Uponor Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

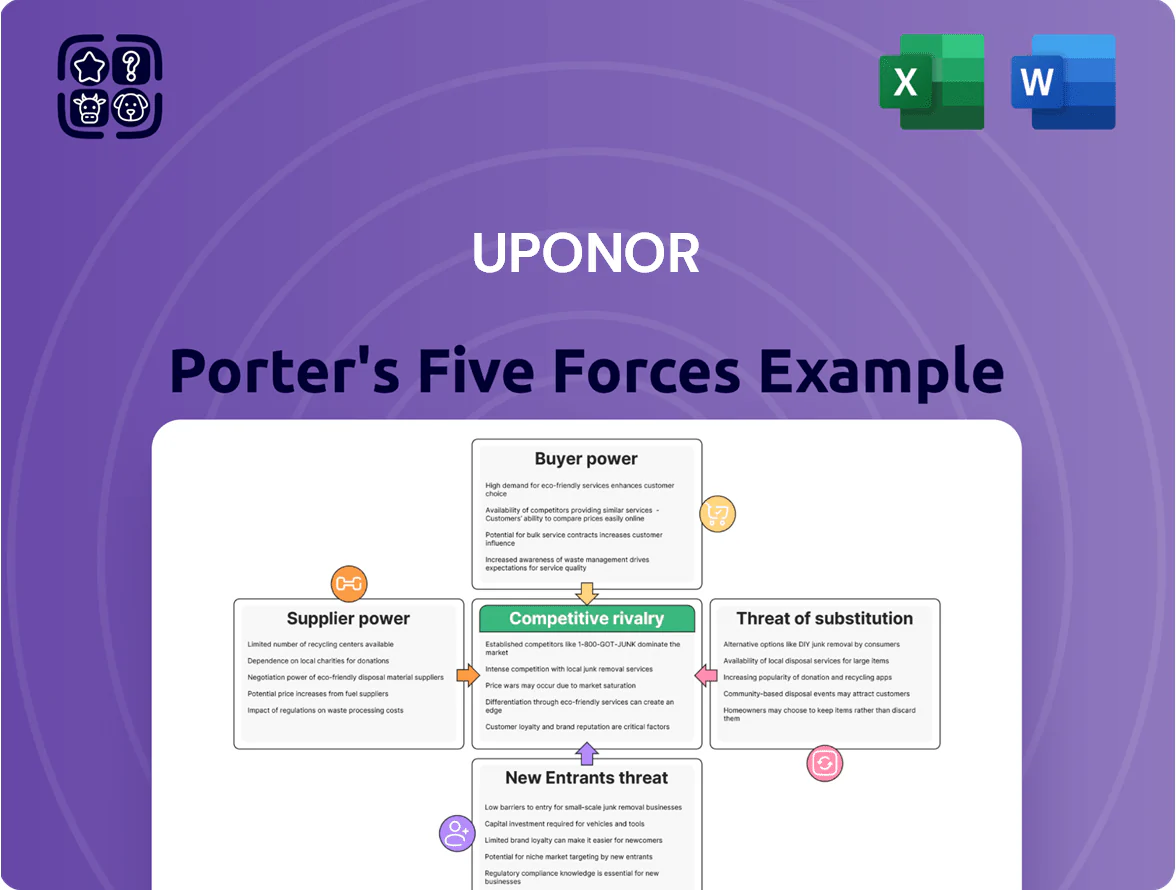

Uponor faces moderate supplier power and steady buyer leverage, with barriers to entry shaped by technical standards and distribution networks; rivalry is intense amid consolidation and substitution risk from alternative piping systems. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Uponor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Price Volatility

Production of PEX and multi-layer pipes hinges on plastic resins and petrochemical derivatives, whose suppliers—major global oil and chemical conglomerates—wield strong pricing power over manufacturers like Uponor. By end-2025, Brent oil averaged ~86 USD/barrel and ethylene spot prices rose ~12% year-to-date, keeping input-cost volatility high and squeezing margins. If feedstock costs jump 10%, gross margins for pipe makers can fall ~3–5 percentage points.

Consolidation of Petrochemical Providers

The supply of high-grade polymers is concentrated: the top 5 petrochemical firms (eg BASF, LyondellBasell, SABIC) control ~45% of global specialty polymer capacity as of 2025, limiting Uponor’s supplier switching without risking quality or lead-time shocks. High technical specs for potable-water pipes (NSF/ANSI 61, WRAS) shrink qualified vendors to a small subset, preserving supplier price and delivery leverage and raising risk of margin pressure from input-cost spikes.

