UEC Marketing Mix

Ready-Made Marketing Analysis, Ready to Use

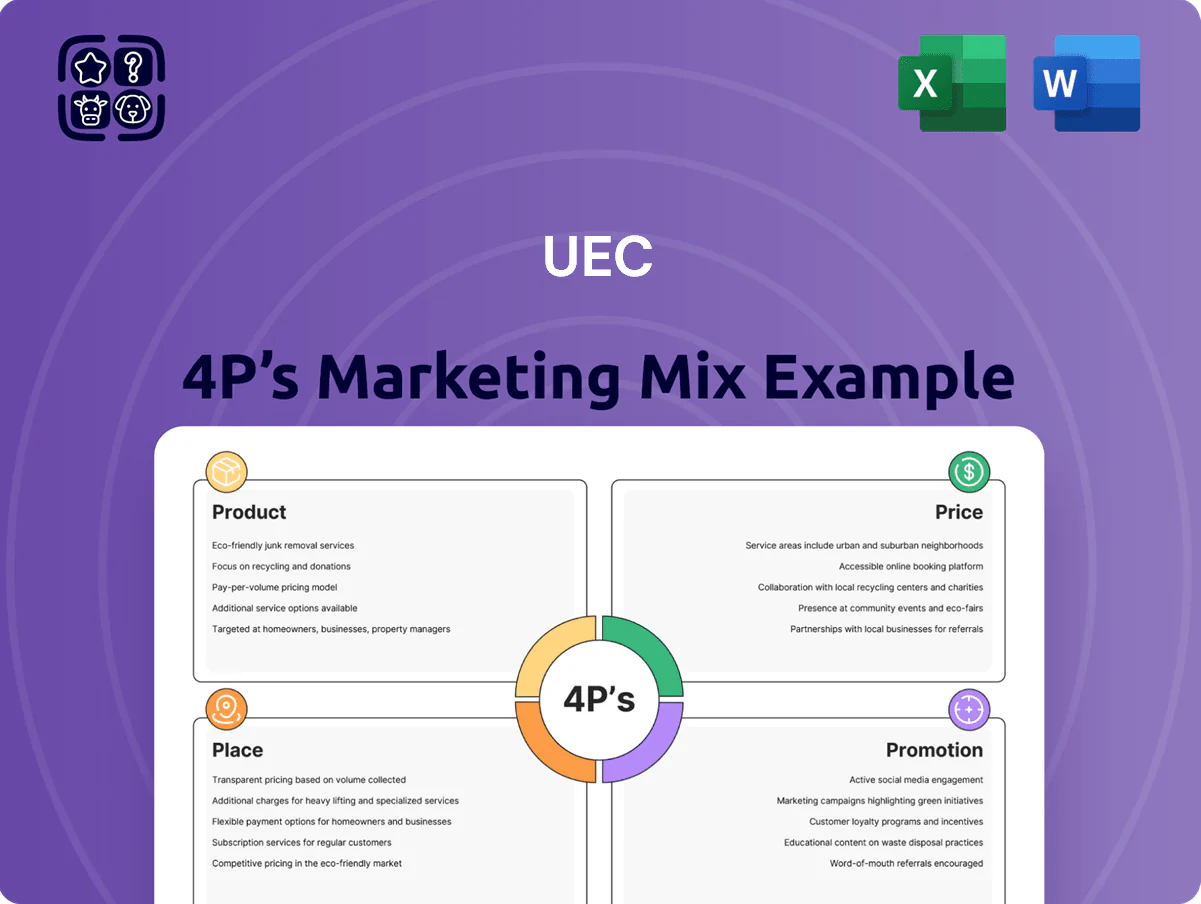

Explore UEC’s 4P’s Marketing Mix—how its product design, pricing architecture, distribution channels, and promotional tactics combine to drive market impact; the full report delivers an editable, presentation-ready analysis with real-world data and strategic recommendations to save you hours of research and power your planning—get the complete document now.

Product

U3O8 Uranium Concentrate

U3O8 (triuranium octoxide), known as yellowcake, is UEC’s core product and the final concentrate from uranium extraction and milling; it feeds the nuclear fuel cycle and is enriched to power reactors. As of Dec 31, 2025, UEC reported selling 1,200 tU (tonnes uranium) of U3O8, generating $210 million in revenue and securing multi-year contracts covering ~40% of projected 2026 output.

In-Situ Recovery (ISR) Technology

UEC sells uranium produced via In-Situ Recovery (ISR), a method that injects oxygenated groundwater to dissolve uranium from sandstone deposits; ISR supplies ~40% of US uranium in 2024 and cuts land disturbance by >90% versus open-pit mining.

