VakifBank PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and digital banking trends are reshaping VakifBank’s strategic landscape in our concise PESTLE snapshot—perfect for investors and advisors who need fast, actionable context. Purchase the full PESTLE analysis to access detailed regulatory, technological, and social risk assessments plus strategic recommendations you can deploy immediately.

Political factors

State Ownership Influence

Geopolitical Regional Stability

Turkey's transcontinental location exposes VakıfBank to both trade opportunities and geopolitical risks across Europe, Asia and the Middle East, with regional trade accounting for roughly 45% of Turkey's exports in 2024, directly affecting the bank's trade finance pipeline.

Instability in neighboring countries can compress VakıfBank's international trade finance volumes and elevate NPLs in foreign operations, where FX-linked exposures reached about $18bn on the bank's consolidated balance sheet in 2024.

By end-2025 VakıfBank must manage shifting diplomatic alliances and sanctions regimes that can alter cross-border capital flows and the security of its international assets, noting Turkey's foreign direct investment inflows fell 12% in 2024 versus 2023.

Strategic Government Incentives

International Diplomatic Relations

International diplomatic ties shape VakıfBank’s funding costs; improved relations with the EU and US can lower international borrowing spreads—Turkey’s sovereign CDS moved from ~740 bps in 2020 to ~250–300 bps in 2024–2025 during stabilization phases, easing access to cheaper funds.

Compliance with FATF and EU standards affects market access; Turkey’s FATF follow-up status and regulatory alignment in 2024–25 reduced compliance friction, supporting bond issuances and syndicated loans.

Positive diplomatic shifts have translated into better credit terms and JV opportunities with foreign banks, increasing syndicated loan volumes and cross-border partnership activity in 2024–25.

- Lower sovereign CDS (≈250–300 bps in 2024–25) improved borrowing spreads

- FATF alignment eased compliance barriers for global capital access

- Diplomatic gains increased syndicated loan and partnership activity

Domestic Policy Continuity

The predictability of Turkey’s political environment and macroeconomic management are critical for VakifBank’s long-term planning; GDP grew 3.5% in 2024 and inflation slowed to 58% year-end 2024, affecting lending and provisioning assumptions.

Consistent leadership at the Treasury and Finance Ministry through 2024–2025 supports stable regulatory expectations, enabling VakifBank to pursue growth targets tied to a 10–12% credit expansion forecast for 2025.

Significant political shifts could prompt leadership changes or a refocus of VakifBank’s mandate, risking adjustments to capital allocation, state-directed lending, or governance structures.

- 2024 GDP +3.5% and inflation ~58% (year-end 2024) influence credit risk pricing

- Treasury continuity supports 10–12% credit growth target for 2025

- Political shifts could alter board/management and state-directed lending priorities

VakıfBank: State Anchor, High TL Growth, FX Risks amid Elevated Inflation and CDS

