Valvoline Boston Consulting Group Matrix

Download Your Competitive Advantage

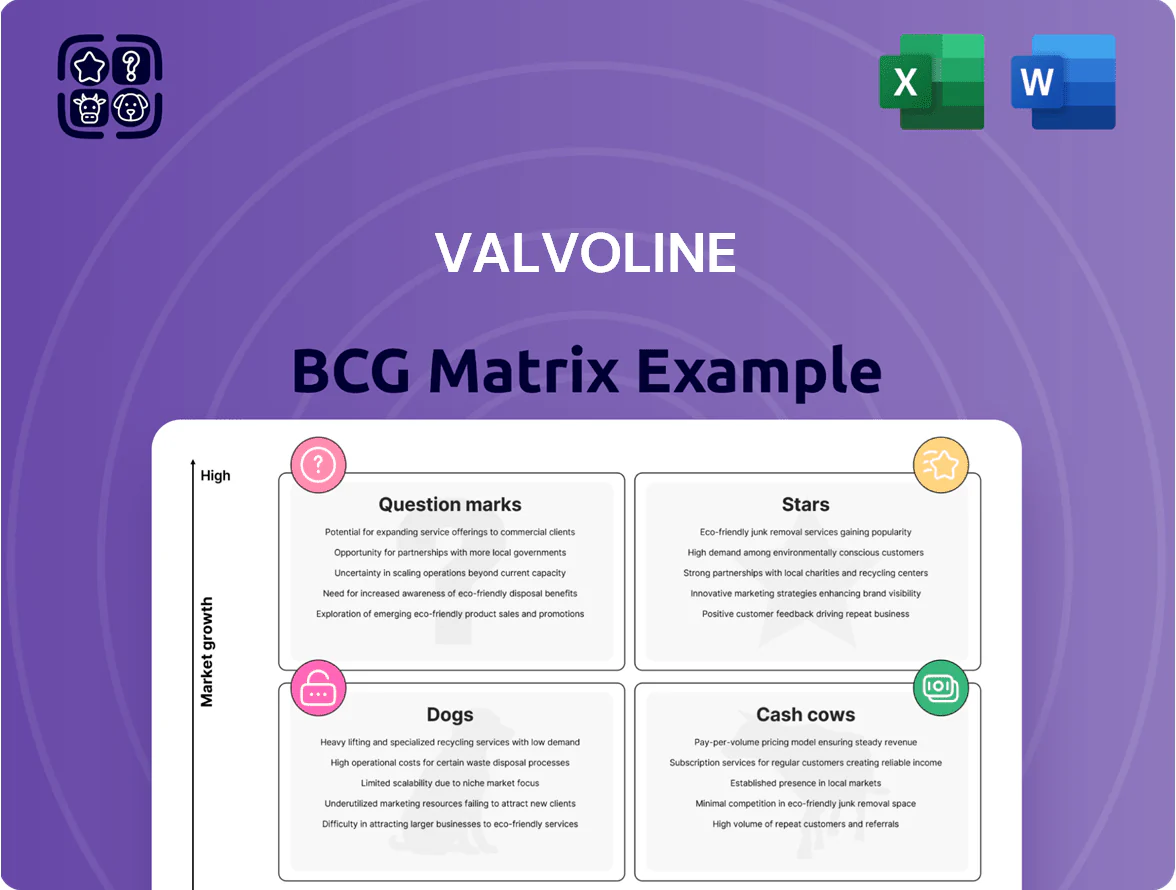

Valvoline’s BCG Matrix snapshot highlights product lines across growth and market-share spectrums, showing where engines of profit and areas of risk live; it’s a strategic lens for prioritizing investment and divestment decisions. This preview teases quadrant placement and high-level implications, but the full BCG Matrix provides precise quadrant mapping, data-backed recommendations, and tactical moves tailored to Valvoline’s market dynamics. Purchase the complete report for a Word analysis + Excel summary to present and act on immediately.

Stars

Quick-Lube Service Expansion

Valvoline is rapidly scaling company and franchised quick-lube sites, adding about 250 net new locations in 2024 to reach ~1,900 stores, targeting the $35B US outsourced maintenance market where pro service share rose to 62% in 2024.

These openings are treated as Stars in a BCG matrix: high market growth (~4–5% CAGR) and rising share, supported by ~ $220M capex in 2024 to outfit sites and drive same-store sales gains.

Electric Vehicle (EV) Specialized Services

As EV adoption hits 14% of US light-vehicle sales in 2024 (EPA/EDR), Valvoline’s EV-focused maintenance protocols sit in the Stars quadrant as a high-growth service line targeting cooling and dielectric fluid needs.

