Valero Energy Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

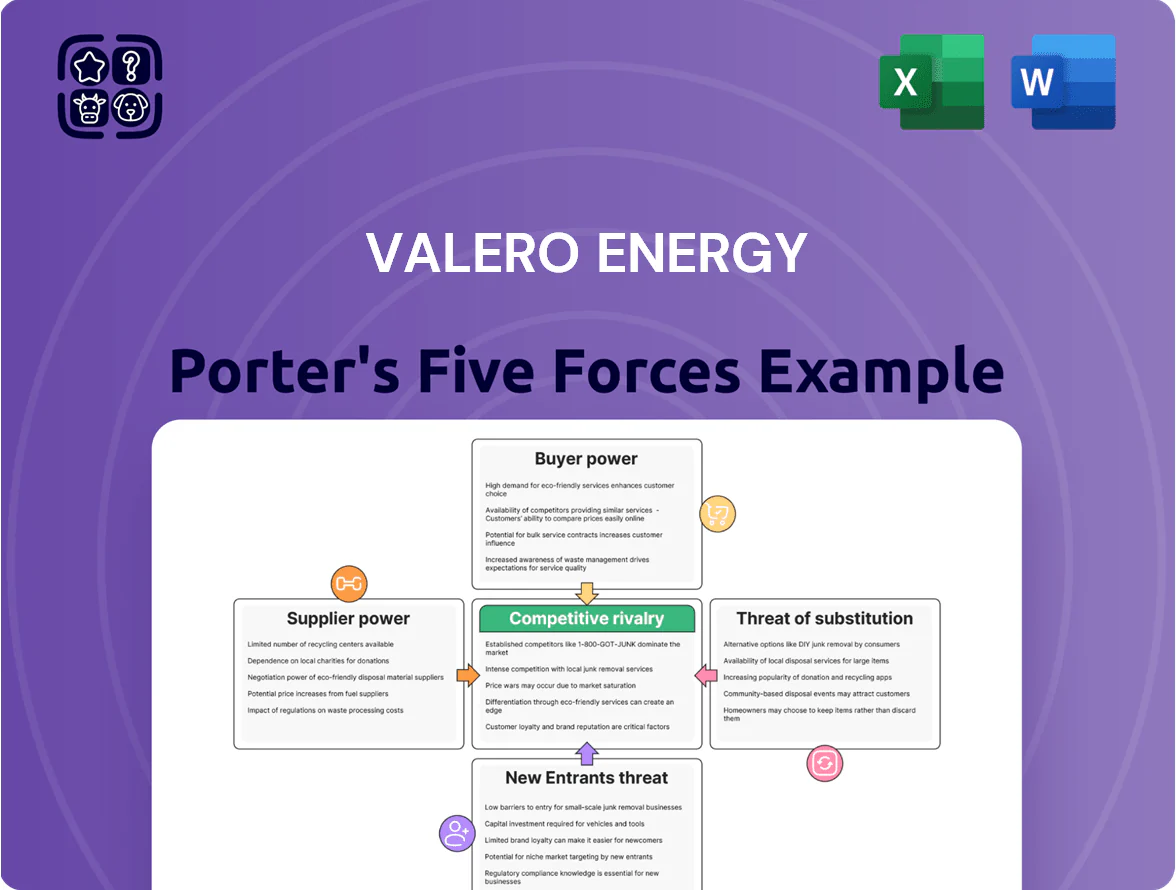

Valero Energy faces intense competitive rivalry, regulatory pressures, and fluctuating input costs that shape its margins and strategic choices; supplier and buyer power vary across regions, while substitutes and entry threats remain moderate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valero Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Global Crude Oil Feedstock

As a merchant refiner, Valero buys most crude from external sources—national oil companies and large independents—so it lacks upstream integration and cannot lock in margins.

By end-2025, OPEC+ quotas and geopolitical tensions kept Brent around $80–90/bbl on average, pushing Valero’s crude cost variability and gross refining margin swings above historical averages.

This exposure makes Valero vulnerable to sudden supply shocks; a 10% crude price jump can cut refinery gross margins by roughly $3–5/BBL, squeezing cash flow and refining returns.

