Valmont Industries Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Valmont Industries faces moderate supplier leverage, intense rivalry among infrastructure-focused peers, and growing substitution pressure from advanced materials and IoT-enabled alternatives, while buyer concentration and regulatory hurdles shape strategic choices; this snapshot highlights key pressures but only scratches the surface.

Suppliers Bargaining Power

Raw Material Price Volatility

The production of Valmont Industries' infrastructure and irrigation systems depends on steel, zinc, and aluminum, exposing margins to global commodity swings; LTM 2025 metal price moves: steel +18% y/y, zinc +22% y/y, aluminum +12% y/y.

Suppliers gain leverage when demand spikes or trade curbs occur—2024–25 export curbs from major producers raised input tightness and premium spreads.

Valmont offsets risk via multi-year supply contracts and price-surcharge clauses, but input cost remains a primary margin driver; raw materials accounted for ~28% of COGS in FY2024.

Geopolitical stability through late 2025—notably tensions in major metal-exporting regions—keeps supplier bargaining power elevated and volatility high.

Specialized Electronic Component Availability

As Valmont adds semiconductors and sensors to Valley irrigation and smart poles, reliance on specialized suppliers rises; global chip shortages in 2021–22 cut industry shipment capacity by ~10–15%, and sensor lead times now often exceed 20 weeks, forcing competition with auto and telecom firms. Technical specs for precision ag limit qualified vendors to a few players, giving suppliers moderate bargaining power and raising risks of delays or 5–12% cost increases on advanced lines.

Energy and Logistics Costs

Valmont’s energy-intensive manufacturing and galvanizing make it hostage to utility and fuel suppliers; US industrial electricity rose ~8% in 2023 and Henry Hub natural gas averaged $2.66/MMBtu in 2024, directly lifting COGS in coatings where heat is central.

Large, bulky poles and irrigation gear make freight a major cost; global ocean freight rates remained ~40% above pre‑pandemic levels in 2024, and carriers pass fuel surcharges and capacity premiums, keeping supplier bargaining power high.

Labor Market Constraints

Valmont relies on highly skilled engineers and specialized trade labor for manufacturing and galvanizing; tight regional labor markets raise worker bargaining power, driving wage and benefit inflation—US specialty construction wages rose 6.2% in 2024 year-over-year, pressuring margins.

To counter this, Valmont invested in training and retention—about $18M in workforce development in 2024—and must sustain those programs, making human capital a recurring supplier-side cost.

- Skilled labor shortage increases wages and benefits

- US specialty wages +6.2% in 2024

- $18M workforce training spend in 2024

- Persistent, recurring cost pressure on margins

Geographic Concentration of Input Sources

- 2024 specialty steel export curbs -> ~12% price rise

- High logistics: inland freight adds 8–15% cost

- Diversification reduces but cannot eliminate regional risk

- Regional supplier power remains critical in procurement

Suppliers Squeeze Valmont: Metals, Freight & Labor Drive Cost Pressure

Suppliers hold elevated bargaining power for Valmont due to concentrated metal sources, elevated freight, specialized chip/sensor vendors, and tight skilled labor—raw materials ~28% of COGS (FY2024), LTM 2025 metal moves: steel +18%, zinc +22%, aluminum +12%; specialty steel export curbs ↑12% (2024); US specialty wages +6.2% (2024); workforce training $18M (2024).

