Valeo Porter's Five Forces Analysis

Don't Miss the Bigger Picture

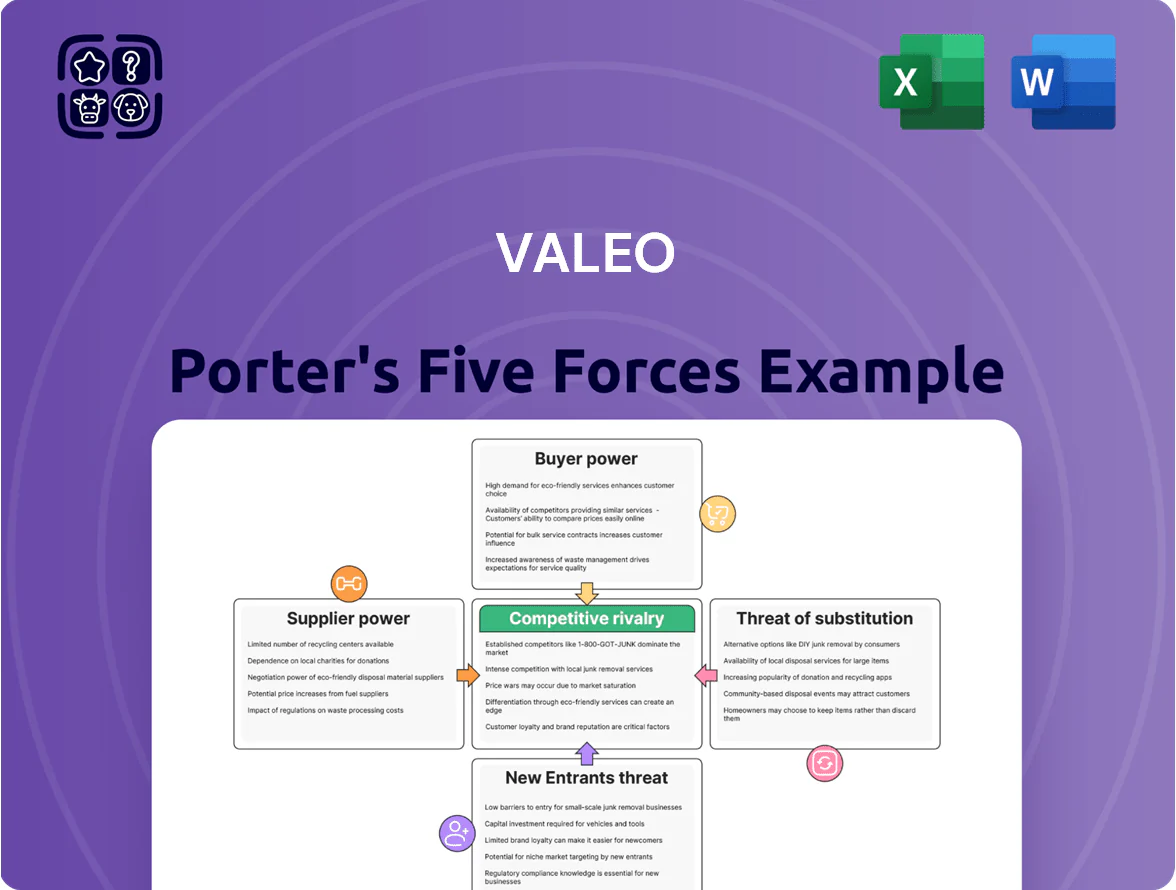

Valeo faces intense rivalry driven by technological shifts to EVs and ADAS, significant supplier power for advanced components, and moderate buyer leverage from OEM consolidation—while new entrants and substitutes present growing threats through software-driven value propositions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valeo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor manufacturers

The automotive shift to ADAS and electrification makes Valeo highly dependent on high-end chips; ADAS content per vehicle rose 22% to 1,350 euros average in 2025, increasing chip spend. As of late 2025, advanced-node capacity is concentrated: TSMC, Samsung Foundry and GlobalFoundries control over 70% of automotive-grade advanced-node output, giving suppliers price and delivery leverage. Valeo needs multi-year supply contracts and equity partnerships to secure silicon for its Move Up strategy and avoid production delays.

Volatility in raw material pricing

Valeo’s electric motor and thermal systems need large volumes of copper, aluminum, and rare earths; end-2025 LME copper averaged about $9,200/ton and alumina-based pressure pushed aluminum near $2,300/ton, adding margin uncertainty despite Valeo’s hedges.

