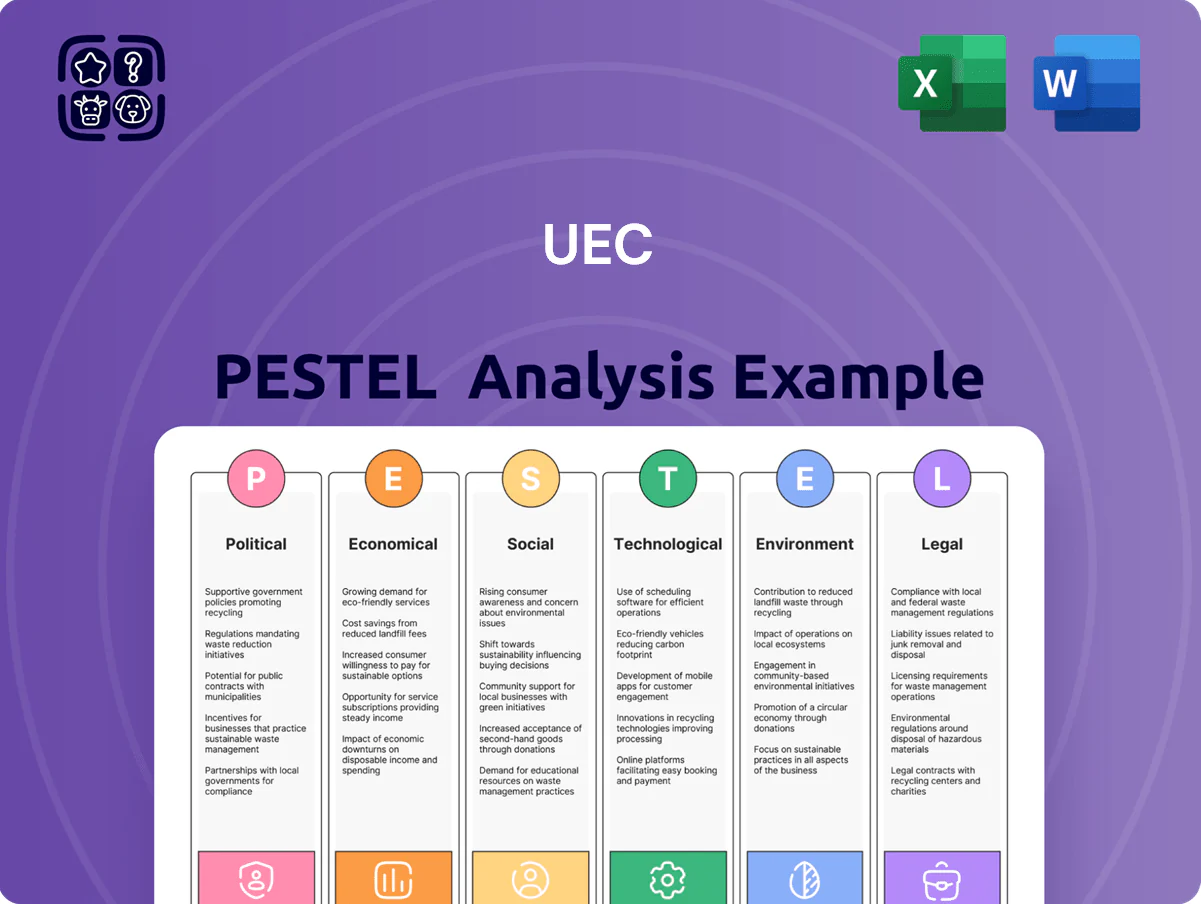

UEC PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our tailored PESTLE Analysis for UEC—spot regulatory, economic, and technological forces shaping its trajectory and use those insights to sharpen your investment or business strategy; purchase the full report for a complete, ready-to-use breakdown you can deploy immediately.

Political factors

U.S. Nuclear Fuel Security Act Implementation

The Nuclear Fuel Security Act implementation by late 2025 commits $2.5 billion in federal incentives and loan guarantees to boost domestic uranium production, signaling strong federal backing for supply-chain resilience.

