Valve Corporation PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, regulatory pressure, and rapid tech innovation are reshaping Valve Corporation’s competitive landscape—our PESTLE snapshot reveals risks and openings you can act on today.

Investors, strategists, and developers: buy the full PESTLE analysis for a complete, editable breakdown that turns external trends into practical strategy and competitive advantage.

Political factors

US-China Trade Relations

The US-China trade tensions affect Valve’s hardware strategy: tariffs or export controls could raise Steam Deck unit costs, given ~70-80% of components are sourced/assembled in Asia, potentially squeezing margins on a device retailing at $399–$649. New tariffs in 2024–25 added up to 10–25% on select electronics, risking supply delays and cost pass-through. Valve also relies on Perfect World to comply with China’s strict game regulations to access ~650m+ gamers, exposing revenue to regulatory shifts.

EU Digital Markets Act Compliance

The EU Digital Markets Act, effective 2023 with enforcement ramping in 2024–25, targets gatekeepers and could subject Valve to fines up to 10% of global turnover (or 20% for repeated breaches); Steam must adopt interoperability and fair competition measures to avoid such penalties.

Regulators push for reduced gatekeeping, potentially forcing Valve to permit third-party payment systems or alternative storefronts on Steam, which could impact its 2023 estimated platform revenues (approximately $4–5 billion).

Noncompliance risks structural changes to store architecture and significant compliance costs as the DMA’s oversight expands across the EU market.

Global Content Censorship and Compliance

Political shifts toward nationalism and stricter social controls force Valve to deploy localized content filters; in 2024 Steam generated an estimated $7.5B in revenue, so removal requests from Germany, Australia, and Brazil—where regulators mandated content edits in multiple cases—pose material risk. Noncompliance can trigger fines or outright bans: Brazil blocked services in past tech disputes and Germany’s Jugendmedienschutz can restrict distribution, threatening access to sizable markets.

Digital Services Taxation

Governments are enacting digital services taxes to capture revenue from multinationals; by 2025 over 40 countries had DSTs or equivalent measures, pressuring firms like Valve.

Valve must navigate VAT and sales tax across 190+ countries and US states, with tax compliance costs that industry estimates place in the tens of millions annually.

These tax policies influence end-user prices and require significant administrative overhead for pricing, reporting, and remittance.

- 40+ countries with DSTs or equivalents by 2025

- Tax coverage: 190+ countries and US states

- Compliance costs: estimated tens of millions annually

- Direct impact on consumer prices and pricing complexity

Government Scrutiny of Virtual Economies

Political scrutiny linking gaming and gambling has intensified, with regulators in the US, UK, South Korea and Netherlands investigating Valve's virtual-item markets; US state-level bills in 2024 proposed loot box restrictions and South Korea fined operators for unregulated item trading.

Legislators seek to classify skin trading and certain loot boxes as gambling, risking revenue from Counter-Strike item economy which Valve-adjacent market estimates valued at several hundred million dollars annually (secondary market activity often cited $500M+ in peak years).

Ongoing litigation and proposed laws force Valve into continuous legal, compliance and diplomatic engagement across jurisdictions, increasing compliance costs and regulatory uncertainty for its Steam platform.

- Increased regulatory actions across US, EU, South Korea

- Legislative risk to skin trading/loot boxes as gambling

- Counter-Strike item economy historically linked to $100sM market activity

- Rising compliance/legal costs and operational uncertainty

Rising tariffs, global taxes & regulatory fines threaten gaming hardware margins

Political risks: tariffs/US-China controls raise Steam Deck costs (70–80% Asia sourcing; 2024–25 tariffs +10–25%), EU DMA fines up to 10–20% global turnover, 40+ countries with DSTs by 2025, tax/VAT across 190+ jurisdictions (compliance tens of millions/year), loot-box/skin gambling risk tied to ~$500M+ secondary market activity; regulatory actions in US/EU/KR raise legal/compliance costs.

