Varonis Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

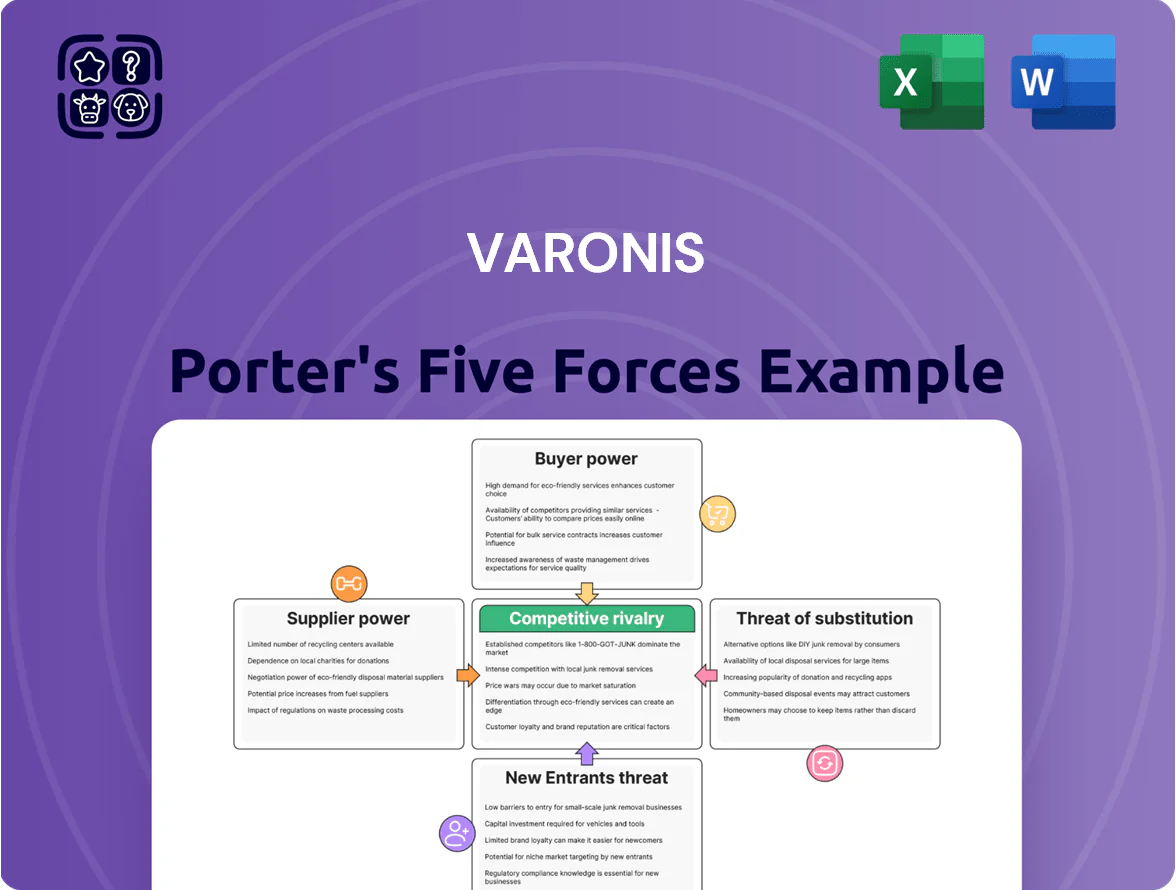

Varonis faces intense competitive rivalry from established cybersecurity firms, moderate supplier leverage due to software-driven delivery, and growing buyer expectations for integrated data-security solutions, while threats from new entrants and substitutes remain manageable but evolving with cloud trends.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Varonis’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Hyperscale Cloud Infrastructure

Varonis's SaaS-first shift makes it heavily reliant on hyperscale clouds—primarily AWS and Microsoft Azure—for real-time data security analytics, with cloud spend representing an estimated 15–25% of cost of revenue in 2024 (company disclosures and industry benchmarks).

Those suppliers hold strong bargaining power because their compute, networking, and regional compliance features are core to Varonis's service delivery and latency-sensitive analytics.

Material price hikes or tighter SLAs—like AWS's 2023 storage repricing moves—could raise Varonis's operating margins or force higher customer pricing, directly affecting FY2025 profitability.

Competition for Specialized Cybersecurity Talent

The market for engineers in data science, behavioral analytics, and cybersecurity remained extremely tight in late 2025, with US unemployment for cybersecurity roles at ~1.8% and a 2024–25 15% year-over-year wage rise for top security engineers. Skilled labor is a primary input for Varonis, so this scarcity raises bargaining power for employees and specialized recruiters, forcing higher hiring premiums.

