United Parcel Service Boston Consulting Group Matrix

Download Your Competitive Advantage

UPS sits at the center of logistics disruption—global scale and strong cash flows suggest core lines act as Cash Cows while growing e-commerce and tech-driven services may be Stars or Question Marks; legacy asset-heavy segments risk Dog status without strategic shifts. This preview highlights placement trends and strategic pressures, but the full BCG Matrix delivers quadrant-level mappings, financial metrics, and clear recommendations to reallocate capital and optimize portfolio balance—purchase the complete report for the detailed Word + Excel deliverables and actionable strategy.

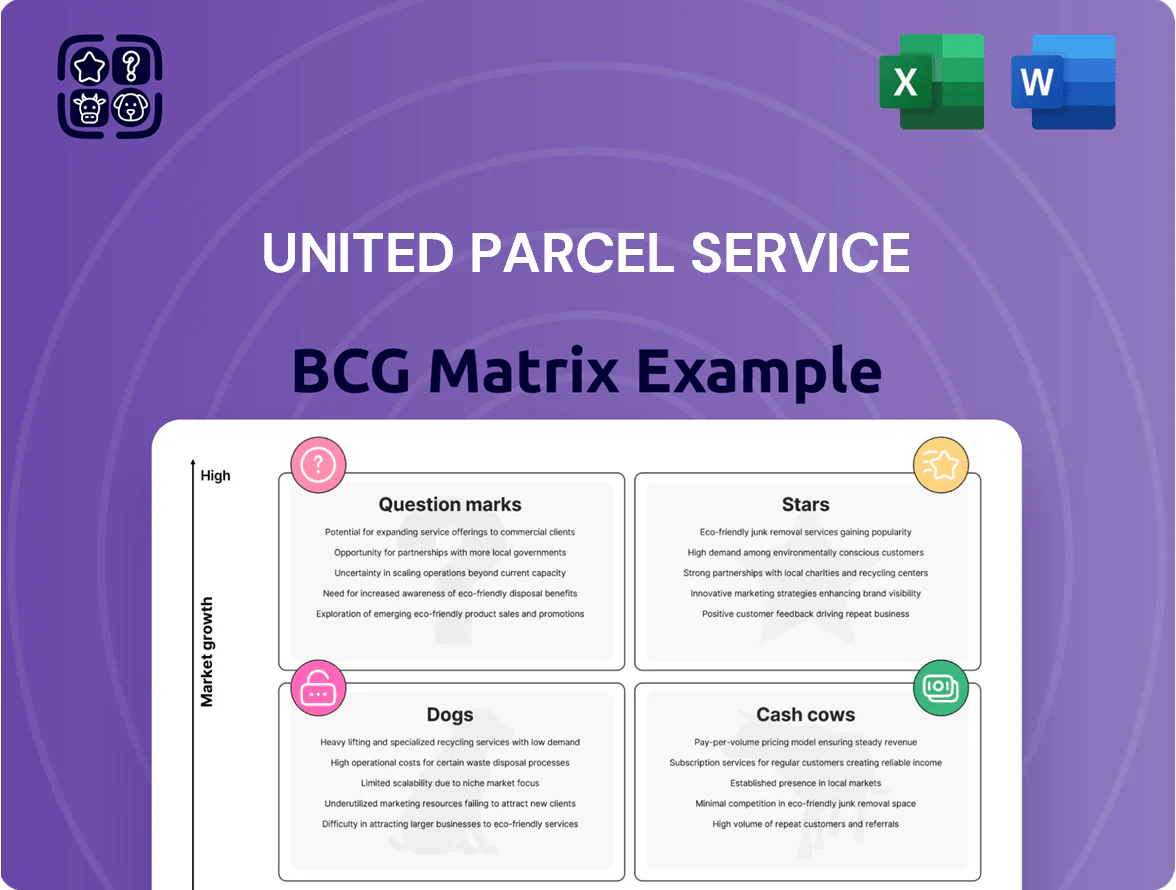

Stars

UPS Healthcare Logistics

UPS Healthcare Logistics, a star in United Parcel Service’s BCG matrix, is scaling cold-chain and pharma reach after acquiring Andlauer Healthcare Group in 2025; revenue is on pace for $20 billion by end-2026, up from roughly $8–9 billion in 2023.

