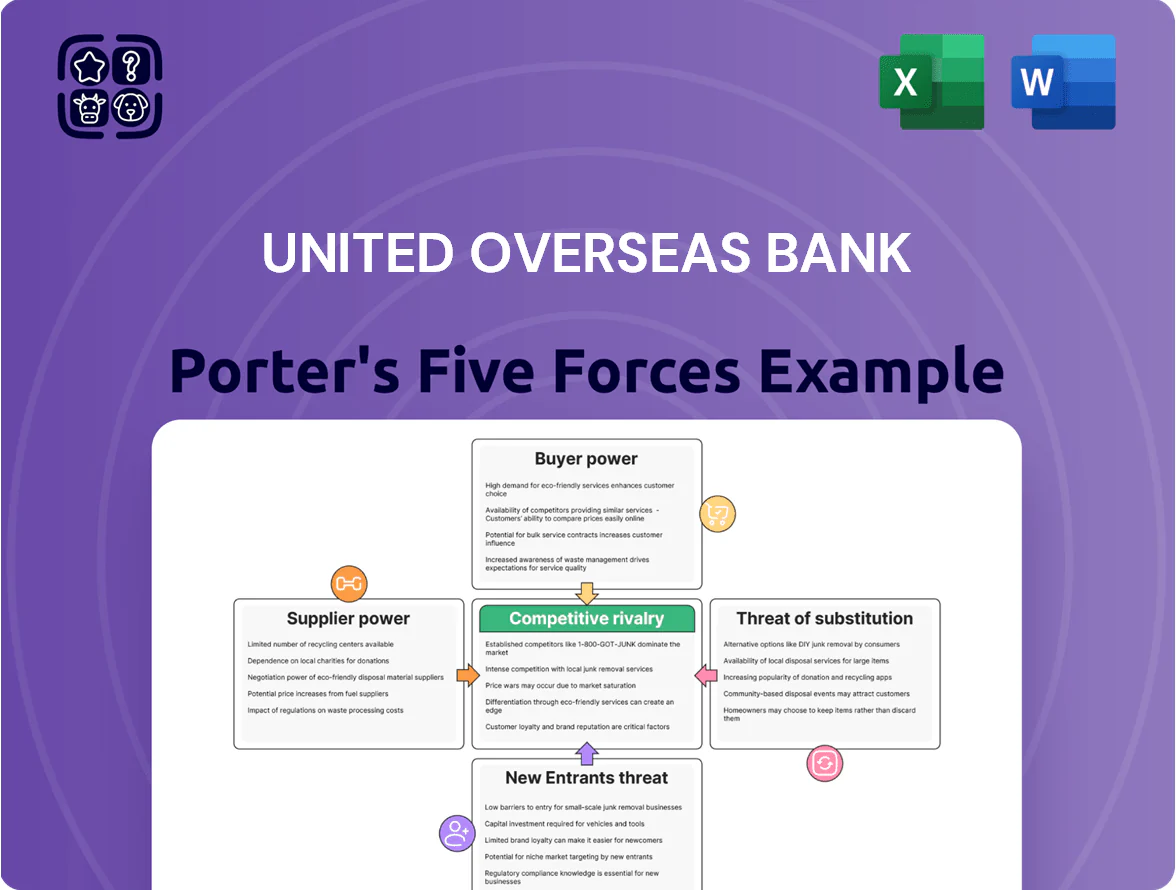

United Overseas Bank faces intense rivalry from regional giants and fintechs, moderate supplier power, high regulatory barriers limiting new entrants, growing buyer price sensitivity, and a manageable threat from substitutes like digital wallets; this snapshot highlights critical competitive pressures and strategic levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore United Overseas Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Regulatory and Central Bank Influence

The Monetary Authority of Singapore (MAS) and regional central banks act as primary suppliers of rules and liquidity standards; by late 2025 MAS set a minimum CET1 (common equity tier 1) target around 11.5% and Singapore policy rates lifted to 3.25%—benchmarks UOB must follow. This regulatory power constrains UOB’s product pricing, forces compliance with a 100%+ liquidity coverage ratio (LCR) and limits balance-sheet flexibility.

Technology and Cloud Infrastructure Providers

UOB depends heavily on third-party cloud and AI providers; Microsoft Azure and AWS supply critical services for digital transformation and cybersecurity, giving them strong supplier leverage. In 2024 UOB disclosed multi-year cloud deals covering core banking, with estimated migration costs above SGD 200–300 million and months of downtime risk—making switching prohibitively costly. This concentration raises vendor lock-in and operational dependency risks for UOB.

Retail and Institutional Depositors

Depositors are UOB’s primary capital suppliers for loans, and retail depositors individually have low bargaining power, but in 2025 a shift toward high-yield digital savings—average market rates up ~80 basis points higher than big-bank onshore rates—pressures UOB to keep retail deposit rates competitive to stem outflows.

