Vaisala Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

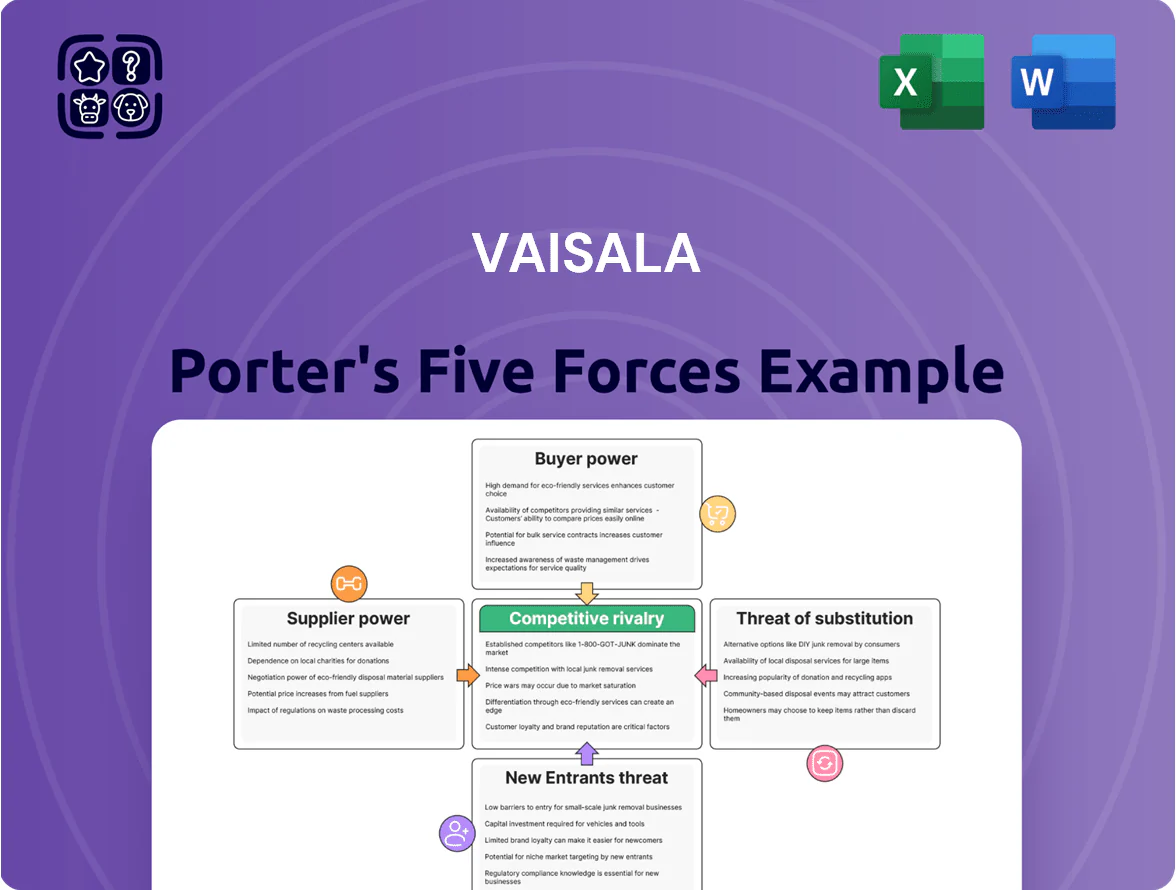

Vaisala faces moderate supplier power, niche customer segments with varied bargaining strength, and evolving substitute risks from low-cost sensor makers and IoT platforms—while high regulatory standards and strong brand reputation shape its competitive moat and entry barriers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vaisala’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Vaisala depends on highly specialized electronic components and high-precision sensors made by a few advanced manufacturers, giving suppliers strong leverage over price and lead times.

These parts are critical to Vaisala’s industry-leading accuracy; any supplier disruption risks product performance and customer trust, impacting revenue—Vaisala reported €544.5M in 2024 net sales, much tied to sensor reliability.