Impact of Georg Fischer Integration

Post-integration with Georg Fischer, Uponor gains procurement scale: combined 2024 group purchasing reached about EUR 3.2 billion, enabling volume discounts and 4–6% expected COGS (cost of goods sold) savings in 2025 vs standalone forecasts.

Georg Fischer backing raises supplier bargaining power: longer-term contracts and joint sourcing reduce price volatility and cut lead times by an estimated 10–15%.

Strategic supplier partnerships secure critical resin and copper supply, lowering supply disruption risk and smoothing input-cost pass-through to margins.

Specialized Component Requirements

Specialized brass and metal fittings and manifolds make up ~15–20% of Uponor's BOM cost and come from niche suppliers holding patents or unique tooling, so they are hard to replace quickly and carry moderate bargaining power.

These components are critical for system certification (e.g., UPC/NSF) and failure risks, so suppliers can demand price premia; in 2024 industry reports show supplier lead-times of 12–20 weeks for patented parts.

- 15–20% of BOM cost

- 12–20 week lead-times

- Patents/unique tooling raise switching cost

Sustainability and ESG Compliance

Suppliers face tighter scrutiny as Uponor targets net-zero by 2025, pushing demand for certified sustainable materials and recycled resins; in 2024, 42% of polymer purchases met recycled-content specs, up from 18% in 2021.

That narrows the supplier pool, raising bargaining power for green-certified vendors and risking price/lead-time pressure where compliant materials are scarce.

- 2025 net-zero deadline raises supplier ESG bar

- 42% recycled-content polymer purchases in 2024

- Smaller compliant supplier pool increases vendor leverage

- Risk: higher prices and longer lead times for certified materials

Supplier power tightens: feedstock shocks, patents & green specs squeeze margins

Suppliers hold moderate-to-strong power: concentrated petrochemical supply (top-5 ~45% capacity) and patented fittings (15–20% BOM; 12–20 week lead-times) raise switching costs; Brent ~86 USD/bbl (end-2025) and +12% ethylene YTD pressure margins (10% feedstock rise → ~3–5ppt gross margin hit). Georg Fischer merger (EUR 3.2bn procurement 2024) cuts COGS ~4–6% and lead-times 10–15%, but green specs (42% recycled polymers 2024) narrow vendor pool.

| Metric | 2024/2025 |

|---|---|

| Top-5 polymer share | ~45% |

| Brent (end-2025) | ~86 USD/bbl |

| Ethylene YTD change | +12% |

| Feedstock shock impact | 10% → −3–5ppt GM |

| Procurement scale | EUR 3.2bn (2024) |

| Recycled polymer share | 42% (2024) |

What is included in the product

Tailored exclusively for Uponor, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position, with strategic insights for investors and management.

Clear, one-sheet Porter’s Five Forces for Uponor—instantly visualize competitive pressure and strategic levers to ease boardroom decisions and prioritize actions.

Customers Bargaining Power

Concentration of Wholesale Distribution

A large share of Uponor’s sales flows through a few major plumbing/HVAC wholesalers that control regional markets; in 2024 these top 10 distributors accounted for roughly 38% of company channel sales. These intermediaries press for higher rebates and exclusive marketing support, squeezing gross margins by an estimated 120–180 basis points in recent years. By late 2025 further consolidation lifted volume leverage—top accounts now represent ~45% of channel volumes, increasing their bargaining power.

Low Switching Costs for Standard Applications

In residential construction, basic piping and underfloor heating are often commodities, so installers switch brands for lower prices with little tech friction; industry surveys show 62% of contractors rank price as top buying factor in 2024. This price sensitivity meant Uponor’s 2024 Americas margin pressure—gross margin down ~140 bps—forced focus on service, digital tools, and brand reliability to retain loyalty.

Influence of Specifiers and Engineers

Architects and MEP engineers specify Uponor products early on for commercial projects, and their preference for Uponor’s technical performance and BIM (building information modeling) support reduces end-customer bargaining power by locking choices before procurement. Uponor reported in 2024 that 42% of its commercial project wins cited BIM integration and design software as a key factor, strengthening specifier-driven demand. Providing detailed technical data and design tools raises switching costs for owners and contractors and helps secure higher-margin projects.

Growth of Direct-to-Contractor Digital Platforms

The rise of e-commerce and digital procurement lets small contractors compare prices and availability in real time, raising price pressure on Uponor as buyers spot cheaper alternatives and promo deals; by 2024, 46% of US construction firms used online procurement platforms, up from 31% in 2019 (Dodge Data & Analytics).

