USD Partners PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, energy markets, and environmental regulations are shaping USD Partners' strategic outlook in our concise PESTLE snapshot—designed to help investors and strategists spot risk and opportunity quickly; purchase the full PESTLE for a detailed, editable report that powers better decisions.

Political factors

Cross-Border Energy Trade Policy

The US-Canada relationship is crucial for USD Partners, which operates Hardisty and Stroud terminals linking cross-border flows; Canada exported 3.1 million b/d of crude in 2024, making policy shifts material to throughput.

Political stability and trade rules on Western Canadian Select affect volumes and revenue; a 10% tariff scenario could reroute ~150–200 kb/d off rail, cutting utilization and fee income.

By late 2025, changes to North American trade alliances or energy import tariffs would reshape competition for rail-based midstream services and impact midstream margins and capital allocation.

Federal Pipeline Oversight and Approvals

Federal oversight of projects like the Trans Mountain Expansion—now facing cost increases to roughly CAD 30–35 billion and ongoing legal/political delays—boosts demand for crude-by-rail, benefiting USD Partners terminal throughput which handled about 4.5 million barrels of crude transload capacity in 2024.

Energy Independence and Security Mandates

Government initiatives for North American energy independence bolster midstream operators like USD Partners, which handled ~$1.2 billion in throughput volumes in 2024, supporting domestic distribution networks.

2025 political focus on reducing overseas oil reliance has translated into increased approvals and potential incentives for heavy crude corridors, benefiting pipelines moving ~600 kbpd from Canada to U.S. refineries.

This geopolitical stance cements USD Partners as a critical link in the regional supply chain, helping stabilize fee-based EBITDA against global price volatility.

Biofuel Subsidy and Incentive Programs

Political support for energy transition has driven federal tax credits like the $1.00/gal RIN-equivalent incentives and Renewable Fuel Standard blending mandates, boosting demand for terminals handling ethanol and renewable diesel where USD Partners has grown assets.

USD Partners’ biofuels-oriented terminals saw utilization gains; industry data show renewable diesel production in the US rose to ~1.6 billion gallons in 2024, supporting terminal throughput and fee-based revenue.

Shifts in congressional appetite for green subsidies through 2026 could either accelerate EBITDA growth for USD’s biofuels segment if credits persist or compress volumes and margins if support is withdrawn.

- Federal tax credits and RFS mandates support steady terminal demand

- US renewable diesel production ~1.6B gallons in 2024

- Policy changes through 2026 are key upside/downside risk to segment EBITDA

Election Cycle Regulatory Uncertainty

Following the 2024 US elections, shifts in DOT and DOE priorities could alter rail safety rules and infrastructure funding, affecting USD Partners’ US$200–300m terminal capex plans and 2025 throughput targets (≈15–20% growth in intermodal volumes).

New administration-led rail safety standards and grant allocations may require operational adjustments to maintain continuity across USD Partners’ leased terminals and protected cash flows.

- DOT/DOE policy shifts can change rail safety compliance costs and timing

- Potential reallocation of infrastructure grants impacts terminal upgrade financing

- Agility required to protect contracted cash flows and throughput growth targets

Trade, pipelines, and biofuels drive USD Partners volumes amid capex, rail and policy headwinds

US-Canada trade policy, Trans Mountain delays (cost ~CAD 30–35B), and 2024 flows (Canada export 3.1M b/d; USD Partners transload capacity 4.5M bbl; throughput ~$1.2B revenue) drive USD Partners’ volumes; biofuels support (US renewable diesel ~1.6B gal in 2024) and DOT/DOE rail rules affect capex ($200–300M) and 2025 throughput targets (~15–20% intermodal growth).

