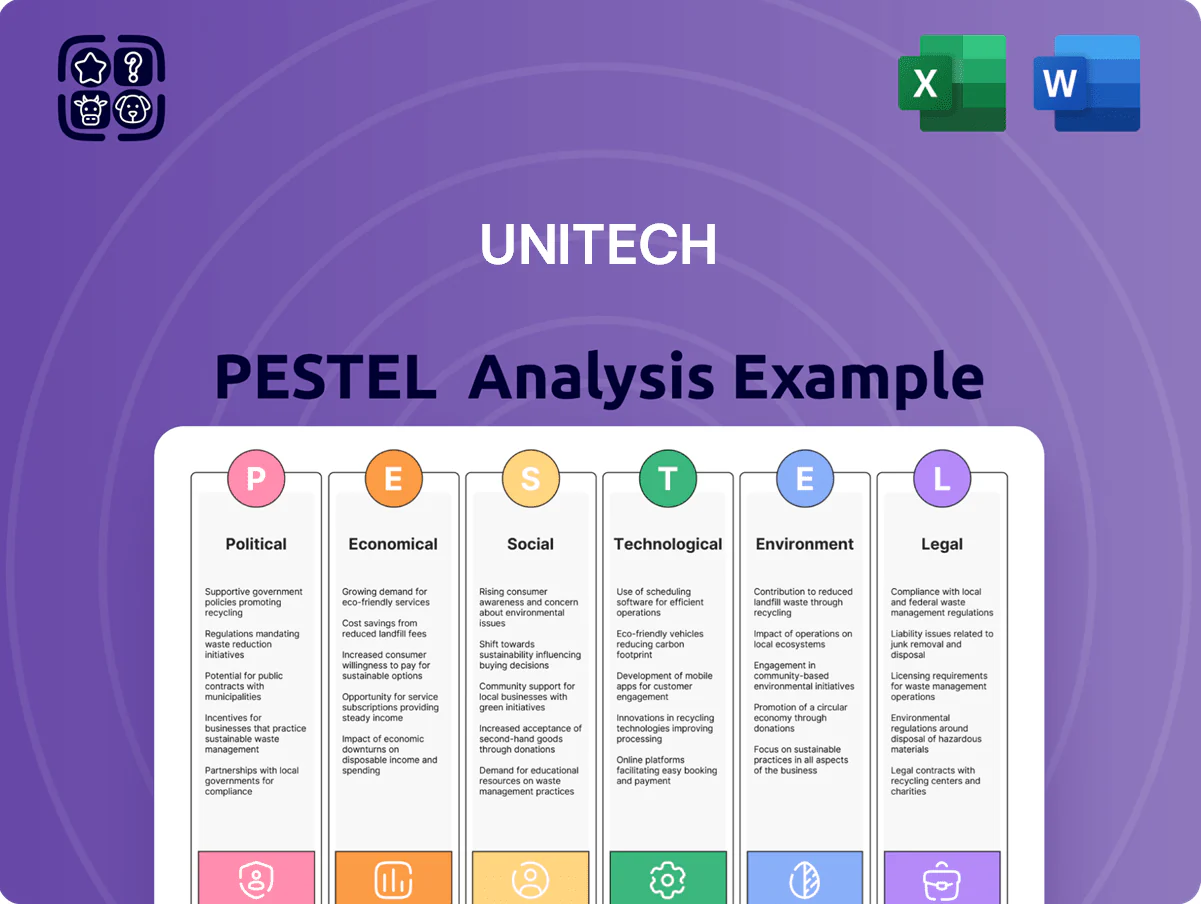

Unitech PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unitech’s future hangs on regulatory shifts, market cycles, and technological adoption—our PESTLE distills these external forces into clear risks and opportunities tailored to investors and strategists; purchase the full report to access the complete, ready-to-use analysis and actionable recommendations now.

Political factors

Geopolitical Trade Tensions

The 2025 US-China trade measures and EU export controls on advanced semiconductors have pushed Unitech to shift 18% of production from China to Southeast Asia and Mexico, raising estimated COGS by 3.2% year-to-date; potential 10–25% tariffs on electronics from designated regions threaten North American and European revenue streams worth $420M in 2024 sales.