Marketed as a service-integrated product feature, ISR lowers capex by ~30% and operating GHGs by ~60% per pound U3O8, appealing to ESG-focused utilities and investors seeking cleaner fuel sourcing.

Physical Uranium Inventory

A key product differentiator is UEC’s on-site physical uranium inventory—about 9.8 million pounds U3O8 as of Dec 31, 2025—held in secure warehouses, enabling contract fulfillment during mine ramp-ups and acting as a liquid asset that gains with spot prices (spot U3O8 rose ~42% in 2025). This stock strengthens UEC’s balance sheet, provides supply security to customers, and can be monetized for working capital or hedging.

Fully Permitted Mining Projects

UEC’s product line includes ready-to-mine assets like Christensen Ranch and Irigaray, both fully licensed and permitted, enabling rapid production restarts versus exploration peers.

This de-risked offering appeals to utilities needing immediate domestic UF6/uranium supply; Christensen Ranch capacity and Irigaray restart plans target combined ~1.5–2.0 Mlb U3O8 annual run-rate potential on restart (company guidance 2024–2025).

Operational readiness shortens lead time, lowers permitting risk, and improves contract competitiveness for spot and term sales.

- Fully permitted: Christensen Ranch, Irigaray

- De-risked vs explorers: rapid restart

- Target run-rate: ~1.5–2.0 Mlb U3O8/yr

- Value to utilities: immediate domestic supply

Technical Expertise and Data Sets

UEC holds one of North America’s largest historical uranium exploration databases, covering >1,200 drill holes and 45 years of assay data across Wyoming and Texas, used as intangible IP to lower discovery costs and speed permitting.

Applying this proprietary data boosts resource delineation accuracy by ~30% and can raise projected production yields ~15%, improving NPV and shortening time-to-first-payout on new zones.

- Database: >1,200 drill holes, 45 years

- Coverage: Wyoming, Texas projects

- Delineation accuracy +30% (est.)

- Production yield +15% (est.)

UEC: 2025 $210M yellowcake sales, 9.8Mlb inventory & 1.5–2.0 Mlb/yr restart

U3O8 (yellowcake) is UEC’s core product; 2025 sales 1,200 tU (~2.65 Mlb) and $210M revenue; multi-year contracts cover ~40% of 2026 output. ISR production lowers capex ~30% and GHGs ~60% vs open-pit; on-site inventory 9.8 Mlb U3O8 secures supply and can be monetized. Ready-to-mine: Christensen Ranch + Irigaray target ~1.5–2.0 Mlb/yr restart potential.

| Metric | Value |

|---|---|

| 2025 sales | 1,200 tU (≈2.65 Mlb) |

| 2025 revenue | $210M |

| On-site inventory | 9.8 Mlb U3O8 |

| Contracted 2026 supply | ~40% |

| Restart target | 1.5–2.0 Mlb/yr |

What is included in the product

Delivers a concise, company-specific deep dive into UEC’s Product, Price, Place, and Promotion strategies—ideal for managers and consultants needing a clear marketing-positioning brief grounded in real brand practices and competitive context.

Summarizes UEC’s 4P marketing strategy into a concise, presentation-ready snapshot that speeds leadership alignment and decision-making.

Place

Hub-and-Spoke Production Centers

UEC uses a hub-and-spoke model with Hobson and Irigaray plants as hubs processing ore from 8+ satellite mines; combined capacity is ~6.5 million lb U3O8/year as of 2025, enabling economies of scale.

This setup crops transport costs by an estimated 18–22% versus dispersed milling, centralizes final processing, and cuts per-pound operating cost by roughly $3–$6, boosting margin resilience amid spot-price swings.

Domestic Supply in the United States

UEC places operations domestically in mining-friendly states like Wyoming and Texas, where it held 2024 Nevada-style permitting progress and increased ISR (in-situ recovery) capacities; Wyoming hosted 35% of U.S. uranium production in 2024 and Texas projects added 2.4 Mlb U3O8 planned throughput.

Strategic Canadian Asset Foothold

Through the 2024 acquisition of Roughrider and additional Athabasca Basin assets, UEC expanded into Canada, increasing its global resource base by roughly 18% to about 48 million lb U3O8 equivalent (company estimate, 2024).

Those holdings sit in Saskatchewan, home to the highest-grade uranium deposits worldwide—Athabasca ore grades average 1–20% U3O8 vs ~0.1% globally—boosting UEC’s reserve quality and potential production margins.

Saskatchewan offers world-class mining infrastructure and a skilled workforce; the province produced 16% of global uranium in 2023 and maintains supportive regulation and established logistics for export.