By end-2025, component complexity and qualification lead times exceed 12–18 months, making alternative sourcing costly or requiring major redesigns, so Vaisala must keep long-term strategic supplier agreements to secure supply and quality.

Semiconductor Market Volatility

Vaisala remains sensitive to the global semiconductor chain, crucial for its digital sensors and software; although chip shortages eased by 2025, 75% of advanced logic capacity is still concentrated in Taiwan and Korea, keeping supplier leverage on price and lead times.

Vaisala mitigates risk by securing multi-year volume commitments and qualifying alternative chip architectures; a single-tier disruption could delay instrument deliveries by 8–12 weeks and hit FY2025 revenue by an estimated 3–5%.

Niche Raw Material Scarcity

The production of Vaisala high-performance sensors relies on rare earths like neodymium and specialty ceramics; global rare-earth prices rose ~18% in 2024 amid China export controls, raising input risk.

Suppliers can push prices or favor big industrial buyers, so Vaisala cuts usage, improves yields, and signs multi-year contracts—its 2024 procurement commitments covered ~60% of projected needs.

Substitution is hard: alternative materials often fail performance specs, so short-term switching is technically unfeasible, keeping supplier power structurally high.

Technical Integration Complexity

Many Vaisala sub-assemblies are custom-engineered for extreme environments or pharma cleanrooms, creating mutual dependency and high switching costs—validation can take 6–18 months and cost millions; this raises supplier leverage.

Suppliers know components are deeply integrated into Vaisala proprietary designs, limiting aggressive price negotiation; supplier-driven price premia of 5–12% are common in high-end measurement markets.

- Custom parts → 6–18 month validation

- Switching cost: $0.5–3M per product line

- Supplier price premium: 5–12%

- Technical lock-in → high supplier power

Supplier Forward Integration Risk

While most suppliers lack Vaisala’s system integration and domain expertise, major tech firms (eg, Google, Bosch) are building end-to-end sensing offers; if a key supplier forward-integrates it could both compete and control parts supply.

Risk is limited today by Vaisala’s track record in harsh environments and 2024 recurring services revenue ~45% of net sales, but IoT convergence raises vigilance needs; Vaisala offsets risk via high-value software and data services hard to copy.

- Suppliers lack deep domain skills; few can fully replicate Vaisala

- Large tech firms are moving into full sensing solutions

- 2024 services ~45% of Vaisala net sales strengthens stickiness

- Focus on software/data services preserves moat vs forward integration

Vaisala faces supplier squeeze: long lead times, price premia; services cushion but 3–5% risk

Suppliers hold high leverage: specialized sensors, rare earths, and semiconductors concentrate supply, causing 12–18 month lead times and 5–12% price premia; Vaisala’s 2024 net sales €544.5M and 45% recurring services partially buffer risk, but single-tier disruption could cut FY2025 revenue 3–5%.

| Metric | Value |

|---|---|

| 2024 net sales | €544.5M |

| Services share | 45% |

| Lead times | 12–18 months |

| Disruption risk | Revenue −3–5% |

What is included in the product

Tailored Porter’s Five Forces analysis for Vaisala uncovering competitive pressures, supplier and buyer influence, entry barriers, substitutes, and strategic implications to safeguard market share and profitability.

A concise Porter's Five Forces one-sheet for Vaisala—clarifying competitive pressures and strategic levers at a glance to speed boardroom decisions and investor reviews.

Customers Bargaining Power

High Switching Costs for Infrastructure

Large customers like national weather services, airports, and energy firms integrate Vaisala systems into core operations, making replacement costly and complex; industry estimates show enterprise system swap costs often exceed 20–30% of annual IT/OT budgets, lowering customer bargaining power. Once installed, clients rely on Vaisala for maintenance, software updates, and calibrated sensor replacements—services that produced about 38% of Vaisala’s 2024 net sales—creating recurring revenue and reducing price-driven churn.