| Metric | 2024/2025 |

|---|---|

| Canada crude exports | 3.1M b/d (2024) |

| USD Partners transload cap. | 4.5M bbl (2024) |

| Throughput revenue | $1.2B (2024) |

| Renewable diesel | 1.6B gal (2024) |

| Planned capex | $200–300M |

What is included in the product

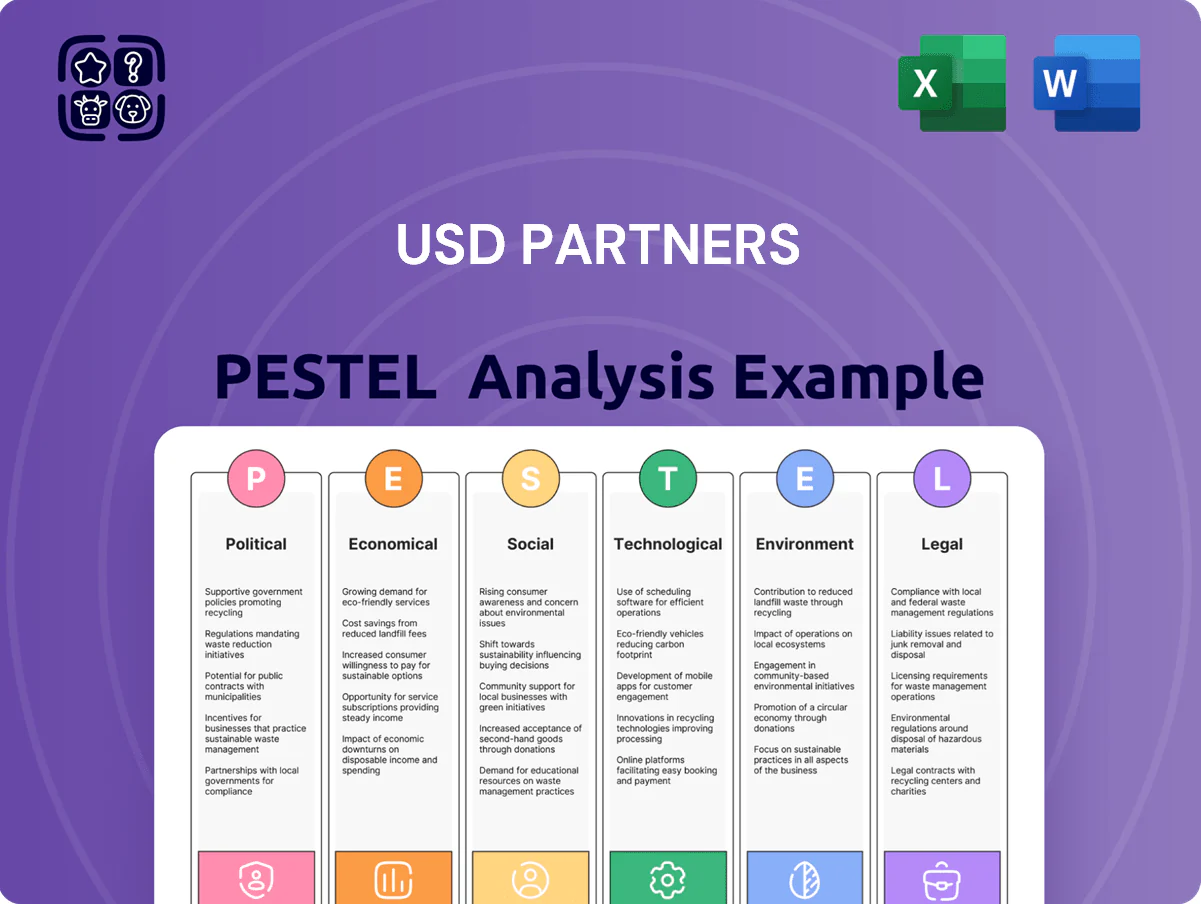

Explores how macro-environmental factors uniquely affect USD Partners across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current market and regulatory trends to highlight risks and opportunities.

Condensed PESTLE insights for USD Partners presented by category to speed strategic discussions and provide a shareable, slide-ready summary for cross-team alignment.

Economic factors

WCS to WTI Crude Price Differentials

The rail terminals’ economics hinge on the WCS–WTI differential; a wider spread incentivizes rail shipments from Western Canada to Gulf Coast refineries. In 2024-25 the differential averaged about 18–22 USD/bbl, and spikes above 25 USD/bbl historically drove higher rail volumes. Analysts tracking spreads into late 2025 use these levels to model throughput and revenue for Hardisty and Stroud, with each $1/bbl change shifting annual gross margin by several million dollars.