| Item | Metric |

|---|---|

| Raw materials | 28% of COGS (FY2024) |

| Steel | +18% LTM 2025 |

| Zinc | +22% LTM 2025 |

| Aluminum | +12% LTM 2025 |

| Specialty steel curbs | +12% price (2024) |

| Wages | +6.2% US specialty (2024) |

| Workforce spend | $18M (2024) |

What is included in the product

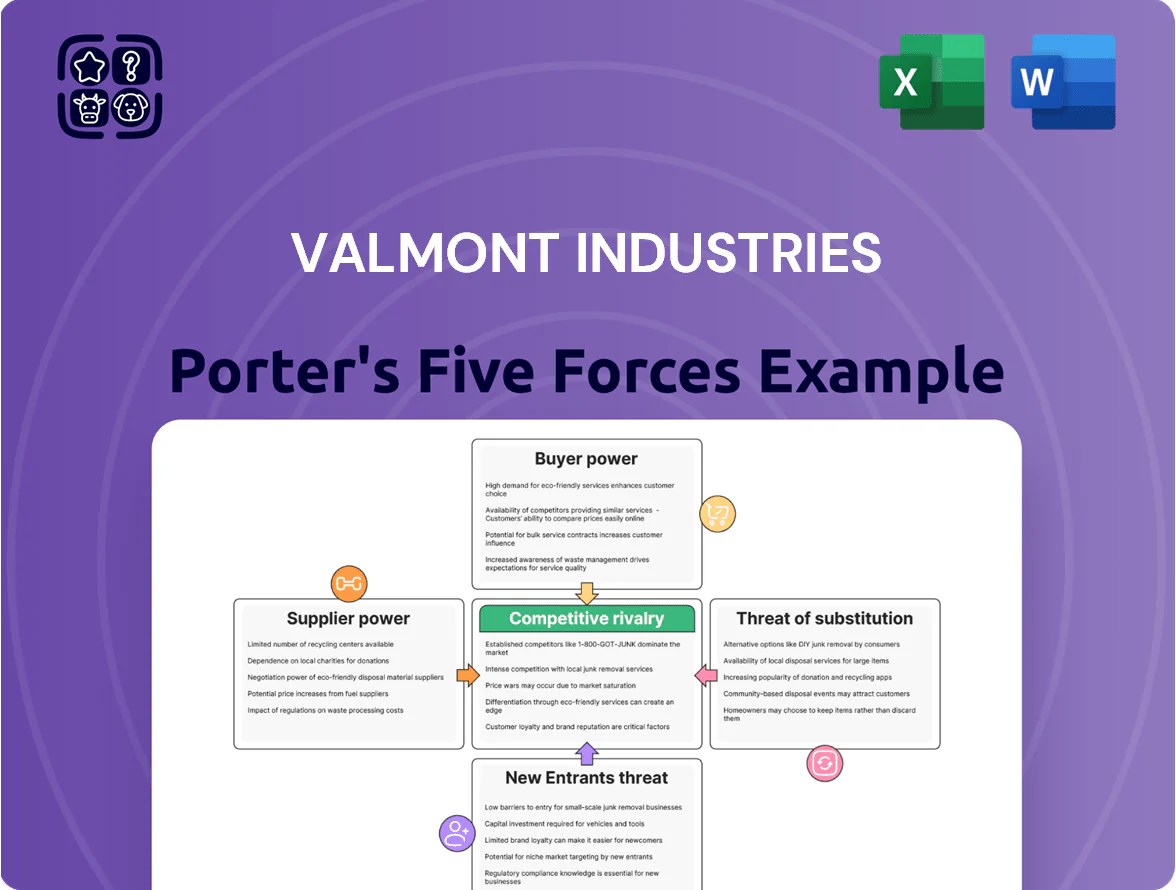

Tailored Porter's Five Forces assessment of Valmont Industries that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and highlights disruptive forces impacting pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Valmont Industries—quickly spot supplier, buyer, and competitive pressures to streamline capital allocation and strategic responses.

Customers Bargaining Power

Government and Utility Procurement Influence

A substantial share of Valmont Industries’ 2024 revenue—about 28%, or roughly $630 million—comes from state utilities and DOTs that use formal competitive bids, giving these institutional buyers strong leverage through large contract sizes and tight specs.

Taxpayer-funded projects force pressure for lowest lifecycle cost plus strict safety; losing a single major government contract can cut regional revenue by >15% and lower plant utilization sharply.