These services command a 15–25% premium versus ICE oil changes, with early pilots showing 30% higher per-visit revenue and 12% gross-margin lift in 2024 pilot centers.

By standardizing EV fluid care and launching 400+ dedicated bays in 2025, Valvoline aims to secure dominant market share as first-mover while EV parc grows toward an expected 40% by 2030 (IEA).

Fleet Management Solutions

Fleet Management Solutions sits in Valvoline’s BCG matrix as a star: delivery and ride-share growth drove US commercial vehicle miles +6.2% in 2024, lifting demand for fleet maintenance. Valvoline offers nationwide high share via centralized billing and standardized care across ~1,400 locations, generating estimated fleet revenue of ~$300M in FY2024. Keeping star status needs ongoing tech and sales spend—Valvoline increased fleet CAPEX +18% in 2024 to scale telematics and sales teams.

Predictive Maintenance Technology

Valvoline is using advanced analytics and proprietary software to predict service needs, reducing breakdowns and boosting preventive visits; pilot programs in 2024 showed a 15% increase in return visits and a 9% lift in per-customer spend.

This high-growth tech acts as a Stars BCG asset: it strengthens loyalty, drives share of annual vehicle spend, and targets a TAM of ~$55B US quick-lube/maintenance market (2024 estimate).

Ongoing R&D spend—Valvoline increased digital R&D by ~30% in 2024—must continue to outpace traditional competitors lacking data platforms to retain advantage.

- 15% increase in return visits (pilot 2024)

- 9% higher per-customer spend (pilot 2024)

- ~$55B US TAM for quick-lube/maintenance (2024)

- 30% rise in digital R&D spend (2024)

Premium Synthetic Upgrades

Premium Synthetic Upgrades sit in the BCG Matrix as a Star: full synthetic oil change demand grew ~6.8% CAGR 2019–2024, driven by tighter engine tolerances and OEM recommendations, and Valvoline’s upsell from conventional to synthetic lifts average ticket by ~28% to ~$95 per service (2024 internal retail data), creating a high-growth, high-share revenue stream.

- Market CAGR 2019–2024: 6.8%

- Valvoline upsell increases ticket ~28% to ~$95 (2024)

- Higher margin per service, premium positioning

- Supports growth and competitive differentiation

Valvoline: Fast 2024 growth—~1,900 stores, $220M capex, EV +14% & higher per-visit revenue

Valvoline Stars: rapid store growth (~1,900 stores after +250 net in 2024), $220M capex 2024, EV services (14% VE sales 2024) with 30% higher per-visit revenue, fleet ~$300M FY2024, digital pilots: +15% returns, +9% spend; premium synthetic upsell +28 to ~$95.

| Metric | 2024 |

|---|---|

| Stores | ~1,900 |

| Capex | $220M |

| EV share | 14% |

| Fleet rev | $300M |

| Return lift | +15% |

What is included in the product

Comprehensive BCG Matrix review of Valvoline’s portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Valvoline BCG Matrix placing each segment in a quadrant for quick strategic clarity

Cash Cows

Core Oil Change Services

The 15-minute oil change is Valvoline’s cash cow, holding roughly 30% share of the US quick-lube market and generating about $1.2 billion in annual service revenue in 2024.

As a mature line, it needs minimal new marketing spend, delivering steady free cash flow—Valvoline reported $280 million operating cash in FY 2024—used to fund expansion into new regions and cover dividends.

Traditional Franchise Royalties

Valvoline’s franchised network generated about $240 million in royalty revenue in 2024, delivering double-digit gross margins with minimal capital deployment.

These mature partnerships secure stable market share across the U.S. and Europe, supported by >70% brand awareness in core regions and steady same-store royalty growth of ~3% annually.

The cash flow from royalties is reinvested to open company-owned urban stores; in 2024 Valvoline funded 85 new urban locations, prioritizing high-growth metros.

Ancillary Preventive Maintenance

Routine services like tire rotations, air filter replacements, and wiper blade changes are mature offerings with >50% market share across Valvoline’s 1,200+ U.S. service centers and typically carry gross margins near 60% versus ~45% for oil changes.

Because they need no major new equipment and average $12–20 ticket add-ons, these services generate steady incremental cash flow—Valvoline reported $120M in aftermarket service revenue in FY2024—helping cover interest on $400M net debt and fund digital service tech pilots.

Brand Licensing and Intellectual Property

Following the 2023 sale of Valvoline’s Global Products segment (closed Oct 31, 2023), Valvoline keeps steady, low-growth income from licensing its brand; FY2024 licensing revenue estimated at ~$45–55M, high-margin and largely operating profit supporting retail operations.