To counter this transparency, Uponor invested in a digital ecosystem—supplier portals, stock visibility, and installation support—aiming to justify a premium and protect margins: reported digital sales/support initiatives targeted a 3–5% uplift in ASP (average selling price) in 2024.

Demand for Integrated Energy Systems

Modern buyers favor integrated systems combining radiant heating, heat pumps, and smart controls, shifting purchasing from parts to full-system performance; this raises customer leverage to demand interoperability and 10–15 year warranties.

In 2025 high-efficiency buildings account for ~28% of European retrofit spend and 34% of US new-build HVAC budgets, so Uponor must certify compatibility and offer longer-term service contracts to stay a preferred partner.

- Customers demand system-level performance, not components

- Interoperability and long warranties increase bargaining power

- ~28% EU retrofit, ~34% US new-build HVAC market relevance

- Uponor must certify integration and extend service terms

Rising distributor clout, price-driven contractors and BIM shape margin squeeze

Customers hold high bargaining power: top 10 distributors ~45% channel volumes (late 2025), press rebates cutting gross margin ~120–180 bps; 62% contractors cite price as top factor (2024); 46% US firms use online procurement (2024), raising transparency; 42% of commercial wins cited BIM support (2024), which reduces switching and protects margins.

| Metric | Value |

|---|---|

| Top-10 distributor share | ~45% (late 2025) |

| Contractors prioritizing price | 62% (2024) |

| Online procurement use | 46% US (2024) |

| Commercial wins citing BIM | 42% (2024) |

| Estimated margin hit | 120–180 bps |

Preview Before You Purchase

Uponor Porter's Five Forces Analysis

This preview shows the exact Uponor Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; it’s fully formatted and ready to download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Uponor faces moderate supplier power and steady buyer leverage, with barriers to entry shaped by technical standards and distribution networks; rivalry is intense amid consolidation and substitution risk from alternative piping systems. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Uponor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Price Volatility

Production of PEX and multi-layer pipes hinges on plastic resins and petrochemical derivatives, whose suppliers—major global oil and chemical conglomerates—wield strong pricing power over manufacturers like Uponor. By end-2025, Brent oil averaged ~86 USD/barrel and ethylene spot prices rose ~12% year-to-date, keeping input-cost volatility high and squeezing margins. If feedstock costs jump 10%, gross margins for pipe makers can fall ~3–5 percentage points.

Consolidation of Petrochemical Providers

The supply of high-grade polymers is concentrated: the top 5 petrochemical firms (eg BASF, LyondellBasell, SABIC) control ~45% of global specialty polymer capacity as of 2025, limiting Uponor’s supplier switching without risking quality or lead-time shocks. High technical specs for potable-water pipes (NSF/ANSI 61, WRAS) shrink qualified vendors to a small subset, preserving supplier price and delivery leverage and raising risk of margin pressure from input-cost spikes.

Impact of Georg Fischer Integration

Post-integration with Georg Fischer, Uponor gains procurement scale: combined 2024 group purchasing reached about EUR 3.2 billion, enabling volume discounts and 4–6% expected COGS (cost of goods sold) savings in 2025 vs standalone forecasts.

Georg Fischer backing raises supplier bargaining power: longer-term contracts and joint sourcing reduce price volatility and cut lead times by an estimated 10–15%.

Strategic supplier partnerships secure critical resin and copper supply, lowering supply disruption risk and smoothing input-cost pass-through to margins.

Specialized Component Requirements

Specialized brass and metal fittings and manifolds make up ~15–20% of Uponor's BOM cost and come from niche suppliers holding patents or unique tooling, so they are hard to replace quickly and carry moderate bargaining power.

These components are critical for system certification (e.g., UPC/NSF) and failure risks, so suppliers can demand price premia; in 2024 industry reports show supplier lead-times of 12–20 weeks for patented parts.

- 15–20% of BOM cost

- 12–20 week lead-times

- Patents/unique tooling raise switching cost

Sustainability and ESG Compliance

Suppliers face tighter scrutiny as Uponor targets net-zero by 2025, pushing demand for certified sustainable materials and recycled resins; in 2024, 42% of polymer purchases met recycled-content specs, up from 18% in 2021.

That narrows the supplier pool, raising bargaining power for green-certified vendors and risking price/lead-time pressure where compliant materials are scarce.

