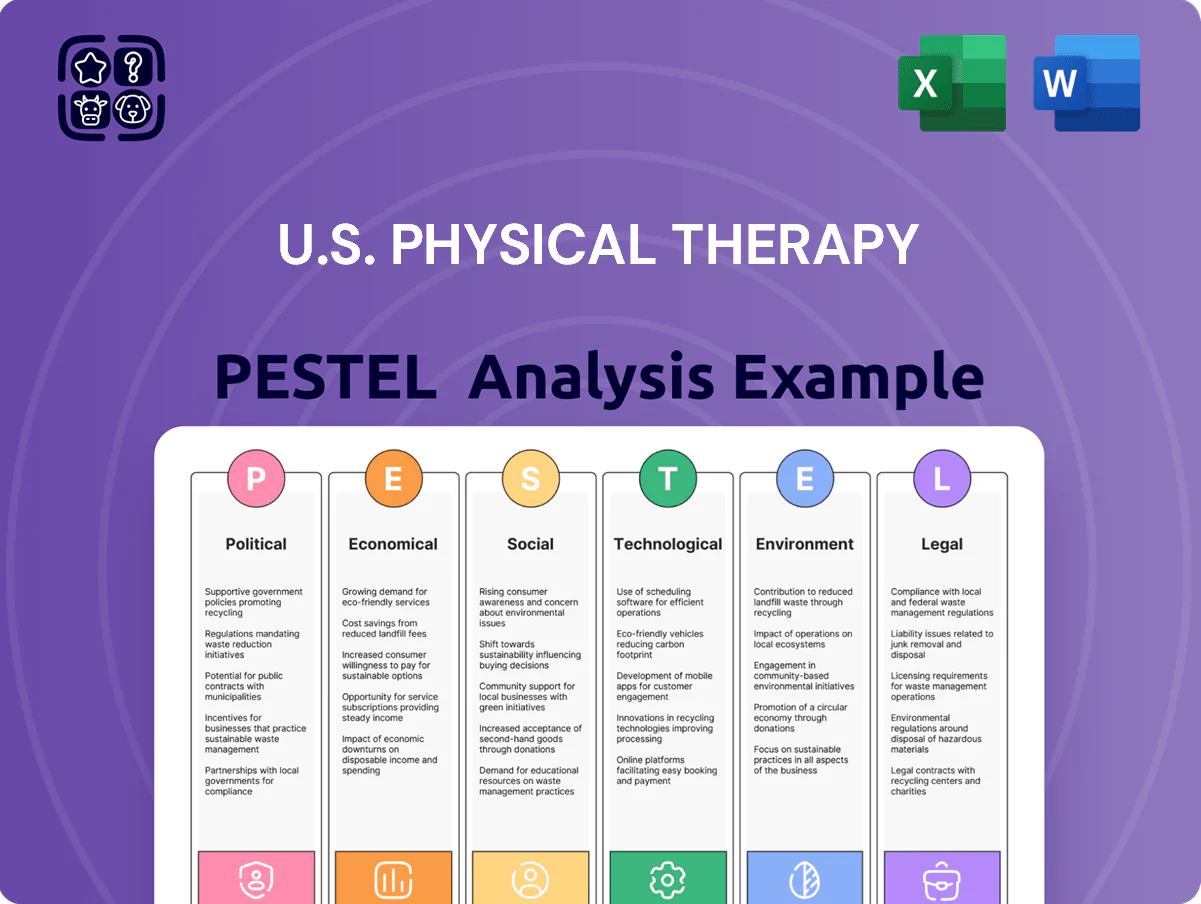

U.S. Physical Therapy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE analysis of U.S. Physical Therapy—uncover how regulation, reimbursement trends, tech adoption, and demographic shifts will shape growth and risk; perfect for investors and strategists. Purchase the full report to access actionable insights, editable charts, and recommendations you can use immediately.

Political factors

Medicare reimbursement policy shifts

Federal adjustments to the Physician Fee Schedule drive outpatient PT revenue; CMS cut the conversion factor by 3.5% in 2024 and proposed modest increases in 2025, while legislative action in late 2025 aims to stabilize the factor to avoid projected clinic revenue declines of up to 6–8% nationwide; the company must track CMS rulemaking and quarterly Medicare reimbursement updates to revise budgets and partner contracts accordingly.