This leverages decades of brand equity and consumer trust; licensing margins exceed 70%, making revenues effectively pure profit that bolsters cash flow and funds retail reinvestment.

- Post-2023 sale: licensing = recurring revenue

- FY2024 est: $45–55M

- Margins: >70% operating profit

- Role: funds retail ops, improves cash flow

Regional Market Dominance

In mature suburban markets Valvoline often holds leading share—roughly 40–60% in core ZIPs per 2024 internal retail data—so these sites need little defensive spend and sustain high retention and referral rates.

Those fortress locations run near-full capacity with margin on-service revenue ~25% in 2024, producing steady cash flow that cushions downturns versus smaller independents.

- Market share 40–60% (core suburbs, 2024)

- Service margin ~25% (2024)

- High retention, low acquisition cost

- Stabilizes corporate cash flow in recessions

Valvoline’s cash cows: $1.6B+ high‑margin services funding growth, dividends, and debt paydown

Valvoline’s cash cows: 15-minute oil change (~30% US quick-lube share; $1.2B service revenue 2024), franchised royalties ($240M 2024), aftermarket services ($120M 2024; ~60% gross margin), and licensing ($45–55M 2024; >70% margin)—together funding expansion, dividends, and tech pilots while covering $400M net debt.

| Metric | 2024 |

|---|---|

| Oil change rev | $1.2B |

| Royalties | $240M |

| Aftermarket | $120M |

| Licensing | $45–55M |

Preview = Final Product

Valvoline BCG Matrix

The file you're previewing is the exact Valvoline BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document tailored for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Valvoline’s BCG Matrix snapshot highlights product lines across growth and market-share spectrums, showing where engines of profit and areas of risk live; it’s a strategic lens for prioritizing investment and divestment decisions. This preview teases quadrant placement and high-level implications, but the full BCG Matrix provides precise quadrant mapping, data-backed recommendations, and tactical moves tailored to Valvoline’s market dynamics. Purchase the complete report for a Word analysis + Excel summary to present and act on immediately.

Stars

Quick-Lube Service Expansion

Valvoline is rapidly scaling company and franchised quick-lube sites, adding about 250 net new locations in 2024 to reach ~1,900 stores, targeting the $35B US outsourced maintenance market where pro service share rose to 62% in 2024.

These openings are treated as Stars in a BCG matrix: high market growth (~4–5% CAGR) and rising share, supported by ~ $220M capex in 2024 to outfit sites and drive same-store sales gains.

Electric Vehicle (EV) Specialized Services

As EV adoption hits 14% of US light-vehicle sales in 2024 (EPA/EDR), Valvoline’s EV-focused maintenance protocols sit in the Stars quadrant as a high-growth service line targeting cooling and dielectric fluid needs.

These services command a 15–25% premium versus ICE oil changes, with early pilots showing 30% higher per-visit revenue and 12% gross-margin lift in 2024 pilot centers.

By standardizing EV fluid care and launching 400+ dedicated bays in 2025, Valvoline aims to secure dominant market share as first-mover while EV parc grows toward an expected 40% by 2030 (IEA).

Fleet Management Solutions

Fleet Management Solutions sits in Valvoline’s BCG matrix as a star: delivery and ride-share growth drove US commercial vehicle miles +6.2% in 2024, lifting demand for fleet maintenance. Valvoline offers nationwide high share via centralized billing and standardized care across ~1,400 locations, generating estimated fleet revenue of ~$300M in FY2024. Keeping star status needs ongoing tech and sales spend—Valvoline increased fleet CAPEX +18% in 2024 to scale telematics and sales teams.

Predictive Maintenance Technology

Valvoline is using advanced analytics and proprietary software to predict service needs, reducing breakdowns and boosting preventive visits; pilot programs in 2024 showed a 15% increase in return visits and a 9% lift in per-customer spend.

This high-growth tech acts as a Stars BCG asset: it strengthens loyalty, drives share of annual vehicle spend, and targets a TAM of ~$55B US quick-lube/maintenance market (2024 estimate).

Ongoing R&D spend—Valvoline increased digital R&D by ~30% in 2024—must continue to outpace traditional competitors lacking data platforms to retain advantage.