Suppliers hold bargaining power as green energy shifts lift demand from EV makers and renewables; rare earth tightness saw NdPr prices spike ~35% in 2025, amplifying input-cost risk for Valeo.

Shift toward specialized software providers

As vehicles go software-defined, Valeo now embeds third-party AI and cybersecurity in its sensors and ECUs; in 2024 software content per vehicle rose ~30% year-over-year, raising supplier leverage.

Specialized firms hold hard-to-replicate IP, so they command premium pricing—software suppliers’ gross margins averaged ~55% in 2024 versus 20–30% for mechanical vendors—strengthening their bargaining power.

Valeo must weigh costly external deals (AI/cyber partnerships can cost tens of millions upfront) against scaling in-house teams to retain control and limit supplier dependency.

Sustainability and ESG compliance requirements

Valeo’s carbon-neutrality commitments force sourcing from suppliers meeting strict 2025 green certifications, shrinking the eligible vendor pool and raising dependency on compliant suppliers.

This selective sourcing increases supplier bargaining power: compliant vendors can charge premiums—estimates show low-carbon suppliers command 3–7% higher prices—while Valeo targets Scope 3 cuts of ~30% by 2030.

- Smaller vendor pool raises leverage for compliant suppliers

- Compliant suppliers can charge 3–7% price premium

- Valeo aims ~30% Scope 3 reduction by 2030

Tier 2 and Tier 3 localization in China

Valeo’s large China footprint makes it rely more on local Tier 2/Tier 3 suppliers for cost and speed; in 2024 China accounted for about 30% of Valeo’s revenue (approx €6.5bn), so supplier proximity matters.

Regional suppliers gained leverage by scaling with Chinese OEMs—some Tier 2 firms grew revenues 15–25% y/y in 2023—raising negotiation pressure on Valeo.

Valeo must localize to stay competitive but faces rising component costs: China labor and input-cost inflation added ~4–6% to parts costs in 2023, squeezing margins.

- China ~30% of Valeo revenue (~€6.5bn in 2024)

- Tier 2 growth 15–25% y/y in 2023

- China parts-cost inflation ~4–6% in 2023

- Trade-off: localization gains speed, loses price leverage

Supplier power squeezes margins: chip, software & commodity spikes amplify Valeo risks

Suppliers wield strong leverage: advanced-node foundries (TSMC, Samsung, GlobalFoundries >70% auto-grade output in late-2025) and specialized software/IP vendors (software gross margins ~55% in 2024) drive price and delivery risk; commodity spikes (LME copper ~$9,200/t in 2025; aluminum ~€2,300/t; NdPr +35% in 2025) add margin pressure. Valeo’s China reliance (≈30% revenue ≈€6.5bn in 2024) and green-cert constraints (low-carbon premium 3–7%) shrink supplier options and raise costs.

| Metric | Value |

|---|---|

| Auto-grade advanced-node share (late-2025) | >70% (TSMC, Samsung, GF) |

| Copper (LME, 2025 avg) | $9,200/ton |

| NdPr price change (2025) | +35% |

| Software vendor gross margin (2024) | ~55% |

| China revenue share (2024) | ~30% (~€6.5bn) |

| Low-carbon supplier premium (2025 est.) | 3–7% |

What is included in the product

Tailored exclusively for Valeo, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics that influence Valeo's pricing, profitability, and strategic positioning.

Compact Porter's Five Forces snapshot for Valeo—instantly visualize supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions.

Customers Bargaining Power

Consolidation and scale of global OEMs

Vertical integration by electric vehicle leaders

Leading EV makers like Tesla and BYD reported vertical integration gains in 2024, with Tesla producing >60% of its e-motors and BYD making >70% of power electronics, forcing Valeo to match with either superior tech or lower prices to stay a supplier.

The risk of insourcing exerts continuous price pressure: Valeo’s electrification module ASPs fell ~4–6% YoY in 2023–24 in Europe, reflecting buyers’ greater leverage and threat of becoming competitors.

Rise of Chinese domestic automakers

The rapid rise of Chinese OEMs—BYD, Geely, SAIC—drove China auto sales to 27.5 million units in 2024, creating customers focused on speed-to-market and aggressive pricing.