Federal healthcare reform initiatives

Ongoing debates over expanding the Affordable Care Act or restructuring Medicare/Medicaid directly affect coverage; 2024 estimates show ~8.6% of nonelderly remain uninsured, influencing demand for physical therapy.

Shifts in federal control alter mandates and subsidies—e.g., ACA subsidy changes in 2023–24 correlated with enrollment swings of several million, changing payer mix for clinics.

U.S. Physical Therapy must adapt to policy swings to protect patient inflows and contract revenue, with Medicare accounting for roughly 35% of outpatient rehab payments as of 2024.

State-level direct access legislation

Political advocacy at the state level increasingly enables patients to access physical therapy without physician referral; as of Dec 2025, 37 states plus DC allow unrestricted or limited direct access, up from 30 in 2020, lowering entry barriers and shortening care pathways.

This shift reduces reliance on physician referral networks, raising the strategic value of direct-to-consumer marketing—practices with strong consumer channels can capture a larger share of the $42B outpatient PT market projected for 2025.

Labor and minimum wage regulations

Legislative changes to federal and state minimum wages and overtime rules raised labor costs for U.S. physical therapy clinics in 2024–25; 21 states increased minimum wages in 2024, with the federal overtime salary threshold proposed to rise from $35,568 (2023) toward ~$48,000 in some rule drafts, pressuring payroll budgets.

Political pressure to boost support-staff pay compresses margins if Medicare Part B and commercial reimbursement rates (Medicare therapy fee schedule growth ~1–2% annually) do not keep pace, increasing cost-per-visit by an estimated 3–7% for affected clinics.

Clinics must tailor workforce strategies by region—using mix of part-time clinicians, telehealth, and centralized admin hubs—to manage heterogeneous state labor laws and contain operating expense growth projected at 4–6% in higher-wage states.

- 21 states raised minimum wage in 2024

- Potential overtime threshold moves toward ~$48,000

- Payroll-driven cost-per-visit up 3–7%

- Operating expense growth 4–6% in high-wage states

Governmental focus on opioid reduction

Public health policies to curb the opioid crisis have elevated physical therapy as a frontline non-opioid pain management option, with Medicare expanding coverage for therapy-first pathways and CDC guidance encouraging nonpharmacologic care; opioid prescribing dropped 48% from 2012–2022, boosting demand for rehab services.

Political backing yields grant funding and favorable clinical guidelines—FY2024 federal opioid-related grants exceeded $7.5 billion—supporting clinic expansion, care integration, and higher reimbursement rates for nonpharmacologic interventions.

Alignment with national priorities creates a strategic tailwind for long-term growth, increasing referral volumes and revenue diversification as payers shift toward value-based models that reward reductions in opioid use and improved functional outcomes.

- Medicare policy shifts favor therapy-first pain care

- Opioid prescriptions down 48% (2012–2022)

- FY2024 federal opioid grants > $7.5B

- Stronger referrals, reimbursement, and value-based incentives

Medicare cuts, direct‑access gains and wage hikes reshape $42B outpatient PT market

Federal CMS cuts and legislative stabilizers shift Medicare revenue (Medicare ~35% of outpatient rehab payments; CF cut 3.5% in 2024; modest 2025 increases) while direct-access in 37 states (Dec 2025) expands addressable market (2025 outpatient PT market ~$42B); labor law changes (21 states raised minimum wage in 2024; OT threshold proposals ~ $48k) push operating costs up 3–7% per visit.

| Metric | Value |

|---|---|

| Medicare share | ~35% |

| Physician Fee Schedule CF 2024 | -3.5% |

| Direct access states (Dec 2025) | 37 |

| Outpatient PT market 2025 | $42B |

| States raised min wage 2024 | 21 |

| Payroll cost-per-visit impact | +3–7% |

What is included in the product

Explores how macro-environmental factors uniquely affect U.S. Physical Therapy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify threats, opportunities, and strategy implications for market positioning, funding, and operational resilience.

