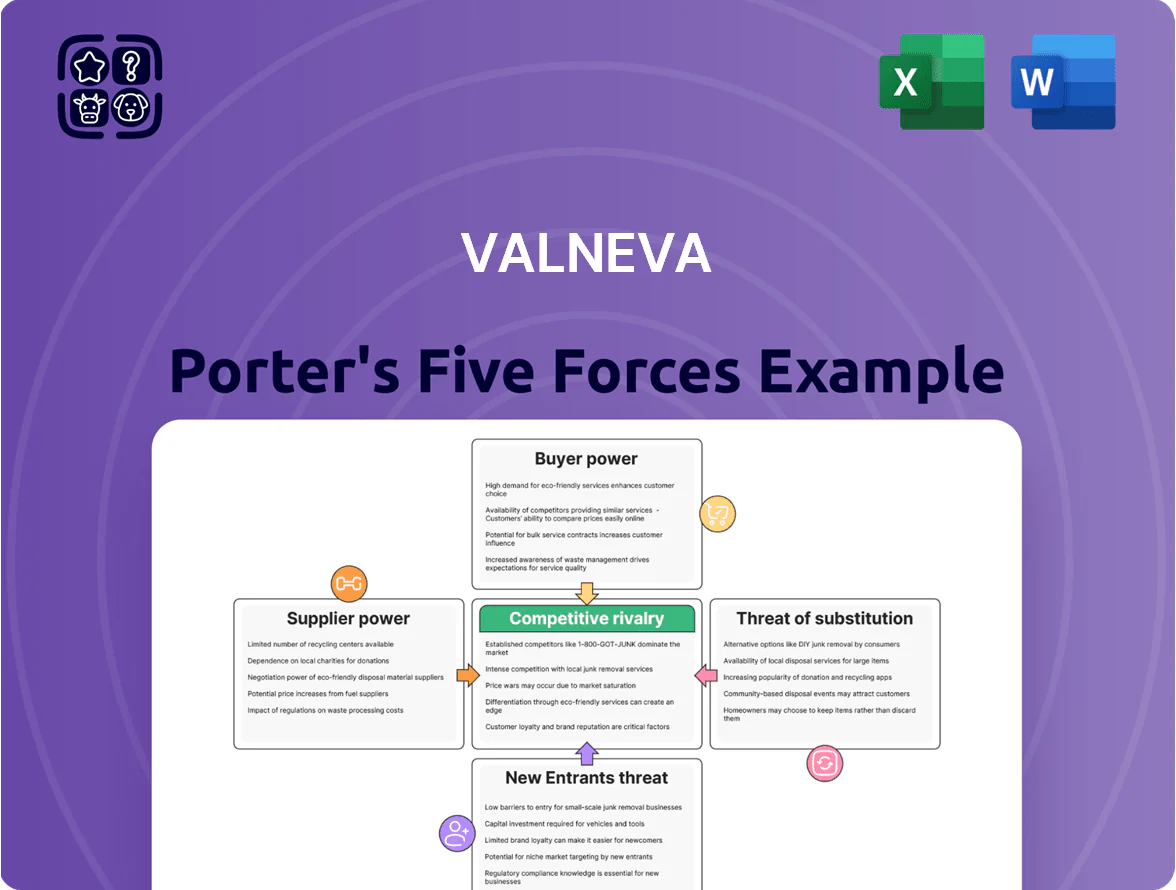

Valneva Porter's Five Forces Analysis

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valneva’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Biological Raw Material Providers

Valneva relies on scarce inputs—proprietary cell lines and specialized adjuvants—sourced from very few global suppliers, so supplier power is high; switching costs are extreme because regulatory approvals lock in specific biological profiles.

Any supply disruption or a 10–20% price hike (seen in biotech supply contracts 2023–2024) would hit Valneva’s margins and delay production timelines, giving suppliers leverage in negotiations.

Contract Development and Manufacturing Organizations

Valneva relies on CDMOs to scale vaccine production, and their specialized biomanufacturing capacity—scarce after COVID-19—gives them moderate-to-high bargaining power; in 2023 global biomanufacturing utilization hit ~85%, tightening access.

Intellectual Property and Technology Licensors

Many Valneva vaccine platforms rely on licensed tech and patented sequences from universities and biotechs; maintaining these agreements is essential to advance candidates like VLA2001 (inactivated COVID-19) and chikungunya programs.