International Premium Express

International Premium Express is a Star in UPSs BCG matrix: premium time-definite small parcels hold high share on lucrative cross-border lanes, driving margin-rich volumes.

Through 2025 UPS reported mid-single-digit volume growth in international air exports and a 6% revenue uptick in Supply Chain & Freight’s premium lines, aided by air-network optimization.

Investments in automated hubs—€420m in Europe (2024–25) and $350m in APAC—secure capacity and high-entry barriers, keeping UPS a leading global integrator.

Digital Access Program (DAP)

The Digital Access Program (DAP) is a high-growth UPS initiative connecting UPS with e-commerce platforms to give small and medium businesses streamlined shipping; by Q4 2025 DAP sustained ~25% year-over-year revenue growth and drove an estimated $350 million in incremental GMV for UPS in 2025.

DAP has expanded UPS reach into the SME segment, raising SME penetration by ~4 percentage points versus 2022 and adding roughly 600,000 active merchant accounts through platform partnerships.

This software-driven segment uses data science to boost yields and market share—improving average order yield by ~8% while avoiding heavy capital spending, keeping incremental capex under $40 million in 2023–2025.

Network of the Future Automation

Network of the Future Automation is a Star in UPS’s BCG matrix: it transforms core logistics via heavy AI and robotics investment, creating scalable growth potential.

By end-2025 UPS automated 63% of hub volume, cutting unit labor costs and raising throughput—supporting revenue resilience as US parcel margins faced wage inflation and peak-season surcharges.

This tech lead defends market share and sets up domestic operations to shift from Star to cash cow as automation maturity boosts free cash flow and lowers incremental costs.

- 63% hub automation by Dec 31, 2025

- Lower unit labor cost, higher throughput

- Supports margin resilience amid rising wages

- Path: Star → Cash cow via scale and FCF

UPS Premier and Cold Chain Services

UPS Premier is the sensor-enabled, high-tech tier for healthcare and tech shipments, offering real-time temperature and location monitoring and priority handling for sensitive cargo.

Adoption rose sharply: healthcare cold-chain demand grew ~12% in 2024 and UPS reported a 20%+ YoY volume increase in specialty logistics services in H1 2025, driven by biologics and high-value electronics.

High market growth plus UPS’s global network and 2024 revenue of $100.3B make Premier a Star in the BCG matrix—worthy of continued capital and tech investment.

- Target: biologics, high-value electronics

- Growth: ~12% sector CAGR (2024), 20%+ UPS specialty volume growth H1 2025

- Scale: UPS 2024 revenue $100.3B

- Why invest: high growth, strong infrastructure, margin uplift

UPS Stars Fuel Growth: Healthcare to $20B by 2026, DAP +25% & Automation 63%

UPS Stars—Healthcare Logistics, Intl Premium Express, DAP, Network of the Future, and UPS Premier—drive high-growth, margin-rich segments: Healthcare rev ~ $20B est. 2026 (from $8–9B in 2023), DAP +25% YoY (2025), hub automation 63% (2025), specialty logistics volume +20% H1 2025; UPS 2024 revenue $100.3B.

| Segment | 2024–25 metric | Role |

|---|---|---|

| Healthcare Logistics | $8–9B (2023) → $20B est. 2026 | Star |

| Intl Premium Express | mid-single-digit vol. growth | Star |

| DAP | +25% YoY (2025); +600k merchants | Star |

| Network Automation | 63% hub automation (2025) | Star→Cash cow |

| UPS Premier | +20% vol. H1 2025; 12% sector CAGR | Star |

What is included in the product

BCG Matrix review of UPS products: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page BCG Matrix mapping UPS business units to quadrants for quick strategic decisions and portfolio optimization.

Cash Cows

U.S. Domestic Ground Package

The U.S. Domestic Ground segment is UPS’s core cash cow, holding about 50%+ domestic market share and operating in a mature market; it produced roughly $9.5B in operating profit in 2024, funding most corporate cash needs.

Volume growth slowed under the Better Not Bigger strategy, but Ground still generated about $7–8B free cash flow in 2024, used for dividends and investments.

Recent automation investments raised productivity and helped sustain ~13–15% operating margins despite higher labor costs from the 2023 Teamsters contract.

B2B Commercial Delivery

B2B commercial delivery is a UPS cash cow: high delivery density and steady pricing drive predictable margins and low churn.