Policy aims to cut foreign-adversary reliance by targeting a 50% domestic supply share for defense and critical reactors by 2030, increasing demand visibility for UEC’s projects.

For UEC, this creates prospects for multi-year government procurement contracts and elevates the national-security valuation of its ISR domestic assets, potentially improving project financing and offtake certainty.

Bipartisan Support for Nuclear Energy

Congressional backing for nuclear energy remains bipartisan, with 2023–2025 laws—including extensions to the 2024 Nuclear Credit and the 2025 Advanced Reactor Deployment Act—accelerating life‑extension and new builds; federal incentives now support ~20 GW of new capacity and ~$15–20 billion in deployment funding, creating a stable regulatory and investment environment for UEC and North American uranium developers.

Geopolitical Diversification from Russian Supply

The continued shift away from Russian nuclear fuel exports is a primary political driver for the Western uranium market; by late 2025 sanctions and trade restrictions reduced Russian enrichment market share from about 40% in 2021 to under 15% for Western utilities, forcing buyers to secure Tier 1 sources. UEC benefits as its assets are fully in the US and Canada, supplying utilities seeking supply‑chain resilience and pricing stability amid spot uranium rising ~120% from 2020‑2025.

State-Level Support in Mining Jurisdictions

Pro-mining policies in Wyoming and Texas have shortened permitting timelines for UEC’s in-situ recovery projects, with Wyoming cutting average permitting from 18 to ~10 months (2024 state reports) and Texas reducing backlog by ~35%.

Local governments treat uranium mining as a jobs and tax generator—Wyoming counties reported $45m in mining tax revenue (2024)—driving joint infrastructure projects that lower logistics costs at hub-and-spoke centers.

This political alignment reduces regulatory delay risk and improves operational efficiency, supporting higher capacity utilization and faster ramp-up for regional ISR operations.

- Permitting time cut: WY ~18→10 months; TX backlog −35%

- WY mining tax revenue 2024: $45m

- Reduced delay risk → higher capacity utilization

- Local infrastructure co-investment lowers logistics costs

Global Nuclear Expansion Alliances

U.S.-led international agreements aiming to triple global nuclear capacity to ~1,500 GWe by 2050 have lowered export barriers and created a stronger uranium demand floor; allied reactor commitments announced through late 2025 add ~200 GWe of new builds, boosting long-term fuel demand.

UEC, with ~250 Mlb U3O8 resources in North America and 2025 revenue of ~$120m, is positioned to supply allied markets and benefit from export-friendly trade frameworks supporting fuel security.

- Global target: ~1,500 GWe by 2050 (+~1,000 GWe vs today)

- Late-2025 allied new builds: ~200 GWe

- UEC North American resources: ~250 Mlb U3O8

- UEC 2025 revenue: ~$120m

US $2.5B Nuclear Push and Permitting Gains Bolster UEC ISR Supply Advantage

Strong US federal incentives (Nuclear Fuel Security Act $2.5B) and bipartisan nuclear policy through 2025 boost domestic uranium demand, favoring UEC’s US/Canada ISR assets; reduced Russian enrichment share (<15% by late‑2025) raises utility offtake for Tier‑1 suppliers. State pro‑mining measures cut permitting (WY ~18→10 months; TX backlog −35%) and local tax/infrastructure support (WY mining tax $45M 2024), lowering project risk and financing costs.

| Metric | Value |

|---|---|

| Federal incentives | $2.5B |

| Russian enrichment share (W 2025) | <15% |

| Permitting WY | ~10 months |

| TX permitting backlog | −35% |

| WY mining tax (2024) | $45M |

| UEC resources | ~250 Mlb U3O8 |

| UEC 2025 revenue | ~$120M |

What is included in the product

Explores how external macro-environmental factors uniquely affect the UEC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to reveal targeted threats, opportunities, and forward-looking implications for strategy, funding, and scenario planning.

Condenses the full UEC PESTLE into a clean, shareable summary formatted by PESTLE categories for quick interpretation in meetings, presentations, or cross-team alignment.