IP owners can set royalties and terms that squeeze margins; industry median vaccine royalty rates were 5–10% in 2024, which could cut long-term product EBITDA materially for Valneva.

Cold Chain Logistics and Distribution Partners

Specialized cold-chain logistics are critical for Valneva vaccines (e.g., Japanese encephalitis, chikungunya) that need continuous temperature control; global providers with capacity into endemic regions are few, raising supplier bargaining power.

These providers can push higher prices and strict SLAs because cold-chain failure causes total product loss, FDA/EMA scrutiny, and revenue hits—vaccine cold-chain failures can cost millions per batch; in 2023 cold-chain incidents caused >$120m industry losses.

- Limited global cold-chain providers → higher pricing power

- Any failure = total product loss + regulatory risk

- 2023 industry cold-chain incidents >$120m losses

Regulatory and Clinical Trial Service Providers

The specialized nature of vaccine trials forces Valneva to partner with Contract Research Organizations (CROs) experienced in infectious disease and immunology; in 2024 about 60–70% of late‑stage vaccine R&D used specialist CROs, concentrating expertise.

Those CROs manage multi‑country patient recruitment and complex data, making them critical to Valneva’s R&D success and timeline integrity.

Switching mid‑trial risks months of delay and millions in extra cost—average phase III vaccine trial delays cost $20–80M and can imperil FDA/EMA approval schedules.

- High dependence on specialist CROs (60–70% market share in late‑stage vaccine projects)

- Complex multi‑geography operations raise switching costs

- Mid‑trial switches can add $20–80M and months of delay

- Supplier power elevated due to regulatory approval risks

High supplier power risks: scarce inputs, 85% CDMO use, costly cold‑chain losses

Suppliers have high power: scarce cell lines, adjuvants, CDMO capacity (~85% utilization in 2023), specialist CROs (60–70% share in late‑stage 2024), cold‑chain incidents >$120m (2023) and typical royalties 5–10% (2024) raise costs and switching risks; a 10–20% input price shock could materially cut margins and delay launches.

| Metric | Value |

|---|---|

| CDMO utilization (2023) | ~85% |

| CRO share (late‑stage 2024) | 60–70% |

| Cold‑chain losses (2023) | >$120m |

| Royalty rate (2024) | 5–10% |

What is included in the product

Tailored Porter's Five Forces analysis for Valneva that uncovers competitive drivers, supplier and buyer power, barriers to entry, threat of substitutes, and industry rivalry—highlighting disruptive risks, strategic defenses, and implications for pricing and profitability.

Concise Porter's Five Forces for Valneva—single-sheet clarity to speed strategic decisions and investor briefings.

Customers Bargaining Power

National Health Authorities and Government Tenders

National health authorities drive much of Valneva’s vaccine revenue—governments bought roughly 60–75% of global routine vaccines in 2023, and Valneva’s 2024 annual report showed >50% of revenues tied to public-sector contracts, so sovereign buyers hold huge bargaining power.

Through tenders and pooled purchasing (e.g., Gavi, EU joint procurements), buyers extract steep discounts; public tenders cut prices by 20–60% versus private sales in many markets in 2022–24.

Because Valneva depends on a few large contracts for high-volume products, losing one major tender can swing annual revenue by double digits—examples: a single EU/UK pediatric contract often represents 10–25% of yearly sales.

International Health Organizations and NGOs

Private Travel Clinics and Specialized Healthcare Providers

In travel medicine, private clinics and healthcare pros—estimated 20,000 outpatient travel clinics in OECD countries in 2024—recommend vaccines and thus shape brand choice, giving them notable bargaining power despite fragmentation.

These buyers influence uptake via patient counseling and formulary decisions, so Valneva must spend on physician outreach; Valneva reported R&D and SG&A of €174m in 2024, showing available but stretched marketing resources.

Clinics favor proven efficacy and safety; Valneva’s 2023/24 vaccine efficacy data and WHO prequalification help, but competitors with lower prices can sway clinics, forcing continued promotion and education.

Military Organizations and Defense Departments

Defense departments buy vaccines for deployed personnel in disease zones and demand high reliability, cold-chain logistics, and validated efficacy; contracts often run 3–10 years and can exceed $10–50m per program based on recent military procurement profiles.

