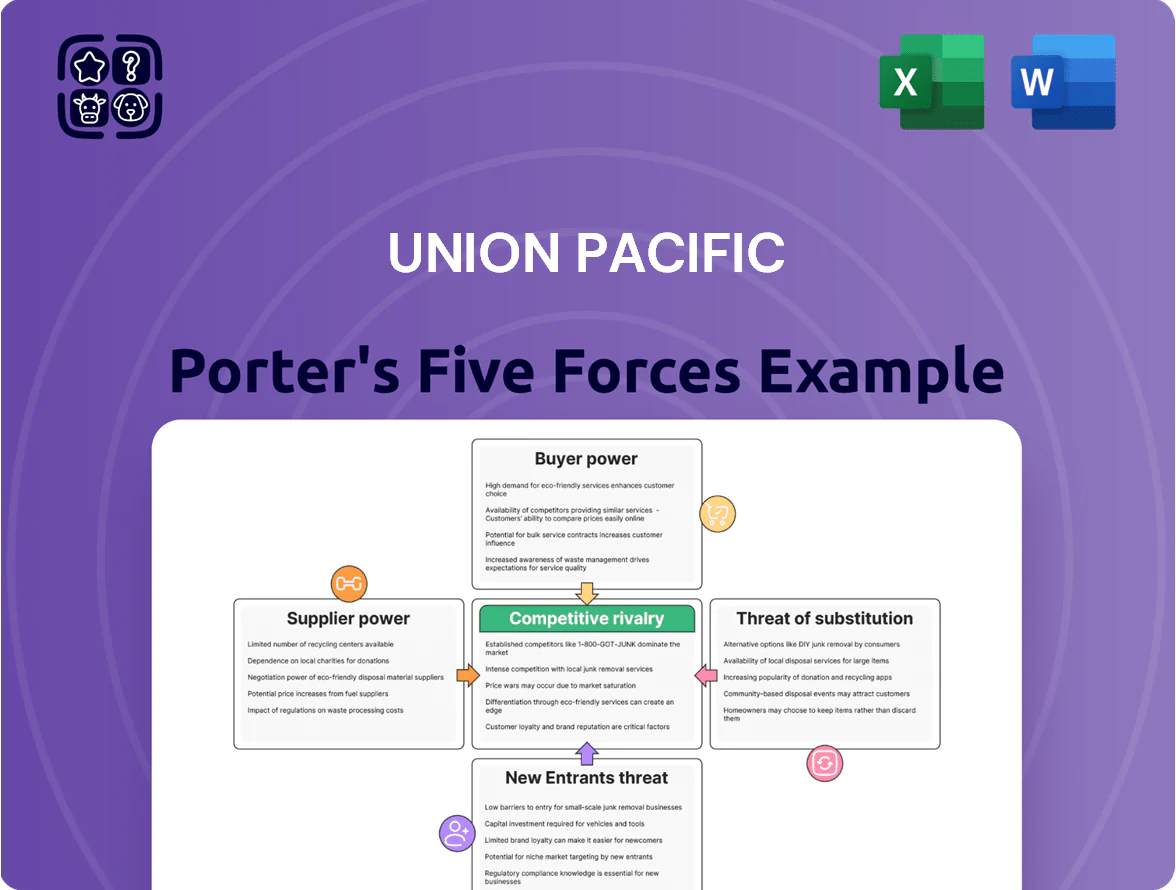

Union Pacific Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Union Pacific operates in a capital-intensive, high-barrier freight rail industry where supplier and buyer power are moderate, rivalry is intense among regional carriers and intermodal providers, and threats from new entrants and substitutes remain low to medium due to infrastructure costs and modal competition.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Union Pacific’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of specialized locomotive manufacturers

The market for high-efficiency locomotives is concentrated among a few global makers—GE Transportation (Wabtec), Siemens, and CRRC—giving suppliers strong price leverage; Union Pacific paid about $1.2–1.6 million per Tier 4 locomotive in recent contracts (2023–2025), limiting negotiation room. These vendors supply emissions-control tech needed to meet 2026 carbon rules and UP’s 2030 targets, and UP relies on them for new units and long-term maintenance, creating supplier dependency and cost exposure.

Influence of unionized labor organizations

Volatility in fuel and energy markets

Union Pacific consumes ~1.7 billion gallons of diesel annually, so fuel-price swings set by a concentrated oil sector (top 10 majors control ~60% of global supply) materially raise operating costs.