In 2025 B2B rose to over 42% of U.S. volume, shifting mix away from lower‑margin residential parcels and lifting network yield; operating margin contribution remains north of core parcel averages.

Requires less marketing, lower customer acquisition cost, and funds investments in high‑growth segments like healthcare logistics and small‑business e‑commerce.

UPS Access Point Network

With over 24,000 UPS Access Point locations, this mature asset cuts last-mile costs by consolidating residential drop-offs—UPS estimated network savings of roughly $0.50–$1.00 per package in 2024, translating to tens of millions annually.

The infrastructure is embedded in consumer habits—58% of e-commerce shoppers used a parcel locker or pick-up point in 2024—so maintenance CapEx is low versus recurring cost savings and density benefits.

As a high-market-share solution for e-commerce pick-up and returns, Access Points handled a growing share of returns in 2024 and consistently lifts margin contribution across UPS’s Ground and Supply Chain segments.

Customs Brokerage and Trade Services

UPS, a top global customs broker, handled over 7 million customs shipments in 2024, providing brokerage, duty management, and trade compliance services that support thousands of multinational clients.

Operating in a mature market with high regulatory and tech entry barriers, UPS captures a commanding share with >20% operating margin in the unit and steady fee-based revenue less tied to parcel volume swings.

Consistent demand for compliance, filings, and trade documentation gives a reliable cash stream, lowering sensitivity to shipping-volume volatility and supporting UPS’s cash-cow status.

- 7M+ customs shipments (2024)

- >20% operating margin

- High entry barriers: regulation + tech

- Fee-based revenue = stable cash flow

Standard Domestic Air Services

Standard domestic air delivery is a mature UPS segment with ~40% US market share in 2025 and steady volume growth under 2% annually, providing predictable revenue and high margins compared with newer express units.

UPS runs these services on its existing 727/757/767 fleet equivalents, boosting aircraft utilization and requiring little capex—cash generation funded $1.2B+ of fleet modernization in 2024 alone.

These stable cash flows underwrite the shift to fuel-efficient aircraft and SAF (sustainable aviation fuel) commitments, supporting UPS’s goal to cut net emissions 46% by 2035 versus 2019 levels.

- ~40% US market share (2025)

- Volume growth <2% annually

- $1.2B+ fleet modernization funding (2024)

- Supports 46% emissions cut by 2035

UPS’s $9.5B cash cows fuel dividends, fleet upgrades & health/e‑commerce bets

UPS cash cows—U.S. Ground, B2B delivery, Access Points, Customs brokerage, and Domestic Air—generated roughly $9.5B operating profit and $7–8B free cash flow in 2024, funding dividends, ~$1.2B fleet modernization, and investments in healthcare and e‑commerce logistics.

| Segment | 2024 key metric | Margin/notes |

|---|---|---|

| U.S. Ground | $9.5B op profit | 13–15% margin |

| B2B | 42% U.S. volume (2025) | Higher yield |

| Access Points | 24,000 locations | $0.50–$1.00 saved/pkg |

| Customs | 7M shipments | >20% margin |

| Domestic Air | ~40% US share (2025) | Low capex |

Delivered as Shown

United Parcel Service BCG Matrix

The file you're previewing on this page is the final United Parcel Service BCG Matrix you'll receive after purchase; no watermarks, no demo content—just the fully formatted, ready-to-use strategic report designed for clear portfolio analysis.

This preview reflects the exact same UPS BCG Matrix report you'll download post-purchase, crafted with market-backed positioning and analysis to inform product/service prioritization and resource allocation.

What you see is the actual BCG Matrix file you’ll get—available immediately for editing, printing, or presenting to stakeholders without further revisions.

You're previewing the real, professionally designed UPS BCG Matrix that becomes yours after a one-time purchase, ready to plug into strategic planning, investor decks, or competitive reviews.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

UPS sits at the center of logistics disruption—global scale and strong cash flows suggest core lines act as Cash Cows while growing e-commerce and tech-driven services may be Stars or Question Marks; legacy asset-heavy segments risk Dog status without strategic shifts. This preview highlights placement trends and strategic pressures, but the full BCG Matrix delivers quadrant-level mappings, financial metrics, and clear recommendations to reallocate capital and optimize portfolio balance—purchase the complete report for the detailed Word + Excel deliverables and actionable strategy.