Agricultural Commodity Price Sensitivity

The demand for Valmont Industries’ mechanized irrigation tracks closely to farmers’ net income, which fell for US row-crop growers 2024–25 as corn, soy and wheat prices declined ~18% year-over-year, boosting customer bargaining power.

When commodity prices drop, growers defer capex or push for better financing; Valmont responded in 2024 with targeted incentives and tech bundles, keeping margins under pressure.

This cyclicality means the farming cohort can significantly influence Valmont’s sales timing and pricing, concentrating negotiating leverage in down cycles.

Sophisticated Corporate Telecommunications Buyers

Customers in Valmont Industries' wireless segment—major telecom carriers and tower operators—are highly sophisticated and price-sensitive, with top five carriers in the US controlling ~70% of wireless subscriptions (CTIA 2024), boosting their negotiating leverage.

These buyers consolidate purchases to secure volume discounts for 5G support structures; for example, large carriers and towercos procure millions in tower equipment annually, pushing unit price pressure of 5–12% on suppliers.

They can evaluate global vendors, forcing Valmont to compete on price, lead times, and engineering support, where delivery windows under 12 weeks and custom design capability matter most.

Buyer concentration into a few large entities—top 10 tower companies and carriers represent the majority of new-site demand—lets them extract favorable payment terms and longer warranty/maintenance concessions.

Switching Costs and Brand Loyalty

High switching costs in irrigation lower customer bargaining power: Valley users face costs from integrated Valley software, dealer networks, and parts compatibility, so many stay with Valmont after investing in systems.

Still, if Valmont’s value premium shrinks—e.g., competitors closing a perceived gap—farmers can threaten switching to extract discounts; Valmont’s 2024 global irrigation revenue of $1.15B and dealer coverage are key retention assets.

- High switching costs: integrated software, parts

- Brand loyalty: strong local dealer support

- Risk: value-gap erosion enables negotiation

- Key defense: maintain dealer network, parts availability

Availability of Third-Party Financing

Customers’ ability to buy Valmont Industries’ high-cost equipment hinges on third-party credit availability and rates; in 2024 US prime at 8.5% pushed many municipal and contractor buyers to delay purchases or demand better in-house financing.

Valmont partners with banks and captive lenders to offer competitive loans, but when benchmark rates rise, buyers gain leverage to negotiate price, longer terms, or to walk away—recorded bid postponements rose ~12% in 2023–24.

- High rates (prime 8.5% in 2024) ↑ buyer leverage

- Valmont uses partner financing to reduce friction

- Buyers more likely to delay purchases or demand terms

- Reported bid postponements +12% in 2023–24

Buyers' leverage rises as carriers, state bids and high rates reshape pricing power

Buyers wield moderate-to-high power: 28% of 2024 revenue from state/DOT bids (~$630M) and US wireless carriers holding ~70% subscriptions press pricing; farm capex cyclicality and 2024 prime at 8.5% raised negotiation leverage (bid postponements +12% in 2023–24), while high switching costs, dealer network and $1.15B 2024 irrigation revenue counterbalance power.

| Metric | Value |

|---|---|

| State/DOT share | 28% (~$630M, 2024) |

| Irrigation revenue | $1.15B (2024) |

| US carrier market | ~70% (top carriers, CTIA 2024) |

| Prime rate | 8.5% (2024) |

| Bid postponements | +12% (2023–24) |

Preview the Actual Deliverable

Valmont Industries Porter's Five Forces Analysis

This preview shows the exact Valmont Industries Porter's Five Forces analysis you'll receive immediately after purchase—no samples, no placeholders, fully formatted and ready for use.

It contains a concise assessment of supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, with actionable insights for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Valmont Industries faces moderate supplier leverage, intense rivalry among infrastructure-focused peers, and growing substitution pressure from advanced materials and IoT-enabled alternatives, while buyer concentration and regulatory hurdles shape strategic choices; this snapshot highlights key pressures but only scratches the surface.