Government Digitalization Subsidies

Government digitalization subsidies — e.g., EU Digitalisation Grants (€3–5k per SME), India’s Production Linked Incentive digital push (₹10k–50k per device) and US SBA tech programs—lower purchase barriers for AIDC hardware, directly boosting Unitech’s addressable SME market; strategists should map programs in EU, India, Southeast Asia and Latin America where 2024–25 uptake of mobile payments rose 12–18% annually to prioritize channels and bespoke financing bundles.

Taiwanese Cross-Strait Relations

As a Taiwan-based entity, Unitech is exposed to cross-strait political risk; investor confidence fell 12% on average for Taiwan-listed firms during the 2023 flare-up, highlighting sensitivity to tensions.

Escalation could disrupt Asia-Pacific logistics—Taiwan handles ~60% of global semiconductor packaging and 20% of container transshipment in 2024—raising supply-chain and cost risks for Unitech.

Investors should review Unitech’s contingency plans and hub diversification; firms with multi-hub footprints reduced revenue volatility by ~30% in 2022–24.

Global Tech Sovereignty Policies

Nation-states are prioritizing tech sovereignty, with 2024 OECD data showing 62% of G20 members adopting local-preference policies for critical infrastructure procurement, pressuring Unitech to source allied-nation components for rugged devices used in government healthcare and utilities.

This trend shifts product positioning—Unitech must certify devices to regional standards like EU NIS2 and US FedRAMP-equivalent baselines to compete for contracts that can exceed $100m annually in some markets.

Non-compliance risks exclusion from public tenders: a 2025 IDC estimate found 28% of public-sector device tenders explicitly require domestic or allied-sourced hardware.

- 62% of G20 with local-preference procurement (2024 OECD)

- Contracts >$100m possible for compliant suppliers

- Certifications needed: NIS2, FedRAMP-like standards

- 28% of tenders require domestic/allied hardware (IDC 2025)

Regional Trade Agreement Shifts

The expansion of RCEP (15 members, covering 30% of global GDP) and CPTPP (13 members post-2023 accessions) alters tariff lines for electronic components across Asia, potentially reducing tariffs by up to 10–15% for in-region inputs and lowering COGS for Unitech in member markets.

Conversely, rules-of-origin clauses may erect regulatory barriers for parts sourced outside these blocs, increasing compliance costs by an estimated 1–3% of revenue in affected markets.

Analysts should monitor tariff schedule changes and CPTPP/RCEP accession moves to assess Unitech’s pricing competitiveness versus local manufacturers in Southeast Asia and Latin America, where Unitech’s 2024 sales exposure exceeded 22% of regional revenue.

- RCEP/CPTPP coverage: ~30% global GDP

- Potential tariff reduction: 10–15%

- Compliance cost increase risk: 1–3% revenue

- Unitech 2024 regional exposure: >22%

Geopolitics reroutes supply chains: 18% relocation, $420M sales at risk, costs up

Political shifts—US-China trade measures, EU export controls and Taiwan cross-strait risk—have driven 18% production relocation (COGS +3.2%), threaten $420M of 2024 sales via potential tariffs, and raise logistics disruption risk given Taiwan’s 2024 semiconductor/transshipment shares; meanwhile 62% of G20 local-preference policies and 28% of tenders (IDC 2025) force certification (NIS2/FedRAMP-like) and allied sourcing, while RCEP/CPTPP could cut component tariffs 10–15% but add 1–3% compliance costs.

| Metric | Value |

|---|---|

| Production relocated | 18% |

| COGS impact YTD | +3.2% |

| At-risk 2024 sales | $420M |

| G20 local-preference | 62% |

| Tenders requiring allied/domestic | 28% |

| Tariff reduction (RCEP/CPTPP) | 10–15% |

| Compliance cost risk | 1–3% revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Unitech across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends, forward-looking insights, and actionable sub-points tailored to the company’s industry and region to support strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary for Unitech that distills regulatory, economic, social, technological, environmental and legal factors into a shareable slide or handout to speed decision-making and alignment across teams.