UP uses fuel surcharges—recouping roughly 40–60% of diesel cost moves since 2020—but surcharges lag markets and compress margins when crude spikes.

Transition to renewable diesel and SAF (sustainable aviation fuel) creates new supplier concentration: a handful of producers supply >70% of US renewable diesel capacity, raising strategic dependence and capex for fuel-compatibility.

Concentration of rail and steel infrastructure providers

The maintenance of 32,000+ route miles on Union Pacific requires specialized steel rails and concrete ties supplied by a small set of industrial vendors, giving suppliers strong pricing leverage.

High barriers to entry in steel (capital intensity, blast furnace scale) and 2024 steel price volatility—U.S. domestic HRC up ~18% YoY in 2024—leave UP with few short-term alternatives when raw-material costs rise.

Technical specs and supplier certification narrow options further: only a handful of certified vendors meet FRA (Federal Railroad Administration) standards and UP’s internal specs, increasing supplier bargaining power.

- 32,000+ route miles depend on limited suppliers

- 2024 U.S. hot-rolled coil prices +18% YoY

- High-capex steel barriers; few certified vendors

Technological and software vendor lock-in

The shift to autonomous systems and precision scheduled railroading ties Union Pacific to niche vendors that hold proprietary software, creating supplier power via long-term licenses and costly platform migration—estimated switching costs can exceed $50–150 million for large Class I railroads per major system in 2024–25.

As Union Pacific’s data-driven operations expand in 2025 (freight telemetry, predictive maintenance, dispatch optimization), vendor importance rises; 60–70% of new digital projects rely on third-party modules, increasing exposure to price hikes and roadmap lock-in.

- Proprietary software reliance raises switching costs: $50–150M

- Long-term licenses limit bargaining and flexibility

- 60–70% of 2025 digital projects use third-party modules

- Vendor roadmaps shape UP operational strategy and costs

Supplier Concentration Squeezes Union Pacific: High Capex, Fuel & Union Costs

Suppliers exert high bargaining power: few locomotive, rail-steel, fuel, and niche-software vendors drive prices and switching costs (Tier 4 loco $1.2–1.6M each; HRC +18% YoY 2024; diesel ~1.7B gal/yr; software switch $50–150M). Union Pacific faces supplier concentration across capital assets, fuel, labor unions (~60% unionized) and certified vendors, compressing margins and raising capex/operating risk.

| Item | 2024–25 |

|---|---|

| Tier 4 loco price | $1.2–1.6M |

| Diesel use | ~1.7B gal/yr |

| HRC change | +18% YoY |

| Unionized workforce | ~60% |

| SW switching cost | $50–150M |

What is included in the product

Tailored Porter's Five Forces analysis for Union Pacific, uncovering competitive dynamics, supplier and buyer power, entry barriers, substitute threats, and strategic vulnerabilities that shape pricing and profitability.

Clear, one-sheet Porter's Five Forces for Union Pacific—instantly spot where competitive pressure hits hardest and use the clean radar chart to guide strategic moves or investor briefs.

Customers Bargaining Power

Concentration of large volume shippers

Major industrial clients in automotive, chemical, and agriculture account for roughly 40–50% of Union Pacific’s revenue (2024 freight mix), giving them strong leverage to demand volume discounts and bespoke service-level agreements; a single large shipper can represent millions of annual carloads, forcing UP to offer lower per-unit rates. These customers can shift traffic to truck or barge—making UP keep pricing competitive and service flexible to protect margins.

Availability of intermodal shipping alternatives

In intermodal, customers can switch between Union Pacific rail and long-haul trucking based on price and speed, capping rail rates for consumer goods and retail inventory.

Per ATRI and USDOT estimates to end-2025, trucking costs fell ~6% real-year-over-year and autonomous pilot deployments cut marginal over-the-road costs by ~8–12%, boosting truck competitiveness.

As a result, UP faces stronger price sensitivity and shorter contract durations as shippers flex to the lowest-cost, quickest option.

Price sensitivity in the bulk commodity market

Shippers of low‑margin commodities such as thermal coal and some grains are highly price sensitive; a 10% freight increase can erase export margins—U.S. coal exports fell ~32% from 2014 to 2023, showing vulnerability. If rail rates push landed costs above global competitors, volume can drop to zero, giving producers indirect leverage in contract renewals. In 2024 negotiations, large agricultural coops pushed for rate caps after rail tariffs rose ~7% year‑over‑year.

