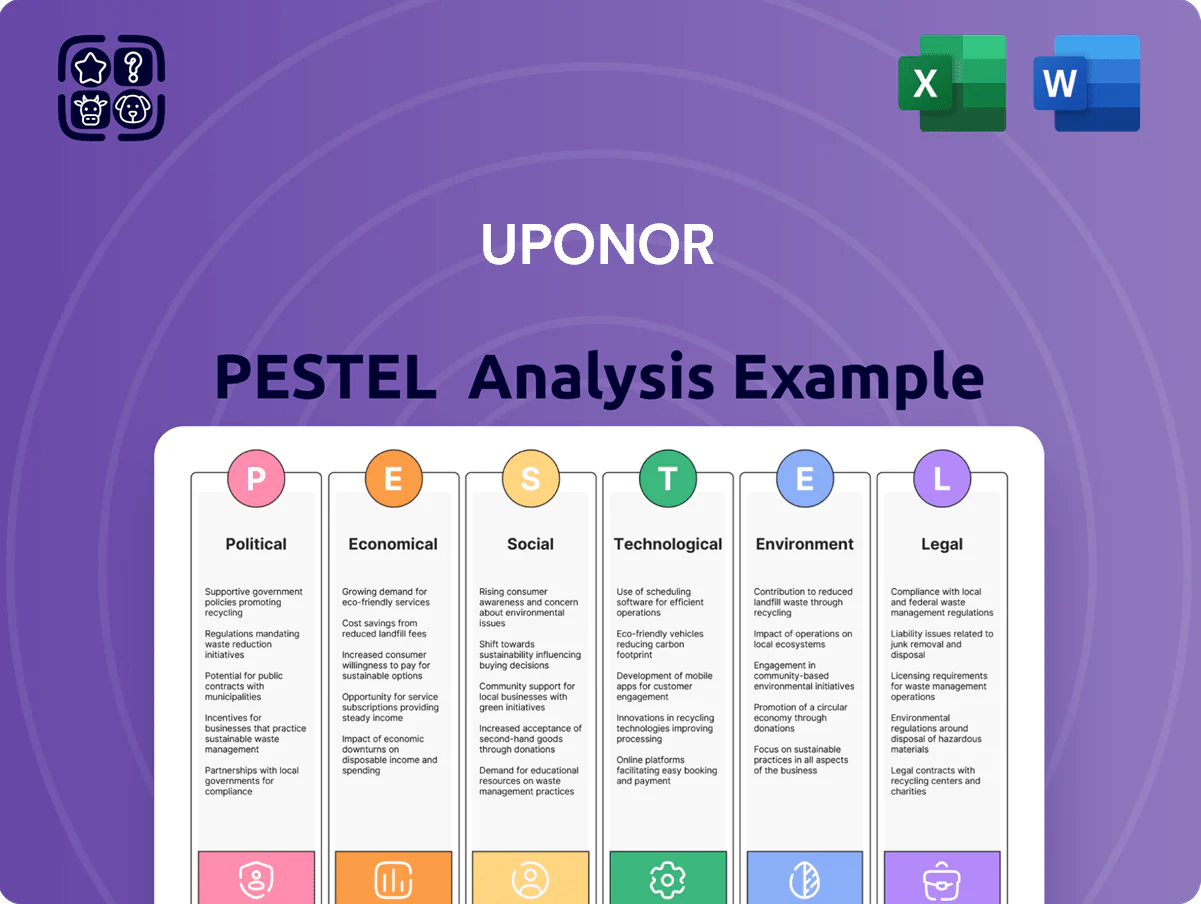

Uponor PESTLE Analysis

Your Competitive Advantage Starts with This Report

Understand how political, economic, social, technological, legal, and environmental forces shape Uponor’s prospects—our concise PESTLE highlights key risks and opportunities to inform investment and strategy decisions; purchase the full, editable report to access the complete, data-driven breakdown and actionable recommendations instantly.

