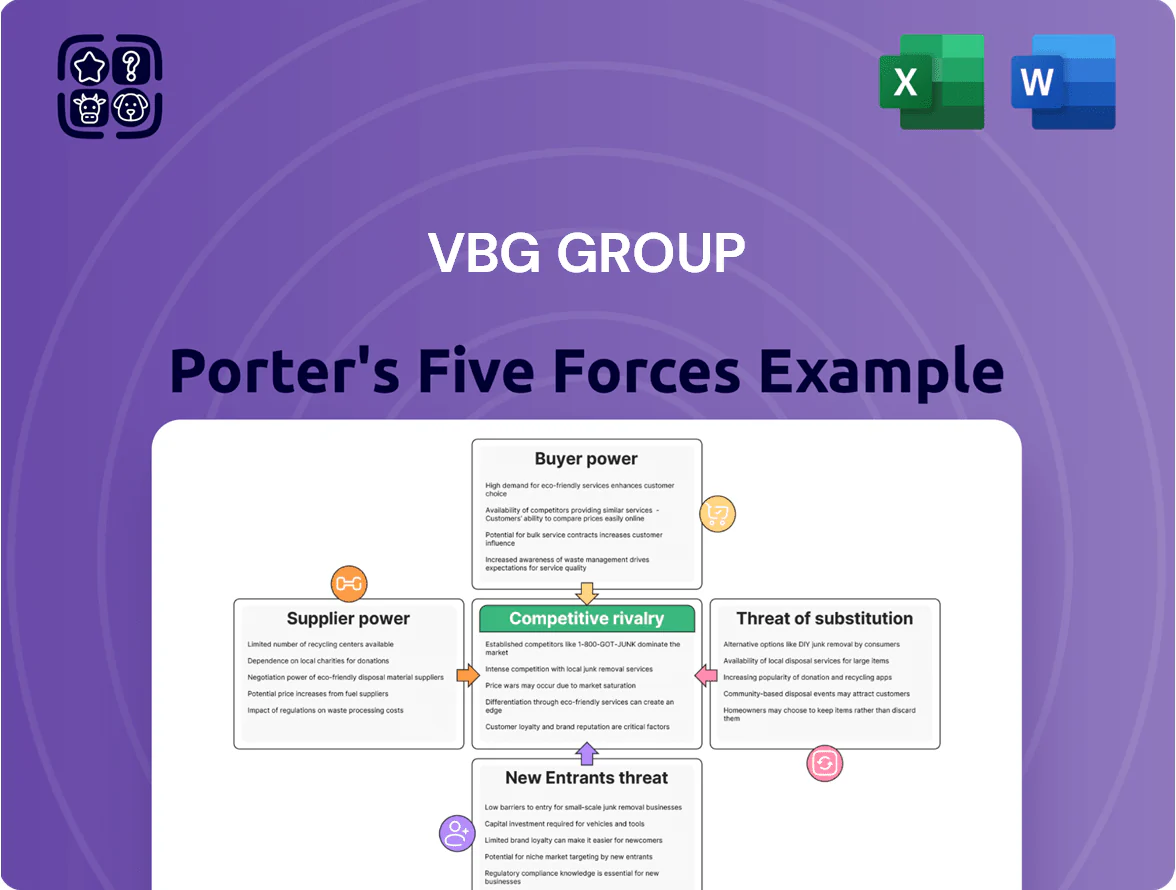

VBG Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VBG Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

VBG Group depends on steel, aluminum and high-strength alloys for couplings and cargo systems, so global metal-price swings directly raise production costs; LME steel and aluminum volatility pushed raw-material spend up ~9% for comparable manufacturers in 2024.

Suppliers pass price rises to OEMs, leaving VBG with limited margin protection unless hedged; typical smelter disruptions in 2024–25 raised premium alloy spreads by ~12%.

By end-2025, geopolitical shifts (Russia sanctions, China export controls) and tighter EU smelting rules increased input-price variance, making raw materials a clear variable-cost risk for VBG.

Specialized component dependency

VBG Group relies on advanced electronic control systems and precision mechanical parts sourced from niche sub-suppliers; global market data shows the top 5 suppliers control ~62% of precision actuator capacity as of 2024. Despite diversified sourcing across 12+ vendors, technical complexity limits qualified vendors to roughly 4–6 per component type, giving specialist suppliers moderate pricing leverage. In 2024 VBG reported 8.3% COGS exposure to high-tech modules, so supplier price moves can shift gross margin by ~0.6–1.2 percentage points.