Institutional depositors hold greater leverage: as of 2024 UOB reported ~S$190bn in non-retail deposits, so large treasury clients can negotiate pricing and terms, influencing UOB’s wholesale funding costs and liquidity management.

Specialized Human Capital

The supply of data scientists, cybersecurity experts, and wealth managers is tight in Singapore and SEA; Singapore reported a 12% year‑on‑year shortfall in tech talent in 2024, raising wage premiums.

High demand from banks and fintechs gives these pros leverage to demand higher pay and equity, pressuring UOB’s margins and hiring costs.

UOB needs ongoing retention spend—training, pay, stock—to protect IP; losing senior analysts can cost 6–12 months of product delays.

- 12% tech talent shortfall (Singapore, 2024)

- Higher wage premiums vs 2019: ~20–30%

- Retention reduces 6–12 month product delays

Global Debt Markets

UOB taps international bond markets to diversify funding and shape long-term capital, issuing about US$2.1bn in senior bonds in 2024–25 to extend maturities.

At end-2025, supplier leverage shifts with UOB’s A2/A- (Moody’s/S&P) ratings and global rates: a 100bp rise in benchmark yields would raise funding costs ~0.15% annualized, squeezing net interest margin.

Institutional investors and rating agencies set pricing and covenants; tougher macro conditions in 2025 increased new-issue spreads by ~40–60bp versus 2023, raising borrowing costs and pressuring profitability.

- 2024–25 issuance ~US$2.1bn

- Ratings A2/A- (Moody’s/S&P) at end-2025

- 100bp yield rise ≈ +0.15% funding cost

- 2025 new-issue spreads +40–60bp vs 2023

Regulatory, cloud and funding pressures amplify costs and constrain UOB’s margins

MAS regulation, cloud vendors (Microsoft/AWS) and depositors/institutional funders jointly give suppliers strong leverage over UOB—regulatory CET1/LCR constraints, multi-year cloud lock‑in (SGD 200–300m migration risk), ~S$190bn non‑retail deposits, and talent shortages (12% tech shortfall, 20–30% wage premium) push costs and limit pricing flexibility.

| Metric | Value |

|---|---|

| CET1 target (MAS, late‑2025) | ~11.5% |

| Cloud migration cost est. | SGD 200–300m |

| Non‑retail deposits (2024) | ~S$190bn |

| Tech talent shortfall (SG, 2024) | 12% |

| Wage premium vs 2019 | 20–30% |

| 2024–25 bond issuance | ~US$2.1bn |

What is included in the product

Tailored exclusively for United Overseas Bank, this Porter's Five Forces overview uncovers competitive intensity, customer and supplier leverage, entry barriers, substitute threats, and disruptive forces shaping its profitability and strategic positioning.

Clean, one-sheet Porter's Five Forces for United Overseas Bank—instantly gauge competitive pressure, tweak force levels with new data, and drop the ready visual into decks or dashboards for fast, boardroom-ready insight.

Customers Bargaining Power

Retail Banking Clients

Individual retail clients in 2025 have high transparency and low switching costs from digital apps; 88% of Singapore adults use mobile banking and 42% compared banks quarterly for rates, so customers can move deposits to competitors offering 3–50 bps higher yields or lower cross‑border fees. This pressures UOB to invest in UX and personalization—UOB reported 20% YoY digital active growth in 2024—to retain deposits and fee income.

Corporate and Institutional Clients

Small and Medium Enterprise Segment

UOB holds a strong SME footprint across ASEAN, serving ~1.2 million SMEs as of 2024, but customer bargaining power is rising as digital lenders and P2P platforms grew 28% YoY in SME loan originations in 2024, offering faster turnarounds and competitive rates.

SMEs now demand better pricing and service terms; UOB defends market share by using its regional branch network, cash-management scale, and specialized advisory services—UOB reported a 15% increase in SME advisory engagements in 2024—keeping churn contained.

Wealth Management Investors

High-net-worth individuals (HNWIs) wield strong bargaining power, demanding diversified portfolios and global, sophisticated advice; Asia-Pacific HNWI wealth hit US$12.7 trillion in 2024, raising stakes for retention.

These clients are mobile—about 28% moved assets to digital or boutique firms in 2023 when returns lagged—so UOB adds AI-driven insights and ESG (sustainable) offerings to retain flows.

- APAC HNWI wealth: US$12.7T (2024)

- 28% asset mobility to boutiques/digital (2023)

- UOB: AI analytics + ESG products to reduce churn

Digital Transparency and Comparison Tools

By end-2025, financial aggregators and comparison engines have pushed information symmetry to nearly 100% for Singapore customers, letting them compare UOB loan rates, credit-card rewards, and fixed-deposit yields in seconds; ACRA/IMDA data show over 78% smartphone penetration and 65% use of finance apps, speeding price-sensitive switching.