Tightening Supply of Renewable Feedstocks

Valero's move into renewable diesel and sustainable aviation fuel shifts suppliers toward fats, oils, and greases (FOG); by 2025 over 30 US refineries target renewables, pushing feedstock demand up ~40% vs 2022 per IEA-style estimates, so FOG suppliers gain pricing power.

Dependency on Midstream Infrastructure

Valero relies on third-party pipelines and marine terminals to move ~70% of crude and products; it owns limited logistics in key hubs but depends on midstream majors like Plains and Kinder Morgan for critical-path routes. In 2024 capacity tightness raised regional tariffs by 12–18%, letting operators push higher fees or delivery windows, squeezing Valero’s refining margins—natural-gas and crude transport costs rose ~8% YoY.

Concentration of Specialized Technology Providers

Refining needs specialized catalysts, chemicals, and engineering from a few global firms; in 2024 the top 5 catalyst suppliers controlled ~65% of the market, raising supplier leverage over Valero’s margins.

As refineries adapt to 2025 EPA and IMO-like standards, complexity and reliance on niche tech rises, increasing switching costs and CAPEX for retrofits.

These suppliers exert power via scarce expertise, long lead times, and service contracts that protect uptime and safety, pressuring operating margins by an estimated 1–2%.

- Top-5 suppliers ~65% market share (2024)

- Switching costs: months of downtime, multimillion-dollar retrofits

- Estimated margin pressure: 1–2% from supplier constraints

Labor Market Pressures for Skilled Trades

The refining sector faces a skilled-labor squeeze: by late 2025 the median refinery technician age was ~49 and petroleum engineering grads fell 18% since 2015, tightening supply for Valero’s operations.

Unions and specialist contractors are extracting higher pay—wage premiums rose ~9% year-over-year in 2024—lifting operating costs and capitalizing on replacement-skills scarcity.

Suppliers Gain Leverage: Brent Volatility, Midstream Costs & Catalyst Concentration Squeeze Margins

Suppliers wield moderate-to-high power: Valero buys most crude externally, faces Brent volatility (~$80–90/bbl in 2025), and relies on midstream players for ~70% of transport, raising logistics fees 12–18% (2024); catalyst/top-tech suppliers hold ~65% market share (2024), adding ~1–2% margin pressure; renewables feedstock demand up ~40% vs 2022, boosting supplier leverage.

| Metric | Value |

|---|---|

| Brent (avg 2025) | $80–90/bbl |

| Crude transported via third parties | ~70% |

| Regional tariff rise (2024) | 12–18% |

| Top-5 catalyst share (2024) | ~65% |

| Renewables feedstock demand ↑ vs 2022 | ~40% |

| Supplier-driven margin pressure | ~1–2% |

What is included in the product

Provides a concise Porter’s Five Forces review for Valero Energy, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, plus emerging disruptors shaping its refinery and retail margins.

A concise Porter's Five Forces one-sheet for Valero—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to guide strategic decisions.

Customers Bargaining Power

Commodity Nature of Refined Products

Valero’s gasoline, diesel, and jet fuel behave as undifferentiated commodities, so buyers switch suppliers on price; wholesale fuel shows minimal brand loyalty.

Transparent pricing across hubs—Argus, Platts—keeps margins tight; U.S. wholesale gasoline crack spread averaged about $10.50/bbl in 2024, constraining Valero’s premium pricing.

Consolidation of Large Scale Wholesale Buyers

Low Switching Costs for Retail Distributors

Independent gas station owners and regional distributors can switch suppliers quickly if logistics allow, and because Valero sells heavily through unbranded channels and wholesale racks, customers respond strongly to daily rack-price moves; in 2024 US rack spreads averaged volatile swings of ±$0.03–$0.07/gal, raising price sensitivity.

Growth of Fleet Management and Procurement Platforms

The rise of digital procurement platforms by 2025 lets fleets aggregate demand and solicit competitive fuel and lubricant bids, raising price transparency and reducing relationship-based sales; Valero saw commercial channel margins face pressure as spot diesel rack spreads narrowed ~15% from 2020–2024.

Platforms force Valero into more competitive bidding, tightening margins and increasing customer bargaining power; in 2024 ~22% of US fleet fuel purchases occurred via digital marketplaces, up from ~8% in 2020.