Energy costs in manufacturing

Suppliers for heavy forging and casting face volatile industrial electricity and gas costs; EU industrial gas prices rose ~45% year-on-year in 2024, pushing Tier 2 input costs up 10–20% for many foundries.

Logistical and supply chain stability

Logistical reliability and container shortages remain key supplier-power levers: global container rates surged 43% in 2021 and spot rates stayed 2–3x pre‑pandemic into 2023, so VBG faces real cost volatility for ocean freight and inland transport.

Suppliers across regions confront different tariffs and road/port quality—for example, 2024 World Bank data shows African ports average 40% longer dwell times than OECD ports—raising lead‑time risk for VBG.

Any raw‑material disruption forces VBG into higher premiums for airfreight or alternate vendors; expedited sourcing can add 20–60% to unit logistics costs based on 2022 industry benchmarks.

- Container rate volatility: +43% (2021 peak)

- Port dwell-time gap: ~40% (Africa vs OECD, 2024)

- Expedited logistics premium: +20–60% (2022 benchmarks)

Supplier concentration in niche materials

For patented materials and specialty high-durability coatings, only a handful of global suppliers exist—industry estimates show fewer than 10 viable providers and price premiums of 15–30% vs. commoditized inputs in 2024.

VBG mitigates this supplier power through multi-year contracts and joint development, securing ~60% of specialty needs under long-term deals, but scarcity still enables suppliers to impose lead-time and price pressure.

Supplier power strong: alloy spreads +12%, top5 control 62%, shocks cut margin 0.6–1.2pp

Supplier power is moderate-high: metal and specialty part concentration, 2024–25 alloy spread +12%, LME-driven raw-material cost rise ~9%, top‑5 precision suppliers = 62% capacity, 60% specialty inputs on long‑term contracts; supplier shocks can swing gross margin ~0.6–1.2 pp and add 20–60% expedited logistics premium.

| Metric | Value (2024–25) |

|---|---|

| Alloy spread change | +12% |

| Raw-material cost move | +9% |

| Top‑5 precision capacity | 62% |

| Specialty on L-T contracts | 60% |

| Expedited logistics premium | 20–60% |

What is included in the product

Uncovers key drivers of competition and buyer/supplier power for VBG Group, identifying entry barriers, substitutes, and disruptive threats that shape pricing, profitability, and strategic positioning.

Compact Porter's Five Forces overview tailored for VBG Group—map supplier, buyer, entrant, substitute, and rivalry pressures on one sheet to speed strategic choices and investor briefings.

Customers Bargaining Power

Concentration of OEM buyers

Large truck makers and OEMs account for roughly 60–70% of VBG Group’s sales, giving them strong bargaining clout because they buy high volumes and can switch among global suppliers.

These customers push for long-term contracts with strict pricing and quality clauses; in 2024 VBG reported a 5% margin squeeze from contract renegotiations with two major OEMs.

Aftermarket fragmentation

The aftermarket for VBG Group is highly fragmented—over 70% of European service points are small workshops, fleet owners, and independent distributors—so individual buyers have low bargaining power.

These customers prioritize availability, brand reputation, and safety over minimal price, with 64% citing parts uptime as top purchase driver in a 2024 industry survey.

VBG leverages strong brand equity and aftersales support to sustain gross margins around 45% in aftermarket channels versus ~30% on direct OEM sales, preserving pricing power.

Switching costs and safety standards

High switching costs deter buyers: replacing VBG Group coupling systems often needs 6–12 months of revalidation, certified testing, and technician retraining, per industry case studies, raising conversion costs by an estimated €50k–€200k per fleet unit.

Demand for integrated digital solutions

Modern fleet managers now demand smart systems reporting coupling status and cargo safety; 2024 telematics adoption hit ~64% in EU fleets, raising expectations for integrated IoT in trailers.

As VBG adds software and IoT, revenue shifts toward service contracts—VBG reported 18% digital-service growth in 2024—raising switching costs and reducing commodity pricing pressure.

That differentiation makes it harder for customers to treat VBG products as simple hardware, improving margin resilience and customer stickiness.