Political factors

European Union Energy Directives

The EU Energy Performance of Buildings Directive (recast 2018/844 and EPBD revision 2021) boosts demand for Uponor radiant heating/cooling as member states aim to cut buildings' CO2 by ~60% vs 1990 by 2050; 2023 estimates show building renovation rates target rising from 1% to 2% annually, expanding retrofit market ~€100–150bn/yr. Political mandates and national recovery plans channel subsidies and create a stable long-term market for Uponor’s sustainable systems.

Infrastructure Investment Legislation

The US Infrastructure Investment and Jobs Act allocates about $55 billion for water infrastructure; federal and state lead pipe replacement programs mobilized nearly $15 billion in grants through 2024, creating large public contracts. Uponor—with FY2024 net sales of approximately €1.9 billion and strong PEX piping product lines—is well positioned to capture market share as municipalities prioritize replacements. This political funding pipeline remains active through 2026, supporting multi-year project flows.

Global Trade and Tariff Policies

Trade tensions and shifting tariffs between blocs like US-EU-China raised input costs; steel/aluminum tariffs added up to 25% historically and input inflation pushed building material prices up ~12% in 2023, affecting Uponor margins. Navigating geopolitics is essential to protect a $1.2bn FY2024 revenue base and keep supply chains agile via diversified sourcing. Rising protectionism in markets such as India and the US may drive further local production to avoid cross-border duties and preserve competitive pricing.

Urbanization and Public Housing Initiatives

Government urban development plans in markets like India and China target millions of high-density units; India aims to build 60 lakh affordable homes under PMAY by 2025, driving demand for efficient plumbing systems.

Political pressure for affordable, quality housing favors Uponor modular and prefabricated plumbing, aligning with lower labor costs and faster installs, improving project IRR and reducing timelines.

Subsidies for green building tech—EU recovery funds and US/China incentives—boost uptake of Uponor high-end systems through tax credits and grants covering up to 20–30% of green retrofit costs.

- Rising urban housing targets (e.g., India 6 million units) increase demand

- Modular plumbing reduces installation time and costs

- Green subsidies (20–30% support) improve ROI for high-end systems

Geopolitical Stability in Manufacturing Hubs

The company’s operations are sensitive to political stability in regions housing key manufacturing and suppliers; 2024 trade disruptions in Eastern Europe raised logistics costs by an estimated 4–6% for EU-based pipe manufacturers.

Conflicts or diplomatic shifts in Eastern Europe or Asia risk interrupting polymer and component flows—Asia accounted for ~22% of global PVC resin exports in 2023, affecting lead times.

Under Georg Fischer, diversified facilities across Europe and North America reduce exposure; Georg Fischer reported manufacturing footprint in 30+ countries and 2024 group net sales of CHF 3.5bn, providing operational resilience.

- Regional instability can raise logistics and input costs ~4–6%

- Asia ~22% share of PVC resin exports (2023) affects supply

- Georg Fischer: 30+ countries, CHF 3.5bn net sales (2024) aids diversification

EU retrofit boom and US IIJA lift radiant heating & PEX demand; €100–150bn/yr market

EU EPBD & national retrofit targets lift radiant heating demand; buildings renovation rate target rising to ~2%/yr expands €100–150bn/yr retrofit market. US IIJA water funds ~$55bn + ~$15bn lead-pipe grants through 2024 drive municipal PEX demand; Uponor FY2024 sales ~€1.9bn. Tariffs/input inflation raised material costs ~12% (2023); regional instability increased logistics ~4–6%.

| Indicator | Value |

|---|---|

| EU retrofit market | €100–150bn/yr |

| Renovation rate target | ~2%/yr |

| US infrastructure funds | $55bn |

| Lead-pipe grants (to 2024) | $15bn |

| Uponor FY2024 sales | €1.9bn |

| Material price rise (2023) | ~12% |

| Logistics rise (2024, E. Europe) | 4–6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Uponor across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities and support executives, consultants, and entrepreneurs in strategy, scenario planning, and investor-ready reporting.

Condenses Uponor's PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation, editable for local context, and ready to drop into presentations or planning sessions to streamline risk and market-position discussions.