Reliance on Specialized Third-Party Software Components

Varonis relies on third-party libraries and niche security feeds to boost its data-security platform; while many are commoditized, proprietary integrations (e.g., specialized threat-intel feeds) give vendors moderate bargaining power. Switching such components often needs extensive re-coding and QA—case in point: enterprise software integrations can add 3–6 months to release cycles and raise R&D costs by up to 5% of revenue, increasing operational drag.

Data Center and Hardware Requirements for Hybrid Deployments

Suppliers of high-performance servers and storage keep leverage as enterprises demand hybrid/on-prem gear; global server revenue hit $87.5B in 2024 (IDC), so pricing and lead times matter for Varonis’ hybrid installs.

Semiconductor-driven shortages raised component lead times to 18+ weeks in 2021–22 and still push price volatility; Varonis must secure supply agreements and certified configs to protect SLAs.

- Server market $87.5B (2024)

- Component lead times ≈18+ weeks peak

- Risk: price and availability shocks

- Mitigation: supply contracts, certified HW, buffer inventory

Threat Intelligence and Regulatory Feed Providers

Varonis depends on specialized threat intelligence and regulatory-feed providers for timely global compliance updates and emerging cyberthreat indicators, which feed its automated remediation and alerting; in 2025 threat-intel market revenue hit about $6.8B, concentrating power among top vendors.

These providers hold supplier power because losing real-time, high-fidelity feeds would weaken Varonis’s compliance accuracy and reduce the effectiveness of its data-loss prevention workflows, lowering customer ROI.

Contracts, latency, and feed quality drive switching costs; Varonis mitigates risk via multiple-feed aggregation and partnerships but remains exposed to vendor consolidation—26% of feeds come from three major vendors in recent industry surveys.

Varonis Supplier Risk: Cloud Concentration, Tight Talent, and Hardware Dependencies

Varonis faces moderate–high supplier power: hyperscale clouds (AWS/Azure) drive 15–25% of COGS (2024), threat‑intel market ~$6.8B (2025) with ~26% concentration among top 3, server market $87.5B (2024), and tight cybersecurity labor (≈1.8% unemployment, +15% wages 2024–25); mitigation: multi‑feed aggregation, supply contracts, certified HW.

| Item | Metric |

|---|---|

| Cloud COGS | 15–25% (2024) |

| Threat‑intel | $6.8B (2025) |

| Server market | $87.5B (2024) |

| Cyber unemployment | ~1.8% (2025) |

What is included in the product

Tailored exclusively for Varonis, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats shaping its cybersecurity data-protection market position.

Interactive Porter's Five Forces for Varonis—condenses competitive pressure into a single, editable radar chart so teams can quickly spot threats, test scenarios (e.g., new entrants, regulation), and export clear slides without complex setup.

Customers Bargaining Power

High Switching Costs for Integrated Data Governance

Once Varonis is embedded for data permissions and compliance, its policies, workflows, and audit trails create operational lock-in; migrating a typical enterprise deployment (often >100k permissions rules and multi-year audit logs) can take 6–18 months and cost tens of millions, per vendor migration case studies in 2024. This technical and cost friction raises switching costs, so customers have reduced bargaining leverage at renewal.

Consolidation of Security Budgets within Large Enterprises

Large enterprises are consolidating security budgets—Gartner reported 2024 buyers cut point tools by 22%—which raises buyer leverage to demand bundled pricing and deeper discounts for multi-year contracts.

This gives top customers negotiating power: Varonis faces pressure to offer volume discounts or integration bundles versus $30B+ broad-suite vendors like Microsoft and Palo Alto.

Varonis must quantify ROI: showcase reduced breach costs (average $4.45M per IBM 2023) and time-savings to justify premium over generalist suites.

Availability of Alternative Data Security Posture Management Solutions

The rise of the Data Security Posture Management (DSPM) market has spawned agile startups and expanded offerings from legacy vendors, giving buyers more choices and leverage over Varonis; DSPM venture funding hit about $1.3bn in 2024, fueling competition. Customers can now negotiate on price and features as 35–45% of enterprises pilot multiple DSPM tools in 2024. Increased market transparency lets buyers pit vendors against each other during procurement, pressuring Varonis on feature parity and margins.

Information Transparency and Third-Party Evaluations

Buyers use analyst reports from Gartner and Forrester and peer reviews to compare security vendors; Gartner placed Varonis in its 2024 Market Guide for Data Security Platforms, boosting buyer expectations.

Independent benchmarks and customer reviews force data-driven demands on performance, pricing, and integrations; 68% of enterprise buyers cite third-party validation as decisive (Gartner, 2023).

Varonis must keep high transparency and measurable SLAs to win deals and justify its 2024 revenue growth of 20% year-over-year.