| Metric | Value (2024) |

|---|---|

| State share | ~58% |

| State-subsidized loans | TRY 78bn |

| State-guaranteed share | ~22% |

| TL loan growth (2023) | ~24% y/y |

| ROAE (2023) | 9–11% |

| FX-linked exposures | $18bn |

| Sovereign CDS | ~250–300bps |

| GDP growth | +3.5% |

| Inflation (YE) | ~58% |

What is included in the product

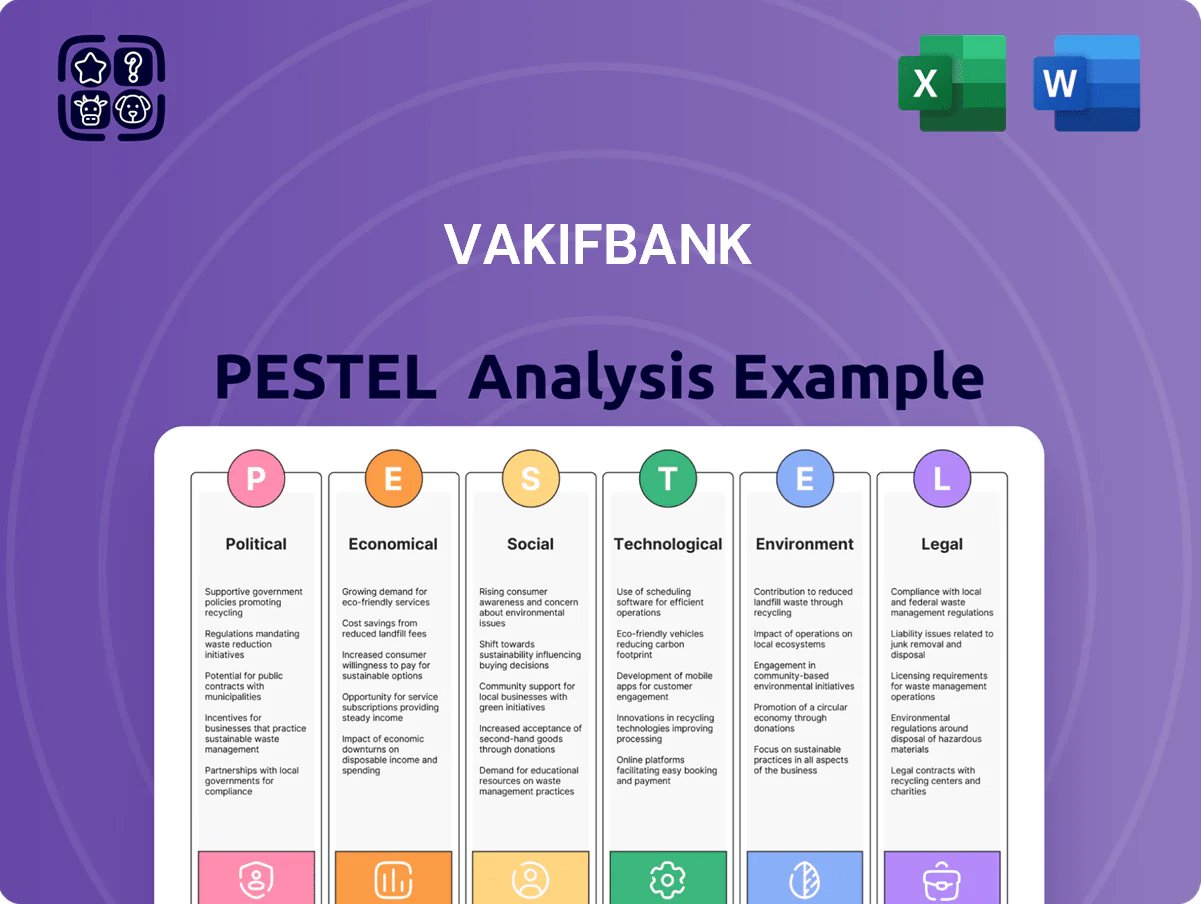

Explores how macro-environmental factors affect VakifBank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to Turkey’s banking sector to identify risks, opportunities, and strategic responses.

A concise VakifBank PESTLE summary that’s visually segmented by category for rapid interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary Environment Management

Monetary Policy Shifts

Central Bank of the Republic of Türkiye policy rate changes—from 8.5% in Jan 2023 to 45% peak in 2023 and easing to 35% by end-2024—directly compress or expand VakıfBank’s net interest margin and profitability.

Higher rates raised funding costs and slowed retail/corporate loan growth, with Turkish credit Y/Y growth falling from 43% (2022) to ~15% in 2024, reducing new loan demand.

VakıfBank must rapidly reprice deposits and lending—short-term repricing actions in 2024 helped protect CET1 ratios around 12–13% amid volatile national monetary shifts.

Currency Exchange Volatility

The Turkish lira’s 2024–2025 volatility—USD/TRY moved from ~27.0 in Jan 2024 to ~31.5 by Dec 2024, and EUR/TRY from ~29.0 to ~33.0—directly pressures VakıfBank’s CET1 and capital adequacy via FX-weighted exposures and FX‑denominated loans totaling several billion TRY. VakıfBank applies stringent FX risk limits, hedging and stress tests to shield the balance sheet; stable FX markets are critical to valuing international assets and servicing foreign debt.