Interest Rate Environment and Cost of Debt

As a capital-intensive midstream partnership, USD Partners is highly sensitive to interest rates that determine its weighted average cost of debt; higher rates raise annual interest expense and capex financing costs. After volatile 2022–2024 tightening, U.S. policy rates stabilized around 5.25–5.50% by late 2025, improving predictability for refinancing and M&A funding. Elevated borrowing costs through 2024 trimmed expansion headroom, constraining terminal capacity additions and tech investments, making Fed policy a critical economic indicator for growth.

Global Demand for Heavy Crude Refining

The economic health of USD Partners ties to U.S. Gulf Coast complex refining capacity built for heavy Canadian crude; Gulf Coast refiners processed about 3.8 million b/d of heavy sour crude in 2024, supporting steady demand for logistics. Strong 2024–25 global refined-product demand—petroleum products consumption ~100.2 million b/d in 2024 OECD+non-OECD mix—keeps refineries seeking reliable feedstock and sustains USD Partners’ volumes. A deep global downturn cutting fuel use (e.g., a 5–10% demand shock) would directly reduce throughput and midstream revenue.

Inflationary Pressure on Operational Costs

Persistent inflation through 2024–2025—US CPI running near 3.4% year-over-year in early 2025—raises labor, materials, and energy costs for USD Partners’ rail terminals and storage, increasing operating expense pressure.

Long-term fee-based contracts limit revenue volatility, but rising opex can compress margins unless cost controls, efficiency gains, and selective pass-throughs to customers are executed.

- 2024–25 US CPI ≈ 3.4% YoY

- Energy and diesel up 10–15% vs. 2023 in some regions

- Fee-based contracts cover revenue risk but not all opex inflation

- Cost controls and customer pass-throughs essential to protect margins

Biofuel Market Penetration and Pricing

The shift to renewables forces USD Partners to retrofit terminals for ethanol/renewable diesel; in 2024 U.S. ethanol production averaged about 13.4 billion gallons and renewable diesel capacity reached ~3.9 billion gallons, creating utilization opportunities and conversion costs.

Ethanol and renewable diesel pricing—tied to corn, soybean oil and RINs—drove 2024 averages: Midwest ethanol rack ~$2.10/gal, renewable diesel ~$3.50–$4.00/gal, affecting terminal throughput and margins.

Raising renewable-product share (targeting >20% of throughput) diversifies revenue, reducing volatility from 2023–24 crude price swings and supporting long-term utilization stability.

- 2024 U.S. ethanol 13.4B gal; renewable diesel ~3.9B gal capacity

- 2024 price ranges: ethanol ~$2.10/gal, renewable diesel $3.50–$4.00/gal

- Targeting >20% renewable throughput to mitigate crude volatility

Rail margins driven by WCS–WTI spreads, rates and Gulf Coast fuel demand

Rail economics hinge on WCS–WTI spreads (~18–22 USD/bbl in 2024–25); each $1/bbl shift moves annual gross margin by several million. U.S. policy rates ~5.25–5.50% by late 2025 raise financing costs; CPI ~3.4% in early 2025 lifts opex. Gulf Coast heavy crude demand ~3.8M b/d (2024) and renewables capacity (ethanol 13.4B gal, renewable diesel 3.9B gal) shape throughput diversification.

| Metric | 2024–25 |

|---|---|

| WCS–WTI spread | 18–22 USD/bbl |

| Fed funds (late 2025) | 5.25–5.50% |

| US CPI (early 2025) | ~3.4% YoY |

| Gulf Coast heavy crude | 3.8M b/d |

| Ethanol | 13.4B gal |

| Renewable diesel | 3.9B gal |

What You See Is What You Get

USD Partners PESTLE Analysis

The preview shown here is the exact USD Partners PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, energy markets, and environmental regulations are shaping USD Partners' strategic outlook in our concise PESTLE snapshot—designed to help investors and strategists spot risk and opportunity quickly; purchase the full PESTLE for a detailed, editable report that powers better decisions.