This transparency constrains UOB from aggressive price cuts—instant comparisons raise churn risk and compress net interest margin (NIM); UOB’s 2024 NIM was ~1.56%, so costly rate promotions would quickly erode margin and market share.

- ~100% info symmetry via aggregators by 2025

- 78% smartphone penetration; 65% finance app use

- UOB 2024 NIM ~1.56%—price cuts hurt margins

- Immediate customer churn risk on visible price gaps

UOB under NIM pressure: corporates drive NII, SMEs and HNWIs fuel digital & AI/ESG push

Customers wield high bargaining power: retail transparency and low switching raise churn risk; UOB 2024 NIM ~1.56% and 20% YoY digital active growth constrain price cuts. Corporates deliver ~40% of 2024 NII (≈SGD 4.8bn) and demand bespoke terms; SMEs (~1.2M clients) face rising digital lender competition (+28% SME originations 2024). HNWIs (APAC wealth US$12.7T 2024) are mobile, so UOB adds AI/ESG to retain flows.

| Metric | Value |

|---|---|

| UOB NIM (2024) | ~1.56% |

| Corporate share of NII (2024) | ~40% (SGD 4.8bn) |

| SMEs served (2024) | ~1.2M |

| SME digital origination growth (2024) | +28% YoY |

| APAC HNWI wealth (2024) | US$12.7T |

Full Version Awaits

United Overseas Bank Porter's Five Forces Analysis

This preview shows the exact United Overseas Bank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full document is professionally formatted, ready for download, and suitable for decision-making and presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

United Overseas Bank faces intense rivalry from regional giants and fintechs, moderate supplier power, high regulatory barriers limiting new entrants, growing buyer price sensitivity, and a manageable threat from substitutes like digital wallets; this snapshot highlights critical competitive pressures and strategic levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore United Overseas Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Regulatory and Central Bank Influence

The Monetary Authority of Singapore (MAS) and regional central banks act as primary suppliers of rules and liquidity standards; by late 2025 MAS set a minimum CET1 (common equity tier 1) target around 11.5% and Singapore policy rates lifted to 3.25%—benchmarks UOB must follow. This regulatory power constrains UOB’s product pricing, forces compliance with a 100%+ liquidity coverage ratio (LCR) and limits balance-sheet flexibility.

Technology and Cloud Infrastructure Providers

UOB depends heavily on third-party cloud and AI providers; Microsoft Azure and AWS supply critical services for digital transformation and cybersecurity, giving them strong supplier leverage. In 2024 UOB disclosed multi-year cloud deals covering core banking, with estimated migration costs above SGD 200–300 million and months of downtime risk—making switching prohibitively costly. This concentration raises vendor lock-in and operational dependency risks for UOB.

Retail and Institutional Depositors

Depositors are UOB’s primary capital suppliers for loans, and retail depositors individually have low bargaining power, but in 2025 a shift toward high-yield digital savings—average market rates up ~80 basis points higher than big-bank onshore rates—pressures UOB to keep retail deposit rates competitive to stem outflows.

Institutional depositors hold greater leverage: as of 2024 UOB reported ~S$190bn in non-retail deposits, so large treasury clients can negotiate pricing and terms, influencing UOB’s wholesale funding costs and liquidity management.

Specialized Human Capital

The supply of data scientists, cybersecurity experts, and wealth managers is tight in Singapore and SEA; Singapore reported a 12% year‑on‑year shortfall in tech talent in 2024, raising wage premiums.

High demand from banks and fintechs gives these pros leverage to demand higher pay and equity, pressuring UOB’s margins and hiring costs.

UOB needs ongoing retention spend—training, pay, stock—to protect IP; losing senior analysts can cost 6–12 months of product delays.

- 12% tech talent shortfall (Singapore, 2024)

- Higher wage premiums vs 2019: ~20–30%

- Retention reduces 6–12 month product delays

Global Debt Markets

UOB taps international bond markets to diversify funding and shape long-term capital, issuing about US$2.1bn in senior bonds in 2024–25 to extend maturities.

At end-2025, supplier leverage shifts with UOB’s A2/A- (Moody’s/S&P) ratings and global rates: a 100bp rise in benchmark yields would raise funding costs ~0.15% annualized, squeezing net interest margin.

Institutional investors and rating agencies set pricing and covenants; tougher macro conditions in 2025 increased new-issue spreads by ~40–60bp versus 2023, raising borrowing costs and pressuring profitability.

