VCREDIT PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping VCREDIT’s trajectory—our concise PESTLE snapshot highlights key external risks and opportunities to inform investment and strategy decisions; purchase the full analysis for a detailed, actionable roadmap you can download and use immediately.

Political factors

Regulatory oversight of fintech

The Chinese government continues tight oversight of micro-lending and fintech to curb systemic risk; since 2020 regulations reduced outstanding peer-to-peer lending by over 95%, pressuring players like VCREDIT to comply.

VCREDIT must navigate evolving directives from the People’s Bank of China and the National Financial Regulatory Administration on capital buffers and leverage ratios—PBOC guidance in 2024 targeted higher capital adequacy and max leverage around 6–8x for nonbank lenders.

Maintaining close ties with state regulators is essential for license retention and continuity, particularly after 2023 enforcement actions that led to license revocations affecting roughly 12% of mid-sized fintechs.

Government focus on common prosperity

Political push for common prosperity has led regulators to cap consumer loan rates and promote inclusive finance, pressuring VCREDIT to balance margins with outreach; e.g., China’s 2023 interest rate guidance and 2024 inclusive-finance targets (aiming to increase lending to underserved by >10%) imply VCREDIT may face ceilinged APRs and should target volume growth—aligning profitability with state goals while keeping default-adjusted yields near current industry averages (~8–12%).

Data sovereignty and security policies

The central government intensified scrutiny in 2024, enforcing data localization for firms processing over $50m annual transactions; VCREDIT must host core customer data domestically and undergo national security reviews that can delay cross-border cloud deployments by 3–6 months.

Support for digital economy transformation

Fintech is prioritized in national digitization plans aiming to raise digital economy share to over 50% of GDP by 2025; VCREDIT leverages this policy tailwind to scale AI and big-data credit scoring.

Political support for AI/big data reduces regulatory friction and unlocks funding; VCREDIT’s automated lending can tap into projected $120bn fintech investment regionally (2024–25).

Geopolitical tensions and funding access

Ongoing US-China trade and tech tensions have lifted risk premia, with global EM bond spreads rising ~120bps in 2024 and IPO exit activity down 18% YoY, which can increase VCREDIT’s cost of offshore capital and damp investor sentiment.

Although VCREDIT is domestic, geopolitical instability reduced cross-border PE/VC deal value to $468bn in 2024, constraining international funding and pressuring domestic liquidity.

Strategic planning must model shifts in cross-border capital flows, potential delisting/scrutiny risks, and tighter foreign-investor regulatory oversight that can raise compliance costs and capital constraints.

- Global EM bond spread +120bps (2024)

- IPO exit activity -18% YoY (2024)

- Cross-border PE/VC deal value $468bn (2024)

VCREDIT pivots to onshore compliance as China tightens fintech caps, data and funding

Tight post-2020 Chinese fintech oversight forces VCREDIT to meet 2024 PBOC/NFRA capital and leverage guidance (6–8x), host >$50m transaction data domestically, and align pricing with common-prosperity caps while leveraging state digitization targets (digital economy >50% GDP by 2025) and ~$120bn regional fintech funding (2024–25); geopolitical strains raised EM spreads +120bps and cut IPO exits −18% (2024), pressuring offshore capital.