Stars

UPS Healthcare Logistics

UPS Healthcare Logistics, a star in United Parcel Service’s BCG matrix, is scaling cold-chain and pharma reach after acquiring Andlauer Healthcare Group in 2025; revenue is on pace for $20 billion by end-2026, up from roughly $8–9 billion in 2023.

International Premium Express

International Premium Express is a Star in UPSs BCG matrix: premium time-definite small parcels hold high share on lucrative cross-border lanes, driving margin-rich volumes.

Through 2025 UPS reported mid-single-digit volume growth in international air exports and a 6% revenue uptick in Supply Chain & Freight’s premium lines, aided by air-network optimization.

Investments in automated hubs—€420m in Europe (2024–25) and $350m in APAC—secure capacity and high-entry barriers, keeping UPS a leading global integrator.

Digital Access Program (DAP)

The Digital Access Program (DAP) is a high-growth UPS initiative connecting UPS with e-commerce platforms to give small and medium businesses streamlined shipping; by Q4 2025 DAP sustained ~25% year-over-year revenue growth and drove an estimated $350 million in incremental GMV for UPS in 2025.

DAP has expanded UPS reach into the SME segment, raising SME penetration by ~4 percentage points versus 2022 and adding roughly 600,000 active merchant accounts through platform partnerships.

This software-driven segment uses data science to boost yields and market share—improving average order yield by ~8% while avoiding heavy capital spending, keeping incremental capex under $40 million in 2023–2025.

Network of the Future Automation

Network of the Future Automation is a Star in UPS’s BCG matrix: it transforms core logistics via heavy AI and robotics investment, creating scalable growth potential.

By end-2025 UPS automated 63% of hub volume, cutting unit labor costs and raising throughput—supporting revenue resilience as US parcel margins faced wage inflation and peak-season surcharges.

This tech lead defends market share and sets up domestic operations to shift from Star to cash cow as automation maturity boosts free cash flow and lowers incremental costs.

- 63% hub automation by Dec 31, 2025

- Lower unit labor cost, higher throughput

- Supports margin resilience amid rising wages

- Path: Star → Cash cow via scale and FCF

UPS Premier and Cold Chain Services

UPS Premier is the sensor-enabled, high-tech tier for healthcare and tech shipments, offering real-time temperature and location monitoring and priority handling for sensitive cargo.

Adoption rose sharply: healthcare cold-chain demand grew ~12% in 2024 and UPS reported a 20%+ YoY volume increase in specialty logistics services in H1 2025, driven by biologics and high-value electronics.

High market growth plus UPS’s global network and 2024 revenue of $100.3B make Premier a Star in the BCG matrix—worthy of continued capital and tech investment.

- Target: biologics, high-value electronics

- Growth: ~12% sector CAGR (2024), 20%+ UPS specialty volume growth H1 2025

- Scale: UPS 2024 revenue $100.3B

- Why invest: high growth, strong infrastructure, margin uplift

UPS Stars Fuel Growth: Healthcare to $20B by 2026, DAP +25% & Automation 63%

UPS Stars—Healthcare Logistics, Intl Premium Express, DAP, Network of the Future, and UPS Premier—drive high-growth, margin-rich segments: Healthcare rev ~ $20B est. 2026 (from $8–9B in 2023), DAP +25% YoY (2025), hub automation 63% (2025), specialty logistics volume +20% H1 2025; UPS 2024 revenue $100.3B.

| Segment | 2024–25 metric | Role |

|---|---|---|

| Healthcare Logistics | $8–9B (2023) → $20B est. 2026 | Star |

| Intl Premium Express | mid-single-digit vol. growth | Star |

| DAP | +25% YoY (2025); +600k merchants | Star |

| Network Automation | 63% hub automation (2025) | Star→Cash cow |

| UPS Premier | +20% vol. H1 2025; 12% sector CAGR | Star |

What is included in the product

BCG Matrix review of UPS products: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page BCG Matrix mapping UPS business units to quadrants for quick strategic decisions and portfolio optimization.

Cash Cows

U.S. Domestic Ground Package

The U.S. Domestic Ground segment is UPS’s core cash cow, holding about 50%+ domestic market share and operating in a mature market; it produced roughly $9.5B in operating profit in 2024, funding most corporate cash needs.