Economic factors

Labor Shortages and Automation Demand

Persistent global labor shortages—UN ILO reports 2024 vacancy rates up 18% in logistics and retail—are accelerating automation; IDC forecasts 2025 warehouse automation spend to reach $50.5B, driving firms to adopt efficiency tools. Unitech’s AIDC rugged handhelds and scanners align as essential capital investments to maintain output with fewer staff, supporting a stable demand floor for automated scanning and inventory systems.

Inflationary Pressures on Manufacturing

By end-2025, raw material and specialized semiconductor cost volatility trimmed Unitech margins; global semiconductor spot prices rose ~18% in 2024 before easing 6% in 2025, while input inflation kept manufacturing overheads up ~9% YoY, forcing Unitech to adopt dynamic pricing and cost-pass strategies. Financial teams must assess price elasticity and channel mix to avoid share loss to low-cost rivals while preserving a target gross margin of ~22%.

Currency Exchange Rate Volatility

As an export-oriented firm, Unitech faces high exposure to TWD volatility versus USD and EUR; TWD moved about 2.8% vs USD and 5.6% vs EUR in 2024, which can erode price competitiveness and swing reported overseas earnings by several percentage points. In 2025 Q1, FX losses forced peers to report EBITDA margin hits of 100–250 bps, highlighting why Unitech’s hedging ratio (forward covers/options) and 2024 revenue split—~62% Asia, 25% Americas, 13% Europe—are critical stability metrics.

Capital Expenditure Trends

Corporate capex on rugged hardware is highly sensitive to global interest rates; a 100 bps rise in borrowing costs can increase financing expenses for large deployments by roughly 10-15%, slowing purchase cycles.

With central banks keeping rates elevated in 2024–2025 (Fed funds ~5.25–5.50% in early 2025), logistics fleet refreshes face timing shifts—surveys show 32% of firms postponed hardware buys in 2024.

Strategists should model macro cycles into sales forecasts, as durable-device revenue can swing ±20% across rate tightening vs easing phases.

- Higher rates raise financing costs ~10–15% per 100 bps

- 32% of logistics firms postponed hardware in 2024

- Rugged-device revenue volatility ~±20% across cycles

Growth of Emerging Market E-commerce

The rapid expansion of e-commerce in Southeast Asia and Latin America—combined GMV growth of roughly 20% CAGR (2021–2025) and e‑commerce penetration rising to ~12% in SEA and ~8% in LATAM by 2025—creates strong demand for affordable, durable mobile scanners for last‑mile delivery and warehousing; Unitech capturing even 2–4% share in these regions could add materially to revenue diversification.

- SEA+LATAM e‑commerce CAGR ~20% (2021–2025)

- Penetration ~12% SEA, ~8% LATAM by 2025

- Targetable share 2–4% = material revenue upside

Higher rates squeeze margins; global e‑commerce growth offers 2–4% diversification upside

Economic forces: elevated rates (Fed 5.25–5.50% early-2025) and 100 bps up → financing +10–15% slow capex; 32% logistics firms delayed buys in 2024; raw input inflation +9% YoY and semiconductor spot +18% in 2024 trimmed margins; TWD moved ~2.8% vs USD/5.6% vs EUR in 2024; SEA+LATAM e‑commerce GMV CAGR ~20% (2021–2025) — 2–4% market share could diversify revenue.

| Metric | Value |

|---|---|

| Fed funds (early‑2025) | 5.25–5.50% |

| Logistics delayed buys (2024) | 32% |

| Input inflation (YoY) | ~9% |

| Semiconductor spot (2024) | +18% |

| TWD vs USD/EUR (2024) | +2.8% / +5.6% |

| SEA+LATAM e‑commerce CAGR | ~20% (2021–2025) |

Preview the Actual Deliverable

Unitech PESTLE Analysis

The preview shown here is the exact Unitech PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unitech’s future hangs on regulatory shifts, market cycles, and technological adoption—our PESTLE distills these external forces into clear risks and opportunities tailored to investors and strategists; purchase the full report to access the complete, ready-to-use analysis and actionable recommendations now.