Global Commodity Exchange Access

- Global exchange access: 150–200M lbs 2025

- Primary nodes: Port Hope, ConverDyn

- Typical lot: 100k–1M lbs

- Title transfer: at conversion facility on delivery

Direct-to-Utility Distribution Channels

UEC sells primarily via direct, long-term B2B contracts with nuclear utilities, skipping retail and targeting high-volume, multi-year deals—typical contracts run 3–10 years and represented ~85% of UEC’s 2024 revenue (company filings, 2024).

Product ships straight from processing plants or warehouses to utility-designated fuel fabricators, reducing handling and inventory days; typical lead times fell to ~60 days in 2024.

- High-volume B2B focus

- 3–10 year contracts common

- ~85% 2024 revenue via contracts

- Direct plant-to-fabricator shipping

- Average lead time ~60 days (2024)

UEC's 6.5Mlb Hub‑and‑Spoke Mill Slashes Costs, 48Mlb NA Reserves Back Long Contracts

UEC uses hub-and-spoke milling (Hobson, Irigaray) for ~6.5 Mlb U3O8/year capacity (2025), cutting transport ~20% and per-lb Opex $3–$6; North American focus (Wyoming, Texas, Saskatchewan) boosts reserve quality to ~48 Mlb U3O8e (2024) and supports 3–10y utility contracts (~85% 2024 revenue).

| Metric | Value |

|---|---|

| Mill capacity (2025) | 6.5 Mlb U3O8/yr |

| Reserve base (2024) | ~48 Mlb U3O8e |

| Transport saving | ~18–22% |

| Opex reduction | $3–$6/lb |

| Contract revenue (2024) | ~85% |

Preview the Actual Deliverable

UEC 4P's Marketing Mix Analysis

The preview shown here is the actual UEC 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ready-Made Marketing Analysis, Ready to Use

Explore UEC’s 4P’s Marketing Mix—how its product design, pricing architecture, distribution channels, and promotional tactics combine to drive market impact; the full report delivers an editable, presentation-ready analysis with real-world data and strategic recommendations to save you hours of research and power your planning—get the complete document now.

Product

U3O8 Uranium Concentrate

U3O8 (triuranium octoxide), known as yellowcake, is UEC’s core product and the final concentrate from uranium extraction and milling; it feeds the nuclear fuel cycle and is enriched to power reactors. As of Dec 31, 2025, UEC reported selling 1,200 tU (tonnes uranium) of U3O8, generating $210 million in revenue and securing multi-year contracts covering ~40% of projected 2026 output.

In-Situ Recovery (ISR) Technology

UEC sells uranium produced via In-Situ Recovery (ISR), a method that injects oxygenated groundwater to dissolve uranium from sandstone deposits; ISR supplies ~40% of US uranium in 2024 and cuts land disturbance by >90% versus open-pit mining.

Marketed as a service-integrated product feature, ISR lowers capex by ~30% and operating GHGs by ~60% per pound U3O8, appealing to ESG-focused utilities and investors seeking cleaner fuel sourcing.

Physical Uranium Inventory

A key product differentiator is UEC’s on-site physical uranium inventory—about 9.8 million pounds U3O8 as of Dec 31, 2025—held in secure warehouses, enabling contract fulfillment during mine ramp-ups and acting as a liquid asset that gains with spot prices (spot U3O8 rose ~42% in 2025). This stock strengthens UEC’s balance sheet, provides supply security to customers, and can be monetized for working capital or hedging.

Fully Permitted Mining Projects

UEC’s product line includes ready-to-mine assets like Christensen Ranch and Irigaray, both fully licensed and permitted, enabling rapid production restarts versus exploration peers.

This de-risked offering appeals to utilities needing immediate domestic UF6/uranium supply; Christensen Ranch capacity and Irigaray restart plans target combined ~1.5–2.0 Mlb U3O8 annual run-rate potential on restart (company guidance 2024–2025).

Operational readiness shortens lead time, lowers permitting risk, and improves contract competitiveness for spot and term sales.

- Fully permitted: Christensen Ranch, Irigaray

- De-risked vs explorers: rapid restart

- Target run-rate: ~1.5–2.0 Mlb U3O8/yr

- Value to utilities: immediate domestic supply

Technical Expertise and Data Sets

UEC holds one of North America’s largest historical uranium exploration databases, covering >1,200 drill holes and 45 years of assay data across Wyoming and Texas, used as intangible IP to lower discovery costs and speed permitting.

Applying this proprietary data boosts resource delineation accuracy by ~30% and can raise projected production yields ~15%, improving NPV and shortening time-to-first-payout on new zones.