| Metric | Value |

|---|---|

| Asia sourcing | 70–80% |

| Tariff impact (2024–25) | +10–25% |

| DSTs by 2025 | 40+ |

| Tax jurisdictions | 190+ |

| Secondary market | $500M+ |

What is included in the product

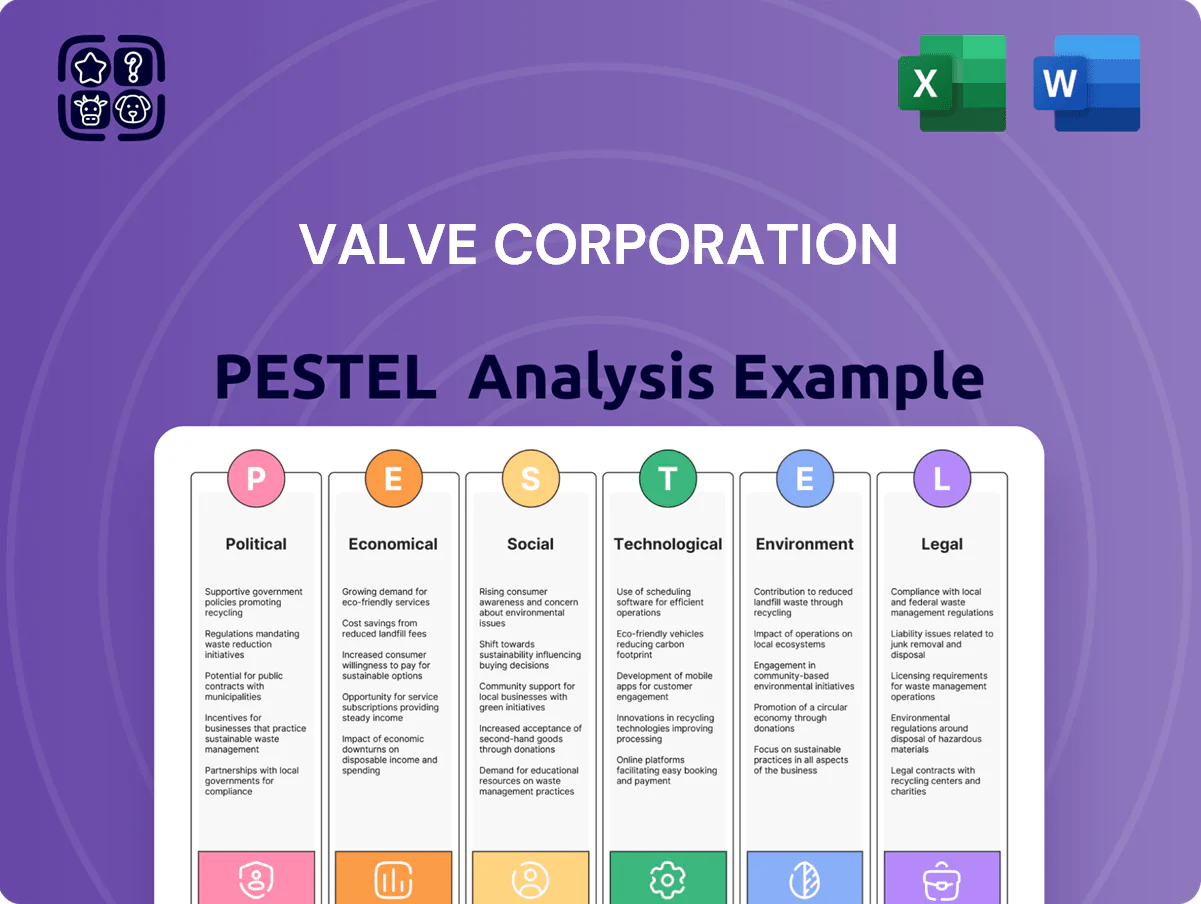

Explores how external macro-environmental factors uniquely affect Valve Corporation across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Condenses Valve Corporation's PESTLE into a concise, shareable brief that highlights external risks and opportunities for strategy meetings or slides, written in clear language and easily annotated for regional or business-specific notes.