- Gartner/Forrester influence buying decisions

- 68% of enterprises weigh third-party validation

- Peer benchmarks drive pricing and SLA demands

- Varonis’ 20% 2024 revenue growth raises expectations

Impact of Global Economic Conditions on IT Spending

During economic uncertainty, corporate buyers delay large software purchases and add approval layers, raising procurement bargaining power and pressuring Varonis for flexible payment terms; in 2023 US IT spending fell 1.1% to $1.7 trillion, showing tighter budgets.

Varonis must extend sales cycles, offer subscription or usage pricing, and accept smaller upfront fees; extended cycles risk longer cash conversion and higher sales costs—Q4 2024 ARR growth slowed to mid-teens for comparable security vendors.

- More approvals → higher buyer leverage

- Demand for flexible terms, lower upfronts

- Longer sales cycles → higher CAC, slower cash flow

- Offer subscriptions, pilots, phased deployments

Varonis: Deep Deployments Cushion Pricing as DSPM Competition and Buyers Squeeze Terms

Customers have moderate bargaining power: high switching costs from Varonis’ deep deployments (6–18 months, tens of millions) reduce leverage, but consolidated security budgets, DSPM competition (≈$1.3bn VC in 2024) and analyst influence raise price/feature pressure; enterprises demand discounts, SLAs, and flexible terms amid tighter IT spend and longer sales cycles.

| Metric | Value (2023–24) |

|---|---|

| Migration time/cost | 6–18 months; tens of $M |

| DSPM funding | $1.3bn (2024) |

| Enterprises piloting multiple DSPM | 35–45% (2024) |

| Third-party influence | 68% decisive (Gartner 2023) |

| Varonis growth | +20% revenue (2024) |

Full Version Awaits

Varonis Porter's Five Forces Analysis

This preview shows the exact Varonis Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; it’s the full, professionally formatted file ready for download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Varonis faces intense competitive rivalry from established cybersecurity firms, moderate supplier leverage due to software-driven delivery, and growing buyer expectations for integrated data-security solutions, while threats from new entrants and substitutes remain manageable but evolving with cloud trends.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Varonis’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Hyperscale Cloud Infrastructure

Varonis's SaaS-first shift makes it heavily reliant on hyperscale clouds—primarily AWS and Microsoft Azure—for real-time data security analytics, with cloud spend representing an estimated 15–25% of cost of revenue in 2024 (company disclosures and industry benchmarks).

Those suppliers hold strong bargaining power because their compute, networking, and regional compliance features are core to Varonis's service delivery and latency-sensitive analytics.

Material price hikes or tighter SLAs—like AWS's 2023 storage repricing moves—could raise Varonis's operating margins or force higher customer pricing, directly affecting FY2025 profitability.

Competition for Specialized Cybersecurity Talent

The market for engineers in data science, behavioral analytics, and cybersecurity remained extremely tight in late 2025, with US unemployment for cybersecurity roles at ~1.8% and a 2024–25 15% year-over-year wage rise for top security engineers. Skilled labor is a primary input for Varonis, so this scarcity raises bargaining power for employees and specialized recruiters, forcing higher hiring premiums.

Reliance on Specialized Third-Party Software Components

Varonis relies on third-party libraries and niche security feeds to boost its data-security platform; while many are commoditized, proprietary integrations (e.g., specialized threat-intel feeds) give vendors moderate bargaining power. Switching such components often needs extensive re-coding and QA—case in point: enterprise software integrations can add 3–6 months to release cycles and raise R&D costs by up to 5% of revenue, increasing operational drag.

Data Center and Hardware Requirements for Hybrid Deployments

Suppliers of high-performance servers and storage keep leverage as enterprises demand hybrid/on-prem gear; global server revenue hit $87.5B in 2024 (IDC), so pricing and lead times matter for Varonis’ hybrid installs.

Semiconductor-driven shortages raised component lead times to 18+ weeks in 2021–22 and still push price volatility; Varonis must secure supply agreements and certified configs to protect SLAs.

- Server market $87.5B (2024)

- Component lead times ≈18+ weeks peak

- Risk: price and availability shocks

- Mitigation: supply contracts, certified HW, buffer inventory

Threat Intelligence and Regulatory Feed Providers

Varonis depends on specialized threat intelligence and regulatory-feed providers for timely global compliance updates and emerging cyberthreat indicators, which feed its automated remediation and alerting; in 2025 threat-intel market revenue hit about $6.8B, concentrating power among top vendors.

These providers hold supplier power because losing real-time, high-fidelity feeds would weaken Varonis’s compliance accuracy and reduce the effectiveness of its data-loss prevention workflows, lowering customer ROI.

Contracts, latency, and feed quality drive switching costs; Varonis mitigates risk via multiple-feed aggregation and partnerships but remains exposed to vendor consolidation—26% of feeds come from three major vendors in recent industry surveys.

