Shilpa Medicare Porter's Five Forces Analysis

From Overview to Strategy Blueprint

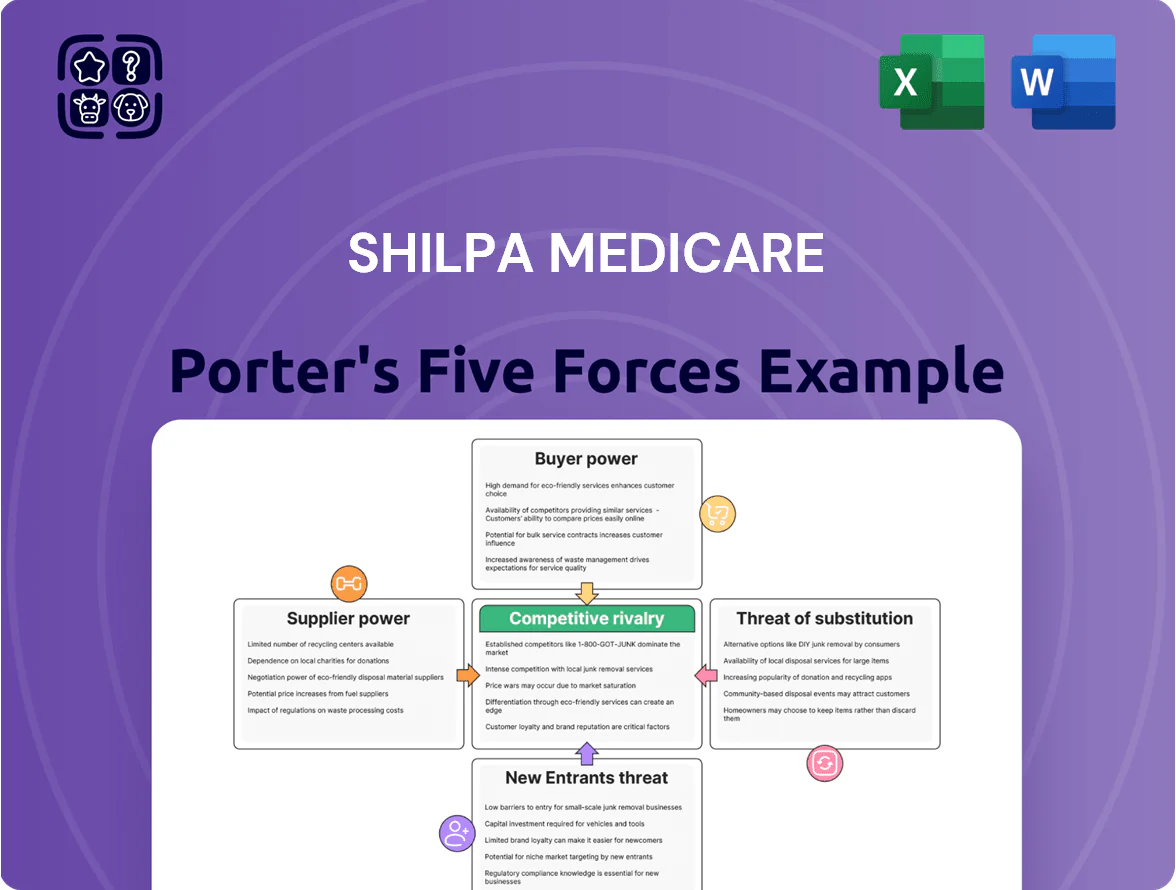

Shilpa Medicare faces moderate supplier power due to specialized raw materials, while buyer power is rising from institutional procurement and price sensitivity in generics.

Barriers to entry are mixed—strong regulatory hurdles but attractive niche opportunities—while rivalry intensifies with domestic peers and MNCs competing on cost and innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shilpa Medicare’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on specialized chemical manufacturers

Shilpa Medicare depends on a small set of specialized chemical suppliers for oncology API intermediates, giving suppliers pricing and lead-time leverage; top three vendors supplied about 68% of raw material volume in 2024.

Strict international purity standards (ICH, EU GMP) limit vendor pool, so price increases of 5–12% in 2023–24 passed through to margins.

By end-2025 Shilpa moved to multi-year contracts covering ~60% of volumes to lock prices and cut stockouts risk amid 18% global specialty chemicals price volatility.

Impact of global supply chain volatility

The cost of raw materials for Shilpa Medicare remains highly sensitive to geopolitical shifts and tighter environmental rules in China and India, where ~65% of key solvents and reagents originate; a 2023 China export control episode pushed solvent prices up 18% month-on-month.