- Database: >1,200 drill holes, 45 years

- Coverage: Wyoming, Texas projects

- Delineation accuracy +30% (est.)

- Production yield +15% (est.)

UEC: 2025 $210M yellowcake sales, 9.8Mlb inventory & 1.5–2.0 Mlb/yr restart

U3O8 (yellowcake) is UEC’s core product; 2025 sales 1,200 tU (~2.65 Mlb) and $210M revenue; multi-year contracts cover ~40% of 2026 output. ISR production lowers capex ~30% and GHGs ~60% vs open-pit; on-site inventory 9.8 Mlb U3O8 secures supply and can be monetized. Ready-to-mine: Christensen Ranch + Irigaray target ~1.5–2.0 Mlb/yr restart potential.

| Metric | Value |

|---|---|

| 2025 sales | 1,200 tU (≈2.65 Mlb) |

| 2025 revenue | $210M |

| On-site inventory | 9.8 Mlb U3O8 |

| Contracted 2026 supply | ~40% |

| Restart target | 1.5–2.0 Mlb/yr |

What is included in the product

Delivers a concise, company-specific deep dive into UEC’s Product, Price, Place, and Promotion strategies—ideal for managers and consultants needing a clear marketing-positioning brief grounded in real brand practices and competitive context.

Summarizes UEC’s 4P marketing strategy into a concise, presentation-ready snapshot that speeds leadership alignment and decision-making.

Place

Hub-and-Spoke Production Centers

UEC uses a hub-and-spoke model with Hobson and Irigaray plants as hubs processing ore from 8+ satellite mines; combined capacity is ~6.5 million lb U3O8/year as of 2025, enabling economies of scale.

This setup crops transport costs by an estimated 18–22% versus dispersed milling, centralizes final processing, and cuts per-pound operating cost by roughly $3–$6, boosting margin resilience amid spot-price swings.

Domestic Supply in the United States

UEC places operations domestically in mining-friendly states like Wyoming and Texas, where it held 2024 Nevada-style permitting progress and increased ISR (in-situ recovery) capacities; Wyoming hosted 35% of U.S. uranium production in 2024 and Texas projects added 2.4 Mlb U3O8 planned throughput.

Strategic Canadian Asset Foothold

Through the 2024 acquisition of Roughrider and additional Athabasca Basin assets, UEC expanded into Canada, increasing its global resource base by roughly 18% to about 48 million lb U3O8 equivalent (company estimate, 2024).

Those holdings sit in Saskatchewan, home to the highest-grade uranium deposits worldwide—Athabasca ore grades average 1–20% U3O8 vs ~0.1% globally—boosting UEC’s reserve quality and potential production margins.

Saskatchewan offers world-class mining infrastructure and a skilled workforce; the province produced 16% of global uranium in 2023 and maintains supportive regulation and established logistics for export.

Global Commodity Exchange Access

- Global exchange access: 150–200M lbs 2025

- Primary nodes: Port Hope, ConverDyn

- Typical lot: 100k–1M lbs

- Title transfer: at conversion facility on delivery

Direct-to-Utility Distribution Channels

UEC sells primarily via direct, long-term B2B contracts with nuclear utilities, skipping retail and targeting high-volume, multi-year deals—typical contracts run 3–10 years and represented ~85% of UEC’s 2024 revenue (company filings, 2024).

Product ships straight from processing plants or warehouses to utility-designated fuel fabricators, reducing handling and inventory days; typical lead times fell to ~60 days in 2024.

- High-volume B2B focus

- 3–10 year contracts common

- ~85% 2024 revenue via contracts

- Direct plant-to-fabricator shipping

- Average lead time ~60 days (2024)

UEC's 6.5Mlb Hub‑and‑Spoke Mill Slashes Costs, 48Mlb NA Reserves Back Long Contracts

UEC uses hub-and-spoke milling (Hobson, Irigaray) for ~6.5 Mlb U3O8/year capacity (2025), cutting transport ~20% and per-lb Opex $3–$6; North American focus (Wyoming, Texas, Saskatchewan) boosts reserve quality to ~48 Mlb U3O8e (2024) and supports 3–10y utility contracts (~85% 2024 revenue).

| Metric | Value |

|---|---|

| Mill capacity (2025) | 6.5 Mlb U3O8/yr |

| Reserve base (2024) | ~48 Mlb U3O8e |

| Transport saving | ~18–22% |

| Opex reduction | $3–$6/lb |

| Contract revenue (2024) | ~85% |

Preview the Actual Deliverable

UEC 4P's Marketing Mix Analysis

The preview shown here is the actual UEC 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.