Their bargaining power is high because purchases are strategic, fund sizes are large, they can set procurement specs, and they influence NATO and WHO standards for military-grade medical supplies.

- Long-term contracts: 3–10 years

- Program size: $10–50m typical

- Require cold-chain & validated efficacy

- Influence international standards (NATO/WHO)

Individual Consumers and High-Risk Populations

Individual travelers and residents in endemic regions are the end-users driving demand for Valneva’s vaccines; individual bargaining power is low, but tribe-like shifts in consumer sentiment on safety/efficacy can rapidly cut uptake.

Valneva must protect brand trust—private-pay channels accounted for ~30% of vaccine revenues in comparable markets in 2024—so drops in confidence could dent sales quickly.

- End-users low power; collective sentiment high impact

- Private-channel share ~30% (2024 proxy)

- Brand reputation directly tied to uptake

Public buyers wield pricing power: >50% revenue, tenders cut 20–60% (EU/UK =10–25%)

Buyers (national health authorities, Gavi, defense, travel clinics) hold strong bargaining power: public-sector >50% of Valneva 2024 revenue, Gavi $2.7bn vaccine funding (2024), tenders cut prices 20–60%, single EU/UK contract = 10–25% annual sales, private channels ~30% (2024 proxy).

| Buyer | Key stat |

|---|---|

| Public sector | >50% rev (2024) |

| Gavi | $2.7bn (2024) |

| Tender discounts | 20–60% |

| EU/UK contract | 10–25% rev |

What You See Is What You Get

Valneva Porter's Five Forces Analysis

This preview shows the exact Valneva Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it includes supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with sector-specific insights.

The document displayed here is the same professionally formatted file you'll be able to download and use instantly—ready for decision-making, valuation inputs, and strategic planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valneva’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Biological Raw Material Providers

Valneva relies on scarce inputs—proprietary cell lines and specialized adjuvants—sourced from very few global suppliers, so supplier power is high; switching costs are extreme because regulatory approvals lock in specific biological profiles.

Any supply disruption or a 10–20% price hike (seen in biotech supply contracts 2023–2024) would hit Valneva’s margins and delay production timelines, giving suppliers leverage in negotiations.

Contract Development and Manufacturing Organizations

Valneva relies on CDMOs to scale vaccine production, and their specialized biomanufacturing capacity—scarce after COVID-19—gives them moderate-to-high bargaining power; in 2023 global biomanufacturing utilization hit ~85%, tightening access.

Intellectual Property and Technology Licensors

Many Valneva vaccine platforms rely on licensed tech and patented sequences from universities and biotechs; maintaining these agreements is essential to advance candidates like VLA2001 (inactivated COVID-19) and chikungunya programs.

IP owners can set royalties and terms that squeeze margins; industry median vaccine royalty rates were 5–10% in 2024, which could cut long-term product EBITDA materially for Valneva.

Cold Chain Logistics and Distribution Partners

Specialized cold-chain logistics are critical for Valneva vaccines (e.g., Japanese encephalitis, chikungunya) that need continuous temperature control; global providers with capacity into endemic regions are few, raising supplier bargaining power.

These providers can push higher prices and strict SLAs because cold-chain failure causes total product loss, FDA/EMA scrutiny, and revenue hits—vaccine cold-chain failures can cost millions per batch; in 2023 cold-chain incidents caused >$120m industry losses.

- Limited global cold-chain providers → higher pricing power

- Any failure = total product loss + regulatory risk

- 2023 industry cold-chain incidents >$120m losses

Regulatory and Clinical Trial Service Providers

The specialized nature of vaccine trials forces Valneva to partner with Contract Research Organizations (CROs) experienced in infectious disease and immunology; in 2024 about 60–70% of late‑stage vaccine R&D used specialist CROs, concentrating expertise.

Those CROs manage multi‑country patient recruitment and complex data, making them critical to Valneva’s R&D success and timeline integrity.

Switching mid‑trial risks months of delay and millions in extra cost—average phase III vaccine trial delays cost $20–80M and can imperil FDA/EMA approval schedules.