Economic factors

Uranium Spot and Term Price Appreciation

Low-Cost ISR Production Profile

UEC’s focus on In-Situ Recovery (ISR) cuts capital intensity—ISR capex can be 30–60% lower than conventional underground mining—supporting unit cash costs near US$20–30/lb U3O8 versus conventional peers often >US$40/lb. As late-2025 inflation lifts labor and materials by ~6–8% year-over-year, ISR’s lower labor intensity cushions margin erosion. This cost profile helped UEC sustain positive EBITDA in 2024–2025 scenarios even with uranium price swings of ±20%. ISR’s operating leverage supports resilience to short-term market volatility.

Strategic Physical Uranium Inventory

The company’s strategic stockpile of ~3.5 million pounds U3O8 valued at roughly $630 million by late 2025 (at ~USD180/lb) functions as a highly liquid asset and an effective hedge against spot volatility.

Rising inventory valuation has created non-dilutive financing optionality, enabling UEC to monetize or collateralize uranium to fund development without issuing equity.

This balance-sheet flexibility is pivotal for restarting production at Christensen Ranch and other sites while preserving shareholder dilution control.

Impact of Global Interest Rate Cycles

Stabilized global rates in late 2025—with major central bank policy rates roughly 4.5–5.0% in the US and 3.5–4.0% in the EU—lowered long-term discount rates, reducing the cost of capital for mining projects and improving present valuations of UEC’s long-dated assets despite its low debt ratio.

Improved rate visibility boosted institutional allocations to energy and commodities, with commodity-focused funds seeing inflows up to 12% YTD, which could ease financing for UEC’s infrastructure expansion.

- Global policy rates ~4.5–5.0% (US), 3.5–4.0% (EU) late 2025

- Lower discount rates improve long-term asset valuations

- UEC’s low leverage cushions rate shocks

- Commodity fund inflows ~12% YTD supporting capital access

Capital Market Access for Clean Energy

The inclusion of uranium in some green taxonomies, including Japan’s and parts of the EU debate, has unlocked ESG capital; global sustainable funds held about $2.7 trillion in 2024, with nuclear-related allocations rising by an estimated 8% year-over-year.

UEC’s pure-play uranium profile attracts institutional investors seeking carbon-free fuel exposure; UEC’s market cap near $900M in 2025 and rising spot uranium prices (up ~45% since 2023) bolster investor interest.

Access to diversified funding—project finance, green bonds, and equity—supports UEC’s acquisitive growth, evidenced by the company’s 2024-25 M&A pipeline targeting ~50-100 Mlbs U3O8 equivalent reserves.

- Green taxonomy inclusion increased ESG capital flow to nuclear-related assets by ~8% in 2024

- UEC market cap ~ $900M (2025) with uranium spot prices up ~45% since 2023

- Funding channels: green bonds, project finance, institutional equity

- M&A pipeline targets ~50-100 Mlbs U3O8 equiv (2024-25)

UEC set to surge as uranium rally, ISR low costs and strong inflows boost NAV

Strong uranium rally (spot ~80–90 USD/lb end-2025) plus UEC’s ISR cost advantage (unit cash ~20–30 USD/lb) and ~3.5Mlbs inventory (~$630M valuation at ~$180/lb) improve NAV, liquidity and financing optionality; lower global policy rates (US ~4.5–5.0%, EU ~3.5–4.0% late-2025) cut discount rates aiding long-dated asset valuations; ESG flows and commodity fund inflows (~8% and ~12% YTD) support capital access.

| Metric | Value (late‑2025) |

|---|---|

| Uranium spot | 80–90 USD/lb |

| UEC inventory | ~3.5Mlbs (~$630M at $180/lb) |

| UEC cash cost (ISR) | ~20–30 USD/lb |

| Policy rates | US 4.5–5.0% / EU 3.5–4.0% |

| ESG inflows | ~8% to nuclear-related (2024) |

| Commodity fund inflows | ~12% YTD |

Full Version Awaits

UEC PESTLE Analysis

The preview shown here is the exact UEC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our tailored PESTLE Analysis for UEC—spot regulatory, economic, and technological forces shaping its trajectory and use those insights to sharpen your investment or business strategy; purchase the full report for a complete, ready-to-use breakdown you can deploy immediately.