- 2025 net-zero deadline raises supplier ESG bar

- 42% recycled-content polymer purchases in 2024

- Smaller compliant supplier pool increases vendor leverage

- Risk: higher prices and longer lead times for certified materials

Supplier power tightens: feedstock shocks, patents & green specs squeeze margins

Suppliers hold moderate-to-strong power: concentrated petrochemical supply (top-5 ~45% capacity) and patented fittings (15–20% BOM; 12–20 week lead-times) raise switching costs; Brent ~86 USD/bbl (end-2025) and +12% ethylene YTD pressure margins (10% feedstock rise → ~3–5ppt gross margin hit). Georg Fischer merger (EUR 3.2bn procurement 2024) cuts COGS ~4–6% and lead-times 10–15%, but green specs (42% recycled polymers 2024) narrow vendor pool.

| Metric | 2024/2025 |

|---|---|

| Top-5 polymer share | ~45% |

| Brent (end-2025) | ~86 USD/bbl |

| Ethylene YTD change | +12% |

| Feedstock shock impact | 10% → −3–5ppt GM |

| Procurement scale | EUR 3.2bn (2024) |

| Recycled polymer share | 42% (2024) |

What is included in the product

Tailored exclusively for Uponor, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market position, with strategic insights for investors and management.

Clear, one-sheet Porter’s Five Forces for Uponor—instantly visualize competitive pressure and strategic levers to ease boardroom decisions and prioritize actions.

Customers Bargaining Power

Concentration of Wholesale Distribution

A large share of Uponor’s sales flows through a few major plumbing/HVAC wholesalers that control regional markets; in 2024 these top 10 distributors accounted for roughly 38% of company channel sales. These intermediaries press for higher rebates and exclusive marketing support, squeezing gross margins by an estimated 120–180 basis points in recent years. By late 2025 further consolidation lifted volume leverage—top accounts now represent ~45% of channel volumes, increasing their bargaining power.

Low Switching Costs for Standard Applications

In residential construction, basic piping and underfloor heating are often commodities, so installers switch brands for lower prices with little tech friction; industry surveys show 62% of contractors rank price as top buying factor in 2024. This price sensitivity meant Uponor’s 2024 Americas margin pressure—gross margin down ~140 bps—forced focus on service, digital tools, and brand reliability to retain loyalty.

Influence of Specifiers and Engineers

Architects and MEP engineers specify Uponor products early on for commercial projects, and their preference for Uponor’s technical performance and BIM (building information modeling) support reduces end-customer bargaining power by locking choices before procurement. Uponor reported in 2024 that 42% of its commercial project wins cited BIM integration and design software as a key factor, strengthening specifier-driven demand. Providing detailed technical data and design tools raises switching costs for owners and contractors and helps secure higher-margin projects.

Growth of Direct-to-Contractor Digital Platforms

The rise of e-commerce and digital procurement lets small contractors compare prices and availability in real time, raising price pressure on Uponor as buyers spot cheaper alternatives and promo deals; by 2024, 46% of US construction firms used online procurement platforms, up from 31% in 2019 (Dodge Data & Analytics).

To counter this transparency, Uponor invested in a digital ecosystem—supplier portals, stock visibility, and installation support—aiming to justify a premium and protect margins: reported digital sales/support initiatives targeted a 3–5% uplift in ASP (average selling price) in 2024.

Demand for Integrated Energy Systems

Modern buyers favor integrated systems combining radiant heating, heat pumps, and smart controls, shifting purchasing from parts to full-system performance; this raises customer leverage to demand interoperability and 10–15 year warranties.

In 2025 high-efficiency buildings account for ~28% of European retrofit spend and 34% of US new-build HVAC budgets, so Uponor must certify compatibility and offer longer-term service contracts to stay a preferred partner.

- Customers demand system-level performance, not components

- Interoperability and long warranties increase bargaining power

- ~28% EU retrofit, ~34% US new-build HVAC market relevance

- Uponor must certify integration and extend service terms

Rising distributor clout, price-driven contractors and BIM shape margin squeeze

Customers hold high bargaining power: top 10 distributors ~45% channel volumes (late 2025), press rebates cutting gross margin ~120–180 bps; 62% contractors cite price as top factor (2024); 46% US firms use online procurement (2024), raising transparency; 42% of commercial wins cited BIM support (2024), which reduces switching and protects margins.

| Metric | Value |

|---|---|

| Top-10 distributor share | ~45% (late 2025) |

| Contractors prioritizing price | 62% (2024) |

| Online procurement use | 46% US (2024) |

| Commercial wins citing BIM | 42% (2024) |

| Estimated margin hit | 120–180 bps |

Preview Before You Purchase

Uponor Porter's Five Forces Analysis

This preview shows the exact Uponor Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; it’s fully formatted and ready to download and use the moment you buy.