Economic factors

Interest Rate and Construction Cycles

The global construction sector is highly sensitive to central bank rate policy: elevated policy rates—with the Fed funds peak near 5.25–5.50% in 2024 and ECB rates around 4.0%—dented mortgage affordability and new residential starts, which fell roughly 10–15% YoY in key markets in 2024; Uponor shifted emphasis toward renovation/modernization, which held steadier (single‑digit declines), and expects new‑build demand to recover in North America and Europe as rates stabilize through 2025.

Raw Material Price Volatility

Raw material price volatility, especially polymers and metals, is a primary driver of Uponor’s margin profile; resin and copper costs comprised roughly 18–22% of COGS in 2024, with oil-linked polymer input prices rising about 12% YoY. Fluctuations in crude and chemical processing costs directly affect PEX and HDPE procurement expenses, where feedstock-linked input swings reached ±15% in 2023–24. Uponor uses strategic hedging and dynamic pricing—hedges covered ~60% of expected polymer needs in 2024—to mitigate sudden inflationary spikes in global commodities markets.

Synergies from Georg Fischer Acquisition

Following the Georg Fischer integration, Uponor expects annual cost synergies of about EUR 40–60m and revenue synergies from cross-selling across a combined EUR ~1.8bn pro forma sales base (2024 estimate), driven by optimized logistics and a unified global distribution network.

Labor Market Shortages in Trades

Labor shortages in trades have pushed US plumber and HVAC vacancy rates above 8% in 2024, raising installation labor costs by an estimated 7–12% on average and prolonging project timelines.

Uponor’s push for press-fit, PEX, and prefabricated systems reduces on-site labor hours up to 30% per install, lowering total installed cost and error-related rework.

By enabling less-specialized crews to complete installs, Uponor secures pricing power and market share amid constrained labor supply.

- Plumber/HVAC vacancy >8% (2024)

- Installation cost inflation 7–12%

- Uponor reduces on-site hours ~30%

- Competitive edge via lower-skilled labor deployment

Currency Exchange Rate Fluctuations

As a Euro-reporting multinational with ~40% revenue in USD, Uponor faces translation and transaction risks from EUR/USD swings; a 10% EUR depreciation vs USD in 2022–2024 would materially boost reported revenues in euros but squeeze purchasing costs for euro-denominated inputs.

Volatility (EUR/USD ranged ~0.95–1.12 in 2023–2025) affects export competitiveness and margin visibility; hedging, local-currency financing and netting policies are vital to stabilize 2024–25 earnings amid divergent ECB-Fed paths.

- ~40% revenue exposure to USD

- EUR/USD ranged ~0.95–1.12 (2023–2025)

- Hedging and local financing reduce translation/transaction risk

Higher rates dent new‑builds; input costs & labor squeeze margins as USD exposure rises

Higher interest rates cut new-build demand ~10–15% in 2024 while renovation held single‑digit declines; resin/copper≈18–22% of COGS with polymer input +12% YoY (2024); Georg Fischer deal targets EUR 40–60m synergies on ~EUR 1.8bn pro‑forma sales; plumber/HVAC vacancy >8% raised installation costs 7–12%, Uponor cuts on‑site hours ~30%; USD ≈40% revenue exposure, EUR/USD 0.95–1.12 (2023–25).

| Metric | 2024 |

|---|---|

| New-build demand change | -10–15% |

| Renovation change | -1–9% |

| Polymer input YoY | +12% |

| Resin/copper of COGS | 18–22% |

| Synergies (Georg Fischer) | EUR 40–60m |

| Pro‑forma sales | ~EUR 1.8bn |

| Plumber/HVAC vacancy | >8% |

| Installation cost inflation | 7–12% |

| On‑site hours reduction | ~30% |

| USD revenue exposure | ~40% |

| EUR/USD range | 0.95–1.12 |

Preview the Actual Deliverable

Uponor PESTLE Analysis

The preview shown here is the exact Uponor PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Understand how political, economic, social, technological, legal, and environmental forces shape Uponor’s prospects—our concise PESTLE highlights key risks and opportunities to inform investment and strategy decisions; purchase the full, editable report to access the complete, data-driven breakdown and actionable recommendations instantly.