A concise U.S. Physical Therapy PESTLE summary that highlights regulatory shifts, reimbursement trends, demographic demand, technological adoption, and competitive dynamics for quick reference in meetings or client reports.

Economic factors

Inflationary pressure on operating costs

Persistently high costs for medical supplies, facility leases, and utilities squeezed margins in 2024–25, with healthcare CPI rising about 4.2% in 2024 and medical supply costs up ~6% year-over-year; fixed third-party reimbursement (Medicare median PT reimbursement down 0.5% real in 2023–24) limits price pass-through. Scale-based procurement and aggressive cost containment—bulk purchasing, lease renegotiation—are essential to preserve operating margins.

Interest rate environment and capital allocation

Rising interest rates have pushed US average corporate borrowing costs higher—10‑year Treasury moved from 1.5% in 2020 to ~4.0% by end‑2023 and CPI‑adjusted Fed funds near 5% in 2024—raising financing costs for U.S. Physical Therapy’s acquisition-funded growth and increasing annual interest expense on leveraged deals.

Labor market competition for clinicians

A nationwide shortage of physical therapists—APTA reported a 12% vacancy rise in 2024—has pushed average PT salaries up about 8% year-over-year, increasing recruitment and labor costs for providers.

Hospitals and private practices aggressively compete for clinicians, threatening revenue since clinician billable hours drive care income; turnover can cut revenue per clinic by an estimated 5–10% annually.

Investing in professional development and benefits is required: firms offering tuition assistance and sign-on bonuses saw retention improve by ~15% in 2024, reducing replacement costs that average $25,000–$40,000 per clinician.

Consumer discretionary spending trends

Economic downturns reduce disposable income—45% of U.S. households reported cutting medical spending during 2023–24; elective procedures and associated PT visits fell in recessions, lowering volume.

High copays/deductibles (median family deductible $2,000 in 2024) cause outpatient therapy drop-off; incomplete treatment raises readmission risk and revenue loss.

The company’s revenue correlates with GDP and consumer spending: a 1% GDP decline historically aligns with ~0.5%–1% drop in outpatient volumes.

- 45% households cut medical spend (2023–24)

- Median family deductible $2,000 (2024)

- 1% GDP decline → ~0.5–1% outpatient volume drop

Consolidation within the healthcare payer market

The 2023–2025 wave of insurer consolidation—Aetna-Cigna style deals and regional roll-ups—has concentrated market share: top 5 payers now cover roughly 65% of U.S. lives, boosting payer bargaining power in contract talks with therapy providers.

Consolidation pressures per-visit reimbursements; industry reports show outpatient therapy rates fell 3–7% real terms 2022–2024, risking margin compression for U.S. Physical Therapy.

Diversifying payer mix and proving superior clinical outcomes (e.g., 15–20% lower readmission or faster functional gains) are key levers to sustain negotiation leverage and defend rates.

- Top 5 payers ≈65% market share

- Outpatient therapy rates down 3–7% (2022–2024)

- Target outcome improvements 15–20% to gain leverage

Rising costs, tighter payers and wages squeeze outpatient margins amid economic risk

Rising input costs (healthcare CPI +4.2% in 2024; medical supplies +6% YoY) and higher financing (10y ~4.0%; Fed funds ~5% in 2024) compress margins while PT wages rose ~8% amid a 12% vacancy increase; top 5 payers cover ~65% of lives, driving reimbursements down 3–7% (2022–24) and linking volumes to GDP (1% GDP fall → ~0.5–1% outpatient drop).

| Metric | 2024/25 |

|---|---|

| Healthcare CPI | +4.2% |

| Medical supplies | +6% YoY |

| PT wages | +8% YoY |

| Vacancy | +12% |

| Top‑5 payers | ~65% |

| Reimbursements | -3–7% (real) |

Same Document Delivered

U.S. Physical Therapy PESTLE Analysis

The preview shown here is the exact U.S. Physical Therapy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE analysis of U.S. Physical Therapy—uncover how regulation, reimbursement trends, tech adoption, and demographic shifts will shape growth and risk; perfect for investors and strategists. Purchase the full report to access actionable insights, editable charts, and recommendations you can use immediately.