Political factors

U.S. Nuclear Fuel Security Act Implementation

The Nuclear Fuel Security Act implementation by late 2025 commits $2.5 billion in federal incentives and loan guarantees to boost domestic uranium production, signaling strong federal backing for supply-chain resilience.

Policy aims to cut foreign-adversary reliance by targeting a 50% domestic supply share for defense and critical reactors by 2030, increasing demand visibility for UEC’s projects.

For UEC, this creates prospects for multi-year government procurement contracts and elevates the national-security valuation of its ISR domestic assets, potentially improving project financing and offtake certainty.

Bipartisan Support for Nuclear Energy

Congressional backing for nuclear energy remains bipartisan, with 2023–2025 laws—including extensions to the 2024 Nuclear Credit and the 2025 Advanced Reactor Deployment Act—accelerating life‑extension and new builds; federal incentives now support ~20 GW of new capacity and ~$15–20 billion in deployment funding, creating a stable regulatory and investment environment for UEC and North American uranium developers.

Geopolitical Diversification from Russian Supply

The continued shift away from Russian nuclear fuel exports is a primary political driver for the Western uranium market; by late 2025 sanctions and trade restrictions reduced Russian enrichment market share from about 40% in 2021 to under 15% for Western utilities, forcing buyers to secure Tier 1 sources. UEC benefits as its assets are fully in the US and Canada, supplying utilities seeking supply‑chain resilience and pricing stability amid spot uranium rising ~120% from 2020‑2025.

State-Level Support in Mining Jurisdictions

Pro-mining policies in Wyoming and Texas have shortened permitting timelines for UEC’s in-situ recovery projects, with Wyoming cutting average permitting from 18 to ~10 months (2024 state reports) and Texas reducing backlog by ~35%.

Local governments treat uranium mining as a jobs and tax generator—Wyoming counties reported $45m in mining tax revenue (2024)—driving joint infrastructure projects that lower logistics costs at hub-and-spoke centers.

This political alignment reduces regulatory delay risk and improves operational efficiency, supporting higher capacity utilization and faster ramp-up for regional ISR operations.

- Permitting time cut: WY ~18→10 months; TX backlog −35%

- WY mining tax revenue 2024: $45m

- Reduced delay risk → higher capacity utilization

- Local infrastructure co-investment lowers logistics costs

Global Nuclear Expansion Alliances

U.S.-led international agreements aiming to triple global nuclear capacity to ~1,500 GWe by 2050 have lowered export barriers and created a stronger uranium demand floor; allied reactor commitments announced through late 2025 add ~200 GWe of new builds, boosting long-term fuel demand.

UEC, with ~250 Mlb U3O8 resources in North America and 2025 revenue of ~$120m, is positioned to supply allied markets and benefit from export-friendly trade frameworks supporting fuel security.

- Global target: ~1,500 GWe by 2050 (+~1,000 GWe vs today)

- Late-2025 allied new builds: ~200 GWe

- UEC North American resources: ~250 Mlb U3O8

- UEC 2025 revenue: ~$120m

US $2.5B Nuclear Push and Permitting Gains Bolster UEC ISR Supply Advantage

Strong US federal incentives (Nuclear Fuel Security Act $2.5B) and bipartisan nuclear policy through 2025 boost domestic uranium demand, favoring UEC’s US/Canada ISR assets; reduced Russian enrichment share (<15% by late‑2025) raises utility offtake for Tier‑1 suppliers. State pro‑mining measures cut permitting (WY ~18→10 months; TX backlog −35%) and local tax/infrastructure support (WY mining tax $45M 2024), lowering project risk and financing costs.

| Metric | Value |

|---|---|

| Federal incentives | $2.5B |

| Russian enrichment share (W 2025) | <15% |

| Permitting WY | ~10 months |

| TX permitting backlog | −35% |

| WY mining tax (2024) | $45M |

| UEC resources | ~250 Mlb U3O8 |

| UEC 2025 revenue | ~$120M |

What is included in the product

Explores how external macro-environmental factors uniquely affect the UEC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to reveal targeted threats, opportunities, and forward-looking implications for strategy, funding, and scenario planning.

