Unibail-Rodamco-Westfield Porter's Five Forces Analysis

From Overview to Strategy Blueprint

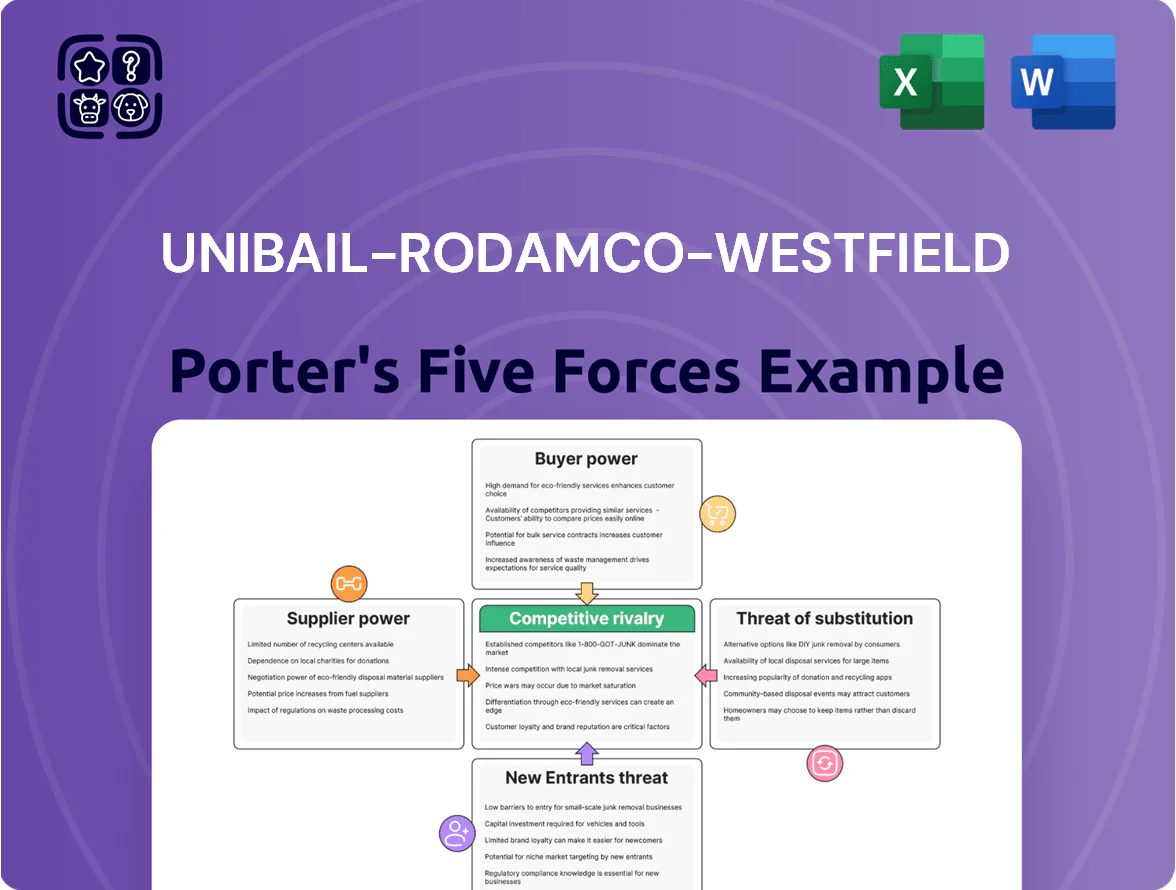

Unibail-Rodamco-Westfield faces intense rivalry from online retail and shifting tenant mixes, while landlord bargaining power and capital intensity moderate entrant threats—consumer behavior and ESG trends magnify strategic risks and opportunities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Unibail-Rodamco-Westfield’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Construction and Maintenance Services

The group relies on a handful of large contractors for flagship projects; in 2024 URW spent ~€850m on capex and refurbishments, so these firms hold moderate pricing leverage given project scale.

URW’s push for sustainable upgrades through 2025 (target: 100% BREEAM/LEED for major assets) raises demand for specialized trades, keeping contractor margins and timeline control elevated.

Technical labor shortages in Europe and the US—construction vacancy rates near 6% in 2024—further bolster supplier bargaining power across URW’s markets.