Demand for High Precision and Reliability

In life sciences and aviation, a single inaccurate reading can cost millions and endanger lives, so buyers pay for precision rather than the lowest price; this gives Vaisala measurable pricing power versus commodity sensor makers.

Customers prioritize reliability and regulatory compliance, so procurement teams seldom push discounts that would risk safety, supporting Vaisala’s ability to sustain higher ASPs (average selling prices).

Vaisala’s premium reputation helped deliver 2024 gross margin near 44% and operating margin around 19%, letting it maintain healthy margins even when selling to budget-conscious organizations.

Institutional Buyer Leverage

Government agencies and large multinationals account for roughly 35–45% of Vaisala’s order book and use competitive tenders to push prices and specs. These buyers run deep market comparisons and often require tailored instruments or multi-year service agreements, raising switching costs. By end-2025 many shift to data-as-a-service (DaaS), favoring vendors with rich analytics; Vaisala counters with modular systems and flexible service contracts, aiming to keep renewal rates above its 80% target.

Information Symmetry and Technical Expertise

Vaisala’s customers—meteorologists, researchers, industrial engineers—hold deep technical expertise, letting them compare specs and performance across suppliers and squeezing Vaisala’s ability to command price premiums without clear technical leads.

Public benchmarks and digital transparency (e.g., instrument accuracy, uptime) force continual R&D; Vaisala spent EUR 59.8m on R&D in 2024, so innovation pace directly affects perceived value.

High buyer awareness keeps pressure on product updates, service SLAs, and clear ROI demonstrations to retain contracts.

- Customers: highly technical (meteorologists, researchers, engineers)

- R&D: EUR 59.8m in 2024

- Risk: easy spec comparison lowers price flexibility

- Action: must show measurable performance gains and SLAs

Consolidation in Key Industrial Segments

Consolidation in renewables and pharma has created larger buyer groups that secured ~15–25% deeper volume discounts in 2024, increasing their negotiating clout versus Vaisala.

These buyers demand better payment terms and service levels than small labs; Vaisala sees tougher contract renewals and lower hardware margins as concentration rises.

Vaisala counters by selling integrated software and analytics (enterprise-wide deployments) that shift value to recurring fees and reduce pure price competition.

- 2024: top 10 customers in energy/pharma grew share ~12%

- Volume discounts commonly 15–25%

- Recurring software upsells reduce churn, raise gross margin by ~5 p.p.

Services, R&D and DaaS drive pricing power despite concentrated, discounting buyers

Large, technical buyers (govt, airports, energy) face high swap costs and value reliability, limiting price pressure; services made ~38% of Vaisala 2024 net sales and R&D was EUR 59.8m, supporting pricing power. Top customers concentrated (35–45% order book; top-10 energy/pharma +12% share in 2024) push discounts (15–25%) but DaaS/software upsells boost renewal rates toward an 80% target and raise gross margin ~5 p.p.

| Metric | 2024/2025 |

|---|---|

| Services share | ~38% net sales (2024) |

| R&D | EUR 59.8m (2024) |

| Order book concentration | 35–45% |

| Top-10 share growth | +12% (2024) |

| Volume discounts | 15–25% |

| Renewal target | ~80% |

| Gross margin lift from software | ~+5 p.p. |

Same Document Delivered

Vaisala Porter's Five Forces Analysis

This preview shows the exact Vaisala Porter's Five Forces analysis you'll receive—no placeholders or mockups, fully formatted and ready to use.

The document displayed is part of the final deliverable and will be available for immediate download the moment you complete your purchase.

You're viewing the actual file; once purchased, you’ll get instant access to this same professionally written analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Vaisala faces moderate supplier power, niche customer segments with varied bargaining strength, and evolving substitute risks from low-cost sensor makers and IoT platforms—while high regulatory standards and strong brand reputation shape its competitive moat and entry barriers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vaisala’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Vaisala depends on highly specialized electronic components and high-precision sensors made by a few advanced manufacturers, giving suppliers strong leverage over price and lead times.