| Metric | Value (2024) |

|---|---|

| Leverage cap guidance | 6–8x |

| Data localization threshold | $50m annual tx |

| Digital economy target | >50% GDP by 2025 |

| Regional fintech funding | $120bn (2024–25) |

| EM spread change | +120bps |

| IPO exits YoY | −18% |

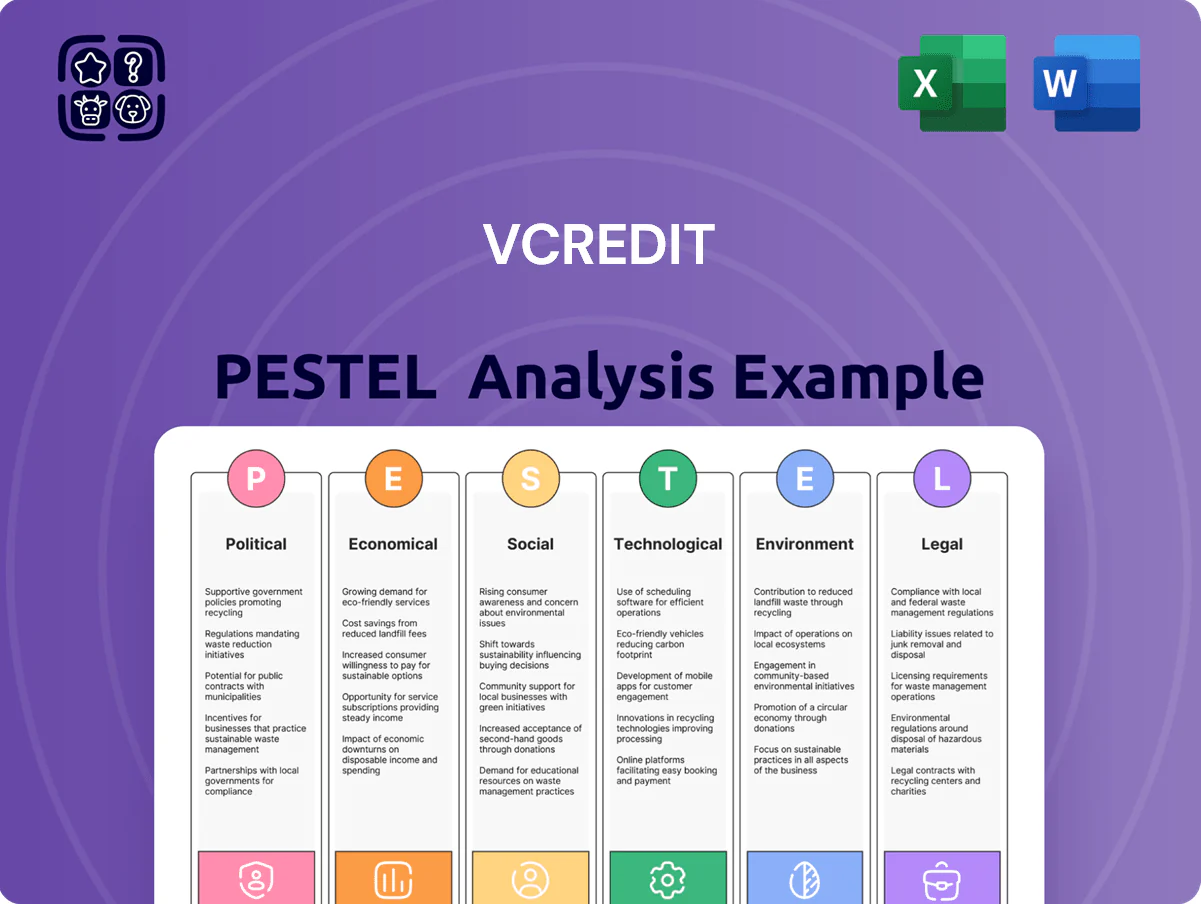

What is included in the product

Explores how external macro-environmental factors uniquely affect VCREDIT across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, investors, and entrepreneurs.

Condenses VCREDIT's full PESTLE into a clear, shareable one-pager that teams can drop into presentations or planning sessions for fast alignment on external risks and market positioning.

Economic factors

Interest rate environment and margins

Fluctuations in central bank benchmark lending rates directly affect VCREDIT's funding costs and loan yields; a 100 bps cut typically reduces asset yields faster than liability costs, squeezing margins. As of late 2025, policy rates stood near 2.25% in the company's key market, a low-rate stance that can compress net interest margins by an estimated 30–80 bps. VCREDIT must optimize its liability mix—short vs long-term, wholesale vs retail—to protect profitability.