Economic factors

Global Exchange Rate Volatility

Valve’s Steam platform transacts in 70+ currencies, exposing revenues to FX shocks; 2023 saw USD strength push emerging-market prices down ~8–12% versus 2021 levels, squeezing reported margins when converted to USD.

Valve adjusts regional pricing frequently—over 40 local price updates in 2023—but such hikes triggered consumer backlash in markets with >5% inflation, reducing conversion rates and local sales velocity.

Impact of Global Inflation on Discretionary Spending

Global inflation, which averaged 6.8% in advanced economies and 9.2% in emerging markets in 2024, squeezes disposable income and can reduce consumer spend on non-essentials like games and premium hardware.

Although gaming remained cost-effective—global game spending rose 3% to $189B in 2024—a prolonged downturn could slow Steam Deck and VR headset adoption.

Valve must calibrate pricing, bundles, and financing to preserve value perception as real wages lag and consumer purchasing power declines.

Competition from Subscription-Based Models

The rise of subscription services like Xbox Game Pass, which reported over 25 million subscribers in 2024, poses an economic threat to Valve’s buy-to-play Steam model as more gamers favor monthly access over individual purchases, potentially lowering Steam’s transactional volume (Steam generated estimated $9–10B gross revenue in 2023). Valve must enhance platform features, curation and community tools to retain spend and justify its transactional marketplace.

Handheld Gaming Market Expansion

The Steam Deck's success created a handheld gaming niche Valve dominated through late 2025, driving a 28% year-over-year increase in handheld-related game purchases and contributing an estimated $650 million in incremental software revenue in 2024–25, as portability boosted user spending within Steam.

Expanding handheld sales — over 2.1 million units shipped by end-2025 — diversified Valve's revenue, partially offsetting flat desktop PC market revenues and improving overall gross margin resilience.

- 28% YoY increase in handheld-related game purchases (2024–25)

- $650M incremental software revenue (2024–25)

- ~2.1M Steam Deck units shipped by end-2025

- Diversified revenue offsets desktop PC stagnation

Platform Revenue Share Pressures

The standard 30% Steam cut faces sustained pushback from developers and competitors like Epic Games, which offers 12%–15% fees and has paid over $1.5B in exclusivity deals through 2024 to attract titles.

Rising AAA development costs—often $100M+—drive publishers to seek higher margins and sometimes launch proprietary clients (Ubisoft Connect, EA App), threatening Steam’s share.

Valve’s retention of the fee relies on Steam’s 120M+ monthly active users (2024) and integrated social discovery tools that justify the economic trade-off for many developers.

- 30% industry standard vs Epic 12%–15%

- Epic paid ~$1.5B+ in exclusivity (through 2024)

- AAA dev costs commonly exceed $100M

- Steam ~120M monthly active users (2024)

Valve under FX/inflation strain—Steam & Deck cushion growth as Epic pressures fees

Valve faces FX and inflation pressure—USD strength and 2024–25 inflation cut regional revenue; Steam ~120M MAU and $9–10B gross (2023) cushion margins. Handhelds (2.1M Decks by end-2025) added ~$650M software revenue and 28% handheld-related purchase growth. Competition: Epic’s 12–15% fees and $1.5B exclusivity spend threaten Steam’s 30% cut; AAA costs >$100M push publishers to alternate clients.

| Metric | Value |

|---|---|

| Steam MAU (2024) | ~120M |

| Steam gross (2023) | $9–10B |

| Steam Deck units (end-2025) | ~2.1M |

| Handheld incremental rev (2024–25) | $650M |

| Epic exclusivity spend (through 2024) | $1.5B+ |

What You See Is What You Get

Valve Corporation PESTLE Analysis

The preview shown here is the exact Valve Corporation PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

No placeholders or teasers: the content, layout, and insights visible in this preview are the final file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, regulatory pressure, and rapid tech innovation are reshaping Valve Corporation’s competitive landscape—our PESTLE snapshot reveals risks and openings you can act on today.