Political factors

Geopolitical Trade Tensions

The 2025 US-China trade measures and EU export controls on advanced semiconductors have pushed Unitech to shift 18% of production from China to Southeast Asia and Mexico, raising estimated COGS by 3.2% year-to-date; potential 10–25% tariffs on electronics from designated regions threaten North American and European revenue streams worth $420M in 2024 sales.

Government Digitalization Subsidies

Government digitalization subsidies — e.g., EU Digitalisation Grants (€3–5k per SME), India’s Production Linked Incentive digital push (₹10k–50k per device) and US SBA tech programs—lower purchase barriers for AIDC hardware, directly boosting Unitech’s addressable SME market; strategists should map programs in EU, India, Southeast Asia and Latin America where 2024–25 uptake of mobile payments rose 12–18% annually to prioritize channels and bespoke financing bundles.

Taiwanese Cross-Strait Relations

As a Taiwan-based entity, Unitech is exposed to cross-strait political risk; investor confidence fell 12% on average for Taiwan-listed firms during the 2023 flare-up, highlighting sensitivity to tensions.

Escalation could disrupt Asia-Pacific logistics—Taiwan handles ~60% of global semiconductor packaging and 20% of container transshipment in 2024—raising supply-chain and cost risks for Unitech.

Investors should review Unitech’s contingency plans and hub diversification; firms with multi-hub footprints reduced revenue volatility by ~30% in 2022–24.

Global Tech Sovereignty Policies

Nation-states are prioritizing tech sovereignty, with 2024 OECD data showing 62% of G20 members adopting local-preference policies for critical infrastructure procurement, pressuring Unitech to source allied-nation components for rugged devices used in government healthcare and utilities.

This trend shifts product positioning—Unitech must certify devices to regional standards like EU NIS2 and US FedRAMP-equivalent baselines to compete for contracts that can exceed $100m annually in some markets.

Non-compliance risks exclusion from public tenders: a 2025 IDC estimate found 28% of public-sector device tenders explicitly require domestic or allied-sourced hardware.

- 62% of G20 with local-preference procurement (2024 OECD)

- Contracts >$100m possible for compliant suppliers

- Certifications needed: NIS2, FedRAMP-like standards

- 28% of tenders require domestic/allied hardware (IDC 2025)

Regional Trade Agreement Shifts

The expansion of RCEP (15 members, covering 30% of global GDP) and CPTPP (13 members post-2023 accessions) alters tariff lines for electronic components across Asia, potentially reducing tariffs by up to 10–15% for in-region inputs and lowering COGS for Unitech in member markets.

Conversely, rules-of-origin clauses may erect regulatory barriers for parts sourced outside these blocs, increasing compliance costs by an estimated 1–3% of revenue in affected markets.

Analysts should monitor tariff schedule changes and CPTPP/RCEP accession moves to assess Unitech’s pricing competitiveness versus local manufacturers in Southeast Asia and Latin America, where Unitech’s 2024 sales exposure exceeded 22% of regional revenue.

- RCEP/CPTPP coverage: ~30% global GDP

- Potential tariff reduction: 10–15%

- Compliance cost increase risk: 1–3% revenue

- Unitech 2024 regional exposure: >22%

Geopolitics reroutes supply chains: 18% relocation, $420M sales at risk, costs up

Political shifts—US-China trade measures, EU export controls and Taiwan cross-strait risk—have driven 18% production relocation (COGS +3.2%), threaten $420M of 2024 sales via potential tariffs, and raise logistics disruption risk given Taiwan’s 2024 semiconductor/transshipment shares; meanwhile 62% of G20 local-preference policies and 28% of tenders (IDC 2025) force certification (NIS2/FedRAMP-like) and allied sourcing, while RCEP/CPTPP could cut component tariffs 10–15% but add 1–3% compliance costs.

| Metric | Value |

|---|---|

| Production relocated | 18% |

| COGS impact YTD | +3.2% |

| At-risk 2024 sales | $420M |

| G20 local-preference | 62% |

| Tenders requiring allied/domestic | 28% |

| Tariff reduction (RCEP/CPTPP) | 10–15% |

| Compliance cost risk | 1–3% revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Unitech across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends, forward-looking insights, and actionable sub-points tailored to the company’s industry and region to support strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary for Unitech that distills regulatory, economic, social, technological, environmental and legal factors into a shareable slide or handout to speed decision-making and alignment across teams.