Disruptions in these hubs can trigger immediate price spikes and input shortages; in 2024 pharma-grade reagent lead times stretched from 4 to 10 weeks.

Shilpa Medicare mitigates this by holding higher strategic inventory — management reported working capital inventory days of ~150 in FY2024 versus industry ~110 — buffering short shocks.

Regulatory compliance of raw material sources

Suppliers must follow Good Manufacturing Practices (GMP) to meet US FDA and EMA standards, which narrows Shilpa Medicare’s supplier pool to audited vendors; in 2024 roughly 30–40% of Indian API suppliers held EU/US approvals.

Because suppliers need extensive documentation and regular audits, switching to a lower-cost vendor can take 9–18 months and cost millions in regulatory re-validation and batch comparability studies.

Backward integration into key intermediates

Shilpa Medicare has invested in backward integration, producing key starting materials and intermediates for core oncology and non-oncology drugs, cutting supplier dependence and exposure to raw-material price shocks.

This move lifted gross margins; management reported a 150–200 bps margin improvement in 2024 and reduced COGS volatility versus peers, boosting control across the value chain.

- Reduced supplier risk

- 150–200 bps margin gain (2024)

- Lowered COGS volatility

Concentration of suppliers for niche oncology inputs

Shilpa shrinks supplier power—backward integration + contracts cut volatility, boost margins

Suppliers hold moderate-to-high power: top-3 vendors supplied ~68% of volumes in 2024, specialized inputs from <5 global firms can spike prices 10–25%, and switching takes 9–18 months; Shilpa cut risk via backward integration (150–200bps gross margin lift in 2024), multi-year contracts (~60% volumes by end-2025) and R&D collaborations reducing input volatility 6–12%.

| Metric | Value |

|---|---|

| Top-3 supplier share (2024) | 68% |

| Switch time/cost | 9–18 months, $m re-validation |

| Backward integration impact | 150–200 bps |

| Volatility reduction (R&D) | 6–12% |

What is included in the product

Tailored exclusively for Shilpa Medicare, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic levers affecting its pricing and profitability.

A concise Porter's Five Forces snapshot for Shilpa Medicare—quickly reveals competitive pressure points and strategic levers for pharma decision-making.

Customers Bargaining Power

Concentration of global pharmaceutical buyers

Government led price controls and procurement

In India and parts of Europe, government buyers use essential medicines lists and bulk tenders to cap prices; India’s National List of Essential Medicines influences prices for ~50% of public procurements.

Public tenders favor lowest-cost suppliers, squeezing margins—many generic contracts leave manufacturers with gross margins under 15%.

Shilpa Medicare must split sales between higher-margin private channels and low-margin, high-volume government tenders to sustain revenue and scale.

Low switching costs for commodity generics

For standard, non-complex generic APIs buyers can switch suppliers purely on price, and global generics price competition cut margins—average API contract price declines ~8–12% annually in commoditized segments (2024 industry data). That commoditization raises buyer bargaining power as customers chase lowest cost. Shilpa Medicare reduces this risk by prioritizing complex generics and value-added formulations, where technical specs and regulatory filings raise switching costs and protect margins.

High bargaining power of large hospital chains

- Large buyers: 40–60% infusion share (2024)

- Discount leverage: double-digit off-list prices

- Shilpa tactic: clinical salesforce, 18% oncology sales growth FY2024

Influence of CRAMS clients on pricing

- Client-driven pricing limits margin upside

- Global hub competition lowers acceptable price bands

- Operational efficiency protects ~5–8% EBITDA impact

- IP protection raises switching costs for clients

High export concentration, squeezed margins: oncology up but API prices fall

| Metric | Value |

|---|---|

| Top-5 export share | ~65% |

| Single-customer rev (FY2024) | ~48% |

| Single-customer rev (end-2025) | ~35% |

| Govt procure influence | ~50% |

| API price decline (2024) | 8–12% |

| Oncology sales growth (FY2024) | 18% |

| CRAMS benchmark | $150–200/kg |

Same Document Delivered

Shilpa Medicare Porter's Five Forces Analysis

This preview shows the exact Shilpa Medicare Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Shilpa Medicare faces moderate supplier power due to specialized raw materials, while buyer power is rising from institutional procurement and price sensitivity in generics.

Barriers to entry are mixed—strong regulatory hurdles but attractive niche opportunities—while rivalry intensifies with domestic peers and MNCs competing on cost and innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shilpa Medicare’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on specialized chemical manufacturers

Shilpa Medicare depends on a small set of specialized chemical suppliers for oncology API intermediates, giving suppliers pricing and lead-time leverage; top three vendors supplied about 68% of raw material volume in 2024.