Energy and Utility Cost Management

Energy providers are a major supplier group as Unibail‑Rodamco‑Westfield (URW) pushes to meet Better Places 2025 targets; in 2024 URW reported 32% of consumption from renewables but still buys large volumes from utilities. URW’s €45bn portfolio and long‑term contracts let it negotiate bulk rates, yet 2021–2024 global gas price spikes made URW largely a price taker for essential utilities. To cut this supplier power URW is investing in on‑site renewables and storage—aiming to add 200+ MW of capacity by 2025—to lock in lower, more predictable energy costs.

Financial Capital and Debt Markets

As a capital‑intensive REIT, Unibail‑Rodamco‑Westfield (URW) depended on ~€9.1bn net debt at end‑2024, so banks and bondholders hold strong bargaining power over refinancing and liquidity terms.

Frequent access to credit markets is essential to fund its €3.6bn development pipeline (2025 plan), keeping financial institutions’ leverage high on covenant terms and pricing.

Credit ratings matter: S&P’s BBB‑/stable (Dec 2024) pushed URW’s average bond yield spread higher, directly raising borrowing costs and lender influence.

Specialized Technology and PropTech Vendors

Specialized proptech vendors hold notable leverage over Unibail‑Rodamco‑Westfield (URW) because their proprietary software and data analytics are crucial for digital customer experiences and smart building ops; industry estimates show retail real‑estate tech spend rose ~18% y/y in 2024 to €1.6bn across European malls.

High integration and data migration costs mean switching platforms often exceeds €2–5m per large site, strengthening vendors' bargaining power at renewal.

- Proptech spend: €1.6bn Europe 2024

- Retail‑tech growth: +18% y/y 2024

- Switch cost per large site: €2–5m

- Proprietary data = renewal leverage

Municipalities and Local Government Agencies

Local authorities supply land-use rights, zoning permits, and infrastructure links that URW must secure to develop or expand; without them projects stall and costs rise.

Their power is near-absolute: URW must meet local planning rules and public consultation requirements before opening or refurbishing centres, which can add months and millions in delay costs.

By 2025, green certifications (BREEAM, HQE) and social-impact metrics drive approvals; failure risks permit denial and higher capex—URW reported €1.2bn ESG-related investment guidance for 2024–25.

- Permits/control: decisive for site feasibility

- Timing: approvals add months; late costs millions

- ESG: €1.2bn ESG spend 2024–25 affects approvals

Suppliers wield rising power as €850m capex, €9.1bn debt and tech costs tighten leverage

Suppliers hold moderate‑to‑high power: contractors and specialized trades gain from €850m capex (2024) and sustainability retrofits; energy/vendors exert sway despite bulk procurement—32% renewables in 2024, 200+ MW on‑site target by 2025; lenders control refinancing over €9.1bn net debt (end‑2024). Technical shortages (construction vacancy ~6% in 2024) and proptech switch costs (€2–5m/site) reinforce supplier leverage.

| Item | 2024–25 figure |

|---|---|

| Capex/refurbs | €850m (2024) |

| Net debt | €9.1bn (end‑2024) |

| Renewables | 32% (2024) |

| On‑site goal | 200+ MW (by 2025) |

| Construction vacancy | ~6% (2024) |

| Proptech switch cost | €2–5m/site |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Unibail-Rodamco-Westfield, uncovering competitive intensity, buyer/supplier power, entry barriers, threat of substitutes, and strategic implications for mall portfolio resilience and profitability.

A concise Porter's Five Forces snapshot for Unibail-Rodamco-Westfield—quickly assess retail property bargaining power, competitive rivalry, tenant threat, supplier influence, and regulatory risk for faster strategic decisions.

Customers Bargaining Power

Dominance of Global Retail Powerhouses

Shift Toward Turnover Based Rent Structures

By end-2025 roughly 40–50% of URW leases include turnover-based rent, boosting tenant leverage as landlords now shoulder more revenue risk; tenants press for clearer sell-through data and ROI-linked marketing support. Retailers demand monthly sales reporting and co-funded promotions—URW reported a 22% growth in turnover-rent schemes in 2024, cutting fixed-rent exposure and raising negotiation power on service charges and tenant mix.

Availability of Alternative Distribution Channels

Retailers treat stores as part of omnichannel mixes, so tenants can leave centres that underdeliver on ROI or visibility; industry data shows 56% of European retailers closed or downsized stores in 2023 to focus on online and flagship formats.