These high-volume buyers show low brand loyalty and frequently switch suppliers for single-digit percent cost savings, increasing customer bargaining power.

To retain them, Valeo must prove value via localized R&D; in 2024 China R&D spend hit $410 billion, so targeted investments and faster product cycles are essential.

Demand for modular and integrated systems

OEMs are shifting from components to integrated systems like Valeo's Smart e-Drive and thermal loops, lowering assembly work but raising demands for system-level warranties and performance guarantees.

By 2025, OEM contracts increasingly require end-to-end responsibility; integrated powertrain modules accounted for ~28% of global EV supplier revenues in 2024, forcing Valeo to offer full-system solutions to stay competitive.

- OEMs demand system guarantees, not parts

- Integrated modules = lower OEM assembly cost

- 2024: ~28% supplier revenue from integrated EV systems

- Full-system capability is a 2025 market necessity

Transparency in cost structures

- Open-book procurement reduces margin opacity

- Std parts margins down ~150–300 bps (2024)

- Valeo R&D €1.2bn in 2024 to target ADAS/lighting

- Buyers gain leverage on price and terms

Valeo margins squeezed by OEM concentration, ASP drops; €1.2bn R&D pivots to ADAS

| Metric | 2024/2025 |

|---|---|

| Top OEM share of revenue | 30–40% |

| Valeo gross margin | 18.9% (2024) |

| R&D spend | €1.2bn (2024) |

| Electrification ASP change | -4–6% YoY (2023–24) |

| Std parts margin hit | -150–300 bps (2024) |

Full Version Awaits

Valeo Porter's Five Forces Analysis

This preview shows the exact Valeo Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups.

The document displayed here is the full, professionally formatted file ready for download and use the moment you buy.

You're viewing the final deliverable: the same comprehensive analysis available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Valeo faces intense rivalry driven by technological shifts to EVs and ADAS, significant supplier power for advanced components, and moderate buyer leverage from OEM consolidation—while new entrants and substitutes present growing threats through software-driven value propositions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valeo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor manufacturers

The automotive shift to ADAS and electrification makes Valeo highly dependent on high-end chips; ADAS content per vehicle rose 22% to 1,350 euros average in 2025, increasing chip spend. As of late 2025, advanced-node capacity is concentrated: TSMC, Samsung Foundry and GlobalFoundries control over 70% of automotive-grade advanced-node output, giving suppliers price and delivery leverage. Valeo needs multi-year supply contracts and equity partnerships to secure silicon for its Move Up strategy and avoid production delays.

Volatility in raw material pricing

Valeo’s electric motor and thermal systems need large volumes of copper, aluminum, and rare earths; end-2025 LME copper averaged about $9,200/ton and alumina-based pressure pushed aluminum near $2,300/ton, adding margin uncertainty despite Valeo’s hedges.

Suppliers hold bargaining power as green energy shifts lift demand from EV makers and renewables; rare earth tightness saw NdPr prices spike ~35% in 2025, amplifying input-cost risk for Valeo.

Shift toward specialized software providers

As vehicles go software-defined, Valeo now embeds third-party AI and cybersecurity in its sensors and ECUs; in 2024 software content per vehicle rose ~30% year-over-year, raising supplier leverage.

Specialized firms hold hard-to-replicate IP, so they command premium pricing—software suppliers’ gross margins averaged ~55% in 2024 versus 20–30% for mechanical vendors—strengthening their bargaining power.

Valeo must weigh costly external deals (AI/cyber partnerships can cost tens of millions upfront) against scaling in-house teams to retain control and limit supplier dependency.

Sustainability and ESG compliance requirements

Valeo’s carbon-neutrality commitments force sourcing from suppliers meeting strict 2025 green certifications, shrinking the eligible vendor pool and raising dependency on compliant suppliers.

This selective sourcing increases supplier bargaining power: compliant vendors can charge premiums—estimates show low-carbon suppliers command 3–7% higher prices—while Valeo targets Scope 3 cuts of ~30% by 2030.

- Smaller vendor pool raises leverage for compliant suppliers

- Compliant suppliers can charge 3–7% price premium

- Valeo aims ~30% Scope 3 reduction by 2030

Tier 2 and Tier 3 localization in China

Valeo’s large China footprint makes it rely more on local Tier 2/Tier 3 suppliers for cost and speed; in 2024 China accounted for about 30% of Valeo’s revenue (approx €6.5bn), so supplier proximity matters.