Strict international purity standards (ICH, EU GMP) limit vendor pool, so price increases of 5–12% in 2023–24 passed through to margins.

By end-2025 Shilpa moved to multi-year contracts covering ~60% of volumes to lock prices and cut stockouts risk amid 18% global specialty chemicals price volatility.

Impact of global supply chain volatility

The cost of raw materials for Shilpa Medicare remains highly sensitive to geopolitical shifts and tighter environmental rules in China and India, where ~65% of key solvents and reagents originate; a 2023 China export control episode pushed solvent prices up 18% month-on-month.

Disruptions in these hubs can trigger immediate price spikes and input shortages; in 2024 pharma-grade reagent lead times stretched from 4 to 10 weeks.

Shilpa Medicare mitigates this by holding higher strategic inventory — management reported working capital inventory days of ~150 in FY2024 versus industry ~110 — buffering short shocks.

Regulatory compliance of raw material sources

Suppliers must follow Good Manufacturing Practices (GMP) to meet US FDA and EMA standards, which narrows Shilpa Medicare’s supplier pool to audited vendors; in 2024 roughly 30–40% of Indian API suppliers held EU/US approvals.

Because suppliers need extensive documentation and regular audits, switching to a lower-cost vendor can take 9–18 months and cost millions in regulatory re-validation and batch comparability studies.

Backward integration into key intermediates

Shilpa Medicare has invested in backward integration, producing key starting materials and intermediates for core oncology and non-oncology drugs, cutting supplier dependence and exposure to raw-material price shocks.

This move lifted gross margins; management reported a 150–200 bps margin improvement in 2024 and reduced COGS volatility versus peers, boosting control across the value chain.

- Reduced supplier risk

- 150–200 bps margin gain (2024)

- Lowered COGS volatility

Concentration of suppliers for niche oncology inputs

Shilpa shrinks supplier power—backward integration + contracts cut volatility, boost margins

Suppliers hold moderate-to-high power: top-3 vendors supplied ~68% of volumes in 2024, specialized inputs from <5 global firms can spike prices 10–25%, and switching takes 9–18 months; Shilpa cut risk via backward integration (150–200bps gross margin lift in 2024), multi-year contracts (~60% volumes by end-2025) and R&D collaborations reducing input volatility 6–12%.

| Metric | Value |

|---|---|

| Top-3 supplier share (2024) | 68% |

| Switch time/cost | 9–18 months, $m re-validation |

| Backward integration impact | 150–200 bps |

| Volatility reduction (R&D) | 6–12% |

What is included in the product

Tailored exclusively for Shilpa Medicare, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic levers affecting its pricing and profitability.

A concise Porter's Five Forces snapshot for Shilpa Medicare—quickly reveals competitive pressure points and strategic levers for pharma decision-making.

Customers Bargaining Power

Concentration of global pharmaceutical buyers

Government led price controls and procurement

In India and parts of Europe, government buyers use essential medicines lists and bulk tenders to cap prices; India’s National List of Essential Medicines influences prices for ~50% of public procurements.

Public tenders favor lowest-cost suppliers, squeezing margins—many generic contracts leave manufacturers with gross margins under 15%.

Shilpa Medicare must split sales between higher-margin private channels and low-margin, high-volume government tenders to sustain revenue and scale.

Low switching costs for commodity generics

For standard, non-complex generic APIs buyers can switch suppliers purely on price, and global generics price competition cut margins—average API contract price declines ~8–12% annually in commoditized segments (2024 industry data). That commoditization raises buyer bargaining power as customers chase lowest cost. Shilpa Medicare reduces this risk by prioritizing complex generics and value-added formulations, where technical specs and regulatory filings raise switching costs and protect margins.

High bargaining power of large hospital chains

- Large buyers: 40–60% infusion share (2024)

- Discount leverage: double-digit off-list prices

- Shilpa tactic: clinical salesforce, 18% oncology sales growth FY2024

Influence of CRAMS clients on pricing

- Client-driven pricing limits margin upside

- Global hub competition lowers acceptable price bands

- Operational efficiency protects ~5–8% EBITDA impact

- IP protection raises switching costs for clients

High export concentration, squeezed margins: oncology up but API prices fall

| Metric | Value |

|---|---|

| Top-5 export share | ~65% |

| Single-customer rev (FY2024) | ~48% |

| Single-customer rev (end-2025) | ~35% |

| Govt procure influence | ~50% |

| API price decline (2024) | 8–12% |

| Oncology sales growth (FY2024) | 18% |

| CRAMS benchmark | $150–200/kg |

Same Document Delivered

Shilpa Medicare Porter's Five Forces Analysis

This preview shows the exact Shilpa Medicare Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted and ready to use.