Investors, strategists, and developers: buy the full PESTLE analysis for a complete, editable breakdown that turns external trends into practical strategy and competitive advantage.

Political factors

US-China Trade Relations

The US-China trade tensions affect Valve’s hardware strategy: tariffs or export controls could raise Steam Deck unit costs, given ~70-80% of components are sourced/assembled in Asia, potentially squeezing margins on a device retailing at $399–$649. New tariffs in 2024–25 added up to 10–25% on select electronics, risking supply delays and cost pass-through. Valve also relies on Perfect World to comply with China’s strict game regulations to access ~650m+ gamers, exposing revenue to regulatory shifts.

EU Digital Markets Act Compliance

The EU Digital Markets Act, effective 2023 with enforcement ramping in 2024–25, targets gatekeepers and could subject Valve to fines up to 10% of global turnover (or 20% for repeated breaches); Steam must adopt interoperability and fair competition measures to avoid such penalties.

Regulators push for reduced gatekeeping, potentially forcing Valve to permit third-party payment systems or alternative storefronts on Steam, which could impact its 2023 estimated platform revenues (approximately $4–5 billion).

Noncompliance risks structural changes to store architecture and significant compliance costs as the DMA’s oversight expands across the EU market.

Global Content Censorship and Compliance

Political shifts toward nationalism and stricter social controls force Valve to deploy localized content filters; in 2024 Steam generated an estimated $7.5B in revenue, so removal requests from Germany, Australia, and Brazil—where regulators mandated content edits in multiple cases—pose material risk. Noncompliance can trigger fines or outright bans: Brazil blocked services in past tech disputes and Germany’s Jugendmedienschutz can restrict distribution, threatening access to sizable markets.

Digital Services Taxation

Governments are enacting digital services taxes to capture revenue from multinationals; by 2025 over 40 countries had DSTs or equivalent measures, pressuring firms like Valve.

Valve must navigate VAT and sales tax across 190+ countries and US states, with tax compliance costs that industry estimates place in the tens of millions annually.

These tax policies influence end-user prices and require significant administrative overhead for pricing, reporting, and remittance.

- 40+ countries with DSTs or equivalents by 2025

- Tax coverage: 190+ countries and US states

- Compliance costs: estimated tens of millions annually

- Direct impact on consumer prices and pricing complexity

Government Scrutiny of Virtual Economies

Political scrutiny linking gaming and gambling has intensified, with regulators in the US, UK, South Korea and Netherlands investigating Valve's virtual-item markets; US state-level bills in 2024 proposed loot box restrictions and South Korea fined operators for unregulated item trading.

Legislators seek to classify skin trading and certain loot boxes as gambling, risking revenue from Counter-Strike item economy which Valve-adjacent market estimates valued at several hundred million dollars annually (secondary market activity often cited $500M+ in peak years).

Ongoing litigation and proposed laws force Valve into continuous legal, compliance and diplomatic engagement across jurisdictions, increasing compliance costs and regulatory uncertainty for its Steam platform.

- Increased regulatory actions across US, EU, South Korea

- Legislative risk to skin trading/loot boxes as gambling

- Counter-Strike item economy historically linked to $100sM market activity

- Rising compliance/legal costs and operational uncertainty

Rising tariffs, global taxes & regulatory fines threaten gaming hardware margins

Political risks: tariffs/US-China controls raise Steam Deck costs (70–80% Asia sourcing; 2024–25 tariffs +10–25%), EU DMA fines up to 10–20% global turnover, 40+ countries with DSTs by 2025, tax/VAT across 190+ jurisdictions (compliance tens of millions/year), loot-box/skin gambling risk tied to ~$500M+ secondary market activity; regulatory actions in US/EU/KR raise legal/compliance costs.

| Metric | Value |

|---|---|

| Asia sourcing | 70–80% |

| Tariff impact (2024–25) | +10–25% |

| DSTs by 2025 | 40+ |

| Tax jurisdictions | 190+ |

| Secondary market | $500M+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Valve Corporation across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities for executives, investors, and strategists.