Regional suppliers gained leverage by scaling with Chinese OEMs—some Tier 2 firms grew revenues 15–25% y/y in 2023—raising negotiation pressure on Valeo.

Valeo must localize to stay competitive but faces rising component costs: China labor and input-cost inflation added ~4–6% to parts costs in 2023, squeezing margins.

- China ~30% of Valeo revenue (~€6.5bn in 2024)

- Tier 2 growth 15–25% y/y in 2023

- China parts-cost inflation ~4–6% in 2023

- Trade-off: localization gains speed, loses price leverage

Supplier power squeezes margins: chip, software & commodity spikes amplify Valeo risks

Suppliers wield strong leverage: advanced-node foundries (TSMC, Samsung, GlobalFoundries >70% auto-grade output in late-2025) and specialized software/IP vendors (software gross margins ~55% in 2024) drive price and delivery risk; commodity spikes (LME copper ~$9,200/t in 2025; aluminum ~€2,300/t; NdPr +35% in 2025) add margin pressure. Valeo’s China reliance (≈30% revenue ≈€6.5bn in 2024) and green-cert constraints (low-carbon premium 3–7%) shrink supplier options and raise costs.

| Metric | Value |

|---|---|

| Auto-grade advanced-node share (late-2025) | >70% (TSMC, Samsung, GF) |

| Copper (LME, 2025 avg) | $9,200/ton |

| NdPr price change (2025) | +35% |

| Software vendor gross margin (2024) | ~55% |

| China revenue share (2024) | ~30% (~€6.5bn) |

| Low-carbon supplier premium (2025 est.) | 3–7% |

What is included in the product

Tailored exclusively for Valeo, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics that influence Valeo's pricing, profitability, and strategic positioning.

Compact Porter's Five Forces snapshot for Valeo—instantly visualize supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions.

Customers Bargaining Power

Consolidation and scale of global OEMs

Vertical integration by electric vehicle leaders

Leading EV makers like Tesla and BYD reported vertical integration gains in 2024, with Tesla producing >60% of its e-motors and BYD making >70% of power electronics, forcing Valeo to match with either superior tech or lower prices to stay a supplier.

The risk of insourcing exerts continuous price pressure: Valeo’s electrification module ASPs fell ~4–6% YoY in 2023–24 in Europe, reflecting buyers’ greater leverage and threat of becoming competitors.

Rise of Chinese domestic automakers

The rapid rise of Chinese OEMs—BYD, Geely, SAIC—drove China auto sales to 27.5 million units in 2024, creating customers focused on speed-to-market and aggressive pricing.

These high-volume buyers show low brand loyalty and frequently switch suppliers for single-digit percent cost savings, increasing customer bargaining power.

To retain them, Valeo must prove value via localized R&D; in 2024 China R&D spend hit $410 billion, so targeted investments and faster product cycles are essential.

Demand for modular and integrated systems

OEMs are shifting from components to integrated systems like Valeo's Smart e-Drive and thermal loops, lowering assembly work but raising demands for system-level warranties and performance guarantees.

By 2025, OEM contracts increasingly require end-to-end responsibility; integrated powertrain modules accounted for ~28% of global EV supplier revenues in 2024, forcing Valeo to offer full-system solutions to stay competitive.

- OEMs demand system guarantees, not parts

- Integrated modules = lower OEM assembly cost

- 2024: ~28% supplier revenue from integrated EV systems

- Full-system capability is a 2025 market necessity

Transparency in cost structures

- Open-book procurement reduces margin opacity

- Std parts margins down ~150–300 bps (2024)

- Valeo R&D €1.2bn in 2024 to target ADAS/lighting

- Buyers gain leverage on price and terms

Valeo margins squeezed by OEM concentration, ASP drops; €1.2bn R&D pivots to ADAS

| Metric | 2024/2025 |

|---|---|

| Top OEM share of revenue | 30–40% |

| Valeo gross margin | 18.9% (2024) |

| R&D spend | €1.2bn (2024) |

| Electrification ASP change | -4–6% YoY (2023–24) |

| Std parts margin hit | -150–300 bps (2024) |

Full Version Awaits

Valeo Porter's Five Forces Analysis

This preview shows the exact Valeo Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups.

The document displayed here is the full, professionally formatted file ready for download and use the moment you buy.

You're viewing the final deliverable: the same comprehensive analysis available instantly after payment.