These parts are critical to Vaisala’s industry-leading accuracy; any supplier disruption risks product performance and customer trust, impacting revenue—Vaisala reported €544.5M in 2024 net sales, much tied to sensor reliability.

By end-2025, component complexity and qualification lead times exceed 12–18 months, making alternative sourcing costly or requiring major redesigns, so Vaisala must keep long-term strategic supplier agreements to secure supply and quality.

Semiconductor Market Volatility

Vaisala remains sensitive to the global semiconductor chain, crucial for its digital sensors and software; although chip shortages eased by 2025, 75% of advanced logic capacity is still concentrated in Taiwan and Korea, keeping supplier leverage on price and lead times.

Vaisala mitigates risk by securing multi-year volume commitments and qualifying alternative chip architectures; a single-tier disruption could delay instrument deliveries by 8–12 weeks and hit FY2025 revenue by an estimated 3–5%.

Niche Raw Material Scarcity

The production of Vaisala high-performance sensors relies on rare earths like neodymium and specialty ceramics; global rare-earth prices rose ~18% in 2024 amid China export controls, raising input risk.

Suppliers can push prices or favor big industrial buyers, so Vaisala cuts usage, improves yields, and signs multi-year contracts—its 2024 procurement commitments covered ~60% of projected needs.

Substitution is hard: alternative materials often fail performance specs, so short-term switching is technically unfeasible, keeping supplier power structurally high.

Technical Integration Complexity

Many Vaisala sub-assemblies are custom-engineered for extreme environments or pharma cleanrooms, creating mutual dependency and high switching costs—validation can take 6–18 months and cost millions; this raises supplier leverage.

Suppliers know components are deeply integrated into Vaisala proprietary designs, limiting aggressive price negotiation; supplier-driven price premia of 5–12% are common in high-end measurement markets.

- Custom parts → 6–18 month validation

- Switching cost: $0.5–3M per product line

- Supplier price premium: 5–12%

- Technical lock-in → high supplier power

Supplier Forward Integration Risk

While most suppliers lack Vaisala’s system integration and domain expertise, major tech firms (eg, Google, Bosch) are building end-to-end sensing offers; if a key supplier forward-integrates it could both compete and control parts supply.

Risk is limited today by Vaisala’s track record in harsh environments and 2024 recurring services revenue ~45% of net sales, but IoT convergence raises vigilance needs; Vaisala offsets risk via high-value software and data services hard to copy.

- Suppliers lack deep domain skills; few can fully replicate Vaisala

- Large tech firms are moving into full sensing solutions

- 2024 services ~45% of Vaisala net sales strengthens stickiness

- Focus on software/data services preserves moat vs forward integration

Vaisala faces supplier squeeze: long lead times, price premia; services cushion but 3–5% risk

Suppliers hold high leverage: specialized sensors, rare earths, and semiconductors concentrate supply, causing 12–18 month lead times and 5–12% price premia; Vaisala’s 2024 net sales €544.5M and 45% recurring services partially buffer risk, but single-tier disruption could cut FY2025 revenue 3–5%.

| Metric | Value |

|---|---|

| 2024 net sales | €544.5M |

| Services share | 45% |

| Lead times | 12–18 months |

| Disruption risk | Revenue −3–5% |

What is included in the product

Tailored Porter’s Five Forces analysis for Vaisala uncovering competitive pressures, supplier and buyer influence, entry barriers, substitutes, and strategic implications to safeguard market share and profitability.

A concise Porter's Five Forces one-sheet for Vaisala—clarifying competitive pressures and strategic levers at a glance to speed boardroom decisions and investor reviews.