Political factors

Cross-Border Energy Trade Policy

The US-Canada relationship is crucial for USD Partners, which operates Hardisty and Stroud terminals linking cross-border flows; Canada exported 3.1 million b/d of crude in 2024, making policy shifts material to throughput.

Political stability and trade rules on Western Canadian Select affect volumes and revenue; a 10% tariff scenario could reroute ~150–200 kb/d off rail, cutting utilization and fee income.

By late 2025, changes to North American trade alliances or energy import tariffs would reshape competition for rail-based midstream services and impact midstream margins and capital allocation.

Federal Pipeline Oversight and Approvals

Federal oversight of projects like the Trans Mountain Expansion—now facing cost increases to roughly CAD 30–35 billion and ongoing legal/political delays—boosts demand for crude-by-rail, benefiting USD Partners terminal throughput which handled about 4.5 million barrels of crude transload capacity in 2024.

Energy Independence and Security Mandates

Government initiatives for North American energy independence bolster midstream operators like USD Partners, which handled ~$1.2 billion in throughput volumes in 2024, supporting domestic distribution networks.

2025 political focus on reducing overseas oil reliance has translated into increased approvals and potential incentives for heavy crude corridors, benefiting pipelines moving ~600 kbpd from Canada to U.S. refineries.

This geopolitical stance cements USD Partners as a critical link in the regional supply chain, helping stabilize fee-based EBITDA against global price volatility.

Biofuel Subsidy and Incentive Programs

Political support for energy transition has driven federal tax credits like the $1.00/gal RIN-equivalent incentives and Renewable Fuel Standard blending mandates, boosting demand for terminals handling ethanol and renewable diesel where USD Partners has grown assets.

USD Partners’ biofuels-oriented terminals saw utilization gains; industry data show renewable diesel production in the US rose to ~1.6 billion gallons in 2024, supporting terminal throughput and fee-based revenue.

Shifts in congressional appetite for green subsidies through 2026 could either accelerate EBITDA growth for USD’s biofuels segment if credits persist or compress volumes and margins if support is withdrawn.

- Federal tax credits and RFS mandates support steady terminal demand

- US renewable diesel production ~1.6B gallons in 2024

- Policy changes through 2026 are key upside/downside risk to segment EBITDA

Election Cycle Regulatory Uncertainty

Following the 2024 US elections, shifts in DOT and DOE priorities could alter rail safety rules and infrastructure funding, affecting USD Partners’ US$200–300m terminal capex plans and 2025 throughput targets (≈15–20% growth in intermodal volumes).

New administration-led rail safety standards and grant allocations may require operational adjustments to maintain continuity across USD Partners’ leased terminals and protected cash flows.

- DOT/DOE policy shifts can change rail safety compliance costs and timing

- Potential reallocation of infrastructure grants impacts terminal upgrade financing

- Agility required to protect contracted cash flows and throughput growth targets

Trade, pipelines, and biofuels drive USD Partners volumes amid capex, rail and policy headwinds

US-Canada trade policy, Trans Mountain delays (cost ~CAD 30–35B), and 2024 flows (Canada export 3.1M b/d; USD Partners transload capacity 4.5M bbl; throughput ~$1.2B revenue) drive USD Partners’ volumes; biofuels support (US renewable diesel ~1.6B gal in 2024) and DOT/DOE rail rules affect capex ($200–300M) and 2025 throughput targets (~15–20% intermodal growth).

| Metric | 2024/2025 |

|---|---|

| Canada crude exports | 3.1M b/d (2024) |

| USD Partners transload cap. | 4.5M bbl (2024) |

| Throughput revenue | $1.2B (2024) |

| Renewable diesel | 1.6B gal (2024) |

| Planned capex | $200–300M |

What is included in the product

Explores how macro-environmental factors uniquely affect USD Partners across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current market and regulatory trends to highlight risks and opportunities.

Condensed PESTLE insights for USD Partners presented by category to speed strategic discussions and provide a shareable, slide-ready summary for cross-team alignment.