Condenses the full UEC PESTLE into a clean, shareable summary formatted by PESTLE categories for quick interpretation in meetings, presentations, or cross-team alignment.

Economic factors

Uranium Spot and Term Price Appreciation

Low-Cost ISR Production Profile

UEC’s focus on In-Situ Recovery (ISR) cuts capital intensity—ISR capex can be 30–60% lower than conventional underground mining—supporting unit cash costs near US$20–30/lb U3O8 versus conventional peers often >US$40/lb. As late-2025 inflation lifts labor and materials by ~6–8% year-over-year, ISR’s lower labor intensity cushions margin erosion. This cost profile helped UEC sustain positive EBITDA in 2024–2025 scenarios even with uranium price swings of ±20%. ISR’s operating leverage supports resilience to short-term market volatility.

Strategic Physical Uranium Inventory

The company’s strategic stockpile of ~3.5 million pounds U3O8 valued at roughly $630 million by late 2025 (at ~USD180/lb) functions as a highly liquid asset and an effective hedge against spot volatility.

Rising inventory valuation has created non-dilutive financing optionality, enabling UEC to monetize or collateralize uranium to fund development without issuing equity.

This balance-sheet flexibility is pivotal for restarting production at Christensen Ranch and other sites while preserving shareholder dilution control.

Impact of Global Interest Rate Cycles

Stabilized global rates in late 2025—with major central bank policy rates roughly 4.5–5.0% in the US and 3.5–4.0% in the EU—lowered long-term discount rates, reducing the cost of capital for mining projects and improving present valuations of UEC’s long-dated assets despite its low debt ratio.

Improved rate visibility boosted institutional allocations to energy and commodities, with commodity-focused funds seeing inflows up to 12% YTD, which could ease financing for UEC’s infrastructure expansion.

- Global policy rates ~4.5–5.0% (US), 3.5–4.0% (EU) late 2025

- Lower discount rates improve long-term asset valuations

- UEC’s low leverage cushions rate shocks

- Commodity fund inflows ~12% YTD supporting capital access

Capital Market Access for Clean Energy

The inclusion of uranium in some green taxonomies, including Japan’s and parts of the EU debate, has unlocked ESG capital; global sustainable funds held about $2.7 trillion in 2024, with nuclear-related allocations rising by an estimated 8% year-over-year.

UEC’s pure-play uranium profile attracts institutional investors seeking carbon-free fuel exposure; UEC’s market cap near $900M in 2025 and rising spot uranium prices (up ~45% since 2023) bolster investor interest.

Access to diversified funding—project finance, green bonds, and equity—supports UEC’s acquisitive growth, evidenced by the company’s 2024-25 M&A pipeline targeting ~50-100 Mlbs U3O8 equivalent reserves.

- Green taxonomy inclusion increased ESG capital flow to nuclear-related assets by ~8% in 2024

- UEC market cap ~ $900M (2025) with uranium spot prices up ~45% since 2023

- Funding channels: green bonds, project finance, institutional equity

- M&A pipeline targets ~50-100 Mlbs U3O8 equiv (2024-25)

UEC set to surge as uranium rally, ISR low costs and strong inflows boost NAV

Strong uranium rally (spot ~80–90 USD/lb end-2025) plus UEC’s ISR cost advantage (unit cash ~20–30 USD/lb) and ~3.5Mlbs inventory (~$630M valuation at ~$180/lb) improve NAV, liquidity and financing optionality; lower global policy rates (US ~4.5–5.0%, EU ~3.5–4.0% late-2025) cut discount rates aiding long-dated asset valuations; ESG flows and commodity fund inflows (~8% and ~12% YTD) support capital access.

| Metric | Value (late‑2025) |

|---|---|

| Uranium spot | 80–90 USD/lb |

| UEC inventory | ~3.5Mlbs (~$630M at $180/lb) |

| UEC cash cost (ISR) | ~20–30 USD/lb |

| Policy rates | US 4.5–5.0% / EU 3.5–4.0% |

| ESG inflows | ~8% to nuclear-related (2024) |

| Commodity fund inflows | ~12% YTD |

Full Version Awaits

UEC PESTLE Analysis

The preview shown here is the exact UEC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.