Customers Bargaining Power

High Switching Costs for Infrastructure

Large customers like national weather services, airports, and energy firms integrate Vaisala systems into core operations, making replacement costly and complex; industry estimates show enterprise system swap costs often exceed 20–30% of annual IT/OT budgets, lowering customer bargaining power. Once installed, clients rely on Vaisala for maintenance, software updates, and calibrated sensor replacements—services that produced about 38% of Vaisala’s 2024 net sales—creating recurring revenue and reducing price-driven churn.

Demand for High Precision and Reliability

In life sciences and aviation, a single inaccurate reading can cost millions and endanger lives, so buyers pay for precision rather than the lowest price; this gives Vaisala measurable pricing power versus commodity sensor makers.

Customers prioritize reliability and regulatory compliance, so procurement teams seldom push discounts that would risk safety, supporting Vaisala’s ability to sustain higher ASPs (average selling prices).

Vaisala’s premium reputation helped deliver 2024 gross margin near 44% and operating margin around 19%, letting it maintain healthy margins even when selling to budget-conscious organizations.

Institutional Buyer Leverage

Government agencies and large multinationals account for roughly 35–45% of Vaisala’s order book and use competitive tenders to push prices and specs. These buyers run deep market comparisons and often require tailored instruments or multi-year service agreements, raising switching costs. By end-2025 many shift to data-as-a-service (DaaS), favoring vendors with rich analytics; Vaisala counters with modular systems and flexible service contracts, aiming to keep renewal rates above its 80% target.

Information Symmetry and Technical Expertise

Vaisala’s customers—meteorologists, researchers, industrial engineers—hold deep technical expertise, letting them compare specs and performance across suppliers and squeezing Vaisala’s ability to command price premiums without clear technical leads.

Public benchmarks and digital transparency (e.g., instrument accuracy, uptime) force continual R&D; Vaisala spent EUR 59.8m on R&D in 2024, so innovation pace directly affects perceived value.

High buyer awareness keeps pressure on product updates, service SLAs, and clear ROI demonstrations to retain contracts.

- Customers: highly technical (meteorologists, researchers, engineers)

- R&D: EUR 59.8m in 2024

- Risk: easy spec comparison lowers price flexibility

- Action: must show measurable performance gains and SLAs

Consolidation in Key Industrial Segments

Consolidation in renewables and pharma has created larger buyer groups that secured ~15–25% deeper volume discounts in 2024, increasing their negotiating clout versus Vaisala.

These buyers demand better payment terms and service levels than small labs; Vaisala sees tougher contract renewals and lower hardware margins as concentration rises.

Vaisala counters by selling integrated software and analytics (enterprise-wide deployments) that shift value to recurring fees and reduce pure price competition.

- 2024: top 10 customers in energy/pharma grew share ~12%

- Volume discounts commonly 15–25%

- Recurring software upsells reduce churn, raise gross margin by ~5 p.p.

Services, R&D and DaaS drive pricing power despite concentrated, discounting buyers

Large, technical buyers (govt, airports, energy) face high swap costs and value reliability, limiting price pressure; services made ~38% of Vaisala 2024 net sales and R&D was EUR 59.8m, supporting pricing power. Top customers concentrated (35–45% order book; top-10 energy/pharma +12% share in 2024) push discounts (15–25%) but DaaS/software upsells boost renewal rates toward an 80% target and raise gross margin ~5 p.p.

| Metric | 2024/2025 |

|---|---|

| Services share | ~38% net sales (2024) |

| R&D | EUR 59.8m (2024) |

| Order book concentration | 35–45% |

| Top-10 share growth | +12% (2024) |

| Volume discounts | 15–25% |

| Renewal target | ~80% |

| Gross margin lift from software | ~+5 p.p. |

Same Document Delivered

Vaisala Porter's Five Forces Analysis

This preview shows the exact Vaisala Porter's Five Forces analysis you'll receive—no placeholders or mockups, fully formatted and ready to use.

The document displayed is part of the final deliverable and will be available for immediate download the moment you complete your purchase.

You're viewing the actual file; once purchased, you’ll get instant access to this same professionally written analysis.