- 15% increase in return visits (pilot 2024)

- 9% higher per-customer spend (pilot 2024)

- ~$55B US TAM for quick-lube/maintenance (2024)

- 30% rise in digital R&D spend (2024)

Premium Synthetic Upgrades

Premium Synthetic Upgrades sit in the BCG Matrix as a Star: full synthetic oil change demand grew ~6.8% CAGR 2019–2024, driven by tighter engine tolerances and OEM recommendations, and Valvoline’s upsell from conventional to synthetic lifts average ticket by ~28% to ~$95 per service (2024 internal retail data), creating a high-growth, high-share revenue stream.

- Market CAGR 2019–2024: 6.8%

- Valvoline upsell increases ticket ~28% to ~$95 (2024)

- Higher margin per service, premium positioning

- Supports growth and competitive differentiation

Valvoline: Fast 2024 growth—~1,900 stores, $220M capex, EV +14% & higher per-visit revenue

Valvoline Stars: rapid store growth (~1,900 stores after +250 net in 2024), $220M capex 2024, EV services (14% VE sales 2024) with 30% higher per-visit revenue, fleet ~$300M FY2024, digital pilots: +15% returns, +9% spend; premium synthetic upsell +28 to ~$95.

| Metric | 2024 |

|---|---|

| Stores | ~1,900 |

| Capex | $220M |

| EV share | 14% |

| Fleet rev | $300M |

| Return lift | +15% |

What is included in the product

Comprehensive BCG Matrix review of Valvoline’s portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Valvoline BCG Matrix placing each segment in a quadrant for quick strategic clarity

Cash Cows

Core Oil Change Services

The 15-minute oil change is Valvoline’s cash cow, holding roughly 30% share of the US quick-lube market and generating about $1.2 billion in annual service revenue in 2024.

As a mature line, it needs minimal new marketing spend, delivering steady free cash flow—Valvoline reported $280 million operating cash in FY 2024—used to fund expansion into new regions and cover dividends.

Traditional Franchise Royalties

Valvoline’s franchised network generated about $240 million in royalty revenue in 2024, delivering double-digit gross margins with minimal capital deployment.

These mature partnerships secure stable market share across the U.S. and Europe, supported by >70% brand awareness in core regions and steady same-store royalty growth of ~3% annually.

The cash flow from royalties is reinvested to open company-owned urban stores; in 2024 Valvoline funded 85 new urban locations, prioritizing high-growth metros.

Ancillary Preventive Maintenance

Routine services like tire rotations, air filter replacements, and wiper blade changes are mature offerings with >50% market share across Valvoline’s 1,200+ U.S. service centers and typically carry gross margins near 60% versus ~45% for oil changes.

Because they need no major new equipment and average $12–20 ticket add-ons, these services generate steady incremental cash flow—Valvoline reported $120M in aftermarket service revenue in FY2024—helping cover interest on $400M net debt and fund digital service tech pilots.

Brand Licensing and Intellectual Property

Following the 2023 sale of Valvoline’s Global Products segment (closed Oct 31, 2023), Valvoline keeps steady, low-growth income from licensing its brand; FY2024 licensing revenue estimated at ~$45–55M, high-margin and largely operating profit supporting retail operations.

This leverages decades of brand equity and consumer trust; licensing margins exceed 70%, making revenues effectively pure profit that bolsters cash flow and funds retail reinvestment.

- Post-2023 sale: licensing = recurring revenue

- FY2024 est: $45–55M

- Margins: >70% operating profit

- Role: funds retail ops, improves cash flow

Regional Market Dominance

In mature suburban markets Valvoline often holds leading share—roughly 40–60% in core ZIPs per 2024 internal retail data—so these sites need little defensive spend and sustain high retention and referral rates.

Those fortress locations run near-full capacity with margin on-service revenue ~25% in 2024, producing steady cash flow that cushions downturns versus smaller independents.

- Market share 40–60% (core suburbs, 2024)

- Service margin ~25% (2024)

- High retention, low acquisition cost

- Stabilizes corporate cash flow in recessions

Valvoline’s cash cows: $1.6B+ high‑margin services funding growth, dividends, and debt paydown

Valvoline’s cash cows: 15-minute oil change (~30% US quick-lube share; $1.2B service revenue 2024), franchised royalties ($240M 2024), aftermarket services ($120M 2024; ~60% gross margin), and licensing ($45–55M 2024; >70% margin)—together funding expansion, dividends, and tech pilots while covering $400M net debt.

| Metric | 2024 |

|---|---|

| Oil change rev | $1.2B |

| Royalties | $240M |

| Aftermarket | $120M |

| Licensing | $45–55M |

Preview = Final Product

Valvoline BCG Matrix

The file you're previewing is the exact Valvoline BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just the fully formatted, analysis-ready document tailored for strategic clarity and professional use.