Suppliers Bargaining Power

Raw Material Price Volatility

The production of Valmont Industries' infrastructure and irrigation systems depends on steel, zinc, and aluminum, exposing margins to global commodity swings; LTM 2025 metal price moves: steel +18% y/y, zinc +22% y/y, aluminum +12% y/y.

Suppliers gain leverage when demand spikes or trade curbs occur—2024–25 export curbs from major producers raised input tightness and premium spreads.

Valmont offsets risk via multi-year supply contracts and price-surcharge clauses, but input cost remains a primary margin driver; raw materials accounted for ~28% of COGS in FY2024.

Geopolitical stability through late 2025—notably tensions in major metal-exporting regions—keeps supplier bargaining power elevated and volatility high.

Specialized Electronic Component Availability

As Valmont adds semiconductors and sensors to Valley irrigation and smart poles, reliance on specialized suppliers rises; global chip shortages in 2021–22 cut industry shipment capacity by ~10–15%, and sensor lead times now often exceed 20 weeks, forcing competition with auto and telecom firms. Technical specs for precision ag limit qualified vendors to a few players, giving suppliers moderate bargaining power and raising risks of delays or 5–12% cost increases on advanced lines.

Energy and Logistics Costs

Valmont’s energy-intensive manufacturing and galvanizing make it hostage to utility and fuel suppliers; US industrial electricity rose ~8% in 2023 and Henry Hub natural gas averaged $2.66/MMBtu in 2024, directly lifting COGS in coatings where heat is central.

Large, bulky poles and irrigation gear make freight a major cost; global ocean freight rates remained ~40% above pre‑pandemic levels in 2024, and carriers pass fuel surcharges and capacity premiums, keeping supplier bargaining power high.

Labor Market Constraints

Valmont relies on highly skilled engineers and specialized trade labor for manufacturing and galvanizing; tight regional labor markets raise worker bargaining power, driving wage and benefit inflation—US specialty construction wages rose 6.2% in 2024 year-over-year, pressuring margins.

To counter this, Valmont invested in training and retention—about $18M in workforce development in 2024—and must sustain those programs, making human capital a recurring supplier-side cost.

- Skilled labor shortage increases wages and benefits

- US specialty wages +6.2% in 2024

- $18M workforce training spend in 2024

- Persistent, recurring cost pressure on margins

Geographic Concentration of Input Sources

- 2024 specialty steel export curbs -> ~12% price rise

- High logistics: inland freight adds 8–15% cost

- Diversification reduces but cannot eliminate regional risk

- Regional supplier power remains critical in procurement

Suppliers Squeeze Valmont: Metals, Freight & Labor Drive Cost Pressure

Suppliers hold elevated bargaining power for Valmont due to concentrated metal sources, elevated freight, specialized chip/sensor vendors, and tight skilled labor—raw materials ~28% of COGS (FY2024), LTM 2025 metal moves: steel +18%, zinc +22%, aluminum +12%; specialty steel export curbs ↑12% (2024); US specialty wages +6.2% (2024); workforce training $18M (2024).

| Item | Metric |

|---|---|

| Raw materials | 28% of COGS (FY2024) |

| Steel | +18% LTM 2025 |

| Zinc | +22% LTM 2025 |

| Aluminum | +12% LTM 2025 |

| Specialty steel curbs | +12% price (2024) |

| Wages | +6.2% US specialty (2024) |

| Workforce spend | $18M (2024) |

What is included in the product

Tailored Porter's Five Forces assessment of Valmont Industries that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and highlights disruptive forces impacting pricing, profitability, and strategic positioning.

A concise Porter's Five Forces snapshot for Valmont Industries—quickly spot supplier, buyer, and competitive pressures to streamline capital allocation and strategic responses.

Customers Bargaining Power

Government and Utility Procurement Influence

A substantial share of Valmont Industries’ 2024 revenue—about 28%, or roughly $630 million—comes from state utilities and DOTs that use formal competitive bids, giving these institutional buyers strong leverage through large contract sizes and tight specs.