Political factors

European Union Energy Directives

The EU Energy Performance of Buildings Directive (recast 2018/844 and EPBD revision 2021) boosts demand for Uponor radiant heating/cooling as member states aim to cut buildings' CO2 by ~60% vs 1990 by 2050; 2023 estimates show building renovation rates target rising from 1% to 2% annually, expanding retrofit market ~€100–150bn/yr. Political mandates and national recovery plans channel subsidies and create a stable long-term market for Uponor’s sustainable systems.

Infrastructure Investment Legislation

The US Infrastructure Investment and Jobs Act allocates about $55 billion for water infrastructure; federal and state lead pipe replacement programs mobilized nearly $15 billion in grants through 2024, creating large public contracts. Uponor—with FY2024 net sales of approximately €1.9 billion and strong PEX piping product lines—is well positioned to capture market share as municipalities prioritize replacements. This political funding pipeline remains active through 2026, supporting multi-year project flows.

Global Trade and Tariff Policies

Trade tensions and shifting tariffs between blocs like US-EU-China raised input costs; steel/aluminum tariffs added up to 25% historically and input inflation pushed building material prices up ~12% in 2023, affecting Uponor margins. Navigating geopolitics is essential to protect a $1.2bn FY2024 revenue base and keep supply chains agile via diversified sourcing. Rising protectionism in markets such as India and the US may drive further local production to avoid cross-border duties and preserve competitive pricing.

Urbanization and Public Housing Initiatives

Government urban development plans in markets like India and China target millions of high-density units; India aims to build 60 lakh affordable homes under PMAY by 2025, driving demand for efficient plumbing systems.

Political pressure for affordable, quality housing favors Uponor modular and prefabricated plumbing, aligning with lower labor costs and faster installs, improving project IRR and reducing timelines.

Subsidies for green building tech—EU recovery funds and US/China incentives—boost uptake of Uponor high-end systems through tax credits and grants covering up to 20–30% of green retrofit costs.

- Rising urban housing targets (e.g., India 6 million units) increase demand

- Modular plumbing reduces installation time and costs

- Green subsidies (20–30% support) improve ROI for high-end systems

Geopolitical Stability in Manufacturing Hubs

The company’s operations are sensitive to political stability in regions housing key manufacturing and suppliers; 2024 trade disruptions in Eastern Europe raised logistics costs by an estimated 4–6% for EU-based pipe manufacturers.

Conflicts or diplomatic shifts in Eastern Europe or Asia risk interrupting polymer and component flows—Asia accounted for ~22% of global PVC resin exports in 2023, affecting lead times.

Under Georg Fischer, diversified facilities across Europe and North America reduce exposure; Georg Fischer reported manufacturing footprint in 30+ countries and 2024 group net sales of CHF 3.5bn, providing operational resilience.

- Regional instability can raise logistics and input costs ~4–6%

- Asia ~22% share of PVC resin exports (2023) affects supply

- Georg Fischer: 30+ countries, CHF 3.5bn net sales (2024) aids diversification

EU retrofit boom and US IIJA lift radiant heating & PEX demand; €100–150bn/yr market

EU EPBD & national retrofit targets lift radiant heating demand; buildings renovation rate target rising to ~2%/yr expands €100–150bn/yr retrofit market. US IIJA water funds ~$55bn + ~$15bn lead-pipe grants through 2024 drive municipal PEX demand; Uponor FY2024 sales ~€1.9bn. Tariffs/input inflation raised material costs ~12% (2023); regional instability increased logistics ~4–6%.

| Indicator | Value |

|---|---|

| EU retrofit market | €100–150bn/yr |

| Renovation rate target | ~2%/yr |

| US infrastructure funds | $55bn |

| Lead-pipe grants (to 2024) | $15bn |

| Uponor FY2024 sales | €1.9bn |

| Material price rise (2023) | ~12% |

| Logistics rise (2024, E. Europe) | 4–6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Uponor across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities and support executives, consultants, and entrepreneurs in strategy, scenario planning, and investor-ready reporting.