URW mitigates this by concentrating on 87 core prime assets (2024 portfolio) and investing €1.2bn in experiential upgrades in 2023–24 to offer events, dining, and leisure that e-commerce cannot match.

Office Tenant Requirements for Flexibility

Corporate tenants now demand flexible leases and premium amenities to support hybrid work; surveys in 2024 show 68% of occupiers prefer flexible terms and 54% cite ESG features as decisive.

If URW fails to offer state‑of‑the‑art, sustainable, well‑connected offices, large clients can downsize or shift to agile operators, increasing vacancy and lowering rents.

The market for high‑quality commercial space gives bargaining power to top corporate tenants, pressuring URW on lease length, fit‑out costs, and service levels.

- 68% occupier preference for flexible terms (2024)

- 54% prioritize ESG features (2024)

- Higher churn risk if upgrades delayed

Convention and Exhibition Organizer Demands

Prime retail strength: URW 95% occupancy, turnover rents surge +22% as corporates demand flex

| Metric | Value |

|---|---|

| URW occupancy 2024 | ~95% |

| Turnover rent share (end‑2025) | 40–50% |

| Turnover‑rent growth 2024 | +22% |

| LVMH revenue 2024 | €79.2bn |

| Inditex revenue 2024 | €32.6bn |

| Core assets 2024 | 87 |

| Experiential capex 2023–24 | €1.2bn |

| Occupier flexible pref. 2024 | 68% |

| Occupier ESG priority 2024 | 54% |

| MICE spend vs 2022 (2024) | +28% |

Full Version Awaits

Unibail-Rodamco-Westfield Porter's Five Forces Analysis

This preview shows the exact Unibail‑Rodamco‑Westfield Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download upon purchase; no samples, no placeholders, just the complete deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Unibail-Rodamco-Westfield faces intense rivalry from online retail and shifting tenant mixes, while landlord bargaining power and capital intensity moderate entrant threats—consumer behavior and ESG trends magnify strategic risks and opportunities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Unibail-Rodamco-Westfield’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Construction and Maintenance Services

The group relies on a handful of large contractors for flagship projects; in 2024 URW spent ~€850m on capex and refurbishments, so these firms hold moderate pricing leverage given project scale.

URW’s push for sustainable upgrades through 2025 (target: 100% BREEAM/LEED for major assets) raises demand for specialized trades, keeping contractor margins and timeline control elevated.

Technical labor shortages in Europe and the US—construction vacancy rates near 6% in 2024—further bolster supplier bargaining power across URW’s markets.

Energy and Utility Cost Management

Energy providers are a major supplier group as Unibail‑Rodamco‑Westfield (URW) pushes to meet Better Places 2025 targets; in 2024 URW reported 32% of consumption from renewables but still buys large volumes from utilities. URW’s €45bn portfolio and long‑term contracts let it negotiate bulk rates, yet 2021–2024 global gas price spikes made URW largely a price taker for essential utilities. To cut this supplier power URW is investing in on‑site renewables and storage—aiming to add 200+ MW of capacity by 2025—to lock in lower, more predictable energy costs.

Financial Capital and Debt Markets

As a capital‑intensive REIT, Unibail‑Rodamco‑Westfield (URW) depended on ~€9.1bn net debt at end‑2024, so banks and bondholders hold strong bargaining power over refinancing and liquidity terms.

Frequent access to credit markets is essential to fund its €3.6bn development pipeline (2025 plan), keeping financial institutions’ leverage high on covenant terms and pricing.

Credit ratings matter: S&P’s BBB‑/stable (Dec 2024) pushed URW’s average bond yield spread higher, directly raising borrowing costs and lender influence.

Specialized Technology and PropTech Vendors

Specialized proptech vendors hold notable leverage over Unibail‑Rodamco‑Westfield (URW) because their proprietary software and data analytics are crucial for digital customer experiences and smart building ops; industry estimates show retail real‑estate tech spend rose ~18% y/y in 2024 to €1.6bn across European malls.

High integration and data migration costs mean switching platforms often exceeds €2–5m per large site, strengthening vendors' bargaining power at renewal.

- Proptech spend: €1.6bn Europe 2024

- Retail‑tech growth: +18% y/y 2024

- Switch cost per large site: €2–5m

- Proprietary data = renewal leverage

Municipalities and Local Government Agencies

Local authorities supply land-use rights, zoning permits, and infrastructure links that URW must secure to develop or expand; without them projects stall and costs rise.