- 64% telematics adoption (EU fleets, 2024)

- VBG digital-service growth 18% (2024)

- Higher switching costs from integrated IoT + SaaS

Price sensitivity in a cyclical industry

The transport and logistics sector is highly cyclical and fuel-sensitive; diesel prices rose ~15% in 2024 vs 2023, and global freight volumes fell 3.4% in H2 2024, raising customer price sensitivity.

In downturns fleets delay renewals and pick lower-cost maintenance, so VBG must balance premium pricing with clients cutting OPEX; a 10% drop in operator capex in 2024 illustrates this risk.

VBG should offer tiered service bundles and financing to protect margins while matching customers’ tighter budgets.

- Diesel +15% (2024 vs 2023)

- Global freight volumes -3.4% H2 2024

- Operator capex down ~10% in 2024

- Recommend tiered pricing + financing

Aftermarket margins and telematics growth offset OEM renegotiation squeeze

Large OEMs (60–70% sales) wield strong price leverage, causing a 5% margin hit in 2024 from renegotiations, while fragmented aftermarket buyers have low individual power; VBG’s 45% aftermarket gross margin vs ~30% OEM preserves pricing. Telematics adoption (64% EU fleets, 2024) and 18% digital-service growth (2024) raise switching costs, offsetting cyclic capex cuts (operator capex −10% in 2024).

| Metric | Value (2024) |

|---|---|

| OEM share of sales | 60–70% |

| Margin squeeze from OEM renegos | −5% |

| Aftermarket gross margin | 45% |

| OEM channel margin | ~30% |

| Telematics adoption (EU) | 64% |

| Digital-service growth | 18% |

| Operator capex change | −10% |

Full Version Awaits

VBG Group Porter's Five Forces Analysis

This preview shows the exact VBG Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the file is fully formatted, professionally written, and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VBG Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

VBG Group depends on steel, aluminum and high-strength alloys for couplings and cargo systems, so global metal-price swings directly raise production costs; LME steel and aluminum volatility pushed raw-material spend up ~9% for comparable manufacturers in 2024.

Suppliers pass price rises to OEMs, leaving VBG with limited margin protection unless hedged; typical smelter disruptions in 2024–25 raised premium alloy spreads by ~12%.

By end-2025, geopolitical shifts (Russia sanctions, China export controls) and tighter EU smelting rules increased input-price variance, making raw materials a clear variable-cost risk for VBG.

Specialized component dependency

VBG Group relies on advanced electronic control systems and precision mechanical parts sourced from niche sub-suppliers; global market data shows the top 5 suppliers control ~62% of precision actuator capacity as of 2024. Despite diversified sourcing across 12+ vendors, technical complexity limits qualified vendors to roughly 4–6 per component type, giving specialist suppliers moderate pricing leverage. In 2024 VBG reported 8.3% COGS exposure to high-tech modules, so supplier price moves can shift gross margin by ~0.6–1.2 percentage points.

Energy costs in manufacturing

Suppliers for heavy forging and casting face volatile industrial electricity and gas costs; EU industrial gas prices rose ~45% year-on-year in 2024, pushing Tier 2 input costs up 10–20% for many foundries.

Logistical and supply chain stability

Logistical reliability and container shortages remain key supplier-power levers: global container rates surged 43% in 2021 and spot rates stayed 2–3x pre‑pandemic into 2023, so VBG faces real cost volatility for ocean freight and inland transport.

Suppliers across regions confront different tariffs and road/port quality—for example, 2024 World Bank data shows African ports average 40% longer dwell times than OECD ports—raising lead‑time risk for VBG.

Any raw‑material disruption forces VBG into higher premiums for airfreight or alternate vendors; expedited sourcing can add 20–60% to unit logistics costs based on 2022 industry benchmarks.

- Container rate volatility: +43% (2021 peak)

- Port dwell-time gap: ~40% (Africa vs OECD, 2024)

- Expedited logistics premium: +20–60% (2022 benchmarks)

Supplier concentration in niche materials

For patented materials and specialty high-durability coatings, only a handful of global suppliers exist—industry estimates show fewer than 10 viable providers and price premiums of 15–30% vs. commoditized inputs in 2024.

VBG mitigates this supplier power through multi-year contracts and joint development, securing ~60% of specialty needs under long-term deals, but scarcity still enables suppliers to impose lead-time and price pressure.