Regulatory Influence on Consumer Choice

By late 2025, ~$25 billion in US and EU subsidies for low-carbon fuels and expanding carbon pricing (e.g., EU ETS price ~95 €/t CO2 in 2025) have shifted buyer power toward low‑carbon substitutes, letting fleets and refiners demand lower carbon intensity fuels.

As carbon taxes and LCFS (low‑carbon fuel standards) tighten, customers can push Valero to shift volumes; failure risks share loss to renewable diesel and SAF producers growing at ~20% CAGR.

- ~$25B subsidies (US/EU) by 2025

- EU ETS ≈95 €/t CO2 (2025)

- Renewable diesel/SAF ~20% CAGR

- Customer demand for low‑CI fuels rising

Consolidated buyers, shrinking rack spreads, and policy-driven shift to low‑CI fuels

Buyers hold high leverage: fuel is commoditized, price‑transparent (Argus/Platts), and large wholesalers/top10 retailers control ~45% pump sales (2025), forcing volume discounts; Valero sold ~3.1 mbpd wholesale/rack in 2024. Digital marketplaces grew fleet purchases to ~22% (2024), narrowing rack spreads ~15% (2020–2024). Policy shifts (≈$25B low‑carbon subsidies by 2025; EU ETS ≈95 €/t CO2) push demand toward low‑CI fuels.

| Metric | Value |

|---|---|

| Valero wholesale/rack (2024) | ≈3.1 mbpd |

| Top10 retail share (2025) | ≈45% |

| Fleet via marketplaces (2024) | ≈22% |

| Rack spread change (2020–24) | −15% |

| Low‑carbon subsidies (US/EU, 2025) | ≈$25B |

| EU ETS price (2025) | ≈95 €/t CO2 |

Preview Before You Purchase

Valero Energy Porter's Five Forces Analysis

This preview shows the exact Valero Energy Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Valero Energy faces intense competitive rivalry, regulatory pressures, and fluctuating input costs that shape its margins and strategic choices; supplier and buyer power vary across regions, while substitutes and entry threats remain moderate.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valero Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Global Crude Oil Feedstock

As a merchant refiner, Valero buys most crude from external sources—national oil companies and large independents—so it lacks upstream integration and cannot lock in margins.

By end-2025, OPEC+ quotas and geopolitical tensions kept Brent around $80–90/bbl on average, pushing Valero’s crude cost variability and gross refining margin swings above historical averages.

This exposure makes Valero vulnerable to sudden supply shocks; a 10% crude price jump can cut refinery gross margins by roughly $3–5/BBL, squeezing cash flow and refining returns.

Tightening Supply of Renewable Feedstocks

Valero's move into renewable diesel and sustainable aviation fuel shifts suppliers toward fats, oils, and greases (FOG); by 2025 over 30 US refineries target renewables, pushing feedstock demand up ~40% vs 2022 per IEA-style estimates, so FOG suppliers gain pricing power.

Dependency on Midstream Infrastructure

Valero relies on third-party pipelines and marine terminals to move ~70% of crude and products; it owns limited logistics in key hubs but depends on midstream majors like Plains and Kinder Morgan for critical-path routes. In 2024 capacity tightness raised regional tariffs by 12–18%, letting operators push higher fees or delivery windows, squeezing Valero’s refining margins—natural-gas and crude transport costs rose ~8% YoY.

Concentration of Specialized Technology Providers

Refining needs specialized catalysts, chemicals, and engineering from a few global firms; in 2024 the top 5 catalyst suppliers controlled ~65% of the market, raising supplier leverage over Valero’s margins.

As refineries adapt to 2025 EPA and IMO-like standards, complexity and reliance on niche tech rises, increasing switching costs and CAPEX for retrofits.

These suppliers exert power via scarce expertise, long lead times, and service contracts that protect uptime and safety, pressuring operating margins by an estimated 1–2%.

- Top-5 suppliers ~65% market share (2024)

- Switching costs: months of downtime, multimillion-dollar retrofits

- Estimated margin pressure: 1–2% from supplier constraints

Labor Market Pressures for Skilled Trades

The refining sector faces a skilled-labor squeeze: by late 2025 the median refinery technician age was ~49 and petroleum engineering grads fell 18% since 2015, tightening supply for Valero’s operations.

Unions and specialist contractors are extracting higher pay—wage premiums rose ~9% year-over-year in 2024—lifting operating costs and capitalizing on replacement-skills scarcity.