Political factors

Medicare reimbursement policy shifts

Federal adjustments to the Physician Fee Schedule drive outpatient PT revenue; CMS cut the conversion factor by 3.5% in 2024 and proposed modest increases in 2025, while legislative action in late 2025 aims to stabilize the factor to avoid projected clinic revenue declines of up to 6–8% nationwide; the company must track CMS rulemaking and quarterly Medicare reimbursement updates to revise budgets and partner contracts accordingly.

Federal healthcare reform initiatives

Ongoing debates over expanding the Affordable Care Act or restructuring Medicare/Medicaid directly affect coverage; 2024 estimates show ~8.6% of nonelderly remain uninsured, influencing demand for physical therapy.

Shifts in federal control alter mandates and subsidies—e.g., ACA subsidy changes in 2023–24 correlated with enrollment swings of several million, changing payer mix for clinics.

U.S. Physical Therapy must adapt to policy swings to protect patient inflows and contract revenue, with Medicare accounting for roughly 35% of outpatient rehab payments as of 2024.

State-level direct access legislation

Political advocacy at the state level increasingly enables patients to access physical therapy without physician referral; as of Dec 2025, 37 states plus DC allow unrestricted or limited direct access, up from 30 in 2020, lowering entry barriers and shortening care pathways.

This shift reduces reliance on physician referral networks, raising the strategic value of direct-to-consumer marketing—practices with strong consumer channels can capture a larger share of the $42B outpatient PT market projected for 2025.

Labor and minimum wage regulations

Legislative changes to federal and state minimum wages and overtime rules raised labor costs for U.S. physical therapy clinics in 2024–25; 21 states increased minimum wages in 2024, with the federal overtime salary threshold proposed to rise from $35,568 (2023) toward ~$48,000 in some rule drafts, pressuring payroll budgets.

Political pressure to boost support-staff pay compresses margins if Medicare Part B and commercial reimbursement rates (Medicare therapy fee schedule growth ~1–2% annually) do not keep pace, increasing cost-per-visit by an estimated 3–7% for affected clinics.

Clinics must tailor workforce strategies by region—using mix of part-time clinicians, telehealth, and centralized admin hubs—to manage heterogeneous state labor laws and contain operating expense growth projected at 4–6% in higher-wage states.

- 21 states raised minimum wage in 2024

- Potential overtime threshold moves toward ~$48,000

- Payroll-driven cost-per-visit up 3–7%

- Operating expense growth 4–6% in high-wage states

Governmental focus on opioid reduction

Public health policies to curb the opioid crisis have elevated physical therapy as a frontline non-opioid pain management option, with Medicare expanding coverage for therapy-first pathways and CDC guidance encouraging nonpharmacologic care; opioid prescribing dropped 48% from 2012–2022, boosting demand for rehab services.

Political backing yields grant funding and favorable clinical guidelines—FY2024 federal opioid-related grants exceeded $7.5 billion—supporting clinic expansion, care integration, and higher reimbursement rates for nonpharmacologic interventions.

Alignment with national priorities creates a strategic tailwind for long-term growth, increasing referral volumes and revenue diversification as payers shift toward value-based models that reward reductions in opioid use and improved functional outcomes.

- Medicare policy shifts favor therapy-first pain care

- Opioid prescriptions down 48% (2012–2022)

- FY2024 federal opioid grants > $7.5B

- Stronger referrals, reimbursement, and value-based incentives

Medicare cuts, direct‑access gains and wage hikes reshape $42B outpatient PT market

Federal CMS cuts and legislative stabilizers shift Medicare revenue (Medicare ~35% of outpatient rehab payments; CF cut 3.5% in 2024; modest 2025 increases) while direct-access in 37 states (Dec 2025) expands addressable market (2025 outpatient PT market ~$42B); labor law changes (21 states raised minimum wage in 2024; OT threshold proposals ~ $48k) push operating costs up 3–7% per visit.

| Metric | Value |

|---|---|

| Medicare share | ~35% |

| Physician Fee Schedule CF 2024 | -3.5% |

| Direct access states (Dec 2025) | 37 |

| Outpatient PT market 2025 | $42B |

| States raised min wage 2024 | 21 |

| Payroll cost-per-visit impact | +3–7% |

What is included in the product

Explores how macro-environmental factors uniquely affect U.S. Physical Therapy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify threats, opportunities, and strategy implications for market positioning, funding, and operational resilience.