Impact of customer supply chain vertical integration

Transparency and digital freight matching platforms

The rise of digital freight-matching platforms (real-time booking, rate transparency) gave shippers immediate visibility into market rates and carrier KPIs; platforms like Uber Freight and Convoy reported combined US spot-market share around 12–15% by 2024, shrinking information gaps.

Smaller shippers now compare rail, truck, and intermodal options quickly and press for better contracts, raising price pressure on Union Pacific’s legacy bargaining edge.

As rate-discovery improves, Union Pacific’s historical info advantage erodes, increasing customer leverage and shortening negotiation cycles.

- Digital platforms ~12–15% US spot share (2024)

- Real-time rate visibility cuts negotiation time by weeks

- Smaller shippers can demand better terms

Shippers Hold Leverage as Trucking Costs Fall and Digital Platforms Threaten Contracts

Large industrial shippers (40–50% revenue, 2024) wield high price leverage; single clients = millions of carloads, forcing discounts. Trucking cost decline (~6% real, 2025) and autonomous pilots (8–12% marginal savings) plus digital platforms (12–15% spot share, 2024) raise switching threat and shorten contracts; UP counters with faster dwell (32 hrs, 2024) and visibility.

| Metric | Value |

|---|---|

| Shipper revenue share | 40–50% (2024) |

| Terminal dwell | 32 hrs (2024) |

| Truck cost change | -6% real (2025) |

| Digital spot share | 12–15% (2024) |

Same Document Delivered

Union Pacific Porter's Five Forces Analysis

This preview shows the exact Union Pacific Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally written file you’ll be able to download and use the moment you buy, fully formatted and ready for your needs.

No mockups or samples: this is the final deliverable, the precise analysis you’ll get instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Union Pacific operates in a capital-intensive, high-barrier freight rail industry where supplier and buyer power are moderate, rivalry is intense among regional carriers and intermodal providers, and threats from new entrants and substitutes remain low to medium due to infrastructure costs and modal competition.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Union Pacific’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of specialized locomotive manufacturers

The market for high-efficiency locomotives is concentrated among a few global makers—GE Transportation (Wabtec), Siemens, and CRRC—giving suppliers strong price leverage; Union Pacific paid about $1.2–1.6 million per Tier 4 locomotive in recent contracts (2023–2025), limiting negotiation room. These vendors supply emissions-control tech needed to meet 2026 carbon rules and UP’s 2030 targets, and UP relies on them for new units and long-term maintenance, creating supplier dependency and cost exposure.

Influence of unionized labor organizations

Volatility in fuel and energy markets

Union Pacific consumes ~1.7 billion gallons of diesel annually, so fuel-price swings set by a concentrated oil sector (top 10 majors control ~60% of global supply) materially raise operating costs.

UP uses fuel surcharges—recouping roughly 40–60% of diesel cost moves since 2020—but surcharges lag markets and compress margins when crude spikes.

Transition to renewable diesel and SAF (sustainable aviation fuel) creates new supplier concentration: a handful of producers supply >70% of US renewable diesel capacity, raising strategic dependence and capex for fuel-compatibility.

Concentration of rail and steel infrastructure providers

The maintenance of 32,000+ route miles on Union Pacific requires specialized steel rails and concrete ties supplied by a small set of industrial vendors, giving suppliers strong pricing leverage.

High barriers to entry in steel (capital intensity, blast furnace scale) and 2024 steel price volatility—U.S. domestic HRC up ~18% YoY in 2024—leave UP with few short-term alternatives when raw-material costs rise.

Technical specs and supplier certification narrow options further: only a handful of certified vendors meet FRA (Federal Railroad Administration) standards and UP’s internal specs, increasing supplier bargaining power.

- 32,000+ route miles depend on limited suppliers

- 2024 U.S. hot-rolled coil prices +18% YoY

- High-capex steel barriers; few certified vendors

Technological and software vendor lock-in

The shift to autonomous systems and precision scheduled railroading ties Union Pacific to niche vendors that hold proprietary software, creating supplier power via long-term licenses and costly platform migration—estimated switching costs can exceed $50–150 million for large Class I railroads per major system in 2024–25.

As Union Pacific’s data-driven operations expand in 2025 (freight telemetry, predictive maintenance, dispatch optimization), vendor importance rises; 60–70% of new digital projects rely on third-party modules, increasing exposure to price hikes and roadmap lock-in.