Consumer spending and credit demand

The health of China’s economy drives demand for unsecured personal loans on VCREDIT; 2023 GDP growth hit 5.2% and retail sales grew 4.1% y/y in 2024 Jan–Nov, signalling potential volume upside for consumer credit.

Higher GDP and retail sales correlate with increased applications and loan originations; VCREDIT’s growth outlook ties closely to these macro indicators and urban consumption recovery.

Rising consumer confidence—China’s CSI consumer sentiment index up from 85 in 2022 to ~98 in 2024—typically boosts demand across VCREDIT’s short-term and installment loan products.

Inflationary pressures on disposable income

Rising CPI-driven costs for food, energy and housing have eroded real wages; US CPI was 3.4% year-over-year in Dec 2025 and core CPI 3.6%, while median wage growth lagged at ~2.1%, shrinking disposable income and raising default risk for VCREDIT borrowers. If inflation outpaces wages, delinquency rates may climb; monitoring CPI and real wage trends is essential to recalibrate credit-risk models and collection strategies.

Employment market stability

The ability of borrowers to repay loans is closely tied to labor market stability; US unemployment fell to 3.7% in Dec 2025, but sectoral layoffs (tech down 18% YoY in 2024) raise default risk for fintech portfolios.

Economic shifts causing concentrated job losses can spike NPLs; fintech lenders saw NPL ratios rise 1.2–2.0 percentage points in prior shocks.

VCREDIT uses real-time employment data and industry signals to tighten credit for high-risk sectors, reducing exposure and default probability.

- Monitors unemployment & sector layoffs in real time

- Tightens criteria for sectors with rising layoffs (e.g., tech, retail)

- Aims to limit NPL increases observed in past downturns (1–2 ppt)

Capital market liquidity

VCREDIT depends on institutional partners and asset-backed securities; with global liquidity indicators such as the Fed balance sheet down ~10% from 2022 peaks and US high-yield spreads averaging ~5.6% in 2024, tightening raises funding costs and reduces ABS issuance volumes.

Economic volatility can push credit spreads wider—2023–24 saw EM local currency issuance fall ~12%—making capital pricier and access harder for lending platforms like VCREDIT.

Maintaining diversified funding (bank lines, institutional credit, securitizations) mitigates risk; firms with broader mix saw funding drawdowns 30–50% smaller in 2022–24 stress episodes.

- Institutional partners + ABS exposure sensitive to market liquidity

- Fed balance sheet ~10% below 2022 peak; high-yield spreads ~5.6% (2024)

- EM issuance down ~12% (2023–24), ABS issuance contracted in stress periods

- Diversification reduced funding drawdowns by 30–50% in 2022–24

Rates, inflation squeeze real wages as funding stress lifts costs and supports loan demand

Policy rates (2.25% key market, late 2025) and US unemployment (3.7% Dec 2025) drive NIM and default risk; CPI/core CPI ~3.4%/3.6% (Dec 2025) squeeze real wages. China GDP ~5.2% (2023) and 2024 retail sales +4.1% support loan demand; funding stress: Fed balance sheet -10% vs 2022, HY spreads ~5.6% (2024), EM issuance -12% (2023–24) raise funding costs.

| Indicator | Value |

|---|---|

| Policy rate (key market) | 2.25% (late 2025) |

| US unemployment | 3.7% (Dec 2025) |

| CPI / core CPI (US) | 3.4% / 3.6% (Dec 2025) |

| China GDP (2023) | 5.2% |

| China retail sales (2024 Jan–Nov) | +4.1% y/y |

| Fed balance sheet vs 2022 | -10% |

| High-yield spreads | ~5.6% (2024) |

| EM issuance | -12% (2023–24) |

What You See Is What You Get

VCREDIT PESTLE Analysis

The preview shown here is the exact VCREDIT PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are the same final file you’ll be able to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping VCREDIT’s trajectory—our concise PESTLE snapshot highlights key external risks and opportunities to inform investment and strategy decisions; purchase the full analysis for a detailed, actionable roadmap you can download and use immediately.