Suppliers Gain Leverage: Brent Volatility, Midstream Costs & Catalyst Concentration Squeeze Margins

Suppliers wield moderate-to-high power: Valero buys most crude externally, faces Brent volatility (~$80–90/bbl in 2025), and relies on midstream players for ~70% of transport, raising logistics fees 12–18% (2024); catalyst/top-tech suppliers hold ~65% market share (2024), adding ~1–2% margin pressure; renewables feedstock demand up ~40% vs 2022, boosting supplier leverage.

| Metric | Value |

|---|---|

| Brent (avg 2025) | $80–90/bbl |

| Crude transported via third parties | ~70% |

| Regional tariff rise (2024) | 12–18% |

| Top-5 catalyst share (2024) | ~65% |

| Renewables feedstock demand ↑ vs 2022 | ~40% |

| Supplier-driven margin pressure | ~1–2% |

What is included in the product

Provides a concise Porter’s Five Forces review for Valero Energy, highlighting competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, plus emerging disruptors shaping its refinery and retail margins.

A concise Porter's Five Forces one-sheet for Valero—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to guide strategic decisions.

Customers Bargaining Power

Commodity Nature of Refined Products

Valero’s gasoline, diesel, and jet fuel behave as undifferentiated commodities, so buyers switch suppliers on price; wholesale fuel shows minimal brand loyalty.

Transparent pricing across hubs—Argus, Platts—keeps margins tight; U.S. wholesale gasoline crack spread averaged about $10.50/bbl in 2024, constraining Valero’s premium pricing.

Consolidation of Large Scale Wholesale Buyers

Low Switching Costs for Retail Distributors

Independent gas station owners and regional distributors can switch suppliers quickly if logistics allow, and because Valero sells heavily through unbranded channels and wholesale racks, customers respond strongly to daily rack-price moves; in 2024 US rack spreads averaged volatile swings of ±$0.03–$0.07/gal, raising price sensitivity.

Growth of Fleet Management and Procurement Platforms

The rise of digital procurement platforms by 2025 lets fleets aggregate demand and solicit competitive fuel and lubricant bids, raising price transparency and reducing relationship-based sales; Valero saw commercial channel margins face pressure as spot diesel rack spreads narrowed ~15% from 2020–2024.

Platforms force Valero into more competitive bidding, tightening margins and increasing customer bargaining power; in 2024 ~22% of US fleet fuel purchases occurred via digital marketplaces, up from ~8% in 2020.

Regulatory Influence on Consumer Choice

By late 2025, ~$25 billion in US and EU subsidies for low-carbon fuels and expanding carbon pricing (e.g., EU ETS price ~95 €/t CO2 in 2025) have shifted buyer power toward low‑carbon substitutes, letting fleets and refiners demand lower carbon intensity fuels.

As carbon taxes and LCFS (low‑carbon fuel standards) tighten, customers can push Valero to shift volumes; failure risks share loss to renewable diesel and SAF producers growing at ~20% CAGR.

- ~$25B subsidies (US/EU) by 2025

- EU ETS ≈95 €/t CO2 (2025)

- Renewable diesel/SAF ~20% CAGR

- Customer demand for low‑CI fuels rising

Consolidated buyers, shrinking rack spreads, and policy-driven shift to low‑CI fuels

Buyers hold high leverage: fuel is commoditized, price‑transparent (Argus/Platts), and large wholesalers/top10 retailers control ~45% pump sales (2025), forcing volume discounts; Valero sold ~3.1 mbpd wholesale/rack in 2024. Digital marketplaces grew fleet purchases to ~22% (2024), narrowing rack spreads ~15% (2020–2024). Policy shifts (≈$25B low‑carbon subsidies by 2025; EU ETS ≈95 €/t CO2) push demand toward low‑CI fuels.

| Metric | Value |

|---|---|

| Valero wholesale/rack (2024) | ≈3.1 mbpd |

| Top10 retail share (2025) | ≈45% |

| Fleet via marketplaces (2024) | ≈22% |

| Rack spread change (2020–24) | −15% |

| Low‑carbon subsidies (US/EU, 2025) | ≈$25B |

| EU ETS price (2025) | ≈95 €/t CO2 |

Preview Before You Purchase

Valero Energy Porter's Five Forces Analysis

This preview shows the exact Valero Energy Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.