Supplier power strong: alloy spreads +12%, top5 control 62%, shocks cut margin 0.6–1.2pp

Supplier power is moderate-high: metal and specialty part concentration, 2024–25 alloy spread +12%, LME-driven raw-material cost rise ~9%, top‑5 precision suppliers = 62% capacity, 60% specialty inputs on long‑term contracts; supplier shocks can swing gross margin ~0.6–1.2 pp and add 20–60% expedited logistics premium.

| Metric | Value (2024–25) |

|---|---|

| Alloy spread change | +12% |

| Raw-material cost move | +9% |

| Top‑5 precision capacity | 62% |

| Specialty on L-T contracts | 60% |

| Expedited logistics premium | 20–60% |

What is included in the product

Uncovers key drivers of competition and buyer/supplier power for VBG Group, identifying entry barriers, substitutes, and disruptive threats that shape pricing, profitability, and strategic positioning.

Compact Porter's Five Forces overview tailored for VBG Group—map supplier, buyer, entrant, substitute, and rivalry pressures on one sheet to speed strategic choices and investor briefings.

Customers Bargaining Power

Concentration of OEM buyers

Large truck makers and OEMs account for roughly 60–70% of VBG Group’s sales, giving them strong bargaining clout because they buy high volumes and can switch among global suppliers.

These customers push for long-term contracts with strict pricing and quality clauses; in 2024 VBG reported a 5% margin squeeze from contract renegotiations with two major OEMs.

Aftermarket fragmentation

The aftermarket for VBG Group is highly fragmented—over 70% of European service points are small workshops, fleet owners, and independent distributors—so individual buyers have low bargaining power.

These customers prioritize availability, brand reputation, and safety over minimal price, with 64% citing parts uptime as top purchase driver in a 2024 industry survey.

VBG leverages strong brand equity and aftersales support to sustain gross margins around 45% in aftermarket channels versus ~30% on direct OEM sales, preserving pricing power.

Switching costs and safety standards

High switching costs deter buyers: replacing VBG Group coupling systems often needs 6–12 months of revalidation, certified testing, and technician retraining, per industry case studies, raising conversion costs by an estimated €50k–€200k per fleet unit.

Demand for integrated digital solutions

Modern fleet managers now demand smart systems reporting coupling status and cargo safety; 2024 telematics adoption hit ~64% in EU fleets, raising expectations for integrated IoT in trailers.

As VBG adds software and IoT, revenue shifts toward service contracts—VBG reported 18% digital-service growth in 2024—raising switching costs and reducing commodity pricing pressure.

That differentiation makes it harder for customers to treat VBG products as simple hardware, improving margin resilience and customer stickiness.

- 64% telematics adoption (EU fleets, 2024)

- VBG digital-service growth 18% (2024)

- Higher switching costs from integrated IoT + SaaS

Price sensitivity in a cyclical industry

The transport and logistics sector is highly cyclical and fuel-sensitive; diesel prices rose ~15% in 2024 vs 2023, and global freight volumes fell 3.4% in H2 2024, raising customer price sensitivity.

In downturns fleets delay renewals and pick lower-cost maintenance, so VBG must balance premium pricing with clients cutting OPEX; a 10% drop in operator capex in 2024 illustrates this risk.

VBG should offer tiered service bundles and financing to protect margins while matching customers’ tighter budgets.

- Diesel +15% (2024 vs 2023)

- Global freight volumes -3.4% H2 2024

- Operator capex down ~10% in 2024

- Recommend tiered pricing + financing

Aftermarket margins and telematics growth offset OEM renegotiation squeeze

Large OEMs (60–70% sales) wield strong price leverage, causing a 5% margin hit in 2024 from renegotiations, while fragmented aftermarket buyers have low individual power; VBG’s 45% aftermarket gross margin vs ~30% OEM preserves pricing. Telematics adoption (64% EU fleets, 2024) and 18% digital-service growth (2024) raise switching costs, offsetting cyclic capex cuts (operator capex −10% in 2024).

| Metric | Value (2024) |

|---|---|

| OEM share of sales | 60–70% |

| Margin squeeze from OEM renegos | −5% |

| Aftermarket gross margin | 45% |

| OEM channel margin | ~30% |

| Telematics adoption (EU) | 64% |

| Digital-service growth | 18% |

| Operator capex change | −10% |

Full Version Awaits

VBG Group Porter's Five Forces Analysis

This preview shows the exact VBG Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the file is fully formatted, professionally written, and ready for use.