Their power is near-absolute: URW must meet local planning rules and public consultation requirements before opening or refurbishing centres, which can add months and millions in delay costs.

By 2025, green certifications (BREEAM, HQE) and social-impact metrics drive approvals; failure risks permit denial and higher capex—URW reported €1.2bn ESG-related investment guidance for 2024–25.

- Permits/control: decisive for site feasibility

- Timing: approvals add months; late costs millions

- ESG: €1.2bn ESG spend 2024–25 affects approvals

Suppliers wield rising power as €850m capex, €9.1bn debt and tech costs tighten leverage

Suppliers hold moderate‑to‑high power: contractors and specialized trades gain from €850m capex (2024) and sustainability retrofits; energy/vendors exert sway despite bulk procurement—32% renewables in 2024, 200+ MW on‑site target by 2025; lenders control refinancing over €9.1bn net debt (end‑2024). Technical shortages (construction vacancy ~6% in 2024) and proptech switch costs (€2–5m/site) reinforce supplier leverage.

| Item | 2024–25 figure |

|---|---|

| Capex/refurbs | €850m (2024) |

| Net debt | €9.1bn (end‑2024) |

| Renewables | 32% (2024) |

| On‑site goal | 200+ MW (by 2025) |

| Construction vacancy | ~6% (2024) |

| Proptech switch cost | €2–5m/site |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Unibail-Rodamco-Westfield, uncovering competitive intensity, buyer/supplier power, entry barriers, threat of substitutes, and strategic implications for mall portfolio resilience and profitability.

A concise Porter's Five Forces snapshot for Unibail-Rodamco-Westfield—quickly assess retail property bargaining power, competitive rivalry, tenant threat, supplier influence, and regulatory risk for faster strategic decisions.

Customers Bargaining Power

Dominance of Global Retail Powerhouses

Shift Toward Turnover Based Rent Structures

By end-2025 roughly 40–50% of URW leases include turnover-based rent, boosting tenant leverage as landlords now shoulder more revenue risk; tenants press for clearer sell-through data and ROI-linked marketing support. Retailers demand monthly sales reporting and co-funded promotions—URW reported a 22% growth in turnover-rent schemes in 2024, cutting fixed-rent exposure and raising negotiation power on service charges and tenant mix.

Availability of Alternative Distribution Channels

Retailers treat stores as part of omnichannel mixes, so tenants can leave centres that underdeliver on ROI or visibility; industry data shows 56% of European retailers closed or downsized stores in 2023 to focus on online and flagship formats.

URW mitigates this by concentrating on 87 core prime assets (2024 portfolio) and investing €1.2bn in experiential upgrades in 2023–24 to offer events, dining, and leisure that e-commerce cannot match.

Office Tenant Requirements for Flexibility

Corporate tenants now demand flexible leases and premium amenities to support hybrid work; surveys in 2024 show 68% of occupiers prefer flexible terms and 54% cite ESG features as decisive.

If URW fails to offer state‑of‑the‑art, sustainable, well‑connected offices, large clients can downsize or shift to agile operators, increasing vacancy and lowering rents.

The market for high‑quality commercial space gives bargaining power to top corporate tenants, pressuring URW on lease length, fit‑out costs, and service levels.

- 68% occupier preference for flexible terms (2024)

- 54% prioritize ESG features (2024)

- Higher churn risk if upgrades delayed

Convention and Exhibition Organizer Demands

Prime retail strength: URW 95% occupancy, turnover rents surge +22% as corporates demand flex

| Metric | Value |

|---|---|

| URW occupancy 2024 | ~95% |

| Turnover rent share (end‑2025) | 40–50% |

| Turnover‑rent growth 2024 | +22% |

| LVMH revenue 2024 | €79.2bn |

| Inditex revenue 2024 | €32.6bn |

| Core assets 2024 | 87 |

| Experiential capex 2023–24 | €1.2bn |

| Occupier flexible pref. 2024 | 68% |

| Occupier ESG priority 2024 | 54% |

| MICE spend vs 2022 (2024) | +28% |

Full Version Awaits

Unibail-Rodamco-Westfield Porter's Five Forces Analysis

This preview shows the exact Unibail‑Rodamco‑Westfield Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download upon purchase; no samples, no placeholders, just the complete deliverable.