Political factors

Regulatory oversight of fintech

The Chinese government continues tight oversight of micro-lending and fintech to curb systemic risk; since 2020 regulations reduced outstanding peer-to-peer lending by over 95%, pressuring players like VCREDIT to comply.

VCREDIT must navigate evolving directives from the People’s Bank of China and the National Financial Regulatory Administration on capital buffers and leverage ratios—PBOC guidance in 2024 targeted higher capital adequacy and max leverage around 6–8x for nonbank lenders.

Maintaining close ties with state regulators is essential for license retention and continuity, particularly after 2023 enforcement actions that led to license revocations affecting roughly 12% of mid-sized fintechs.

Government focus on common prosperity

Political push for common prosperity has led regulators to cap consumer loan rates and promote inclusive finance, pressuring VCREDIT to balance margins with outreach; e.g., China’s 2023 interest rate guidance and 2024 inclusive-finance targets (aiming to increase lending to underserved by >10%) imply VCREDIT may face ceilinged APRs and should target volume growth—aligning profitability with state goals while keeping default-adjusted yields near current industry averages (~8–12%).

Data sovereignty and security policies

The central government intensified scrutiny in 2024, enforcing data localization for firms processing over $50m annual transactions; VCREDIT must host core customer data domestically and undergo national security reviews that can delay cross-border cloud deployments by 3–6 months.

Support for digital economy transformation

Fintech is prioritized in national digitization plans aiming to raise digital economy share to over 50% of GDP by 2025; VCREDIT leverages this policy tailwind to scale AI and big-data credit scoring.

Political support for AI/big data reduces regulatory friction and unlocks funding; VCREDIT’s automated lending can tap into projected $120bn fintech investment regionally (2024–25).

Geopolitical tensions and funding access

Ongoing US-China trade and tech tensions have lifted risk premia, with global EM bond spreads rising ~120bps in 2024 and IPO exit activity down 18% YoY, which can increase VCREDIT’s cost of offshore capital and damp investor sentiment.

Although VCREDIT is domestic, geopolitical instability reduced cross-border PE/VC deal value to $468bn in 2024, constraining international funding and pressuring domestic liquidity.

Strategic planning must model shifts in cross-border capital flows, potential delisting/scrutiny risks, and tighter foreign-investor regulatory oversight that can raise compliance costs and capital constraints.

- Global EM bond spread +120bps (2024)

- IPO exit activity -18% YoY (2024)

- Cross-border PE/VC deal value $468bn (2024)

VCREDIT pivots to onshore compliance as China tightens fintech caps, data and funding

Tight post-2020 Chinese fintech oversight forces VCREDIT to meet 2024 PBOC/NFRA capital and leverage guidance (6–8x), host >$50m transaction data domestically, and align pricing with common-prosperity caps while leveraging state digitization targets (digital economy >50% GDP by 2025) and ~$120bn regional fintech funding (2024–25); geopolitical strains raised EM spreads +120bps and cut IPO exits −18% (2024), pressuring offshore capital.

| Metric | Value (2024) |

|---|---|

| Leverage cap guidance | 6–8x |

| Data localization threshold | $50m annual tx |

| Digital economy target | >50% GDP by 2025 |

| Regional fintech funding | $120bn (2024–25) |

| EM spread change | +120bps |

| IPO exits YoY | −18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect VCREDIT across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, investors, and entrepreneurs.

Condenses VCREDIT's full PESTLE into a clear, shareable one-pager that teams can drop into presentations or planning sessions for fast alignment on external risks and market positioning.

Economic factors

Interest rate environment and margins

Fluctuations in central bank benchmark lending rates directly affect VCREDIT's funding costs and loan yields; a 100 bps cut typically reduces asset yields faster than liability costs, squeezing margins. As of late 2025, policy rates stood near 2.25% in the company's key market, a low-rate stance that can compress net interest margins by an estimated 30–80 bps. VCREDIT must optimize its liability mix—short vs long-term, wholesale vs retail—to protect profitability.