Condenses Uponor's PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation, editable for local context, and ready to drop into presentations or planning sessions to streamline risk and market-position discussions.

Economic factors

Interest Rate and Construction Cycles

The global construction sector is highly sensitive to central bank rate policy: elevated policy rates—with the Fed funds peak near 5.25–5.50% in 2024 and ECB rates around 4.0%—dented mortgage affordability and new residential starts, which fell roughly 10–15% YoY in key markets in 2024; Uponor shifted emphasis toward renovation/modernization, which held steadier (single‑digit declines), and expects new‑build demand to recover in North America and Europe as rates stabilize through 2025.

Raw Material Price Volatility

Raw material price volatility, especially polymers and metals, is a primary driver of Uponor’s margin profile; resin and copper costs comprised roughly 18–22% of COGS in 2024, with oil-linked polymer input prices rising about 12% YoY. Fluctuations in crude and chemical processing costs directly affect PEX and HDPE procurement expenses, where feedstock-linked input swings reached ±15% in 2023–24. Uponor uses strategic hedging and dynamic pricing—hedges covered ~60% of expected polymer needs in 2024—to mitigate sudden inflationary spikes in global commodities markets.

Synergies from Georg Fischer Acquisition

Following the Georg Fischer integration, Uponor expects annual cost synergies of about EUR 40–60m and revenue synergies from cross-selling across a combined EUR ~1.8bn pro forma sales base (2024 estimate), driven by optimized logistics and a unified global distribution network.

Labor Market Shortages in Trades

Labor shortages in trades have pushed US plumber and HVAC vacancy rates above 8% in 2024, raising installation labor costs by an estimated 7–12% on average and prolonging project timelines.

Uponor’s push for press-fit, PEX, and prefabricated systems reduces on-site labor hours up to 30% per install, lowering total installed cost and error-related rework.

By enabling less-specialized crews to complete installs, Uponor secures pricing power and market share amid constrained labor supply.

- Plumber/HVAC vacancy >8% (2024)

- Installation cost inflation 7–12%

- Uponor reduces on-site hours ~30%

- Competitive edge via lower-skilled labor deployment

Currency Exchange Rate Fluctuations

As a Euro-reporting multinational with ~40% revenue in USD, Uponor faces translation and transaction risks from EUR/USD swings; a 10% EUR depreciation vs USD in 2022–2024 would materially boost reported revenues in euros but squeeze purchasing costs for euro-denominated inputs.

Volatility (EUR/USD ranged ~0.95–1.12 in 2023–2025) affects export competitiveness and margin visibility; hedging, local-currency financing and netting policies are vital to stabilize 2024–25 earnings amid divergent ECB-Fed paths.

- ~40% revenue exposure to USD

- EUR/USD ranged ~0.95–1.12 (2023–2025)

- Hedging and local financing reduce translation/transaction risk

Higher rates dent new‑builds; input costs & labor squeeze margins as USD exposure rises

Higher interest rates cut new-build demand ~10–15% in 2024 while renovation held single‑digit declines; resin/copper≈18–22% of COGS with polymer input +12% YoY (2024); Georg Fischer deal targets EUR 40–60m synergies on ~EUR 1.8bn pro‑forma sales; plumber/HVAC vacancy >8% raised installation costs 7–12%, Uponor cuts on‑site hours ~30%; USD ≈40% revenue exposure, EUR/USD 0.95–1.12 (2023–25).

| Metric | 2024 |

|---|---|

| New-build demand change | -10–15% |

| Renovation change | -1–9% |

| Polymer input YoY | +12% |

| Resin/copper of COGS | 18–22% |

| Synergies (Georg Fischer) | EUR 40–60m |

| Pro‑forma sales | ~EUR 1.8bn |

| Plumber/HVAC vacancy | >8% |

| Installation cost inflation | 7–12% |

| On‑site hours reduction | ~30% |

| USD revenue exposure | ~40% |

| EUR/USD range | 0.95–1.12 |

Preview the Actual Deliverable

Uponor PESTLE Analysis

The preview shown here is the exact Uponor PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.