GDP Growth Trends

Turkey's GDP expanded 3.5% in 2024 with IMF projecting ~3.2% for 2025, affecting VakifBank's loan demand across retail, SME and corporate segments; stronger growth reduces credit costs and supports fee income from trade finance.

Historical cycles show lower NPL ratios during expansions—Turkey's banking sector NPL ratio fell to 3.1% in Q3 2024—benefiting VakifBank's asset quality and investment banking activity tied to industry and services resilience through 2025.

- 2024 GDP growth: 3.5%

- IMF 2025 forecast: ~3.2%

- Banking sector NPL (Q3 2024): 3.1%

- Performance tied to industrial/service sector resilience

Global Market Access

VakıfBank depends on international syndication and securitization to diversify funding and back lending; in 2024 international borrowings accounted for around 18% of total liabilities, easing domestic liquidity pressure.

Its credit spreads are constrained by Turkey’s sovereign rating (BB- by S&P in 2025), which raises funding costs versus peers and affects rates paid to global investors.

Maintaining CET1 ratio of ~13.5% (2024) and robust liquidity coverage is essential to attract capital during global uncertainty.

- Intl funding ~18% of liabilities (2024)

- Sovereign cap: S&P BB- (2025)

- CET1 ~13.5% (2024)

VakıfBank set for NIM rebound as easing inflation, policy normalization and FX risks persist

| Metric | 2024/2025 |

|---|---|

| Inflation (CPI) | 24.5% (2024) |

| CBRT policy rate | 35% (end-2024) |

| USD/TRY | ~31.5 (Dec-2024) |

| GDP growth | 3.5% (2024) / IMF ~3.2% (2025) |

| Intl funding | ~18% liabilities (2024) |

| CET1 | ~13.5% (2024) |

| Banking NPL | 3.1% (Q3-2024) |

Full Version Awaits

VakifBank PESTLE Analysis

The preview shown here is the exact VakifBank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and digital banking trends are reshaping VakifBank’s strategic landscape in our concise PESTLE snapshot—perfect for investors and advisors who need fast, actionable context. Purchase the full PESTLE analysis to access detailed regulatory, technological, and social risk assessments plus strategic recommendations you can deploy immediately.

Political factors

State Ownership Influence

Geopolitical Regional Stability

Turkey's transcontinental location exposes VakıfBank to both trade opportunities and geopolitical risks across Europe, Asia and the Middle East, with regional trade accounting for roughly 45% of Turkey's exports in 2024, directly affecting the bank's trade finance pipeline.

Instability in neighboring countries can compress VakıfBank's international trade finance volumes and elevate NPLs in foreign operations, where FX-linked exposures reached about $18bn on the bank's consolidated balance sheet in 2024.

By end-2025 VakıfBank must manage shifting diplomatic alliances and sanctions regimes that can alter cross-border capital flows and the security of its international assets, noting Turkey's foreign direct investment inflows fell 12% in 2024 versus 2023.

Strategic Government Incentives

International Diplomatic Relations

International diplomatic ties shape VakıfBank’s funding costs; improved relations with the EU and US can lower international borrowing spreads—Turkey’s sovereign CDS moved from ~740 bps in 2020 to ~250–300 bps in 2024–2025 during stabilization phases, easing access to cheaper funds.

Compliance with FATF and EU standards affects market access; Turkey’s FATF follow-up status and regulatory alignment in 2024–25 reduced compliance friction, supporting bond issuances and syndicated loans.

Positive diplomatic shifts have translated into better credit terms and JV opportunities with foreign banks, increasing syndicated loan volumes and cross-border partnership activity in 2024–25.

- Lower sovereign CDS (≈250–300 bps in 2024–25) improved borrowing spreads

- FATF alignment eased compliance barriers for global capital access

- Diplomatic gains increased syndicated loan and partnership activity

Domestic Policy Continuity

The predictability of Turkey’s political environment and macroeconomic management are critical for VakifBank’s long-term planning; GDP grew 3.5% in 2024 and inflation slowed to 58% year-end 2024, affecting lending and provisioning assumptions.

Consistent leadership at the Treasury and Finance Ministry through 2024–2025 supports stable regulatory expectations, enabling VakifBank to pursue growth targets tied to a 10–12% credit expansion forecast for 2025.