Varonis Supplier Risk: Cloud Concentration, Tight Talent, and Hardware Dependencies

Varonis faces moderate–high supplier power: hyperscale clouds (AWS/Azure) drive 15–25% of COGS (2024), threat‑intel market ~$6.8B (2025) with ~26% concentration among top 3, server market $87.5B (2024), and tight cybersecurity labor (≈1.8% unemployment, +15% wages 2024–25); mitigation: multi‑feed aggregation, supply contracts, certified HW.

| Item | Metric |

|---|---|

| Cloud COGS | 15–25% (2024) |

| Threat‑intel | $6.8B (2025) |

| Server market | $87.5B (2024) |

| Cyber unemployment | ~1.8% (2025) |

What is included in the product

Tailored exclusively for Varonis, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats shaping its cybersecurity data-protection market position.

Interactive Porter's Five Forces for Varonis—condenses competitive pressure into a single, editable radar chart so teams can quickly spot threats, test scenarios (e.g., new entrants, regulation), and export clear slides without complex setup.

Customers Bargaining Power

High Switching Costs for Integrated Data Governance

Once Varonis is embedded for data permissions and compliance, its policies, workflows, and audit trails create operational lock-in; migrating a typical enterprise deployment (often >100k permissions rules and multi-year audit logs) can take 6–18 months and cost tens of millions, per vendor migration case studies in 2024. This technical and cost friction raises switching costs, so customers have reduced bargaining leverage at renewal.

Consolidation of Security Budgets within Large Enterprises

Large enterprises are consolidating security budgets—Gartner reported 2024 buyers cut point tools by 22%—which raises buyer leverage to demand bundled pricing and deeper discounts for multi-year contracts.

This gives top customers negotiating power: Varonis faces pressure to offer volume discounts or integration bundles versus $30B+ broad-suite vendors like Microsoft and Palo Alto.

Varonis must quantify ROI: showcase reduced breach costs (average $4.45M per IBM 2023) and time-savings to justify premium over generalist suites.

Availability of Alternative Data Security Posture Management Solutions

The rise of the Data Security Posture Management (DSPM) market has spawned agile startups and expanded offerings from legacy vendors, giving buyers more choices and leverage over Varonis; DSPM venture funding hit about $1.3bn in 2024, fueling competition. Customers can now negotiate on price and features as 35–45% of enterprises pilot multiple DSPM tools in 2024. Increased market transparency lets buyers pit vendors against each other during procurement, pressuring Varonis on feature parity and margins.

Information Transparency and Third-Party Evaluations

Buyers use analyst reports from Gartner and Forrester and peer reviews to compare security vendors; Gartner placed Varonis in its 2024 Market Guide for Data Security Platforms, boosting buyer expectations.

Independent benchmarks and customer reviews force data-driven demands on performance, pricing, and integrations; 68% of enterprise buyers cite third-party validation as decisive (Gartner, 2023).

Varonis must keep high transparency and measurable SLAs to win deals and justify its 2024 revenue growth of 20% year-over-year.

- Gartner/Forrester influence buying decisions

- 68% of enterprises weigh third-party validation

- Peer benchmarks drive pricing and SLA demands

- Varonis’ 20% 2024 revenue growth raises expectations

Impact of Global Economic Conditions on IT Spending

During economic uncertainty, corporate buyers delay large software purchases and add approval layers, raising procurement bargaining power and pressuring Varonis for flexible payment terms; in 2023 US IT spending fell 1.1% to $1.7 trillion, showing tighter budgets.

Varonis must extend sales cycles, offer subscription or usage pricing, and accept smaller upfront fees; extended cycles risk longer cash conversion and higher sales costs—Q4 2024 ARR growth slowed to mid-teens for comparable security vendors.

- More approvals → higher buyer leverage

- Demand for flexible terms, lower upfronts

- Longer sales cycles → higher CAC, slower cash flow

- Offer subscriptions, pilots, phased deployments

Varonis: Deep Deployments Cushion Pricing as DSPM Competition and Buyers Squeeze Terms

Customers have moderate bargaining power: high switching costs from Varonis’ deep deployments (6–18 months, tens of millions) reduce leverage, but consolidated security budgets, DSPM competition (≈$1.3bn VC in 2024) and analyst influence raise price/feature pressure; enterprises demand discounts, SLAs, and flexible terms amid tighter IT spend and longer sales cycles.

| Metric | Value (2023–24) |

|---|---|

| Migration time/cost | 6–18 months; tens of $M |

| DSPM funding | $1.3bn (2024) |

| Enterprises piloting multiple DSPM | 35–45% (2024) |

| Third-party influence | 68% decisive (Gartner 2023) |

| Varonis growth | +20% revenue (2024) |

Full Version Awaits

Varonis Porter's Five Forces Analysis

This preview shows the exact Varonis Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; it’s the full, professionally formatted file ready for download and use.