Economic factors

WCS to WTI Crude Price Differentials

The rail terminals’ economics hinge on the WCS–WTI differential; a wider spread incentivizes rail shipments from Western Canada to Gulf Coast refineries. In 2024-25 the differential averaged about 18–22 USD/bbl, and spikes above 25 USD/bbl historically drove higher rail volumes. Analysts tracking spreads into late 2025 use these levels to model throughput and revenue for Hardisty and Stroud, with each $1/bbl change shifting annual gross margin by several million dollars.

Interest Rate Environment and Cost of Debt

As a capital-intensive midstream partnership, USD Partners is highly sensitive to interest rates that determine its weighted average cost of debt; higher rates raise annual interest expense and capex financing costs. After volatile 2022–2024 tightening, U.S. policy rates stabilized around 5.25–5.50% by late 2025, improving predictability for refinancing and M&A funding. Elevated borrowing costs through 2024 trimmed expansion headroom, constraining terminal capacity additions and tech investments, making Fed policy a critical economic indicator for growth.

Global Demand for Heavy Crude Refining

The economic health of USD Partners ties to U.S. Gulf Coast complex refining capacity built for heavy Canadian crude; Gulf Coast refiners processed about 3.8 million b/d of heavy sour crude in 2024, supporting steady demand for logistics. Strong 2024–25 global refined-product demand—petroleum products consumption ~100.2 million b/d in 2024 OECD+non-OECD mix—keeps refineries seeking reliable feedstock and sustains USD Partners’ volumes. A deep global downturn cutting fuel use (e.g., a 5–10% demand shock) would directly reduce throughput and midstream revenue.

Inflationary Pressure on Operational Costs

Persistent inflation through 2024–2025—US CPI running near 3.4% year-over-year in early 2025—raises labor, materials, and energy costs for USD Partners’ rail terminals and storage, increasing operating expense pressure.

Long-term fee-based contracts limit revenue volatility, but rising opex can compress margins unless cost controls, efficiency gains, and selective pass-throughs to customers are executed.

- 2024–25 US CPI ≈ 3.4% YoY

- Energy and diesel up 10–15% vs. 2023 in some regions

- Fee-based contracts cover revenue risk but not all opex inflation

- Cost controls and customer pass-throughs essential to protect margins

Biofuel Market Penetration and Pricing

The shift to renewables forces USD Partners to retrofit terminals for ethanol/renewable diesel; in 2024 U.S. ethanol production averaged about 13.4 billion gallons and renewable diesel capacity reached ~3.9 billion gallons, creating utilization opportunities and conversion costs.

Ethanol and renewable diesel pricing—tied to corn, soybean oil and RINs—drove 2024 averages: Midwest ethanol rack ~$2.10/gal, renewable diesel ~$3.50–$4.00/gal, affecting terminal throughput and margins.

Raising renewable-product share (targeting >20% of throughput) diversifies revenue, reducing volatility from 2023–24 crude price swings and supporting long-term utilization stability.

- 2024 U.S. ethanol 13.4B gal; renewable diesel ~3.9B gal capacity

- 2024 price ranges: ethanol ~$2.10/gal, renewable diesel $3.50–$4.00/gal

- Targeting >20% renewable throughput to mitigate crude volatility

Rail margins driven by WCS–WTI spreads, rates and Gulf Coast fuel demand

Rail economics hinge on WCS–WTI spreads (~18–22 USD/bbl in 2024–25); each $1/bbl shift moves annual gross margin by several million. U.S. policy rates ~5.25–5.50% by late 2025 raise financing costs; CPI ~3.4% in early 2025 lifts opex. Gulf Coast heavy crude demand ~3.8M b/d (2024) and renewables capacity (ethanol 13.4B gal, renewable diesel 3.9B gal) shape throughput diversification.

| Metric | 2024–25 |

|---|---|

| WCS–WTI spread | 18–22 USD/bbl |

| Fed funds (late 2025) | 5.25–5.50% |

| US CPI (early 2025) | ~3.4% YoY |

| Gulf Coast heavy crude | 3.8M b/d |

| Ethanol | 13.4B gal |

| Renewable diesel | 3.9B gal |

What You See Is What You Get

USD Partners PESTLE Analysis

The preview shown here is the exact USD Partners PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.