- High dependence on specialist CROs (60–70% market share in late‑stage vaccine projects)

- Complex multi‑geography operations raise switching costs

- Mid‑trial switches can add $20–80M and months of delay

- Supplier power elevated due to regulatory approval risks

High supplier power risks: scarce inputs, 85% CDMO use, costly cold‑chain losses

Suppliers have high power: scarce cell lines, adjuvants, CDMO capacity (~85% utilization in 2023), specialist CROs (60–70% share in late‑stage 2024), cold‑chain incidents >$120m (2023) and typical royalties 5–10% (2024) raise costs and switching risks; a 10–20% input price shock could materially cut margins and delay launches.

| Metric | Value |

|---|---|

| CDMO utilization (2023) | ~85% |

| CRO share (late‑stage 2024) | 60–70% |

| Cold‑chain losses (2023) | >$120m |

| Royalty rate (2024) | 5–10% |

What is included in the product

Tailored Porter's Five Forces analysis for Valneva that uncovers competitive drivers, supplier and buyer power, barriers to entry, threat of substitutes, and industry rivalry—highlighting disruptive risks, strategic defenses, and implications for pricing and profitability.

Concise Porter's Five Forces for Valneva—single-sheet clarity to speed strategic decisions and investor briefings.

Customers Bargaining Power

National Health Authorities and Government Tenders

National health authorities drive much of Valneva’s vaccine revenue—governments bought roughly 60–75% of global routine vaccines in 2023, and Valneva’s 2024 annual report showed >50% of revenues tied to public-sector contracts, so sovereign buyers hold huge bargaining power.

Through tenders and pooled purchasing (e.g., Gavi, EU joint procurements), buyers extract steep discounts; public tenders cut prices by 20–60% versus private sales in many markets in 2022–24.

Because Valneva depends on a few large contracts for high-volume products, losing one major tender can swing annual revenue by double digits—examples: a single EU/UK pediatric contract often represents 10–25% of yearly sales.

International Health Organizations and NGOs

Private Travel Clinics and Specialized Healthcare Providers

In travel medicine, private clinics and healthcare pros—estimated 20,000 outpatient travel clinics in OECD countries in 2024—recommend vaccines and thus shape brand choice, giving them notable bargaining power despite fragmentation.

These buyers influence uptake via patient counseling and formulary decisions, so Valneva must spend on physician outreach; Valneva reported R&D and SG&A of €174m in 2024, showing available but stretched marketing resources.

Clinics favor proven efficacy and safety; Valneva’s 2023/24 vaccine efficacy data and WHO prequalification help, but competitors with lower prices can sway clinics, forcing continued promotion and education.

Military Organizations and Defense Departments

Defense departments buy vaccines for deployed personnel in disease zones and demand high reliability, cold-chain logistics, and validated efficacy; contracts often run 3–10 years and can exceed $10–50m per program based on recent military procurement profiles.

Their bargaining power is high because purchases are strategic, fund sizes are large, they can set procurement specs, and they influence NATO and WHO standards for military-grade medical supplies.

- Long-term contracts: 3–10 years

- Program size: $10–50m typical

- Require cold-chain & validated efficacy

- Influence international standards (NATO/WHO)

Individual Consumers and High-Risk Populations

Individual travelers and residents in endemic regions are the end-users driving demand for Valneva’s vaccines; individual bargaining power is low, but tribe-like shifts in consumer sentiment on safety/efficacy can rapidly cut uptake.

Valneva must protect brand trust—private-pay channels accounted for ~30% of vaccine revenues in comparable markets in 2024—so drops in confidence could dent sales quickly.

- End-users low power; collective sentiment high impact

- Private-channel share ~30% (2024 proxy)

- Brand reputation directly tied to uptake

Public buyers wield pricing power: >50% revenue, tenders cut 20–60% (EU/UK =10–25%)

Buyers (national health authorities, Gavi, defense, travel clinics) hold strong bargaining power: public-sector >50% of Valneva 2024 revenue, Gavi $2.7bn vaccine funding (2024), tenders cut prices 20–60%, single EU/UK contract = 10–25% annual sales, private channels ~30% (2024 proxy).

| Buyer | Key stat |

|---|---|

| Public sector | >50% rev (2024) |

| Gavi | $2.7bn (2024) |

| Tender discounts | 20–60% |

| EU/UK contract | 10–25% rev |

What You See Is What You Get

Valneva Porter's Five Forces Analysis

This preview shows the exact Valneva Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it includes supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with sector-specific insights.

The document displayed here is the same professionally formatted file you'll be able to download and use instantly—ready for decision-making, valuation inputs, and strategic planning.