- 2024–25 issuance ~US$2.1bn

- Ratings A2/A- (Moody’s/S&P) at end-2025

- 100bp yield rise ≈ +0.15% funding cost

- 2025 new-issue spreads +40–60bp vs 2023

Regulatory, cloud and funding pressures amplify costs and constrain UOB’s margins

MAS regulation, cloud vendors (Microsoft/AWS) and depositors/institutional funders jointly give suppliers strong leverage over UOB—regulatory CET1/LCR constraints, multi-year cloud lock‑in (SGD 200–300m migration risk), ~S$190bn non‑retail deposits, and talent shortages (12% tech shortfall, 20–30% wage premium) push costs and limit pricing flexibility.

| Metric | Value |

|---|---|

| CET1 target (MAS, late‑2025) | ~11.5% |

| Cloud migration cost est. | SGD 200–300m |

| Non‑retail deposits (2024) | ~S$190bn |

| Tech talent shortfall (SG, 2024) | 12% |

| Wage premium vs 2019 | 20–30% |

| 2024–25 bond issuance | ~US$2.1bn |

What is included in the product

Tailored exclusively for United Overseas Bank, this Porter's Five Forces overview uncovers competitive intensity, customer and supplier leverage, entry barriers, substitute threats, and disruptive forces shaping its profitability and strategic positioning.

Clean, one-sheet Porter's Five Forces for United Overseas Bank—instantly gauge competitive pressure, tweak force levels with new data, and drop the ready visual into decks or dashboards for fast, boardroom-ready insight.

Customers Bargaining Power

Retail Banking Clients

Individual retail clients in 2025 have high transparency and low switching costs from digital apps; 88% of Singapore adults use mobile banking and 42% compared banks quarterly for rates, so customers can move deposits to competitors offering 3–50 bps higher yields or lower cross‑border fees. This pressures UOB to invest in UX and personalization—UOB reported 20% YoY digital active growth in 2024—to retain deposits and fee income.

Corporate and Institutional Clients

Small and Medium Enterprise Segment

UOB holds a strong SME footprint across ASEAN, serving ~1.2 million SMEs as of 2024, but customer bargaining power is rising as digital lenders and P2P platforms grew 28% YoY in SME loan originations in 2024, offering faster turnarounds and competitive rates.

SMEs now demand better pricing and service terms; UOB defends market share by using its regional branch network, cash-management scale, and specialized advisory services—UOB reported a 15% increase in SME advisory engagements in 2024—keeping churn contained.

Wealth Management Investors

High-net-worth individuals (HNWIs) wield strong bargaining power, demanding diversified portfolios and global, sophisticated advice; Asia-Pacific HNWI wealth hit US$12.7 trillion in 2024, raising stakes for retention.

These clients are mobile—about 28% moved assets to digital or boutique firms in 2023 when returns lagged—so UOB adds AI-driven insights and ESG (sustainable) offerings to retain flows.

- APAC HNWI wealth: US$12.7T (2024)

- 28% asset mobility to boutiques/digital (2023)

- UOB: AI analytics + ESG products to reduce churn

Digital Transparency and Comparison Tools

By end-2025, financial aggregators and comparison engines have pushed information symmetry to nearly 100% for Singapore customers, letting them compare UOB loan rates, credit-card rewards, and fixed-deposit yields in seconds; ACRA/IMDA data show over 78% smartphone penetration and 65% use of finance apps, speeding price-sensitive switching.

This transparency constrains UOB from aggressive price cuts—instant comparisons raise churn risk and compress net interest margin (NIM); UOB’s 2024 NIM was ~1.56%, so costly rate promotions would quickly erode margin and market share.

- ~100% info symmetry via aggregators by 2025

- 78% smartphone penetration; 65% finance app use

- UOB 2024 NIM ~1.56%—price cuts hurt margins

- Immediate customer churn risk on visible price gaps

UOB under NIM pressure: corporates drive NII, SMEs and HNWIs fuel digital & AI/ESG push

Customers wield high bargaining power: retail transparency and low switching raise churn risk; UOB 2024 NIM ~1.56% and 20% YoY digital active growth constrain price cuts. Corporates deliver ~40% of 2024 NII (≈SGD 4.8bn) and demand bespoke terms; SMEs (~1.2M clients) face rising digital lender competition (+28% SME originations 2024). HNWIs (APAC wealth US$12.7T 2024) are mobile, so UOB adds AI/ESG to retain flows.

| Metric | Value |

|---|---|

| UOB NIM (2024) | ~1.56% |

| Corporate share of NII (2024) | ~40% (SGD 4.8bn) |

| SMEs served (2024) | ~1.2M |

| SME digital origination growth (2024) | +28% YoY |

| APAC HNWI wealth (2024) | US$12.7T |

Full Version Awaits

United Overseas Bank Porter's Five Forces Analysis

This preview shows the exact United Overseas Bank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full document is professionally formatted, ready for download, and suitable for decision-making and presentation.