Significant political shifts could prompt leadership changes or a refocus of VakifBank’s mandate, risking adjustments to capital allocation, state-directed lending, or governance structures.

- 2024 GDP +3.5% and inflation ~58% (year-end 2024) influence credit risk pricing

- Treasury continuity supports 10–12% credit growth target for 2025

- Political shifts could alter board/management and state-directed lending priorities

VakıfBank: State Anchor, High TL Growth, FX Risks amid Elevated Inflation and CDS

| Metric | Value (2024) |

|---|---|

| State share | ~58% |

| State-subsidized loans | TRY 78bn |

| State-guaranteed share | ~22% |

| TL loan growth (2023) | ~24% y/y |

| ROAE (2023) | 9–11% |

| FX-linked exposures | $18bn |

| Sovereign CDS | ~250–300bps |

| GDP growth | +3.5% |

| Inflation (YE) | ~58% |

What is included in the product

Explores how macro-environmental factors affect VakifBank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to Turkey’s banking sector to identify risks, opportunities, and strategic responses.

A concise VakifBank PESTLE summary that’s visually segmented by category for rapid interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary Environment Management

Monetary Policy Shifts

Central Bank of the Republic of Türkiye policy rate changes—from 8.5% in Jan 2023 to 45% peak in 2023 and easing to 35% by end-2024—directly compress or expand VakıfBank’s net interest margin and profitability.

Higher rates raised funding costs and slowed retail/corporate loan growth, with Turkish credit Y/Y growth falling from 43% (2022) to ~15% in 2024, reducing new loan demand.

VakıfBank must rapidly reprice deposits and lending—short-term repricing actions in 2024 helped protect CET1 ratios around 12–13% amid volatile national monetary shifts.

Currency Exchange Volatility

The Turkish lira’s 2024–2025 volatility—USD/TRY moved from ~27.0 in Jan 2024 to ~31.5 by Dec 2024, and EUR/TRY from ~29.0 to ~33.0—directly pressures VakıfBank’s CET1 and capital adequacy via FX-weighted exposures and FX‑denominated loans totaling several billion TRY. VakıfBank applies stringent FX risk limits, hedging and stress tests to shield the balance sheet; stable FX markets are critical to valuing international assets and servicing foreign debt.

GDP Growth Trends

Turkey's GDP expanded 3.5% in 2024 with IMF projecting ~3.2% for 2025, affecting VakifBank's loan demand across retail, SME and corporate segments; stronger growth reduces credit costs and supports fee income from trade finance.

Historical cycles show lower NPL ratios during expansions—Turkey's banking sector NPL ratio fell to 3.1% in Q3 2024—benefiting VakifBank's asset quality and investment banking activity tied to industry and services resilience through 2025.

- 2024 GDP growth: 3.5%

- IMF 2025 forecast: ~3.2%

- Banking sector NPL (Q3 2024): 3.1%

- Performance tied to industrial/service sector resilience

Global Market Access

VakıfBank depends on international syndication and securitization to diversify funding and back lending; in 2024 international borrowings accounted for around 18% of total liabilities, easing domestic liquidity pressure.

Its credit spreads are constrained by Turkey’s sovereign rating (BB- by S&P in 2025), which raises funding costs versus peers and affects rates paid to global investors.

Maintaining CET1 ratio of ~13.5% (2024) and robust liquidity coverage is essential to attract capital during global uncertainty.

- Intl funding ~18% of liabilities (2024)

- Sovereign cap: S&P BB- (2025)

- CET1 ~13.5% (2024)

VakıfBank set for NIM rebound as easing inflation, policy normalization and FX risks persist

| Metric | 2024/2025 |

|---|---|

| Inflation (CPI) | 24.5% (2024) |

| CBRT policy rate | 35% (end-2024) |

| USD/TRY | ~31.5 (Dec-2024) |

| GDP growth | 3.5% (2024) / IMF ~3.2% (2025) |

| Intl funding | ~18% liabilities (2024) |

| CET1 | ~13.5% (2024) |

| Banking NPL | 3.1% (Q3-2024) |

Full Version Awaits

VakifBank PESTLE Analysis

The preview shown here is the exact VakifBank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.