Volume growth slowed under the Better Not Bigger strategy, but Ground still generated about $7–8B free cash flow in 2024, used for dividends and investments.

Recent automation investments raised productivity and helped sustain ~13–15% operating margins despite higher labor costs from the 2023 Teamsters contract.

B2B Commercial Delivery

B2B commercial delivery is a UPS cash cow: high delivery density and steady pricing drive predictable margins and low churn.

In 2025 B2B rose to over 42% of U.S. volume, shifting mix away from lower‑margin residential parcels and lifting network yield; operating margin contribution remains north of core parcel averages.

Requires less marketing, lower customer acquisition cost, and funds investments in high‑growth segments like healthcare logistics and small‑business e‑commerce.

UPS Access Point Network

With over 24,000 UPS Access Point locations, this mature asset cuts last-mile costs by consolidating residential drop-offs—UPS estimated network savings of roughly $0.50–$1.00 per package in 2024, translating to tens of millions annually.

The infrastructure is embedded in consumer habits—58% of e-commerce shoppers used a parcel locker or pick-up point in 2024—so maintenance CapEx is low versus recurring cost savings and density benefits.

As a high-market-share solution for e-commerce pick-up and returns, Access Points handled a growing share of returns in 2024 and consistently lifts margin contribution across UPS’s Ground and Supply Chain segments.

Customs Brokerage and Trade Services

UPS, a top global customs broker, handled over 7 million customs shipments in 2024, providing brokerage, duty management, and trade compliance services that support thousands of multinational clients.

Operating in a mature market with high regulatory and tech entry barriers, UPS captures a commanding share with >20% operating margin in the unit and steady fee-based revenue less tied to parcel volume swings.

Consistent demand for compliance, filings, and trade documentation gives a reliable cash stream, lowering sensitivity to shipping-volume volatility and supporting UPS’s cash-cow status.

- 7M+ customs shipments (2024)

- >20% operating margin

- High entry barriers: regulation + tech

- Fee-based revenue = stable cash flow

Standard Domestic Air Services

Standard domestic air delivery is a mature UPS segment with ~40% US market share in 2025 and steady volume growth under 2% annually, providing predictable revenue and high margins compared with newer express units.

UPS runs these services on its existing 727/757/767 fleet equivalents, boosting aircraft utilization and requiring little capex—cash generation funded $1.2B+ of fleet modernization in 2024 alone.

These stable cash flows underwrite the shift to fuel-efficient aircraft and SAF (sustainable aviation fuel) commitments, supporting UPS’s goal to cut net emissions 46% by 2035 versus 2019 levels.

- ~40% US market share (2025)

- Volume growth <2% annually

- $1.2B+ fleet modernization funding (2024)

- Supports 46% emissions cut by 2035

UPS’s $9.5B cash cows fuel dividends, fleet upgrades & health/e‑commerce bets

UPS cash cows—U.S. Ground, B2B delivery, Access Points, Customs brokerage, and Domestic Air—generated roughly $9.5B operating profit and $7–8B free cash flow in 2024, funding dividends, ~$1.2B fleet modernization, and investments in healthcare and e‑commerce logistics.

| Segment | 2024 key metric | Margin/notes |

|---|---|---|

| U.S. Ground | $9.5B op profit | 13–15% margin |

| B2B | 42% U.S. volume (2025) | Higher yield |

| Access Points | 24,000 locations | $0.50–$1.00 saved/pkg |

| Customs | 7M shipments | >20% margin |

| Domestic Air | ~40% US share (2025) | Low capex |

Delivered as Shown

United Parcel Service BCG Matrix

The file you're previewing on this page is the final United Parcel Service BCG Matrix you'll receive after purchase; no watermarks, no demo content—just the fully formatted, ready-to-use strategic report designed for clear portfolio analysis.

This preview reflects the exact same UPS BCG Matrix report you'll download post-purchase, crafted with market-backed positioning and analysis to inform product/service prioritization and resource allocation.

What you see is the actual BCG Matrix file you’ll get—available immediately for editing, printing, or presenting to stakeholders without further revisions.

You're previewing the real, professionally designed UPS BCG Matrix that becomes yours after a one-time purchase, ready to plug into strategic planning, investor decks, or competitive reviews.