Condenses Valve Corporation's PESTLE into a concise, shareable brief that highlights external risks and opportunities for strategy meetings or slides, written in clear language and easily annotated for regional or business-specific notes.

Economic factors

Global Exchange Rate Volatility

Valve’s Steam platform transacts in 70+ currencies, exposing revenues to FX shocks; 2023 saw USD strength push emerging-market prices down ~8–12% versus 2021 levels, squeezing reported margins when converted to USD.

Valve adjusts regional pricing frequently—over 40 local price updates in 2023—but such hikes triggered consumer backlash in markets with >5% inflation, reducing conversion rates and local sales velocity.

Impact of Global Inflation on Discretionary Spending

Global inflation, which averaged 6.8% in advanced economies and 9.2% in emerging markets in 2024, squeezes disposable income and can reduce consumer spend on non-essentials like games and premium hardware.

Although gaming remained cost-effective—global game spending rose 3% to $189B in 2024—a prolonged downturn could slow Steam Deck and VR headset adoption.

Valve must calibrate pricing, bundles, and financing to preserve value perception as real wages lag and consumer purchasing power declines.

Competition from Subscription-Based Models

The rise of subscription services like Xbox Game Pass, which reported over 25 million subscribers in 2024, poses an economic threat to Valve’s buy-to-play Steam model as more gamers favor monthly access over individual purchases, potentially lowering Steam’s transactional volume (Steam generated estimated $9–10B gross revenue in 2023). Valve must enhance platform features, curation and community tools to retain spend and justify its transactional marketplace.

Handheld Gaming Market Expansion

The Steam Deck's success created a handheld gaming niche Valve dominated through late 2025, driving a 28% year-over-year increase in handheld-related game purchases and contributing an estimated $650 million in incremental software revenue in 2024–25, as portability boosted user spending within Steam.

Expanding handheld sales — over 2.1 million units shipped by end-2025 — diversified Valve's revenue, partially offsetting flat desktop PC market revenues and improving overall gross margin resilience.

- 28% YoY increase in handheld-related game purchases (2024–25)

- $650M incremental software revenue (2024–25)

- ~2.1M Steam Deck units shipped by end-2025

- Diversified revenue offsets desktop PC stagnation

Platform Revenue Share Pressures

The standard 30% Steam cut faces sustained pushback from developers and competitors like Epic Games, which offers 12%–15% fees and has paid over $1.5B in exclusivity deals through 2024 to attract titles.

Rising AAA development costs—often $100M+—drive publishers to seek higher margins and sometimes launch proprietary clients (Ubisoft Connect, EA App), threatening Steam’s share.

Valve’s retention of the fee relies on Steam’s 120M+ monthly active users (2024) and integrated social discovery tools that justify the economic trade-off for many developers.

- 30% industry standard vs Epic 12%–15%

- Epic paid ~$1.5B+ in exclusivity (through 2024)

- AAA dev costs commonly exceed $100M

- Steam ~120M monthly active users (2024)

Valve under FX/inflation strain—Steam & Deck cushion growth as Epic pressures fees

Valve faces FX and inflation pressure—USD strength and 2024–25 inflation cut regional revenue; Steam ~120M MAU and $9–10B gross (2023) cushion margins. Handhelds (2.1M Decks by end-2025) added ~$650M software revenue and 28% handheld-related purchase growth. Competition: Epic’s 12–15% fees and $1.5B exclusivity spend threaten Steam’s 30% cut; AAA costs >$100M push publishers to alternate clients.

| Metric | Value |

|---|---|

| Steam MAU (2024) | ~120M |

| Steam gross (2023) | $9–10B |

| Steam Deck units (end-2025) | ~2.1M |

| Handheld incremental rev (2024–25) | $650M |

| Epic exclusivity spend (through 2024) | $1.5B+ |

What You See Is What You Get

Valve Corporation PESTLE Analysis

The preview shown here is the exact Valve Corporation PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

No placeholders or teasers: the content, layout, and insights visible in this preview are the final file you’ll download immediately after payment.