- Proprietary software reliance raises switching costs: $50–150M

- Long-term licenses limit bargaining and flexibility

- 60–70% of 2025 digital projects use third-party modules

- Vendor roadmaps shape UP operational strategy and costs

Supplier Concentration Squeezes Union Pacific: High Capex, Fuel & Union Costs

Suppliers exert high bargaining power: few locomotive, rail-steel, fuel, and niche-software vendors drive prices and switching costs (Tier 4 loco $1.2–1.6M each; HRC +18% YoY 2024; diesel ~1.7B gal/yr; software switch $50–150M). Union Pacific faces supplier concentration across capital assets, fuel, labor unions (~60% unionized) and certified vendors, compressing margins and raising capex/operating risk.

| Item | 2024–25 |

|---|---|

| Tier 4 loco price | $1.2–1.6M |

| Diesel use | ~1.7B gal/yr |

| HRC change | +18% YoY |

| Unionized workforce | ~60% |

| SW switching cost | $50–150M |

What is included in the product

Tailored Porter's Five Forces analysis for Union Pacific, uncovering competitive dynamics, supplier and buyer power, entry barriers, substitute threats, and strategic vulnerabilities that shape pricing and profitability.

Clear, one-sheet Porter's Five Forces for Union Pacific—instantly spot where competitive pressure hits hardest and use the clean radar chart to guide strategic moves or investor briefs.

Customers Bargaining Power

Concentration of large volume shippers

Major industrial clients in automotive, chemical, and agriculture account for roughly 40–50% of Union Pacific’s revenue (2024 freight mix), giving them strong leverage to demand volume discounts and bespoke service-level agreements; a single large shipper can represent millions of annual carloads, forcing UP to offer lower per-unit rates. These customers can shift traffic to truck or barge—making UP keep pricing competitive and service flexible to protect margins.

Availability of intermodal shipping alternatives

In intermodal, customers can switch between Union Pacific rail and long-haul trucking based on price and speed, capping rail rates for consumer goods and retail inventory.

Per ATRI and USDOT estimates to end-2025, trucking costs fell ~6% real-year-over-year and autonomous pilot deployments cut marginal over-the-road costs by ~8–12%, boosting truck competitiveness.

As a result, UP faces stronger price sensitivity and shorter contract durations as shippers flex to the lowest-cost, quickest option.

Price sensitivity in the bulk commodity market

Shippers of low‑margin commodities such as thermal coal and some grains are highly price sensitive; a 10% freight increase can erase export margins—U.S. coal exports fell ~32% from 2014 to 2023, showing vulnerability. If rail rates push landed costs above global competitors, volume can drop to zero, giving producers indirect leverage in contract renewals. In 2024 negotiations, large agricultural coops pushed for rate caps after rail tariffs rose ~7% year‑over‑year.

Impact of customer supply chain vertical integration

Transparency and digital freight matching platforms

The rise of digital freight-matching platforms (real-time booking, rate transparency) gave shippers immediate visibility into market rates and carrier KPIs; platforms like Uber Freight and Convoy reported combined US spot-market share around 12–15% by 2024, shrinking information gaps.

Smaller shippers now compare rail, truck, and intermodal options quickly and press for better contracts, raising price pressure on Union Pacific’s legacy bargaining edge.

As rate-discovery improves, Union Pacific’s historical info advantage erodes, increasing customer leverage and shortening negotiation cycles.

- Digital platforms ~12–15% US spot share (2024)

- Real-time rate visibility cuts negotiation time by weeks

- Smaller shippers can demand better terms

Shippers Hold Leverage as Trucking Costs Fall and Digital Platforms Threaten Contracts

Large industrial shippers (40–50% revenue, 2024) wield high price leverage; single clients = millions of carloads, forcing discounts. Trucking cost decline (~6% real, 2025) and autonomous pilots (8–12% marginal savings) plus digital platforms (12–15% spot share, 2024) raise switching threat and shorten contracts; UP counters with faster dwell (32 hrs, 2024) and visibility.

| Metric | Value |

|---|---|

| Shipper revenue share | 40–50% (2024) |

| Terminal dwell | 32 hrs (2024) |

| Truck cost change | -6% real (2025) |

| Digital spot share | 12–15% (2024) |

Same Document Delivered

Union Pacific Porter's Five Forces Analysis

This preview shows the exact Union Pacific Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally written file you’ll be able to download and use the moment you buy, fully formatted and ready for your needs.

No mockups or samples: this is the final deliverable, the precise analysis you’ll get instantly after payment.