Economic factors

Labor Shortages and Automation Demand

Persistent global labor shortages—UN ILO reports 2024 vacancy rates up 18% in logistics and retail—are accelerating automation; IDC forecasts 2025 warehouse automation spend to reach $50.5B, driving firms to adopt efficiency tools. Unitech’s AIDC rugged handhelds and scanners align as essential capital investments to maintain output with fewer staff, supporting a stable demand floor for automated scanning and inventory systems.

Inflationary Pressures on Manufacturing

By end-2025, raw material and specialized semiconductor cost volatility trimmed Unitech margins; global semiconductor spot prices rose ~18% in 2024 before easing 6% in 2025, while input inflation kept manufacturing overheads up ~9% YoY, forcing Unitech to adopt dynamic pricing and cost-pass strategies. Financial teams must assess price elasticity and channel mix to avoid share loss to low-cost rivals while preserving a target gross margin of ~22%.

Currency Exchange Rate Volatility

As an export-oriented firm, Unitech faces high exposure to TWD volatility versus USD and EUR; TWD moved about 2.8% vs USD and 5.6% vs EUR in 2024, which can erode price competitiveness and swing reported overseas earnings by several percentage points. In 2025 Q1, FX losses forced peers to report EBITDA margin hits of 100–250 bps, highlighting why Unitech’s hedging ratio (forward covers/options) and 2024 revenue split—~62% Asia, 25% Americas, 13% Europe—are critical stability metrics.

Capital Expenditure Trends

Corporate capex on rugged hardware is highly sensitive to global interest rates; a 100 bps rise in borrowing costs can increase financing expenses for large deployments by roughly 10-15%, slowing purchase cycles.

With central banks keeping rates elevated in 2024–2025 (Fed funds ~5.25–5.50% in early 2025), logistics fleet refreshes face timing shifts—surveys show 32% of firms postponed hardware buys in 2024.

Strategists should model macro cycles into sales forecasts, as durable-device revenue can swing ±20% across rate tightening vs easing phases.

- Higher rates raise financing costs ~10–15% per 100 bps

- 32% of logistics firms postponed hardware in 2024

- Rugged-device revenue volatility ~±20% across cycles

Growth of Emerging Market E-commerce

The rapid expansion of e-commerce in Southeast Asia and Latin America—combined GMV growth of roughly 20% CAGR (2021–2025) and e‑commerce penetration rising to ~12% in SEA and ~8% in LATAM by 2025—creates strong demand for affordable, durable mobile scanners for last‑mile delivery and warehousing; Unitech capturing even 2–4% share in these regions could add materially to revenue diversification.

- SEA+LATAM e‑commerce CAGR ~20% (2021–2025)

- Penetration ~12% SEA, ~8% LATAM by 2025

- Targetable share 2–4% = material revenue upside

Higher rates squeeze margins; global e‑commerce growth offers 2–4% diversification upside

Economic forces: elevated rates (Fed 5.25–5.50% early-2025) and 100 bps up → financing +10–15% slow capex; 32% logistics firms delayed buys in 2024; raw input inflation +9% YoY and semiconductor spot +18% in 2024 trimmed margins; TWD moved ~2.8% vs USD/5.6% vs EUR in 2024; SEA+LATAM e‑commerce GMV CAGR ~20% (2021–2025) — 2–4% market share could diversify revenue.

| Metric | Value |

|---|---|

| Fed funds (early‑2025) | 5.25–5.50% |

| Logistics delayed buys (2024) | 32% |

| Input inflation (YoY) | ~9% |

| Semiconductor spot (2024) | +18% |

| TWD vs USD/EUR (2024) | +2.8% / +5.6% |

| SEA+LATAM e‑commerce CAGR | ~20% (2021–2025) |

Preview the Actual Deliverable

Unitech PESTLE Analysis

The preview shown here is the exact Unitech PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.