Consumer spending and credit demand

The health of China’s economy drives demand for unsecured personal loans on VCREDIT; 2023 GDP growth hit 5.2% and retail sales grew 4.1% y/y in 2024 Jan–Nov, signalling potential volume upside for consumer credit.

Higher GDP and retail sales correlate with increased applications and loan originations; VCREDIT’s growth outlook ties closely to these macro indicators and urban consumption recovery.

Rising consumer confidence—China’s CSI consumer sentiment index up from 85 in 2022 to ~98 in 2024—typically boosts demand across VCREDIT’s short-term and installment loan products.

Inflationary pressures on disposable income

Rising CPI-driven costs for food, energy and housing have eroded real wages; US CPI was 3.4% year-over-year in Dec 2025 and core CPI 3.6%, while median wage growth lagged at ~2.1%, shrinking disposable income and raising default risk for VCREDIT borrowers. If inflation outpaces wages, delinquency rates may climb; monitoring CPI and real wage trends is essential to recalibrate credit-risk models and collection strategies.

Employment market stability

The ability of borrowers to repay loans is closely tied to labor market stability; US unemployment fell to 3.7% in Dec 2025, but sectoral layoffs (tech down 18% YoY in 2024) raise default risk for fintech portfolios.

Economic shifts causing concentrated job losses can spike NPLs; fintech lenders saw NPL ratios rise 1.2–2.0 percentage points in prior shocks.

VCREDIT uses real-time employment data and industry signals to tighten credit for high-risk sectors, reducing exposure and default probability.

- Monitors unemployment & sector layoffs in real time

- Tightens criteria for sectors with rising layoffs (e.g., tech, retail)

- Aims to limit NPL increases observed in past downturns (1–2 ppt)

Capital market liquidity

VCREDIT depends on institutional partners and asset-backed securities; with global liquidity indicators such as the Fed balance sheet down ~10% from 2022 peaks and US high-yield spreads averaging ~5.6% in 2024, tightening raises funding costs and reduces ABS issuance volumes.

Economic volatility can push credit spreads wider—2023–24 saw EM local currency issuance fall ~12%—making capital pricier and access harder for lending platforms like VCREDIT.

Maintaining diversified funding (bank lines, institutional credit, securitizations) mitigates risk; firms with broader mix saw funding drawdowns 30–50% smaller in 2022–24 stress episodes.

- Institutional partners + ABS exposure sensitive to market liquidity

- Fed balance sheet ~10% below 2022 peak; high-yield spreads ~5.6% (2024)

- EM issuance down ~12% (2023–24), ABS issuance contracted in stress periods

- Diversification reduced funding drawdowns by 30–50% in 2022–24

Rates, inflation squeeze real wages as funding stress lifts costs and supports loan demand

Policy rates (2.25% key market, late 2025) and US unemployment (3.7% Dec 2025) drive NIM and default risk; CPI/core CPI ~3.4%/3.6% (Dec 2025) squeeze real wages. China GDP ~5.2% (2023) and 2024 retail sales +4.1% support loan demand; funding stress: Fed balance sheet -10% vs 2022, HY spreads ~5.6% (2024), EM issuance -12% (2023–24) raise funding costs.

| Indicator | Value |

|---|---|

| Policy rate (key market) | 2.25% (late 2025) |

| US unemployment | 3.7% (Dec 2025) |

| CPI / core CPI (US) | 3.4% / 3.6% (Dec 2025) |

| China GDP (2023) | 5.2% |

| China retail sales (2024 Jan–Nov) | +4.1% y/y |

| Fed balance sheet vs 2022 | -10% |

| High-yield spreads | ~5.6% (2024) |

| EM issuance | -12% (2023–24) |

What You See Is What You Get

VCREDIT PESTLE Analysis

The preview shown here is the exact VCREDIT PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are the same final file you’ll be able to download immediately after payment.