A concise U.S. Physical Therapy PESTLE summary that highlights regulatory shifts, reimbursement trends, demographic demand, technological adoption, and competitive dynamics for quick reference in meetings or client reports.

Economic factors

Inflationary pressure on operating costs

Persistently high costs for medical supplies, facility leases, and utilities squeezed margins in 2024–25, with healthcare CPI rising about 4.2% in 2024 and medical supply costs up ~6% year-over-year; fixed third-party reimbursement (Medicare median PT reimbursement down 0.5% real in 2023–24) limits price pass-through. Scale-based procurement and aggressive cost containment—bulk purchasing, lease renegotiation—are essential to preserve operating margins.

Interest rate environment and capital allocation

Rising interest rates have pushed US average corporate borrowing costs higher—10‑year Treasury moved from 1.5% in 2020 to ~4.0% by end‑2023 and CPI‑adjusted Fed funds near 5% in 2024—raising financing costs for U.S. Physical Therapy’s acquisition-funded growth and increasing annual interest expense on leveraged deals.

Labor market competition for clinicians

A nationwide shortage of physical therapists—APTA reported a 12% vacancy rise in 2024—has pushed average PT salaries up about 8% year-over-year, increasing recruitment and labor costs for providers.

Hospitals and private practices aggressively compete for clinicians, threatening revenue since clinician billable hours drive care income; turnover can cut revenue per clinic by an estimated 5–10% annually.

Investing in professional development and benefits is required: firms offering tuition assistance and sign-on bonuses saw retention improve by ~15% in 2024, reducing replacement costs that average $25,000–$40,000 per clinician.

Consumer discretionary spending trends

Economic downturns reduce disposable income—45% of U.S. households reported cutting medical spending during 2023–24; elective procedures and associated PT visits fell in recessions, lowering volume.

High copays/deductibles (median family deductible $2,000 in 2024) cause outpatient therapy drop-off; incomplete treatment raises readmission risk and revenue loss.

The company’s revenue correlates with GDP and consumer spending: a 1% GDP decline historically aligns with ~0.5%–1% drop in outpatient volumes.

- 45% households cut medical spend (2023–24)

- Median family deductible $2,000 (2024)

- 1% GDP decline → ~0.5–1% outpatient volume drop

Consolidation within the healthcare payer market

The 2023–2025 wave of insurer consolidation—Aetna-Cigna style deals and regional roll-ups—has concentrated market share: top 5 payers now cover roughly 65% of U.S. lives, boosting payer bargaining power in contract talks with therapy providers.

Consolidation pressures per-visit reimbursements; industry reports show outpatient therapy rates fell 3–7% real terms 2022–2024, risking margin compression for U.S. Physical Therapy.

Diversifying payer mix and proving superior clinical outcomes (e.g., 15–20% lower readmission or faster functional gains) are key levers to sustain negotiation leverage and defend rates.

- Top 5 payers ≈65% market share

- Outpatient therapy rates down 3–7% (2022–2024)

- Target outcome improvements 15–20% to gain leverage

Rising costs, tighter payers and wages squeeze outpatient margins amid economic risk

Rising input costs (healthcare CPI +4.2% in 2024; medical supplies +6% YoY) and higher financing (10y ~4.0%; Fed funds ~5% in 2024) compress margins while PT wages rose ~8% amid a 12% vacancy increase; top 5 payers cover ~65% of lives, driving reimbursements down 3–7% (2022–24) and linking volumes to GDP (1% GDP fall → ~0.5–1% outpatient drop).

| Metric | 2024/25 |

|---|---|

| Healthcare CPI | +4.2% |

| Medical supplies | +6% YoY |

| PT wages | +8% YoY |

| Vacancy | +12% |

| Top‑5 payers | ~65% |

| Reimbursements | -3–7% (real) |

Same Document Delivered

U.S. Physical Therapy PESTLE Analysis

The preview shown here is the exact U.S. Physical Therapy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.