Taxpayer-funded projects force pressure for lowest lifecycle cost plus strict safety; losing a single major government contract can cut regional revenue by >15% and lower plant utilization sharply.

Agricultural Commodity Price Sensitivity

The demand for Valmont Industries’ mechanized irrigation tracks closely to farmers’ net income, which fell for US row-crop growers 2024–25 as corn, soy and wheat prices declined ~18% year-over-year, boosting customer bargaining power.

When commodity prices drop, growers defer capex or push for better financing; Valmont responded in 2024 with targeted incentives and tech bundles, keeping margins under pressure.

This cyclicality means the farming cohort can significantly influence Valmont’s sales timing and pricing, concentrating negotiating leverage in down cycles.

Sophisticated Corporate Telecommunications Buyers

Customers in Valmont Industries' wireless segment—major telecom carriers and tower operators—are highly sophisticated and price-sensitive, with top five carriers in the US controlling ~70% of wireless subscriptions (CTIA 2024), boosting their negotiating leverage.

These buyers consolidate purchases to secure volume discounts for 5G support structures; for example, large carriers and towercos procure millions in tower equipment annually, pushing unit price pressure of 5–12% on suppliers.

They can evaluate global vendors, forcing Valmont to compete on price, lead times, and engineering support, where delivery windows under 12 weeks and custom design capability matter most.

Buyer concentration into a few large entities—top 10 tower companies and carriers represent the majority of new-site demand—lets them extract favorable payment terms and longer warranty/maintenance concessions.

Switching Costs and Brand Loyalty

High switching costs in irrigation lower customer bargaining power: Valley users face costs from integrated Valley software, dealer networks, and parts compatibility, so many stay with Valmont after investing in systems.

Still, if Valmont’s value premium shrinks—e.g., competitors closing a perceived gap—farmers can threaten switching to extract discounts; Valmont’s 2024 global irrigation revenue of $1.15B and dealer coverage are key retention assets.

- High switching costs: integrated software, parts

- Brand loyalty: strong local dealer support

- Risk: value-gap erosion enables negotiation

- Key defense: maintain dealer network, parts availability

Availability of Third-Party Financing

Customers’ ability to buy Valmont Industries’ high-cost equipment hinges on third-party credit availability and rates; in 2024 US prime at 8.5% pushed many municipal and contractor buyers to delay purchases or demand better in-house financing.

Valmont partners with banks and captive lenders to offer competitive loans, but when benchmark rates rise, buyers gain leverage to negotiate price, longer terms, or to walk away—recorded bid postponements rose ~12% in 2023–24.

- High rates (prime 8.5% in 2024) ↑ buyer leverage

- Valmont uses partner financing to reduce friction

- Buyers more likely to delay purchases or demand terms

- Reported bid postponements +12% in 2023–24

Buyers' leverage rises as carriers, state bids and high rates reshape pricing power

Buyers wield moderate-to-high power: 28% of 2024 revenue from state/DOT bids (~$630M) and US wireless carriers holding ~70% subscriptions press pricing; farm capex cyclicality and 2024 prime at 8.5% raised negotiation leverage (bid postponements +12% in 2023–24), while high switching costs, dealer network and $1.15B 2024 irrigation revenue counterbalance power.

| Metric | Value |

|---|---|

| State/DOT share | 28% (~$630M, 2024) |

| Irrigation revenue | $1.15B (2024) |

| US carrier market | ~70% (top carriers, CTIA 2024) |

| Prime rate | 8.5% (2024) |

| Bid postponements | +12% (2023–24) |

Preview the Actual Deliverable

Valmont Industries Porter's Five Forces Analysis

This preview shows the exact Valmont Industries Porter's Five Forces analysis you'll receive immediately after purchase—no samples, no placeholders, fully formatted and ready for use.

It contains a concise assessment of supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, with actionable insights for strategic decision-making.